A China shock 2.0 is in full play. It is destroying domestic manufacturing bases, upending international trade regimes, and triggering backlashes in advanced and developing countries. In addition to its economic consequences, China’s increasing weaponisation of its manufacturing dominance and the integration of trade and national security policies are alarming its trade partners. With the US decoupling under the policies of Trump 2.0, the frontline for China shock 2.0 is in Europe and Southeast Asia.

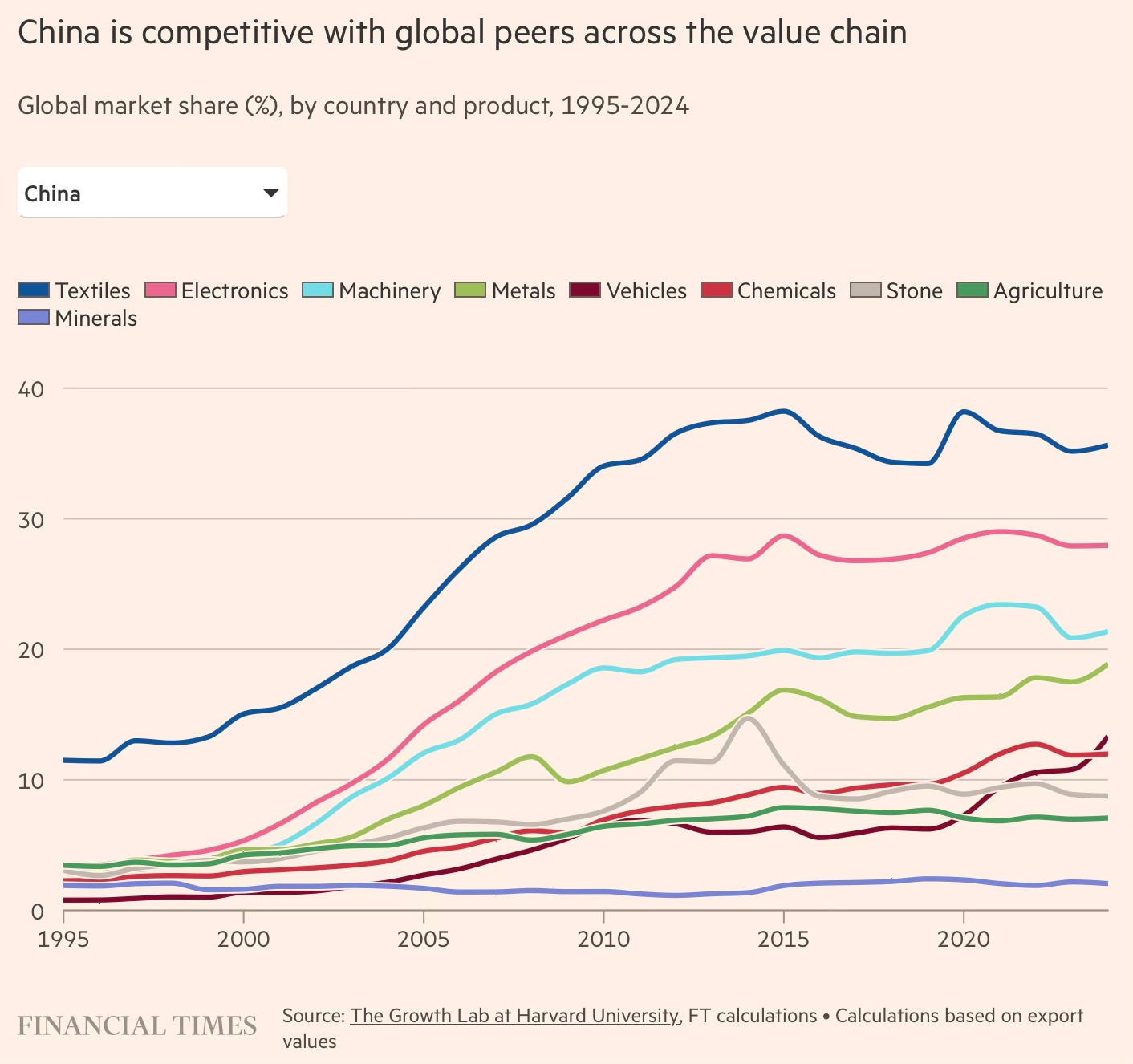

There’s now a clear recognition that the global competitiveness of Chinese manufacturers goes much beyond their manufacturing efficiency. Instead, the former is substantively built on a massive foundation of subsidies, low-interest loans, cheap inputs, and so on. Its scale is such that these anti-competitive practices completely skew the playing field, cannot be matched by anyone else, and therefore cannot be allowed to go unrestricted. The challenge, though, is how to respond given that China holds pretty much all the cards in the manufacturing supply chain, especially all metals and intermediate inputs.

What complicates matters is that the growth strategy being pursued has boxed Beijing itself into a corner. Subsidies, cheap credit and inputs have fuelled a capacity buildup in multiples of the domestic market, leaving export market expansion as the only outlet. Any pullback risks factory closures and job losses, stoking public discontent and worsening matters in a struggling economy. It also risks a cascade of corporate defaults that could imperil the financial system. In these conditions, even efforts to recalibrate the economy towards consumption would be extremely challenging.

This post will examine these issues in greater detail, drawing from an excellent FT series on the second China shock and a new Rhodium Group report on how China came to dominate industrial metals.

1. This is a representative illustration of a story that has been playing out for years in industry after industry.

Huang Xian’s product is about the size of his fist, a sensor that detects electrical current leakage and slots into electric vehicle chargers as a safety guard between the car and the grid. The device is not just a symbol of the innovation and accomplishments of China’s high-tech sector. It also reflects a trend eviscerating high-end manufacturing across the world, to the near despair of governments from Asia to Europe and beyond. The EV boom has propelled Huang’s sensor shipments to a projected 10mn units this year, up from about 20,000 in 2019, when his company Mega-Senway Electronic Technology entered the market. Back then it was still a niche product, supplied by a handful of German and Swiss groups that sold the sensors for roughly Rmb200 (around $30) — or more per unit. Mega-Senway made its first sensors for about Rmb40 each and sold them for Rmb100, leaving Huang with a healthy margin. As Chinese competition poured in, prices started to fall. European groups gradually exited the market. Huang’s Shanghai-based company now sells some sensors for as little as Rmb10 a pop.

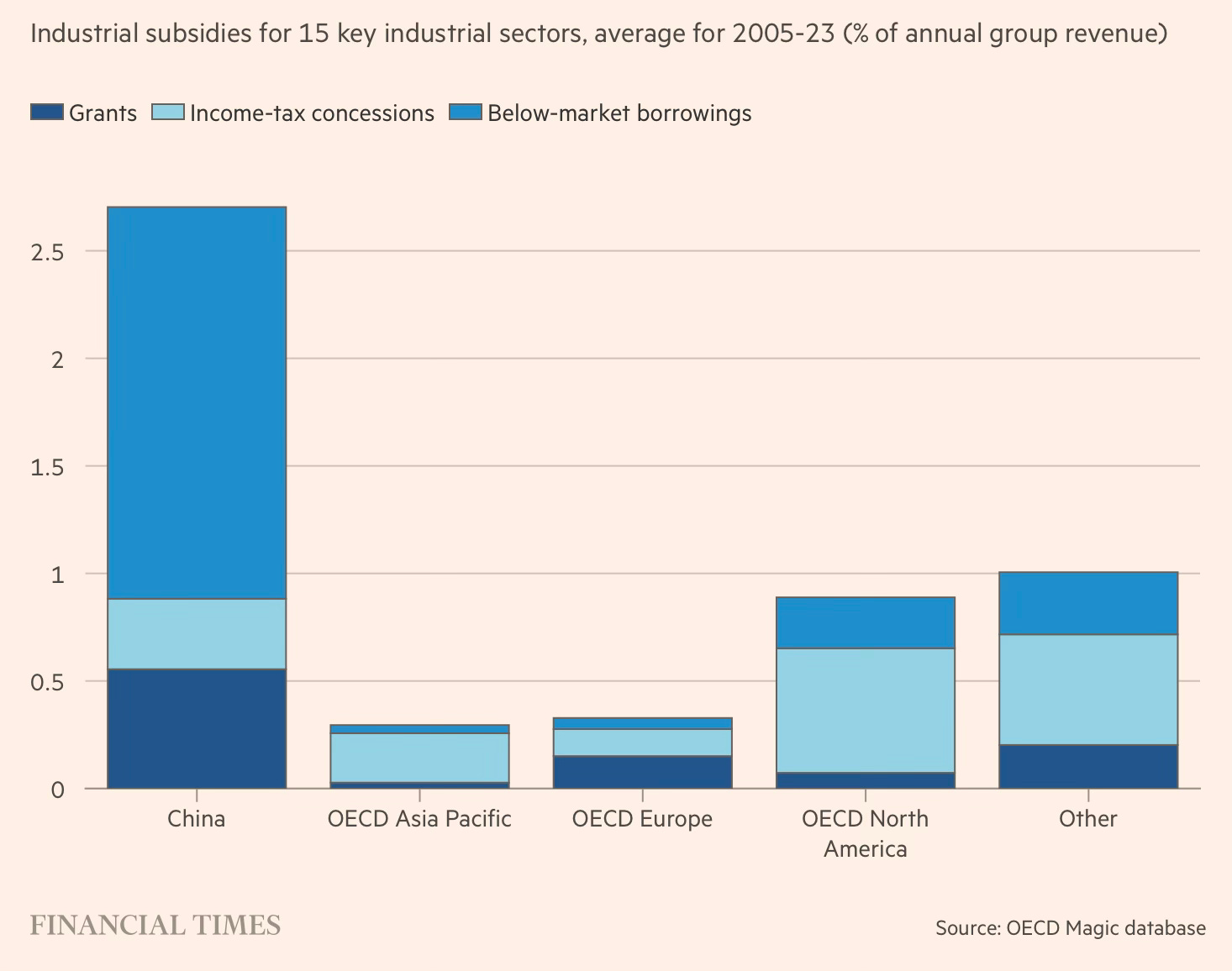

2. The scale of Chinese subsidies is staggering compared to the rest of the world.

Recent OECD analysis underscores the role of subsidies. Company-level analysis of Chinese industry by the 38-member organisation estimates that Chinese businesses are subsidised at between three and nine times the rate of their rich-world counterparts. As well as grants and tax breaks, the OECD data finds that the biggest subsidies come in the form of loans from Chinese state banks offering below-market rates to Chinese companies that undercut international competition.

The role of weak currency in driving the Chinese surpluses should not be underestimated.

Lower inflation relative to Chinese trading partners has led to a real exchange rate devaluation in the past three years, helping boost net exports and the current account surplus, which stood at 3.7 per cent of GDP last year. The IMF estimates the country’s real effective exchange rate — which measures the real value of the currency against a basket of competitors — is undervalued by around 16 per cent, fuelling the competitive advantage enjoyed by Chinese exporters. China has kept exports competitive by buying dollars and depreciating the currency, accumulating “shadow reserves” through a complex web of state-owned banks.

In this context, Michael Pettis makes an important point about China’s global competitiveness.

“Analysts often confuse the global competitiveness of Chinese manufacturing with manufacturing efficiency but these are two very different things. China’s manufacturing competitiveness depends on an undervalued exchange rate, very cheap financing and very low wages relative to productivity.”

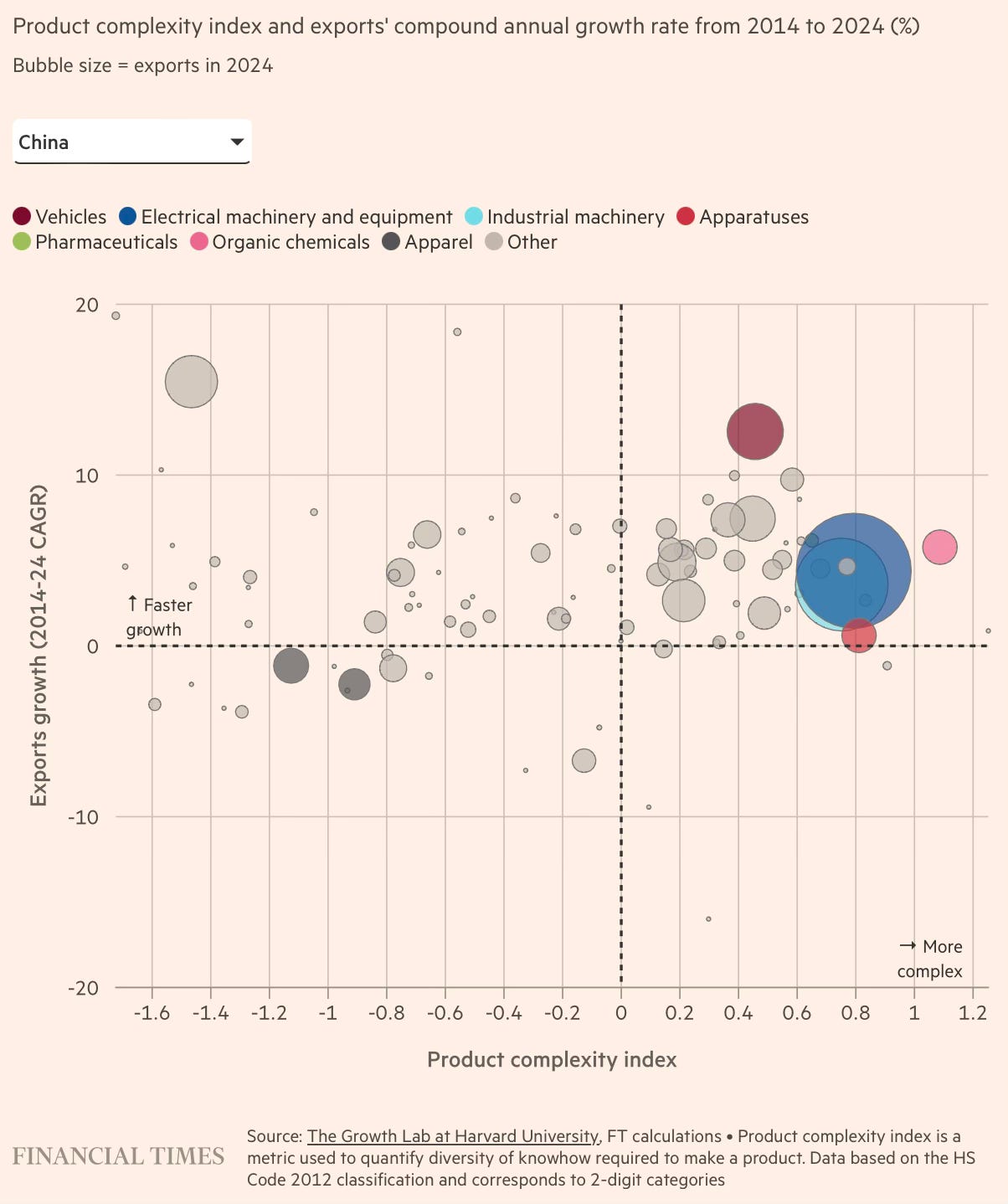

3. The first China Shock, famously documented by David Autor et al as having cost nearly 2 million jobs in the US and having caused significant localised deindustrialisation, covered lower-cost clothes and footwear, consumer electronics, furniture, and appliances. The China Shock 2.0 is about high-end manufacturing, covering products such as solar panels, wind turbines, heavy equipment, electric vehicles, batteries, robots, speciality chemicals, and so on.

While the China Shock 1.0 did cause job losses in the advanced countries, it did not have the same effect as China Shock 2.0 is having since the advanced countries had been vacating the lower-end manufacturing and had been focused on high-end manufacturing, which the China Shock 2.0 threatens to upend.

4. Soumaya Keynes points to some differences between the first and second China Shocks. For one, unlike the first shock when China’s goods export prices rose by about 40% in the 2000-07 period, they were at the same level in 2025 as they were in 2018.

Another important difference is that while during the first shock, China’s imports rose as it bought the manufacturing equipment for its exports, whereas today it makes even these equipment and has not vacated the low-end manufacturing it dominated in its early stages of growth.

5. There are two sides to this phenomenon. On the external front, domestic manufacturers in advanced countries are unable to compete with the flood of cheap, high-quality Chinese-manufactured products. This is causing deindustrialisation and job losses in these countries.

On the domestic front, Chinese manufacturers, both public and private, have entered these industries in large numbers and built up massive manufacturing capacities, far in excess of domestic demand, and are competing fiercely by undercutting each other in remorseless price wars. There are over 125 EV companies and over 150 humanoid robot companies, all benefiting and kept alive by the generous flows of subsidies of all kinds. This phenomenon, described as neijuan, or involution, has resulted in a race to the bottom with steep declines in profitability. Everyone is innovating more and working harder for ever-diminishing returns, and volumes keep rising even as profits are shrinking or negative.

It forces companies like Mega-Senway to move fast. Huang explains how they cut their own costs so dramatically over just a few years. First they acquired the factory that manufactured the sensors they designed. Then he visited nearby factories to study their best practices. A worker testing their finished sensors initially did it one at a time, he says. Huang redesigned the testing jigs to test four at a time, then eight, with a worker constantly loading or unloading batches. Now he has replaced the workers with robotic arms. “We would update our processes two or three times a year,” Huang says. “The pressure came that fast.”

The five-year product cycles with annual price negotiations that the auto industry once ran on have disappeared, he says. One large automaker has cut out all middlemen and puts out tenders each month directly to manufacturers up the supply chain such as Mega-Senway. They submit prices, are told if they are the lowest or not, and submit again — round after round, until no one will go lower. Huang, in turn, has had to bring in more suppliers to pit against each other. “I’m being squeezed, so my only option is to pass my pressure on to them,” he says… Huang says he wishes he could escape the ruthless competition. “We started the company because we loved developing new products,” he says. “Now every year when I’m working through the budget, I’m asking how much can I squeeze out to invest in building something new.”

The phenomenon of involution has been amplified by similarly fierce competition among local governments and provinces.

China has a ream of policies to help companies get off the ground, with local governments in particular battling with each other to offer the best subsidies, cheap land, financing and tax breaks to lure in manufacturers and seed new industries on their turf. The competition between localities can be so great that some businesses move from one place to the next as they chase subsidies and investment. They have become known as “migratory bird enterprises”.

All this creates a self-reinforcing spiral and a bad equilibrium from which breakout is difficult.

Corporate data provider Qichacha lists 1.2mn Chinese companies with “robot” in their name or business scope. Some have recently pivoted from fields like cosmetics, green energy or semiconductors. The founder of a robotics company in western China ticked off the subsidies that have helped him get started: grants to help his customers purchase his robots, subsidies to expand his factory vertically instead of horizontally, money for rooftop solar panels and energy storage and a “smart factory” plaque from the provincial government with more attached benefits. His competitors get the same benefits, he says, acknowledging it may have contributed to the onslaught of new rivals that has forced his prices down 10 per cent over the past year… The system creates more and more companies fighting for the same piece of pie, says Huang He, whose group, Northern Light Venture Capital, is an investor in Mega-Senway. The problems arise when the government money for nurturing companies becomes what sustains them, he says. “Local governments are reluctant to let their local companies fail,” he says. “That’s why overcapacity is so hard to fix.”

The way the Chinese system works, local officials have every incentive to protect their companies. Value added tax generates nearly 40 per cent of China’s tax revenue, and the central government splits the receipts with the localities where products are made, giving them a direct stake in keeping factories running. Adding local production capacity also creates the growth that officials are largely judged on, and any large-scale lay-off could threaten social stability, Beijing’s overriding priority. “Officials are scared of missing their GDP targets. Nobody is scared of overcapacity,” says another founder, who asks to remain unnamed. “As long as you’re manufacturing, there’s VAT revenue. Whether you sell [a product] or make a profit, that doesn’t really affect them.”.. Huang of Mega-Senway suspects some of his competitors are losing money on every sensor they sell and are being sustained by investment from local government funds… The result is that companies which should exit the market keep operating, sustained by government capital, especially China’s politically favoured industries, such as solar, wind, batteries and EVs.

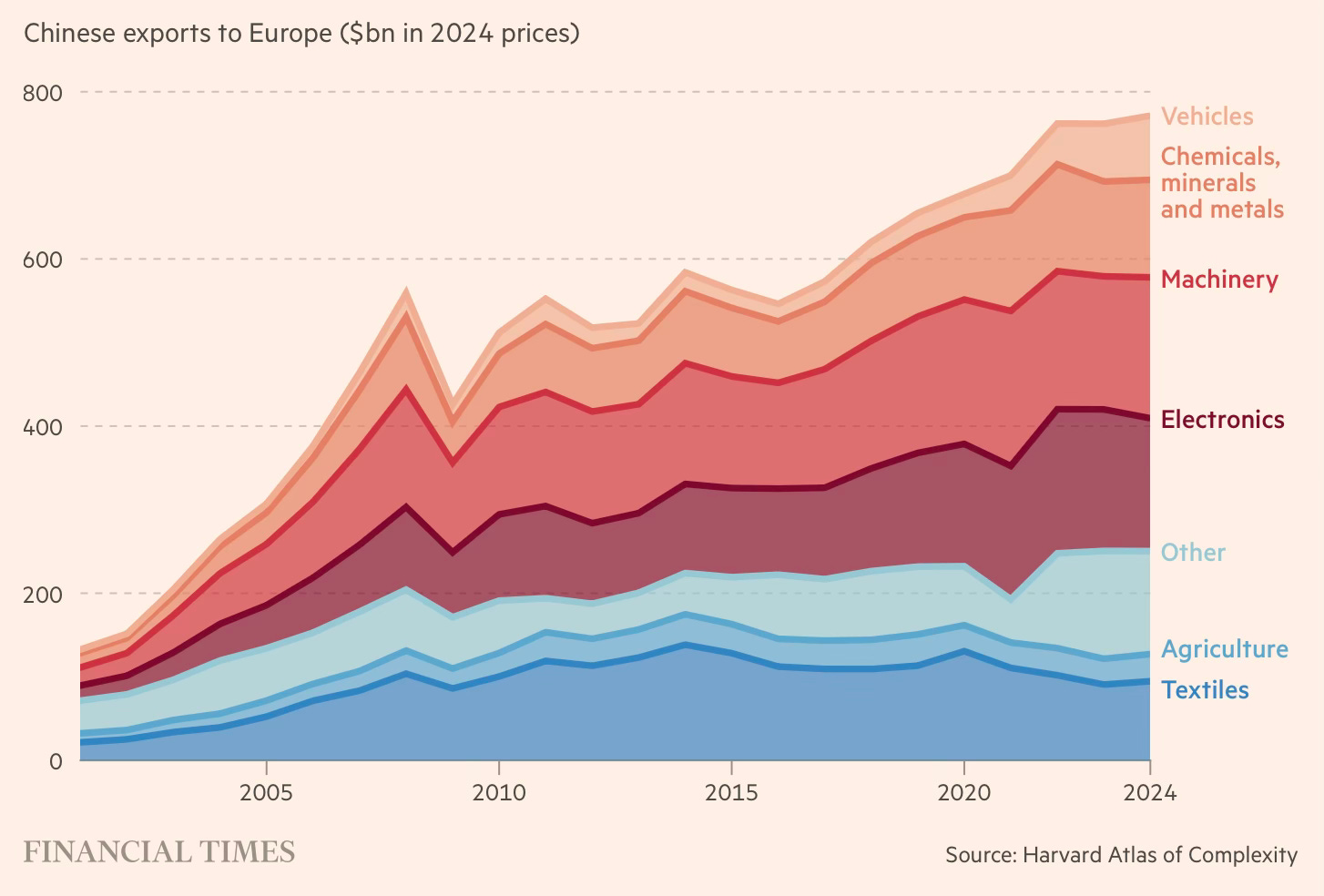

6. The Europeans are emerging as the biggest losers from the China Shock 2.0. Their companies had maintained a competitive advantage in automobile manufacturing, engineering and high-tech manufacturing, which is now being dismantled clinically by Chinese competition. In fact, the surge in Chinese exports in the first three months of 2026 was driven by shipments to the EU by 21.1%, even as those to the US fell. High-tech products have driven the growth in Chinese exports to Europe.

China’s trade policy is also tightly integrated with its national security policy, and nowhere is this more evident than in Europe, where China is trying to establish manufacturing facilities in countries like Hungary, Serbia, and Spain, to diversify supply chains and also gain access to the large EU market.

Xi is explicit about his goal to foster foreign dependence on China’s advanced manufacturing, which Beijing sees as a source of leverage in an era of geopolitical shocks. Salvation for one country can look like the seeds of subjugation to others. The question for Europe is whether it should welcome Chinese investment or repel it… Spanish historian Florentino Portero said: “China’s trade policy is in fact part of its national security strategy. We are seeing how China is taking control of certain companies and integrating them into its own system at our expense.”

In response, taking a leaf out of the playbook that China used so effectively to catch up with the Western manufacturers, the EU recently announced a Made in Europe Bill (the Industrial Accelerator Act, IAA) that mandates Chinese manufacturers to establish facilities to share technology. There is a strong consensus among Europeans that “Europe must be a complete industrial base and not a mere assembly platform”.

The bill lets member states veto any FDI exceeding €100mn in strategic sectors if the investor is from a country with more than 40 per cent of global manufacturing capacity. Those sectors include batteries, EVs, solar panels and the extraction and processing of critical raw materials — all areas where China dominates. To win approval, investment projects must fill at least half of their jobs with EU workers and satisfy three of five other conditions. One is that the investment must be undertaken via a joint venture. Another is that the foreign partner does not own more than 49 per cent of the entity — a condition unpopular with Chinese companies, according to European officials. Other conditions cover the licensing of intellectual property rights, spending 1 per cent of revenue on research and development in the EU, and publishing a strategy for sourcing 30 per cent of inputs from the bloc. The legislation will give companies meeting its requirements access to public funding from the EU, national and regional governments. Without such financial support, Europe’s relatively high labour costs versus China make many industrial investments unviable.

7. Even more than the Europeans, the biggest losers from the China shock 2.0 may be its neighbours in South East Asia, who had been hoping to move up the industrial value chain when China shifts to ever more sophisticated products and services. But, as mentioned earlier, China seems unwilling to vacate any space in the manufacturing landscape. Worse still, its exports are destroying its manufacturing bases.

They are becoming dependent on China for lower-value products, industrial inputs for manufacturing, and also finished goods like EVs and solar panels.

China’s trade surplus with the 11-nation Asean bloc hit a record $276bn in 2025 — up 45 per cent from the year before — with strong growth in intermediate goods, including electronics and capital goods such as machinery used by manufacturers. Labour-intensive manufacturing sectors such as shoes and clothing have been particularly affected. In Indonesia, around 60 factories closed between 2022 and 2025, according to the Indonesian Textile Association… The textile association estimates that 250,000 jobs have been lost in the sector over the past four years… At the other end of the value chain, Chinese exports of EVs, batteries and solar panels to members of the Association of Southeast Asian Nations increased more than 50 per cent last year to nearly $22bn. Vietnam imported $84bn in electrical machinery and electronics from China last year, up 43 per cent, according to the Asia Society Policy Institute (ASPI) think-tank.

This flood of cheap Chinese imports and its impact on domestic manufacturing in terms of factory closures and job losses is already generating backlash in these countries.

Indonesian finance minister Purbaya Yudhi Sadewa said in March that Jakarta was considering measures to curb the growing dominance of Chinese products on the country’s e-commerce platforms. “If this continues without intervention, it would be as if we are handing over our domestic market directly to China,” Purbaya said… Liew Chin Tong, Malaysia’s deputy finance minister, has warned that Asian countries that long relied on the US as their export destination of “first and last resort” now risk crashing each other’s markets, “resulting in cut-throat price wars, involution and deindustrialisation of fellow Asian economies”.

8. There’s little to indicate that even with the rising global backlash at Chinese exports, including among developing countries, Beijing has any intention to change course and focus on domestic consumption. After the property slump and given the reluctance to rebalance towards consumption, manufacturing investments have emerged as the engine for sustaining the 5% growth target. Exports have become a convenient outlet to sustain growth and prevent domestic discontent through factory closures and job losses.

9. The solar industry is a good illustration of all these distortions.

As Chinese factories rushed into solar, production capacity skyrocketed. The country has the ability to manufacture 1,200GW of solar panels annually, roughly double the 647GW installed worldwide last year, according to the China Photovoltaic Industry Association and energy think-tank Ember… local governments poured money into building solar plants over the past five years, contributing more than 50 per cent of funding for many projects. Almost none was built without local government capital involvement…

“Why was it possible to build capacity exceeding global demand by double in such a short time?” asked Li Dongsheng, the chair of television and solar conglomerate TCL. “The key reason is the distortion of resource allocation and inappropriate local government participation,” he said in an interview with local media last month… In the solar industry, overcapacity has led to vast losses, which China’s top six publicly traded solar groups indicated would cumulatively total Rmb43bn for 2025. Yet the subsidies continue. One of those six companies, Jinko Solar, received Rmb1.3bn in subsidies in the first half of 2025 but still lost Rmb3bn in the period. Another, Trina Solar, received hundreds of millions of renminbi during the period…

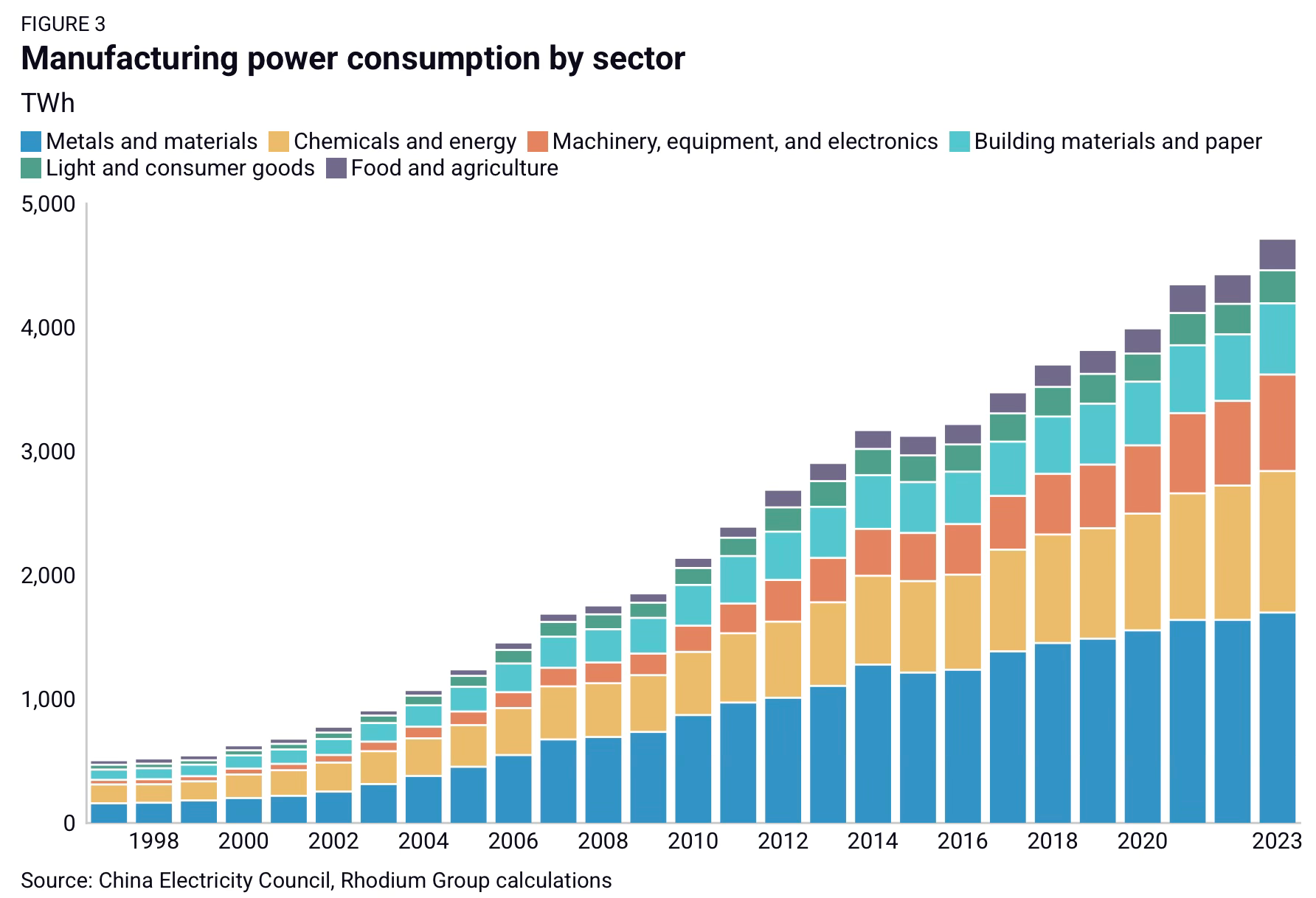

10. The Rhodium Group has an excellent report on how China managed to construct an “electro-state” that has electrified power generation and transportation, and has become so utterly dominant in the manufacturing of the likes of electric vehicles and batteries. Abundant and cheap electricity enables metals processing, which is the foundation of hardware manufacturing. It attributes this outcome to Beijing’s “expansion of cheap electricity, the agglomeration of upstream materials production (metals refining, synthesis, and fabrication, which are low-margin, energy- and capital-intensive businesses), and policies that enabled China to develop a dominant position in green technologies, while maintaining its competitive advantage in manufacturing of almost anything with an electric current.”

This is a good summary of the dynamics that led to the emergence of the electro-state:

Local government incentives to invest heavily and a financial system granting cheap credit to state-owned enterprises allowed Chinese energy-intensive industries to develop much faster than the growth of domestic downstream demand… Policy choices incentivized fully localized industrial clusters regardless of the costs of maintaining them, and central planners then prioritized the expansion of power supply and grid development to facilitate these investments.

11. It describes the explosive growth in manufacturing sector's power consumption.

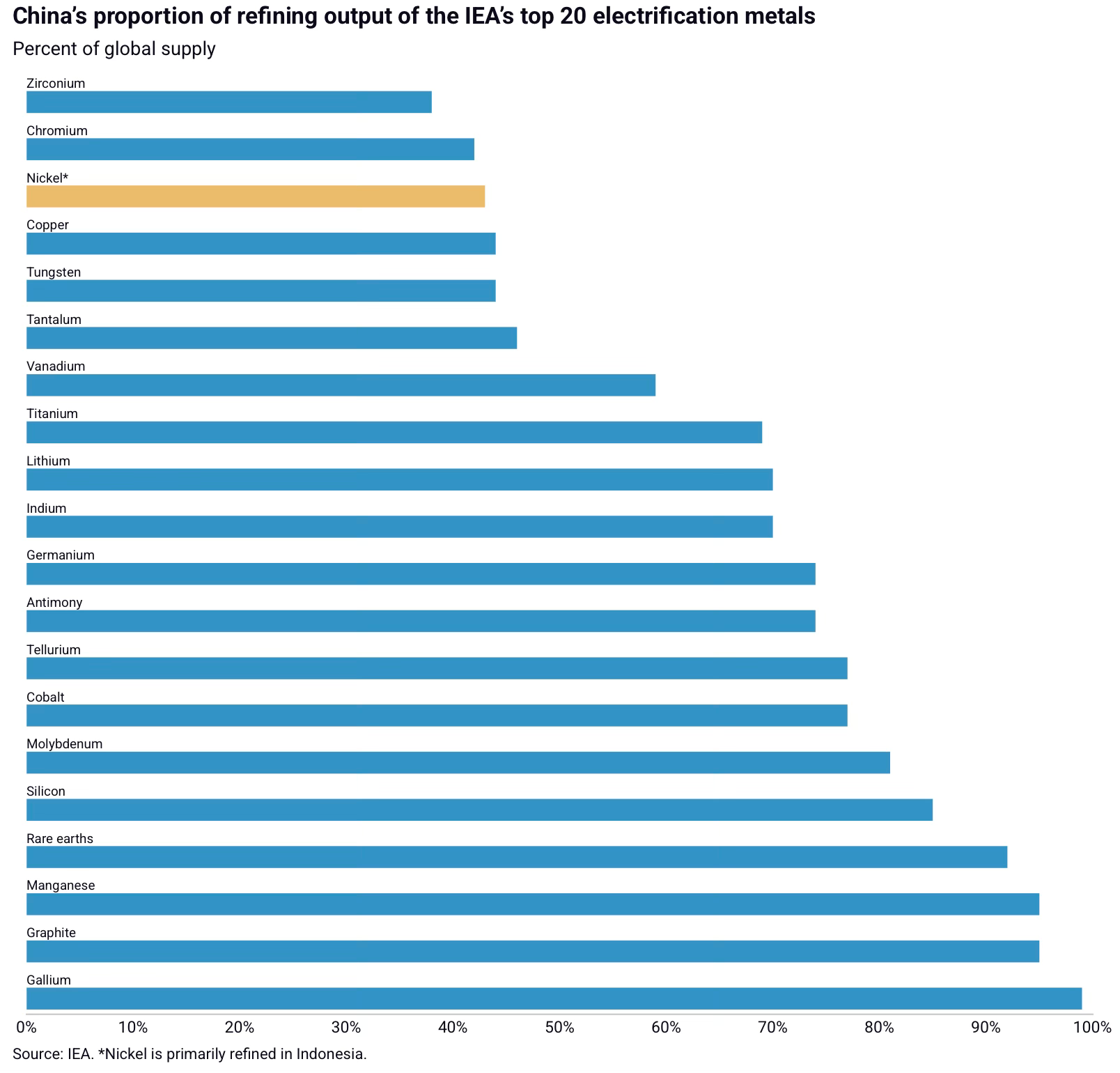

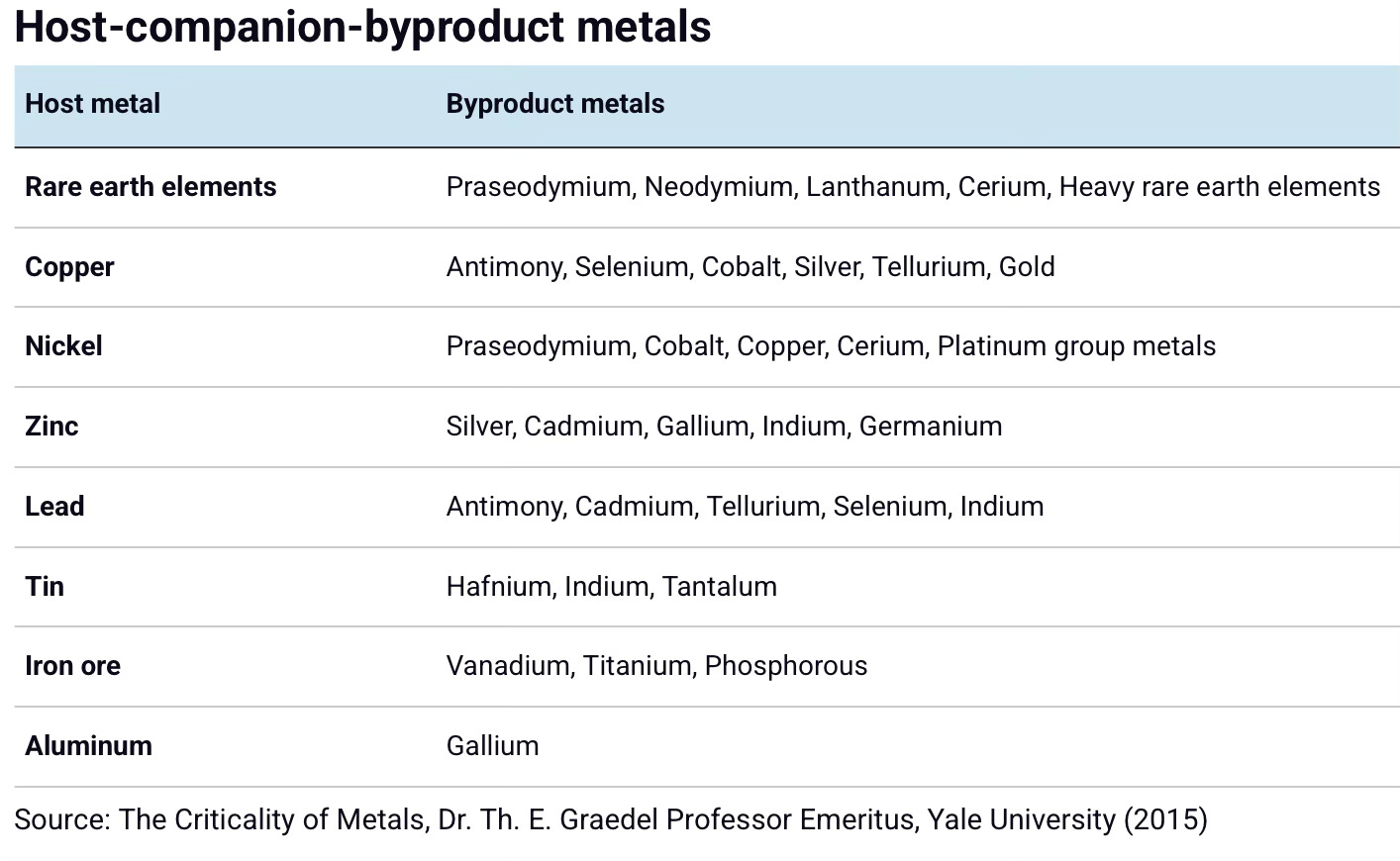

Nowhere is the dominance more pronounced than in metals refining.

This is a very good description of the industrial metals processing and refining ecosystem.

Ore bodies almost always host multiple metals, but the economic viability of extracting non-primary metals varies… These companion and by-product metals require specialized refining capacity to recover, which can be costly… There are several well-known examples of critical minerals that originate as byproducts of major host-metal supply chains… While some of these metals can be mined from dedicated deposits, if they are not captured during host-metal processing, they typically end up in tailings, slags, or other waste streams. Many companion and byproduct metals are traditionally considered too costly to extract, and as a result they often accumulate in waste piles outside processing facilities. Installing the additional capacities required to recover metals such as gallium, germanium, indium, or tellurium involve significant capital expenditures that are difficult to justify given the relatively small market size and historically low prices of these materials. In most markets, this makes recovery and processing uneconomic.

The challenge of the commercial viability of extraction, processing, and refining is overcome by China’s downstream manufacturing ecosystem.

Because Chinese mobile phone, battery, semiconductor, LED, and other manufacturers require stable supplies of minor metals, refiners can enter into offtake agreements that guarantee downstream demand from the domestic manufacturing ecosystem. This reduces commercial risk and allows smelters and refineries to justify capital expenditures for byproduct recovery in ways that are not feasible elsewhere. For minor metals, especially companion and byproduct metals, the offtake agreements are essential to start production. Major metals benefit from the ability to sell refined output to exchanges. Minor metals maintain a smaller set of potential customers because materials are produced for specialized purposes. Because minor-metal refineries depend on continuous operation, producing output without assured demand represents a material commercial risk that most firms are unwilling to assume.

The symbiotic relationship between refiners and manufacturers within the Chinese industrial ecosystem reduces uncertainty in upstream supply chains while also empowering incremental innovation in downstream manufacturing. The outcome is a supply chain that combines upstream metals processors with downstream metals consumers that simply does not exist anywhere else in the world… China produces 200 million televisions and 1.5 billion smartphones per year. Producing the TV sets guarantees offtake of 25 to 30 metals, while the phones require close to 60 metals. By establishing the world’s largest manufacturing base, the ecosystem ensures the greatest volume and diversity of offtake for processed metals and minerals. The total volume of downstream manufacturing enhances midstream processing competition for upstream materials to fabricate or process on behalf of downstream buyers.

There’s no way this tightly coupled ecosystem can be replicated anywhere globally. The only option is to start with this ecosystem and figure out ways to gradually diversify.

The report is essentially a warning that Western efforts to diversify critical mineral supply chains face a structural disadvantage: China's advantage is not simply about individual metals or policies, but about the integrated system that links cheap electricity, processing expertise, state-backed finance, and massive downstream manufacturing demand. Replicating any one piece is feasible; replicating the whole ecosystem is a generational challenge.

12. By illustrating with the example of the metals manufacturing ecosystem, the report highlights the dilemma faced by China’s trade partners. On the one hand, continuing business as usual access to Chinese imports will invariably destroy their local manufacturing bases. On the other hand, domestic manufacturers will not only be uncompetitive with respect to Chinese manufacturers, but they must also necessarily rely on Chinese suppliers for critical inputs like specialised materials that go into manufacturing.

When faced with such a dominant manufacturing power, there are very few choices. For sure, they must resort to tariffs and other trade barriers to restrict entry. The European IAA is a good example of an effort aimed at attracting Chinese investments on the condition that it would transfer technology and localise manufacturing, instead of mere assembly. But there are daunting barriers, including strong resistance and subversion by the Chinese investors.

While no country, including the US, can compete against China, the situation changes when countries form supply-chain alliances to diversify and decouple from China. I blogged earlier, pointing to Kurt Campbell and Rush Doshi who have argued in favour of America forging alliances with like-minded partners to create a meta-economy that can outcompete China and manufacture at scale.

To achieve scale, Washington must transform its alliance architecture from a collection of managed relationships to a platform for integrated and pooled capacity building across the military, economic, and technological domains. In practical terms, that might mean Japan and Korea help build American ships and Taiwan builds American semiconductor plants while the United States shares its best military technology with allies, and all come together to pool their markets behind a shared tariff or regulatory wall erected against China. This kind of coherent and interoperable bloc, with the United States at its core, would generate aggregate advantages that China cannot match alone.

Unfortunately, the Trump administration’s policies are pulling in exactly the opposite direction in terms of antagonising and decoupling from its traditional alliances.