Opinion makers and experts on urban finance in India focus disproportionately on municipal bond issuance and Public Private Partnerships (PPPs). I believe that instead they should prioritise encouraging cities to increase their municipal revenues and also access non-recourse bank debt. Given the very nature of these works and the limited capabilities within local governments, both municipal bonds and PPPs are likely to be marginal contributors compared to other sources for the foreseeable future.

In this context, there have been two very informative recent reports on municipal finance, from the Reserve Bank of India (RBI) and the World Bank (WB). The RBI report shows that in 2019-20 property tax as a share of GDP in India is among the lowest at 0.11% of GDP, with own tax revenues being 0.22%, own revenues (tax and non-tax) being 0.45%. Disturbingly, capital expenditure by cities was just 0.32% of GDP whereas revenue expenditure was 0.58%. Strikingly, own source revenues declined from 84.8% to 64% over 1960-61 to 2019-20, whereas property tax as a share of total revenue receipts declined from 60.9% to 15.5%. See also this from the WB report

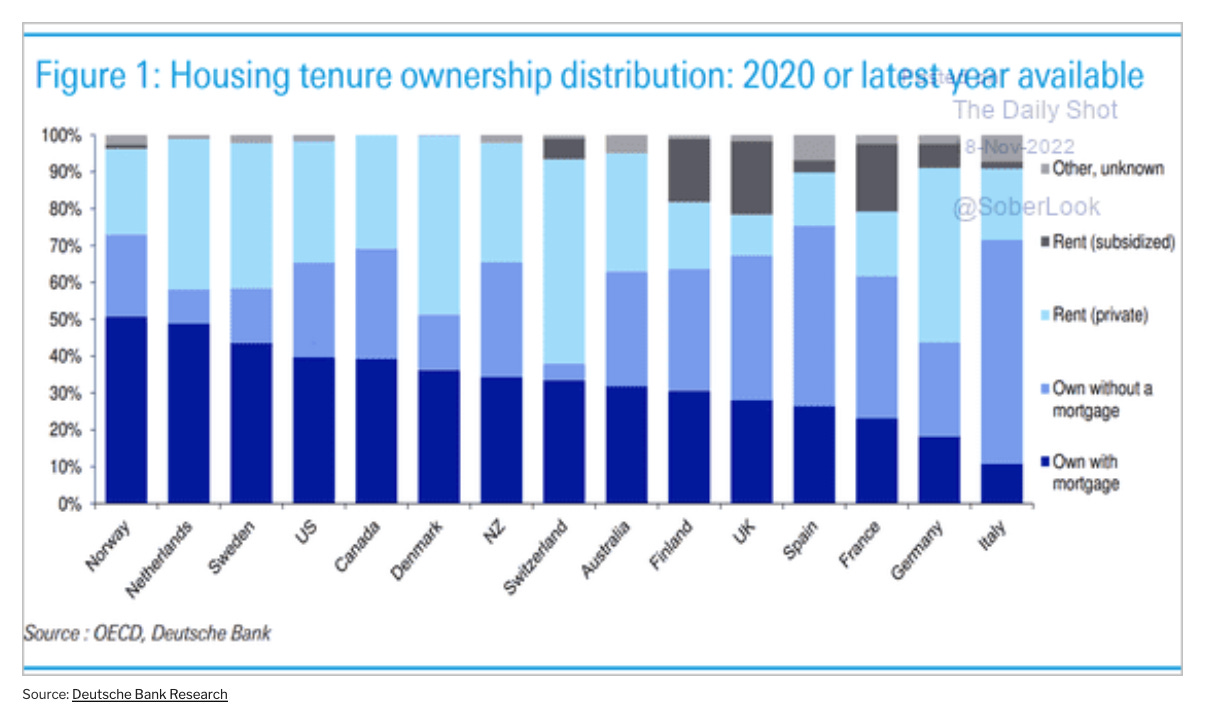

One graphic from the WB report caught my attention.

The RBI report informs that while cities are the engines of national economic growth, contributing 63% of national GDP, ULBs received just 5% of the credit by Scheduled Commercial Banks (SCBs) and gross municipal borrowings was less than 0.05% of GDP. In simple terms, the most important growth driver is the least leveraged and thereby employing capital in a most inefficient manner.

This draws attention to the problem of sorely inadequate commercial debt mobilisation by ULBs. Within commercial debt, as I have written in detail here, the role of capital markets have been marginal outside of US (unique and long historical reasons) and China (where it can be better described as land bonds than municipal bonds). As is the case elsewhere, banks will have to be the predominant source of commercial debt.

It's important that public policy prioritise the removal of barriers that come in the way of ULBs accessing bank debt, and to expand the envelope of municipal projects that can be bank financed. I'll outline a proposal in regard to the latter.

One way to do this is to make the project self-financing and thereby unlock private capital through debt financing. Certain categories of projects can be made financially sustainable or commercially attractive with some bridge financing support. Infrastructure services which generate revenue – mass transit, water and sewerage, solid waste management etc – are good examples. In a rapidly urbanising and chronically infrastructure deficient country, while the demand for these urban infrastructure projects is massive, the available public finance is scarce. Besides, the small volume of municipal finances as aforementioned means that very few of these projects find the light of day.

The Government of India’s (GoI’s) Viability Gap Funding (VGF) scheme already provides bridge grants (of upto 40% of project cost) to PPP projects to make them commercially attractive for private investors. But, as experience from across developed markets show, for a variety of reasons relating to risk appetite of private capital and limited supply-side, a major share of these projects will have to be public managed. The challenge is to ensure its management is efficient.

In the circumstances, it’s proposed that the GoI expand the scope of its existing VGF scheme beyond PPPs to also include public financed revenue generating projects that become bankable once the viability gap is bridged. This can be called the Project Finance Fund for Infrastructure (PFFI).

The Fund should be accessible to all eligible infrastructure projects. Eligibility can be defined in simple terms – projects financed by bank debt or bonds, bridge finance restricted to 40% of the project cost, non-guaranteed by state governments, and repayments to be met only from project revenues. There should not be any other restriction. Essentially, the Fund can be catalytic to crowd-in institutional finance.

The requirement that the debt not be guaranteed should be sufficient to ensure that the proposal is not abused or subverted to push through routine public financed projects.

Accessing the fund should also be easy and simple, so as to allow state and sub-state entities to access it without onerous conditions and administrative hassles. Simplified eligibility requirements and easy accessibility are critical requirements for the success of PFFI (an issue underlined by the failure of VGF scheme). In order to realise synergies and expertise, it can be considered to have the scheme's administration be with any of the existing or newly created development finance institutions (DFIs).

As regards concerns about debt recovery given that a water or solid waste project are non-appropriable public goods, we only need to look at national highway projects, for example, for which bank loans are among the main source of financing. Or the case of weaker section public housing projects where too similar concerns exist. On the issue of asset-liability mismatches (ALM), many projects require loans with only 5-7 years tenor which can be managed by banks. Further, mechanisms like syndicated takeout financing can mitigate ALM risks.

This would help kick-start several bankable urban and other infrastructure projects undertaken by public agencies that are currently unable to attract institutional finance. Institutional finance, like private participation through PPPs, can be a strong efficiency enhancing and sustainability factor in such projects.

The case for restricting VGF to PPPs rests on the premise that private management will bring in discipline and improve operating efficiencies. A comparable discipline and efficiency can be realised by mobilising project finance debt. In fact, project finance model can also help commit governments to maximise project revenues generation, thereby encouraging good practices like higher connection charges, tariffs, user fees etc and ring-fencing of such project revenues.

The PFFI would be a good complement to the GoI’s focus on capital expenditure in general and the national infrastructure pipeline in particular. Further, it would be a welcome stimulus to support state and local governments at a time their revenues are squeezed due to the pandemic. Given that state and local governments make up two-thirds of capital expenditures, any compression in their capital expenditures would adversely impact the economic recovery from the pandemic and also medium-term economic growth prospects.

The Fund’s proposed eligibility requirements contain easily identifiable restrictions which may be sufficient to limit its possible abuse. It can be made explicit that bank financing be limited to project finance, and not state government guarantee or general revenues of the public entity/agency. In order to ensure their skin in the game, the sponsoring public agency can be made to contribute a small minimum percentage of the project cost.

Needless to say, such financing initiatives will have to be complemented with measures to increase revenues - property taxes, non-tax revenues, and utility tariffs. The Government of India could mandate that cities seeking to access PFFI should undertake a well-defined set of reforms relevant to enhancing the commercial viability of the project being financed. The WB report consolidates the well-known list of regulatory and enabling requirements to facilitate project finance like debt mobilisation.

{kind=link}

{kind=link}