1. Very cool data visualization of the respective sizes (nominal) of major world economies. The ball constitutes the world economy and the shares of each country are proportionately distributed, and within each of them the respective shares of manufacturing, services, and agriculture.

3. Japan faces a problem of housing in plenty outside of its largest cities - declining population and vacant houses, with no buyers and owners (more specifically, their children) unwilling to tend for them. "We have too much infrastructure. We can't maintain it all," says Takashi Onishi, an urban planning professor and the president of the Science Council of Japan, as large numbers of towns surrounding Tokyo depopulate.

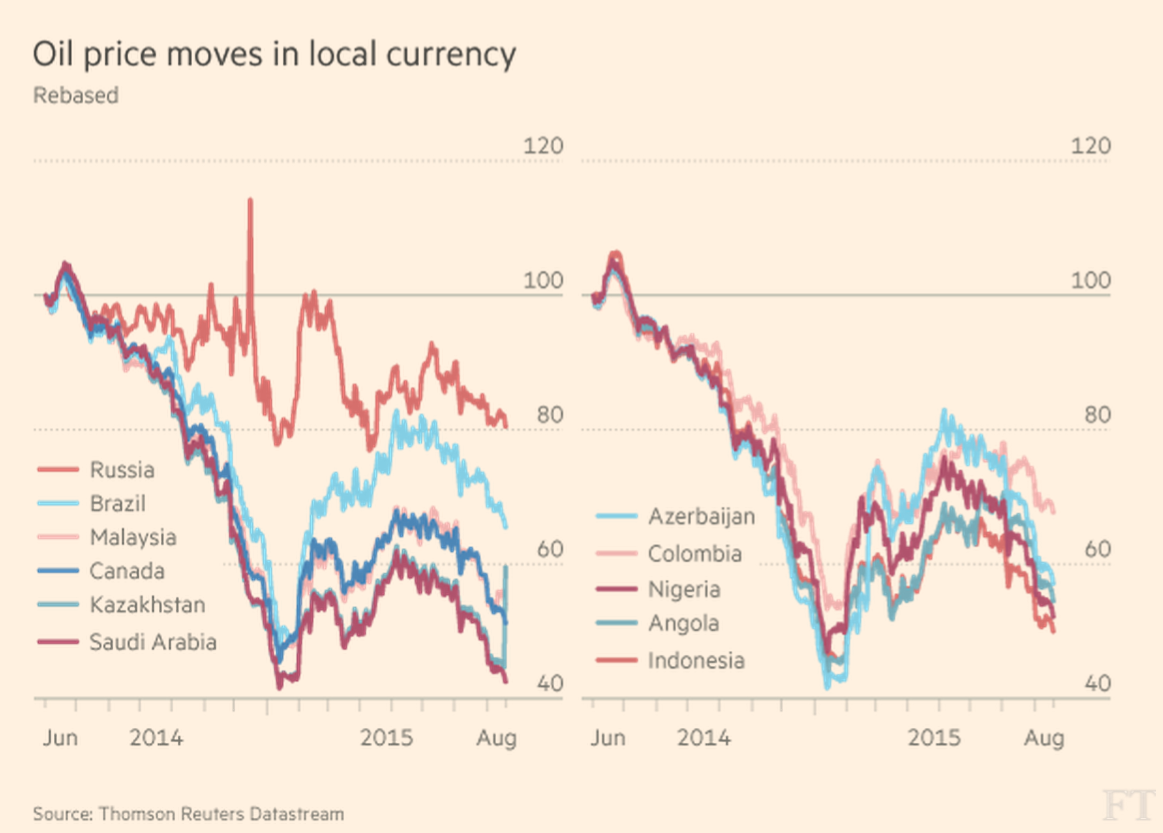

4. FT captures China's importance for the world economy in four graphics,

5. FT has a nice article highlighting the resurgence of conflicts of interest in the large audit firms as their consulting practices race ahead of their staple audit and tax advisory services. While the consulting wing offers everything from legal services and insolvency procedures to capital markets advisory and advise on cyber security, their audit wing offers verification and certification services on the same areas, raising serious conflicts of interests which cannot be mitigated.

Though in 2002 the Sarbanes-Oxley Act prohibited auditors from offering non-audit services, forcing the Big Four to divest their consulting arms, they have found ways since mid-2000s to build back their empires. Now, through aggressive acquisitions, non-audit work makes up about 60% of the Big Four's total global revenues and is the fastest growing and most profitable practice division.

6. Gillian Tett highlights the growing importance (they form more than half all US stock trades) and risks posed by high-frequency trading,

These machines are being programmed to link numerous market segments together into trading strategies. So when computer programs cannot buy or sell assets in one segment of the market, they will rush into another, hunting for liquidity. Since their algorithms are often similar (or created by computer scientists with the same training) this pattern tends to create a “herding” effect. If a circuit breaks in one market segment, it can ripple across the system faster than the human mind can process. This is a world prone to computer stampedes.

On the scale of technology sophistication, sample this from Alvin Roth's new book on market design,

Before 2010, market news between Chicago and New York was transmitted fastest on cables that ran along the rights-of-way of roads and railways. But that year, a company called Spread Networks spent hundreds of millions of dollars to build a high-speed fiber-optic cable that went in a much straighter line and cut round-trip transmission of information and orders from 16 milliseconds to just 13. That 3 millisecond differential basically meant that only traders who used the new cable could make a profit by trading on momentary price differences between Chicago and New York.

7. A crime-infested Mexican slum, Las Palmitas, has sought to graffitize itself out of neglect and despair with bright paints for its houses and public landmarks, as part of a $300,000 federal government crime and violence prevention program,

Las Palmitas, now an abstract and beautiful 20,000 sq metre mural that bursts out of the browny-grey landscape, marks “a new stage in Mexican muralism”... the mural, which covers 209 houses and which used 20,000 litres of paint in 190 colours... Painting houses cheerful colours is only part of the programme to revitalise a community rife with drug and alcohol abuse, violence and scant prospects. Las Palmitas, which had no electricity until about seven years ago and still has no internet access, now has video surveillance cameras. Police officers include the neighbourhood in their rounds; the government is working with residents to help them develop businesses; and high school dropouts now have access to scholarships funded by a major Mexican university... In Las Palmitas, officials say the programme, of which the mega-mural is part, led to a 79 per cent drop in the crime rate in the first half of this year, compared with levels in 2012. They see such grassroots campaigns as vital in a country struggling with rampant drug cartel-related violence and crime.

8. From Martin Sandbu's myth-busting piece in the FT on the Eurozone, this graphic appears to over-turn the conventional wisdom that a sovereign debt default would have devastating consequences and would confine the country to a long period of ostracism.

The graphic shows that both credit worthiness and economic growth improved after the sovereign debt restructuring. The former would reflect the easing of uncertainty after the restructuring.

The graphic shows that both credit worthiness and economic growth improved after the sovereign debt restructuring. The former would reflect the easing of uncertainty after the restructuring.

9. Finally, the age of million dollar parking spots in apartment complexts has arrived! I had written earlier about how a melange of policies, including higher parking charges or scarcer parking slots are necessary to addressing urban traffic problems.

9. Finally, the age of million dollar parking spots in apartment complexts has arrived! I had written earlier about how a melange of policies, including higher parking charges or scarcer parking slots are necessary to addressing urban traffic problems.