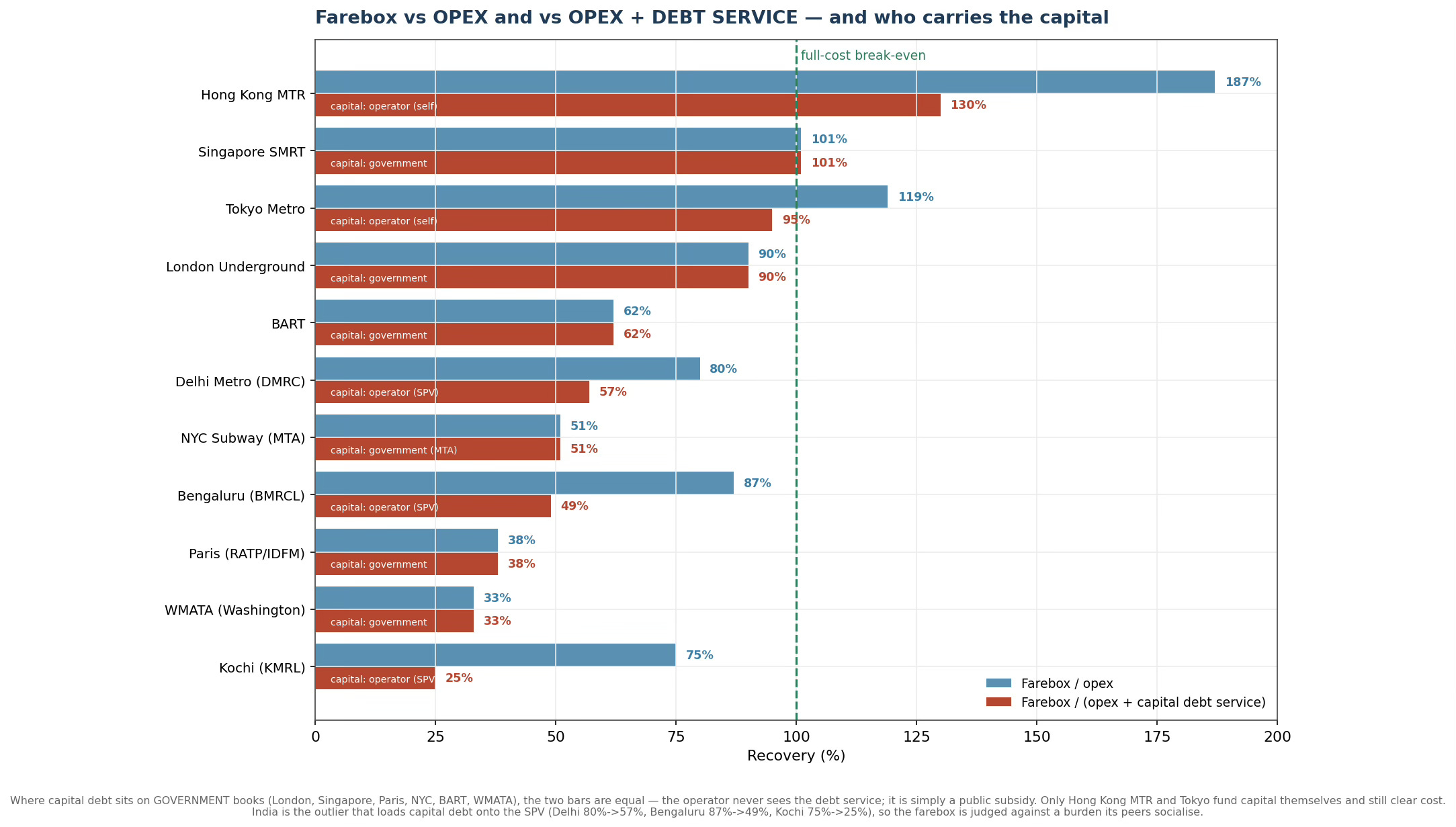

I have written about the problems with private equity (PE) investments in infrastructure. The argument has been that infrastructure is a boring asset with low but stable returns, hardly the kind of asset that would excite high-return investors like PE funds. However, over the last 15 years, private capital has flowed in large amounts to infrastructure assets. And it has resulted in some spectacular failures, most famously Thames Water in the UK and water privatisation in general.

This post will offer an important qualification of this view to avoid the impression that private capital, in general, has no place in infrastructure.

Let’s start with the same UK water sector itself. FT recently reported that the PE group EQT snapped up a 42% stake in strained UK water utility Yorkshire Water’s parent company Kelda Holdings at £9.4bn (with 5.7 million customers in northern England) at 90% of the company’s regulated asset base.

Yorkshire Water… is under close watch by regulator Ofwat, which warned last year that it was “lagging behind” on pollution. Ofwat demanded the company repay a £600mn loan amid concern about its finances and EQT agreed to contribute to the loan’s repayment as part of the deal… In the 30 years to 2024, Ofwat data show that listed water companies were valued on average 10 per cent higher than their regulatory capital value — the asset base on which they are allowed to earn a set return through customer bills. Between 2017 and 2024, stakes in UK water companies sold at a 36 per cent premium to their regulatory capital values, according to a court filing in a Thames Water case. But EQT’s deal for a 42 per cent stake in Yorkshire also demonstrates continuing interest in the sector despite big shareholders in Thames Water previously declaring the largest water utility “uninvestable”… A decision to allow some water companies to raise bills by more than half between 2025 and 2030 was a key factor in EQT’s decision to buy into the sector.

Yorkshire Water’s problems are only a microcosm of those faced by Thames Water, which serves 16 million customers in London, and is trying to stave off nationalisation by the incoming Labour government of Andy Burnham. The heavily indebted Thames Water’s lenders have recently offered a “golden share” to the UK government (similar to that held in Royal Mail) as part of a bid to keep it private and avert nationalisation. The creditors have been in control of the utility since its shareholders walked away in 2024 and have been talking to Ofwat to take formal ownership before it runs out of money by October 2026.

The government is expected to announce whether it will temporarily renationalise Thames Water under its special administration regime (SAR) within weeks. That could spark a legal battle, with lenders appointing law firm Pallas Partners and indicating they would continue to bid for the utility once nationalised… The senior creditors previously offered to inject £3.35bn of new equity into the utility and stump up £3.25bn of fresh debt. The group is also asking Ofwat to waive certain penalties until March 2030 in exchange for a one-off £800mn payment to the business… The group of creditors, which represents holders of about £17bn of the utility’s debt, is planning a stock market listing of the business as early as 2030.

In simple terms, the distressed-debt and PE funds now offering a golden share and pledging to reinvest all profits are being forced back into utility-like behaviour by the credible threat of state administration.

However, it is hard to imagine any scenario through which this restructuring can address the underlying insolvency of Thames Water as an asset. This is merely kicking the can down the road. A sustainable resolution would require significant haircuts for creditors, sharp squeezing of costs, significant maintenance and capex investments, and running the utility on thin margins for long enough to reach a sustainable debt pathway. It is hard to achieve all this under PE management. So this appears to be the latest in the series of pass-the-parcel routine that Thames Water has been going through.

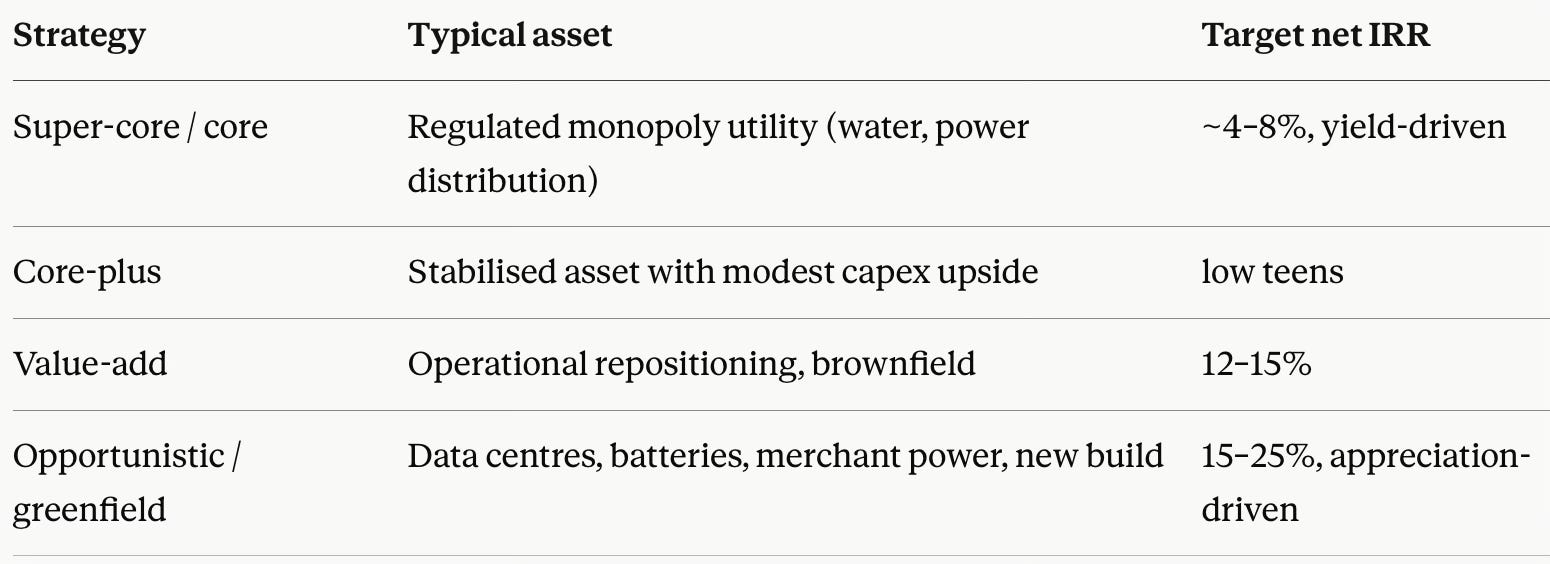

To better understand such investments, the table below shows the likely returns from various categories of infrastructure investments.

If an asset’s true economic return is 4–6% because a regulator sets it, and the private fund must clear a 12–20% net IRR to justify its fee load and honour its LP promise, the ~10-point gap cannot come from operations, which are capped by the regulator. It has to come from somewhere, and there are only four options.

The first option of leverage (i.e. excessive) is fatal in a regulated asset base (RAB) framework since debt-service costs enter the allowed tariff, thereby making the customer pay the interest bill. It is about socialising the financing choice. The second option is tax structuring of the kind that Macquarie did when Thames Water paid no UK corporation tax during its ownership tenure. The third option is to skimp on cost and maintenance by deferring capital investments, stretching maintenance schedules, socialising externalities (sewage, leakage). Finally, there is the option of dividend recapitalisations, multiple arbitrage, and ‘pass the parcel’ secondary sales.

The balance sheet on the UK water sector privatisation over the 32 years is instructive in so far as it exhibits the use of all four options by PE investors. The sixteen monopolies paid out roughly £78bn in dividends against about £190bn of capex. At the same time, net debt rose from zero at privatisation to the £60–72bn range, much of it borrowed to fund the payouts and loaded onto customers’ bills. Thames alone now carries over £19bn of debt - the highest of any UK water company - after a £3bn rescue loan at 9.75%, was fined £123m by Ofwat in 2025 (the largest ever, including £18m for unjustified dividends), and has been allowed a 35% bill rise to 2030 despite losing roughly a quarter of its treated water to leaks. On the investors’ side, Water UK claims £236bn has been invested since privatisation.

Water is representative of several low-risk and low-but-stable-return sectors (also here) in which private capital has been deployed, such as health, education, prisons, veterinary care, and public housing. Research (also here) shows that PE ownership of clinics raised short-term mortality by about 10%, implying roughly 21,000 additional deaths over the sample, while increasing spending by 19%, the vast majority billed to taxpayers, via lower nurse staffing, worse patient well-being, and reduced compliance with care standards. Similar concerns are highlighted in the Indian context in education and health sectors in a recent oped which argued that in the absence of an independent statutory regulator with outcome-disclosure powers, the extraction by PE runs through billing intensity and selective access rather than balance-sheet gearing.

There are some generalisable lessons from the history of PE funds in infrastructure and similar sectors. Wherever four features coincide - an essential service, a captive or vulnerable user who cannot judge quality at the point of purchase, a third-party payer (the taxpayer or the ratepayer), and an implicit public backstop - high-powered return incentives invariably create faultlines.

In this context, as a slight digression, I came across a brilliant articulation by Aswath Damodaran of how alternative investment strategies have lost their way in the quest for scale.

His broader point is that hedge funds, private equity, and private credit… began as a genuinely good niche business solving a real problem. Hedge funds 30 years ago produced positive alpha, beating passive investing by 3 to 5 percent annually. Today they look like expensive mutual funds, underperforming passive by roughly 1.5 percent. Private equity started as a focused, disciplined strategy for a small set of operators and has grown into a sprawling category that now struggles to deliver the returns that justified its emergence. Private credit had a legitimate original purpose, which was lending to borrowers that banks structurally could not serve. What killed each of these businesses was the same disease. Overreach. A $200 billion niche business gets sold as a $20 trillion opportunity. When that scaling happens, sloppiness follows, bad actors enter the space, and the average quality of every participant deteriorates. The original alpha disappears not because the strategy stopped working, but because too much money chased too few good deals.

The danger with private credit is far more severe than the parallel problems in private equity and hedge funds. Equity investors take their losses and move on. Lending businesses, when they overreach, take others down with them. Banks. Pensions. Insurance companies. Sovereign wealth funds. The systemic linkages run far deeper than most participants understand, and the social costs of a real default cycle in private credit would extend well beyond the funds themselves… the industry is repeating the exact mistake that produced every previous credit crisis. Take a good idea, scale it past its natural capacity, attract bad actors with the promise of easy returns, and wait for the inevitable cycle that exposes how much of the underwriting was never serious in the first place.

I have blogged earlier here and here about Ludovic Phalippou’s extensive research on PE returns (here and here). Across three large datasets for the period 2006-20, PE funds delivered net Multiple of Money (net-of-fee) of ~1.55–1.63x, or about 11% annually, matching public equity indices in the same period. During that time, roughly $230bn in carry accrued to a small number of managers, with the number of PE multibillionaires rising from 3 in 2005 to 22 by 2020. Much of the apparent outperformance, he shows, came from choice of benchmark rather than from the returns themselves.

Now, back to our examination of PE in infrastructure sectors.

Given all the aforesaid, investing in infrastructure becomes a rational choice for PE funds. Once the alpha is gone but the fee structure and the promised IRRs remain, reaching into stable, socially backstopped, “boring” cashflows is not a puzzle. It is the rational move. Those assets are attractive precisely because they are low-risk and captive: low-risk cashflows can bear more leverage, and an essential service that the state cannot let fail carries a free option on the public balance sheet. The infrastructure fund is not, in economic substance, buying a low-return asset. It is buying a levered claim on a government guarantee.

In short, a return-maximiser in a regulated essential monopoly is not investing in a low-return asset at all, but it is buying a levered claim on the public balance sheet, which is why it is drawn to “boring” cashflows. Its investment is not despite the low returns, but because low-risk, captive, socially-guaranteed cashflows can support an extraction that competitive assets cannot.

Some important qualifications are in order lest it be seen as a sweeping claim that private capital investment, especially private equity, in infrastructure is uniformly bad.

As I have written here, infrastructure is not one asset class. PE investment becomes problematic when three conditions coincide - a regulated natural monopoly with captive demand; an essential service the state cannot allow to fail; and returns set by a regulator so operational upside is capped. Water and sewerage hit all three. But they do not apply to a large and growing share of infrastructure segments like fibre, data centres, batteries, new technologies etc., where higher returns are legitimately earned by bearing real development, technology and demand risk. There, return-seeking capital is not merely tolerable, but given fiscal constraints, it is arguably necessary, because patient capital typically won’t take the associated construction and demand risks.

The question should therefore not be about the asset’s headline return but its structure. “Should return-maximisers be in low-return assets?” is the wrong question. Instead, “should they own regulated essential monopolies whose returns are capped and whose failure is likely to be socialised?” is the right one.

It must also be acknowledged that it is not the specific vehicle of PE that is the problem. Apart from Macquarie, an infrastructure fund manager and not a classic buyout shop, Thames’s later owners have included pension and sovereign funds (OMERS, USS, CPPIB-type investors), some of which geared just as aggressively. The largest infrastructure owners today are pension/SWF/insurer capital, though much of it is deployed through fee-charging, IRR-targeting fund structures (Brookfield, GIP-BlackRock, KKR). The problem is a configuration - high return target plus leverage plus regulatory arbitrage - that any owner, including a public pension, can adopt.

Finally, there are the issues of competition and regulation. Too much return-seeking capital chasing a genuinely competitive asset pushes returns down toward the asset’s true economic return. However, in the absence of competition, as with captive-customer monopolies with a public backstop and a weak regulator, incentive distortions emerge quickly. Here the deficiency of regulatory competence and/or avoidance of regulatory capture assumes significance.

In conclusion, the problem with private capital in infrastructure arises when there is a combination of return-maximising capital, high leverage, regulator-capped returns, captive users, socialised failure moral hazard, and a weak or captured regulator. This is a recipe for systematic transfer of value from the public to investors through a pass-the-parcel game, presented as investment and public-private partnership.

The policy challenge then is to match the ownership and return model to the asset’s structure, and where the asset is a regulated essential monopoly, regulate the balance sheet, not just the tariff. This aligns with the findings of the UK government’s Cunliffe Independent Water Commission (July 2025), which, apart from proposing the scrapping of Ofwat in favour of a single integrated regulator and nine regional water authorities, also proposed a supervisory (rather than arms-length) regulatory approach and mandatory asset-health monitoring. This goes against the conventional wisdom on regulation and is exactly in line with the patient capital under active public oversight approach proposed in the long paper here.

The main takeaway for India is not to import the UK’s RAB-plus-leverage-plus-socialisation architecture, but to reserve genuinely patient capital (NIIF/NABFID-type, pension, insurer, etc.) for revenue-generating infrastructure assets (or Core I/II from the paper here), admit return-seeking capital only where the asset is genuinely commercial or greenfield and bears real risk, and in TOT-style road or water monetisation, get the discount rate and the balance-sheet ring-fence right before the concession, not after the renegotiation.

Most importantly, these assets should be regulated with active supervision, including of financing practices, and close asset-health monitoring. This is especially important since, when stripped to its bare bones, the binding constraint to the successful management of private investment in any kind of regulated asset is regulatory capacity and independence. Unfortunately, both are challenging, even in developed countries.