Once indoor temperatures rise above the low-twenties centigrade, or around 75 Fahrenheit, humans start to suffer. Sleep duration and quality fall rapidly when temperatures rise above 23C. Cognitive performance fares similarly, with scores in US high school tests dipping on hot days, and the affected students suffering a lasting impact on their prospects of graduation. The same is true of office workers’ productivity, which peaks at around 21C and rapidly deteriorates as the mercury rises. And that’s all before we get on to mortality, where death rates climb steeply once temperatures hit 30C.

2. Lessons for life from Roger Federer.

In tennis, a small, consistent edge over your opponent can translate into big margins in the long run. Nadal, for instance, also won exactly 54 percent of his points. And when Carlos Alcaraz defeated Jannik Sinner on Sunday in the French Open final — in one of the greatest matches since the 2008 Wimbledon final — Alcaraz, the champion, actually won one fewer point than Sinner. It’s an easy concept to apply to almost any field. In 2022, Ronald van Loon, a portfolio manager at BlackRock, authored a paper on the percentage of investment decisions that need to be correct to beat market benchmarks for returns. He researched markets, crunched the numbers and came up with a number: As low as 53 percent... Federer may have only won 54 percent of his points... but he always seemed to win the points that mattered most.

The three lessons offered by Federer - effortless is a myth; it's only a point; and life is bigger than the court.

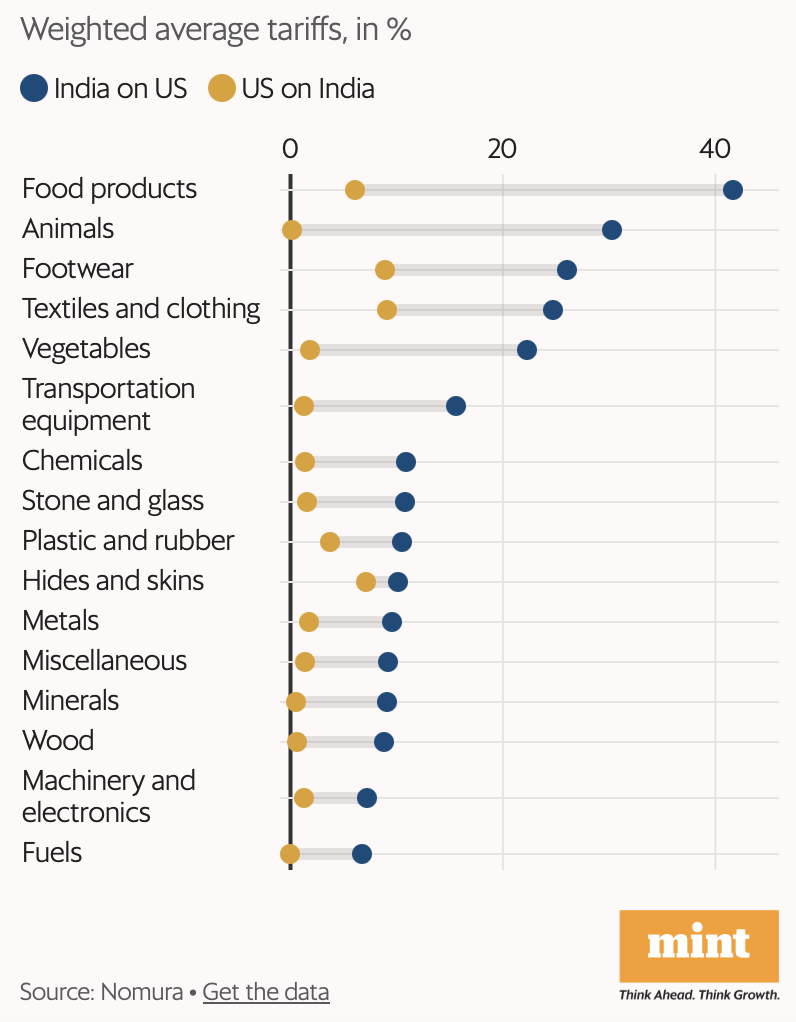

3. The US-Vietnam trade deal depends on how the Trump administration will define "transshipment" which attracts a 40% duty.

Experts say the Trump administration’s definition of transshipment could refer to a range of practices from simply repackaging Chinese goods with a counterfeit “made in Vietnam” label or to using Chinese raw materials in goods manufactured in Vietnam. “The impact may be more limited if these 40 per cent tariffs are enforced solely for the most egregious practices of plain diversion of trade to avoid US tariffs,” said MUFG analyst Michael Wan. “In contrast, if there is a stricter determination of transshipment defined as a certain threshold of foreign value added, the impact . . . may be pronounced.” Given the Trump administration’s interest in isolating China, businesses fear a wider definition. This would be extremely damaging for Vietnam, where many businesses rely on Chinese raw materials and components, and warned that removing them would be impossible.

The Netherlands already has some of the highest electricity costs in western Europe because of the grid bottlenecks... To cover the necessary investment, tariffs are expected to increase each year until 2034 by an average of between 4.3 and 4.7 per cent in real terms, a presentation from national grid operator Tennet said. To free up capacity, Tennet and regional grid operators have started to offer contracts to households that discount electricity used at non-peak times, such as between 11am and 3pm, and other flexible contracts that allow users to pay for electricity in time blocks. From April 1, operators could offer contracts where large industrial users are barred from using their connections at all during certain busy hours in exchange for lower tariffs. The Hague has also put out a “more conscious use of energy” advertising campaign across TV and social media that asks consumers to charge bikes and cars outside of the 4pm-to-9pm peak, when the grid comes under greatest strain...“Everything is going electric and electricity infrastructure needs to grow massively everywhere,” said Jeroen Dijsselbloem, mayor of Eindhoven. The Brainport region around Eindhoven, covering 750,000 people in several municipalities in the southern Netherlands, had lost investment because it had to ration power supply, he said. Brainport is also home to a cluster of advanced technology companies led by ASML, the maker of the world’s most sophisticated chipmaking machines. No significant new grid capacity would be installed in the region until 2027, Tennet figures show. “We need more than 100 medium-size substations and 4,000 small substations,” Dijsselbloem said. Grid operators are also short of 28,000 technicians to install the necessary infrastructure, according to Netbeheer Nederland. Companies such as Thermo Fisher, a US medical business with a base in the Eindhoven area, have maintained their growth plans but invested in on-site battery storage and solar to counter the grid congestion issues.

5. Does the US suffer from Dutch disease?

The US has Dutch disease. Its export is the dollar... The dollar lost roughly 8 per cent of its value over the past six months, which has renewed the old discussion of whether holding the world’s reserve currency is an exorbitant privilege or an exorbitant burden... In 1999, Aaron Tornell, now at UCLA, and Philip Lane, now European Central Bank chief economist, offered a theoretical framework to explain (Dutch Disease). The commodity export changed the budgeting process, they argued. After a windfall, powerful groups will fight to get their hands on any new spending. If the country has strong institutions and social solidarity, this grab for spending will fail. With weak institutions, it will succeed: instead of going to things that increase productivity, such as roads and schools, new spending goes to powerful groups, as unproductive gifts. Tornell and Lane called this the “voracity effect”.They applied it to data from Nigeria, Venezuela and Mexico, but if we accept that the US is not magic, we can easily ask these questions of it, too. How voracious are its powerful groups? How strong are its institutions? The answers in order are: quite, and not as strong as we’d thought. The voracity effect does help explain the gobsmacking audacity of Donald Trump’s so-called “Big Beautiful” Bill, with a cost of $3.4tn over 10 years and the benefits going overwhelmingly to the wealthy. In the past, Republicans have attempted to present tax cuts for the rich as a policy to release productive investment. They’ve even attempted to model this idea as a process called “dynamic scoring”.

6. The balance sheet of six months of Trump tariffs.

Chinese exports to the US fell 9.9 per cent year on year in renminbi terms between January and June... Exports to countries in the Association of Southeast Asian Nations, which the US accuses of transshipment of Chinese exports, rose 14.3 per cent, while imports increased 2.3 per cent in the first half.

7. The Israeli economic miracle

In tech-driven Israel, GDP per head has nearly tripled since 2000 to more than $55,000, rising from 50 to 70 per cent of the level in the US... Its $550bn economy is now among the largest 30 in the world... Total factor productivity, which captures how well labour is using new machines, has grown four times faster in Israel than in other developed economies over the past 25 years... Perhaps the most telling sign of its dynamism is that Israel now spends more than 6 per cent of GDP on research and development — more than any other nation and over double the global average... Since the early 2000s, as most other developed governments have increased spending and debt, Israel has cut state spending from 50 to 40 per cent of GDP, and public debt from a high of 90 per cent to under 70 per cent of GDP. The government also made some smart investments, seeding the venture capital industry that helped to launch the nation’s vaunted tech sector... Spillovers from defence have made Israel a global leader in fields from air-traffic control to, above all, cyber security. With more start-ups per head than any other country, its business culture is closer to that of California than the Middle East. It has 73 start-ups in the hot field of generative artificial intelligence, the third largest in the world. Half of its exports are tech products.

8. Akash Prakash on corporate India

One of the clear takeaways when speaking with senior people working with Apple is their disappointment at the lack of willingness among India Inc to step up and make the investments needed to bring the Apple ecosystem into India. While China is putting up obstacles, the profit focus of Indian entrepreneurs is also a stumbling block. Whether it is putting up the component supply chain or making large capital investments for display units, there is a lack of interest on the part of large Indian groups to commit capital. They cite the low margins on offer and the intense scrutiny that Apple demands on quality and scale. In effect, it would take years of sustained effort to earn a reasonable return on capital — if at all. Is it worth it? Many believe they would be derated by their shareholders, who would not accept the initial losses and question the ultimate return on capital. With a drop in margins will come pressure on valuations and market capitalisation — this is the common belief among Indian industrialists. Indian markets are hyper-focussed on profitability and return on capital.

9. FT long read on BYD, China's battery and EV champion.

Until recently, the main advantage Chinese EV manufacturers had over Tesla was that their products were significantly cheaper. But in February, BYD’s founder Wang Chuanfu stood on stage in Shenzhen and unveiled “God’s Eye”, an advanced driver-assistance system that is a precursor to fully autonomous vehicles. A month later, Lian, who now heads BYD’s automotive engineering research institute, was on stage with Wang to announce a new battery charging system capable of adding a driving range of about 470km in five minutes — a fraction of the time it would take a Tesla to charge to that level. The startling technological advances made by BYD and others have sparked panic among legacy carmakers, who have responded by partnering with Chinese rivals to learn how to build vehicles faster and cheaper, and with better software.

Now that the linkage is established, the Chinese will use the rare earths instrument to combat both tariffs and export restrictions.

This is a good article about how Nvidia's Jensen Huang charmed Trump and convinced him to lift the ban on the export of its powerful H20 chips. One more example of how corporate America's commercial interests have trumped America's national interests. It also underlines the point that President Trump has no deep interest in containing China.

11. As Donald Trump warms up to Ukraine, even suggesting that the US could supply missiles to Ukraine if it could target sites deep inside Russia, including Moscow, Janan Ganesh makes some very important points about Donald Trump.

Trump and Maga are no longer the same thing. His movement — the intellectuals, the donors, the more online of the grassroots — have intense beliefs. Besides a life-long conviction that running a current account deficit with another nation constitutes “losing”, he doesn’t. None of this is fatal to Trump himself. He papers over the differences with force of charisma, electoral success and the dutiful enactment of key Maga priorities. This will protect him from serious internal dissent... Still, we can now see what the future of the US right looks like. Unless the Republicans find another version of Trump — someone whose star power overwhelms all philosophical reservations about him or her — the next leader will have to be more in tune with the movement. That is, more Christianist, more nationalist, more paranoid. An extreme right-winger can put up with half a loaf under Trump because he provides so much else in dazzle and tribal leadership. You aren’t getting that with JD Vance. Ideological and even personal litmus tests, which have been waived for Trump, could return. In other words, we have to entertain the notion that Trump is a moderating influence on a movement that will become much more doctrinal once he is gone. He approaches the world through personal relations, which are malleable, not ideas, which aren’t.Consider Ukraine policy. In all likelihood, Trump has been soft on Putin because he appreciates the Russian’s well-aimed flattery and resents the cost to the US of protecting Europe from him. This is bad, but it isn’t dogmatic. Much of Maga, in contrast, backs Putin out of a belief that Russia is nothing less than Christendom’s frontline, whether against Islam or secular Chinese communism or the woke enemy within. Because it is practical, Trump’s position can be shaken, as seems to be happening now... There are worse things than a personality cult, such as an ideas cult. For a decade, conservatism has been whatever Trump says it is. He has made it possible to regard China as the threat of the century but admire Viktor Orbán, who is China’s biggest friend in Europe; to oppose vaccines but not the president who oversaw the Covid vaccine; to view Ukraine as another region’s problem but Iran as a core US interest. This is an intellectual farrago, but it might be preferable to hard, consistent doctrine... Trump doesn’t share the movement’s interest in the fate of “western civilisation” and other grandiose abstractions. He is not much of a China hawk: his concern is the bilateral trade data, not the grand strategy, much less the contest of values. As for religion, we can’t know another person’s inner life, but come on.

12. China is staring at zero interest rates.

The release of China’s second-quarter growth data this week... real economic expansion was strong and steady at 5.2 per cent but widespread falling prices meant nominal growth was much weaker, at 3.9 per cent... The central bank’s benchmark seven-day reverse repo rate, following a series of gradual cuts, now stands at 1.4 per cent... The yield on China’s 10-year government bond has been hovering around 1.7 per cent, near historic lows, suggesting investor expectations of persistent disinflation... The average interest margin at China’s top six state lenders fell to 1.48 per cent in the first quarter, its lowest level on record, compared with more than 2 per cent in 2021... At most Chinese banks, the interest rate on demand deposits is 0.05 per cent, while one-year term deposits yield less than 2 per cent.

13. Europe's rural depopulation

In the decade to 2024, the estimated number of people living in predominantly rural EU regions fell by nearly 8mn, an 8.3 per cent drop, while the urban population rose by over 10mn, or 6 per cent. Regions making up about 40 per cent of the EU’s land area and containing almost one-third of its population, are experiencing a sustained drop in residents. Dwindling numbers mean shops and bars are forced to close, buses run less frequently, doctors are harder to find, and classrooms become emptier. This fuels further departures, in what the OECD describes as a vicious cycle... Depopulation threatens Europe’s cultural heritage, local languages, cuisines, crafts, farmland, traditions and even national security... Attempts at reversing the trend range from selling houses for €1 to encourage new arrivals to restore them, to subsidising vital services and repurposing civic buildings so they can serve several different functions. Some areas are turning to tourism, encouraging second-home ownership even as some other areas turn against it... the EU’s rural population is forecast to shrink by 18 per cent by 2100, with some areas — including in Bulgaria, Croatia, Portugal and Lithuania — expected to lose one-third of their rural inhabitants or more.

14. China is snapping up mines across the world at record rates.

Chinese companies had become adept at snapping up mining assets from western rivals in recent years, often being willing to take a longer-term view on valuations and invest in riskier jurisdictions... The most active Chinese mining groups in overseas deals include CMOC, MMG and Zijin Mining. Chinese financial institutions have also issued billions in loans for minerals mining and processing projects in the developing world... Chinese companies were positioning themselves to benefit from resource nationalism in nations such as Mali. Some military governments in Africa have sought to take control of western mining assets and are demanding higher royalty payments. Chinese companies are often prepared to accept a less lucrative arrangement if they can take over the running of the asset.

15. As China grapples with overproduction and deflation, President Xi has warned against excessive production in EVs, computing power (data centres), and AI.

“When it comes to projects, there are a few things — artificial intelligence, computing power and new energy vehicles. Do all provinces in the country have to develop industries in these directions?” Xi told the Central Urban Work Conference, a rarely held high-level Communist party meeting on urban development.

Since September 2022, Chinese producer prices have been in a deflationary trajectory.

In articles across state and party media, Chinese President Xi Jinping and other leading officials have attacked what they call neijuan, or “involution”, meaning excessive price competition... Beijing is growing increasingly wary that surging industrial output, coupled with weak consumer demand at home, is fuelling a race to the bottom in prices that is entrenching deflation and fuelling tensions with the country’s biggest trading partners. Official data is expected to show on Wednesday that factory gate price growth remained negative in June for a 33rd consecutive month, one of the country’s longest such falls in decades. Overcapacity is a sensitive issue for China, which has sought to dispel complaints that its industrial policy has flooded its partners’ markets with artificially low-cost goods.

16. Important decision by the University of California's $190 bn endowment fund to completely exit its hedge fund investments.

UC Investments in a meeting on Tuesday approved a plan to reallocate its 10 per cent absolute return portfolio — or its investments in hedge funds — to public equities, finalising a wind-down that began five years ago. Jagdeep Singh Bachher, chief investment officer of UC Investments, one of the largest institutional investors in the US, sharply criticised the industry in a recent meeting for not delivering for clients... He added that UC Investment’s hedge fund positions had undermined its overall performance by introducing risks during market upheavals in 1999, 2008 and 2020. “In each of those three scenarios, hedge funds didn’t hedge us,” he said. “They exposed us to the opposite kind of risk, which actually meant they hurt us.” The move underscores concerns among asset allocators about hedge fund investments that come with unstable returns and high fees that have ballooned in recent years.