Conventional wisdom would have it that one of the important obstacles to surmounting poverty is lack of access to formal banking services. It is assumed that once people are given access to bank accounts, they will manage their finances more efficiently, save more, and also leverage it to raise capital for their self-employment and other entrepreneurial needs.

However, as I have already written here, this may only be a partial interpretation. There is mounting evidence to show that conditional on access to a bank account, the majority of people use their bank accounts sub-optimally, most often as a mere storage for their cash balances. The Economist, which points to a newly released World Bank report (pdf here) on banking services usage across the world, writes,

Even among those saving money, banks have not been able to marginalize the informal sources.

Further, a majority of those with bank accounts did not save.

Loans were mostly drawn for personal consumption than for business purposes.

Purchases of insurance products for health and agriculture is minuscule.

However, as I have already written here, this may only be a partial interpretation. There is mounting evidence to show that conditional on access to a bank account, the majority of people use their bank accounts sub-optimally, most often as a mere storage for their cash balances. The Economist, which points to a newly released World Bank report (pdf here) on banking services usage across the world, writes,

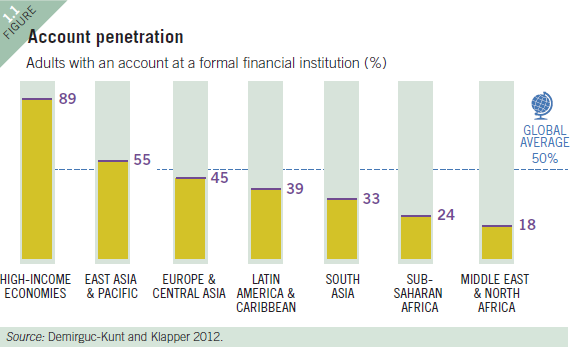

The vast majority of people in developing countries - 88% - say they use banks solely for personal use. The commonest reason for taking out a loan, for example, is to pay for family emergencies (typically someone falling ill). That is followed by school fees, home construction and the expenses of a wedding or funeral. In Africa, 38% of those with bank accounts say they use them to receive remittances from family members abroad. One particularly important reason for having an account in Europe, Central Asia and Latin America is to bank money from the government, either salaries or benefits. In comparison, banks do not seem to be used so much for what seems like a basic purpose: saving money. More than a third (36%) of adults said they had saved some money last year. But only a fifth (22%) said they used a bank or other formal financial institution to do it; 29% saved, but not at a bank (presumably they put the money under the mattress or used it to buy jewellery).A few graphics from the report highlights these findings. Accounts penetration is very low in South Asia.

Even among those saving money, banks have not been able to marginalize the informal sources.

Further, a majority of those with bank accounts did not save.

Loans were mostly drawn for personal consumption than for business purposes.

Purchases of insurance products for health and agriculture is minuscule.

No comments:

Post a Comment