1. Scott Galloway is spot on in his assessment of Elon Musk's attempt to takeover Twitter. It's the sixth point that Morgan Housel makes here - people who are abnormally good at one thing are abnormally bad at other things. You can be the greatest entrepreneur but also be a very diminished human being!

2. Staggering numbers on employee attrition rates in Indian software companies,

Attrition has reached an all-time high at both the companies. TCS bled at a rate of 17.4 per cent in the fourth quarter of 2021-22, to compound the 15.3 per cent outgo in the previous quarter. Infosys lost 27.7 percent of its people in the fourth quarter and 25.5 percent in the one before... Offer letters are pouring in, and yet at least 40 percent of those who receive offers choose not to join... Three years ago, TCS would have reached out to maybe 500 institutes for hiring. Now it taps nearly 4,000, thanks to the TCS National Qualifier Test (NQT), whose launch in FY2018-19 was a big part of the company’s revamp of its hiring mechanism... Tata Consultancy Services, India’s largest software exporter, hired 100,000 freshers in the financial year 2021-22, more than in any other year. That means an average of 8,300 trainees joining the company every month.

More Indian software industry facts of the week,

Infosys lost 27% of its employees last quarter. TCS is also above 25%. HCL Tech is up to nearly 22%. Wipro is at nearly 24%... Back in 2010, the average salary for a fresher at a top-tier IT company was around Rs 3-3.5 lakh (~US$4,300-5,000 at that time). In 2021, the average salary for a fresher at a top-tier IT company is around… Rs. 3-3.5 lakh (~US$4,000-4,500)... there is a good reason for fresher salaries in the IT services industry barely rising over a decade: there is more supply than demand. Close to 10-15 lakh engineers graduate every year in India, and a significant portion are not employable... Consequently, companies have continued to hire freshers for more or less the same package for over 10 years. To put this in perspective, the CEO salaries for the top four IT companies have seen over 500 percent increase in compensation during the same period.

Two observations. One, are the big Indian software companies becoming the training ground for India's newly entering software developers, and to that extent are they are generating positive externalities? Second, does the high attrition rates also indicate the largely commodified nature of employees in these companies, and thereby the nature of work being done by them?

3. Sri Lankan inflation scenario is not pleasant

A surge in global oil and gas prices, combined with a 60 per cent drop in the value of the Sri Lankan rupee since last month, has also led to critical shortages of petrol and cooking gas. Sri Lanka’s state oil company, which had previously rationed petrol to conserve its limited stock, last week raised prices by a third to SLRs338 ($1.00) a litre... The lack of fuel has led to long queues, lengthy power cuts and stoked inflation as businesses pass on higher costs to consumers. Sri Lanka’s consumer inflation rate in March of 21.5 per cent was the highest in the Asia-Pacific region... Both private and public transport is becoming unaffordable. The Lanka Private Bus Owners‘ Association has received government approval for a 30 per cent fare increase.

4. Underlining the global food security vulnerabilities, at a time when the Ukraine invasion has already edible oil prices have risen sharply on the back of a ban on palm oil exports by its largest producer Indonesia which has been struggling to keep down food prices as consumption peaks during the Eid feasting season.

5. Excellent FT graphical feature on how the Russian invasion has impacted the global foodgrains supply.

Ukraine accounts for 8 per cent of global wheat exports, 13 per cent of corn flows, and more than one third of the sunflower oil trade. Normally the country exports 40mn to 50mn tonnes of cereals every year, but Russia’s invasion has meant export volumes in March were a quarter of those in February, according to the agriculture ministry... The country accounts for 30 per cent of the world’s supply of sunflower oil, widely used in both industrial and domestic food production, and grows 4 per cent of the world’s wheat... Some countries are particularly reliant on Ukraine for crucial food supplies. In Libya, for example, 44 per cent of the wheat supply used domestically came from Ukraine in 2018. In India, 77 per cent of the domestic supply of sunflower oil came from Ukraine in 2019. In China, it was 63 per cent. Ukraine supplied 43 per cent of the corn used in the UK in 2019, much of it to feed livestock.

The Russians have targeted the entire agriculture production chain in Ukraine and have taken control of many of the Black Sea ports which formed the gateways for Ukrainian exports. The impact on global food prices have been marked.

6. As Emmanuel Macron returns to power, he'll have the challenge of pruning down the French state, the biggest among large economies. Ruchir Sharma shines light at the French state,

Macron had promised to reduce state spending — then a record at more than 56 per cent of gross domestic product — by about 5 percentage points. Instead, under pressure from protests and the pandemic, state spending rose to a staggering 60 per cent of GDP. France’s government spending is 15 points above the average for developed economies. Moreover, that gap is explained less by heavy spending on education, health or housing than on welfare programmes, which at 18 per cent of GDP is nearly double the average for developed economies. France is stuck in a welfare trap, spending generously on income transfers but pushed by voters to spend even more, given discontent with the rising cost of living and with inequality. Despite its strengths, from large-scale manufacturing to luxury goods, France remains at best an average economic competitor. Its growth rate has long hovered at or below the developed world average. And though GDP growth has picked up under Macron, it averaged just 1 per cent a year in his first term, which ranks 13th among the top 20 developed economies over that period. The French state, taxing heavily to fund its spending habits and muscular regulatory arms, is a major reason for this mediocrity. France’s government deficit is 7 per cent of GDP and its public debt is 112 per cent, both among the heaviest burdens of any developed country.

7. For all the talk of embargoes and sanctions on Russia, the west has stepped back from where it really hurts - energy imports. Gillian Tett points to a study by Anette Hosoi and Simon Johnson who highlight that the volume of Russian exports has risen after sanctions,

In fact, the movement of Russian crude by tanker ship was just over 3 million barrels per day in February and March, but more than 4 million barrels per day in the first 17 days of April. Despite the evidence of atrocities in Bucha and elsewhere, and the deliberate targeting of civilians with missile attacks (for example, at Kramatorsk railway station), Western countries remain reluctant to impose sanctions on Russian oil exports, fearing the consequences for fuel prices around the world. Most notably, the EU buys 2.2 million barrels of oil and 1.2 million barrels of petroleum product from Russia every day... Speaking in early April, Josep Borell, the EU High Representative for Common Foreign and Security Policy, pointed out that while the EU had pledged €1 billion to Ukraine for military aid: “€1bn is what we pay Putin every day for the energy he provides us. Since the beginning of the war we have given him €35bn.”

They propose targeting tanker companies and their insurers in London to enforce the sanctions.

The hypocrisy in putting pressure on countries like India to ban import of oil and weapons from Russia is striking given this level of continuing European imports of Russian oil and gas.

8. Brendan Greeley writes that the Fed's balance sheet expansion through Treasuries acquisition was a political choice which led to "returns allocation",

Buying Treasuries, however, was also a political choice. There is some argument, even among central bankers, about how buying trillions of dollars of government debt helps lower unemployment. It might work through the “signal channel”, as a sign to investors that the Fed intends to keep rates low for a while. It might work by driving down returns on 10-year Treasuries and encouraging riskier long-term investments. Or it might work through the “supply channel” — buying a lot of Treasuries lowers the return on Treasuries, encouraging investors to buy anything else. Indeed, that is what it seems to have done. If you held any kind of asset before the pandemic — a stock, a bond, a house, a start-up looking for another round of venture capital funding — the returns over the past two years have been amazing. The good news for the Fed is that buying a lot of Treasuries is not credit allocation. The bad news is that it is return allocation. If you didn’t own an asset, you didn’t get the return. Only half of American families hold stocks and bonds in a retirement account.

9. FT long read on the acute scarcity of rental housing in the western cities. This about Berlin,

Berlin is often held up as a model affordable rental market, with a network of rent control regulations and public housing keeping prices low and tenures secure.

And how financialisation may be worsening affordability,

“Berlin is the new New York: everybody wants to live there,” she says. “And the city never had a co-ordinated land policy in response. Public procurement rules push local government land sales to the highest bidders, often those building the most expensive homes, ignoring the lower bids from not-for-profit associations providing affordable rental housing.” The growing popularity of rental housing to investors is not confined to Berlin. New money flowing into Europe’s rental sector from institutions such as pension funds and insurance companies worldwide increased from $75bn in 2019 to $124bn in 2021; in the US it increased from $193bn to $350bn, according to Real Capital Analytics, a real estate data company. Leilani Farha, a housing campaigner who was UN special rapporteur on the right to adequate housing until 2020, is worried about the social impact of the “financialisation” of housing in this way. She says investment funds are ill suited to owning homes: the need to generate returns for investors must either jack up rents or cut their maintenance costs; either way tenants lose out. In many cases, investors target affordable housing schemes in the US and Europe where people are especially sensitive to price rises. “When you’re a pension fund you’re just looking for a good return,” she says. “Favourable conditions for investors and real estate professionals will not work for tenants.”

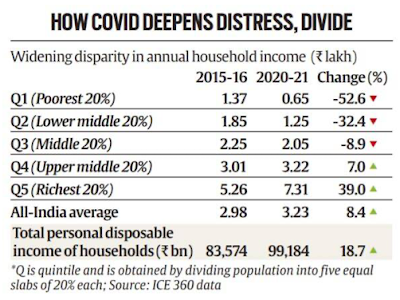

10. Amidst the debate on petrol taxes, The Hindu has a useful graphic