In the early 1970s workers at Dongfeng, or “East Wind”, imported American trucks to inform their early attempts at making off-road vehicles destined for the People’s Liberation Army. Nearly 60 years later Stellantis, the European owner of the Jeep brand, is partnering with Dongfeng to produce a new battery-powered version of the iconic American light utility vehicle for consumers in China, the Middle East and south-east Asia... International carmakers, struggling for survival amid an expensive transition to electric vehicles, are turning to China’s technologically advanced and cost-efficient factories as manufacturing bases for their global businesses. Foreign companies already account for around two-fifths of China’s car exports to Europe, when joint ventures with local groups are included, according to the Rhodium Group, a US consultancy... Indeed, Volkswagen, BMW, Nissan, Hyundai and others are increasing exports from Chinese factories with spare capacity to markets other than Europe and the US.

2. A new approach to making clean hydrogen.

Most of the hydrogen the world uses today — mainly for fertilizer and refining — is produced using natural gas in a process that creates lots of emissions. In recent years, the United States and other countries have invested billions of dollars trying to make “green” hydrogen with wind and solar power, but it has proved difficult and expensive. Now a growing number of companies think a better answer could lie underground. Dozens of start-ups are trying to find large reservoirs of natural hydrogen thought to exist below the surface. Others, like Vema, are trying to stimulate the processes that generate that hydrogen, without any emissions. It’s a field often referred to as “geologic hydrogen.”...

Hydrogen is the most abundant element in the universe, and it gets made naturally in the Earth’s crust when certain iron-rich minerals react with water and rust. This process, known as serpentinization, often leaves behind rocks with a mottled green color. For a long time, many geologists believed that any natural hydrogen produced this way was unlikely to accumulate in large underground deposits because the tiny molecules would slip away through cracks in rocks. Lately, that conventional wisdom has been upended... By the 2020s, scientists were publishing papers estimating that natural hydrogen deposits underground could supply the world’s needs for hundreds of years. One promising location was North America’s Midcontinent Rift, an enormous formation of iron-rich basalt that stretches 1,200 miles from Kansas to Michigan... The Energy Department has estimated that geologic hydrogen could be produced for less than $1 per kilogram. That would be cheaper than hydrogen made from fossil fuels and one-sixth the current cost of making hydrogen from wind and solar power.

It has started attracting private capital.

Companies are racing to find the fuel. One of the best-funded start-ups, Koloma, has raised $400 million from investors including Amazon and United Airlines and has drilled exploratory wells in Iowa. HyTerra, an Australian firm, is searching for hydrogen and helium in Kansas and Nebraska. Not everyone thinks the best strategy is to search for natural deposits underground. A better idea, some say, is to create them. In Quebec, a startup called Vema Hydrogen plans to spend the rest of the year injecting water into its underground test wells to see if it can speed up the process of serpentinization that creates natural hydrogen underground... Vema has already raised $15 million and is working to raise more. There are ophiolites all over the Earth, including a ridge stretching from Costa Rica to Alaska, and the company is looking at sites in Oregon and California as well. Other start-ups, including one out of M.I.T. called GeoRedox, are developing their own approaches.

3. Semiconductor chips are one area where China lags badly.

Chinese companies will most likely make just 2 percent as many A.I. chips as foreign firms do this year, said Tim Fist, a director at the Institute for Progress, a think tank in Washington. The production gap between Chinese and foreign manufacturers is especially big for memory chips, which are essential for the large calculations done by A.I. Companies outside China will make 70 times as much memory storage capacity this year as Chinese chip makers will, Mr. Fist said...The inability to get essential tools from ASML has been a major chokehold for Chinese chip makers. Since U.S. officials led an effort to lobby the Dutch government to block shipments to China, no Chinese company has been able to buy ASML’s most advanced tools. Instead, Chinese chip makers have recruited engineers with experience using those machines at TSMC, the world’s top chip maker. And now, Chinese start-ups are trying to make their own chip manufacturing equipment... China’s A.I. companies are trying to get the computing power they need by strapping together numerous less powerful chips. Huawei has taken such an approach... The chips Huawei does produce are prone to defects and use more electricity than cutting-edge foreign ones.

4. This is one of the greatest messages from a student to a teacher, Albert Camus to his elementary school teacher Louis Germain after he won the Nobel Prize.

In a sign of Bab el-Mandeb strait’s strategic importance, Djibouti – whose coastline runs along the waterway – is home to military bases of several major countries, including the US, Italy, France, Japan, and the sole People’s Liberation Army base outside China. The Bab el-Mandeb strait is among several trade chokepoints that, when blocked, require vessels to travel more than 8,000 miles. These also include the Strait of Gibraltar and the Suez and Panama Canals...

The knock-on effects of a blockage can be much more significant where there is no alternative route to fall back on, as with the Strait of Hormuz, the Øresund between Denmark and Sweden, and the Turkish straits, comprising the Dardanelles and the Bosphorus, which act as the gateway between the Black Sea and Mediterranean. With the Hormuz strait, says Jasper Verschuur, co-author of a study into the risks of the world’s 24 narrow straits, “there is no alternative for 80 per cent of the trade”.

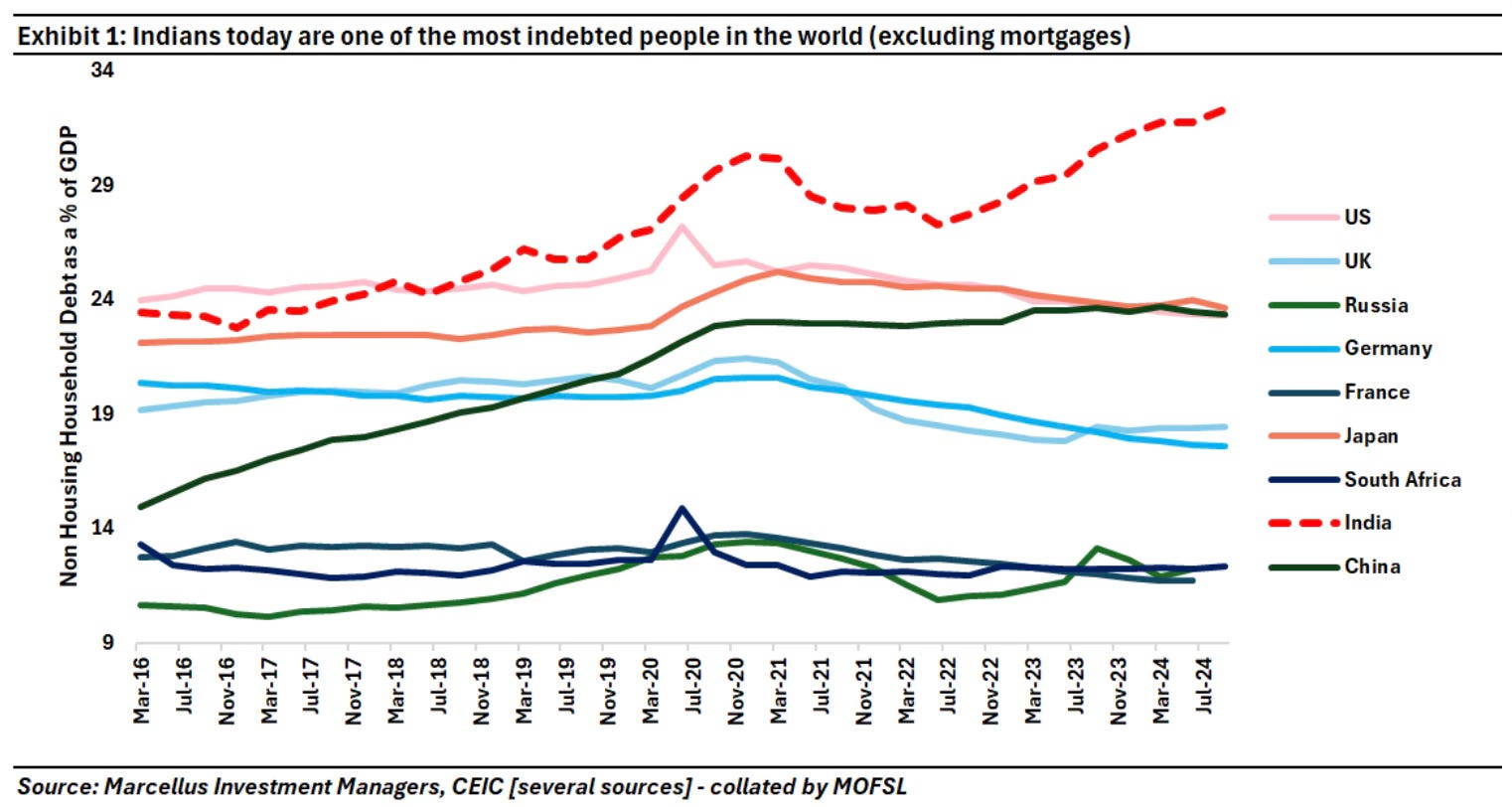

This is India's exposure to various maritime routes

The objective must be to attract a large-enough quantum of near-term capital inflows across multiple avenues — even if it involves a subsidised swap — to change exporter, importer and investor behaviour, and prevent a destabilising overshooting of the Rupee.

I am not sure how this is at all possible precisely when capital is flowing the other direction.

10. For all talk of private participations and efficiencies, the long-distance railway networks in continental Europe is largely state-owned - Deutsche Bahn (Germany), Ferrovie dello Stato (Italy), Renfe (Spain), SNCF (France), and SBB (Switzerland). The Economist writes about how Italo, the private high-speed rail operator co-founded by Luca Cordero di Montezemolo, is trying to disrupt the German network.

11. Securitisation and deepening of financial intermediation in Europe.

The securitisation market in Europe remains moribund, comprising around 0.3 per cent of GDP compared with 4 per cent in the US.

12. SpaceX's IPO prospectus takes the widest liberties with US securities law.

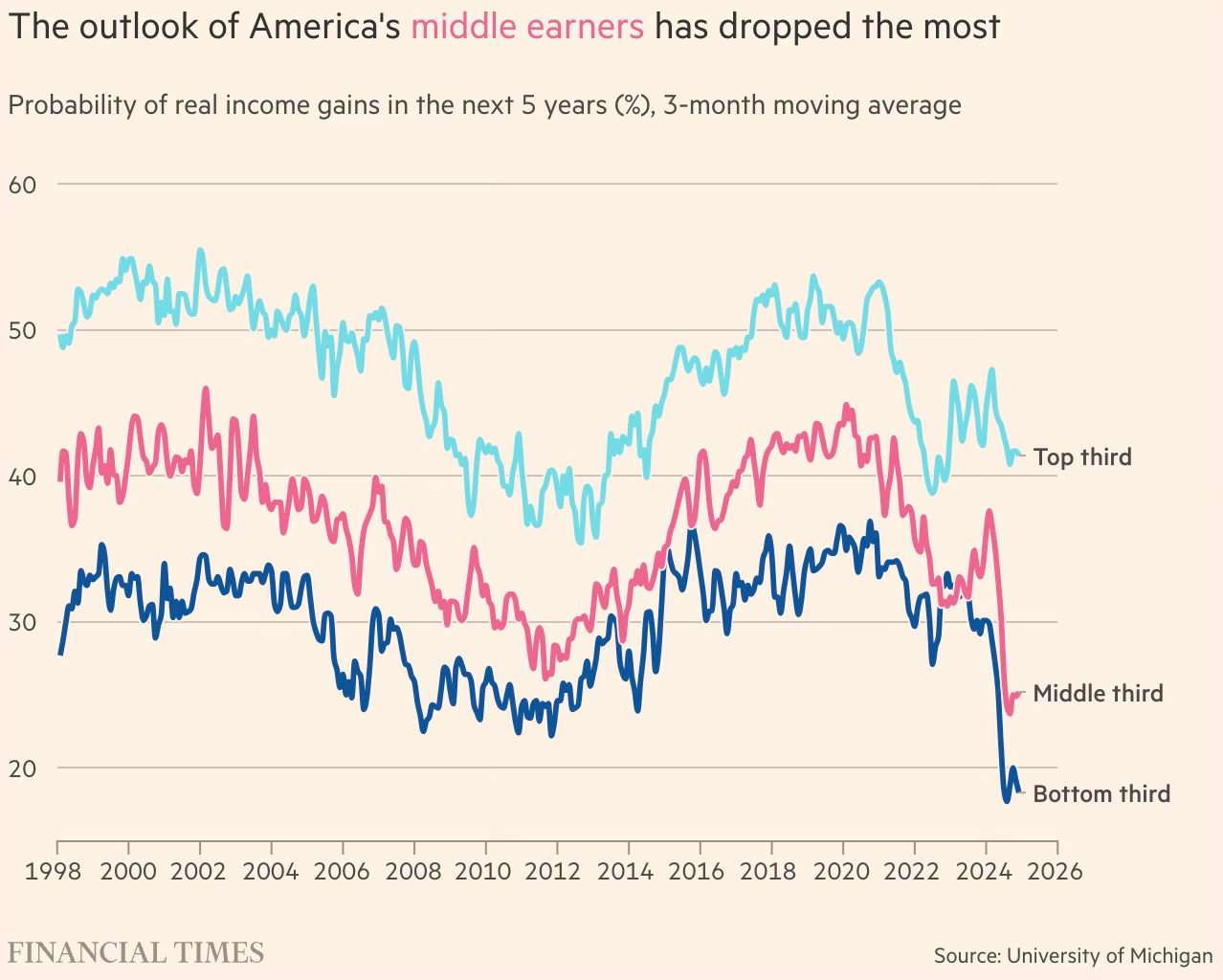

13. K-shape in US economy.

Some intelligence reports indicate that a staggering 1.2mn Russian soldiers have been killed or wounded since February 2022, a casualty figure no major power has suffered in a single conflict since the second world war... Backed by some €90bn in EU loans, Kyiv is pouring resources into domestic arms production in a bid to reduce dependence on western weapons and the political constraints that often accompany them. It has moved at breakneck speed to scale up the manufacture of land, sea and air drones, artillery systems, electronic warfare equipment, and even ballistic and cruise missiles.

15. The consulting industry is threatened by AI.

Few industries are debating AI’s implications more intensely than consulting, whose core work of research, summarising data and producing neatly designed PowerPoint presentations is highly automatable. Richard Susskind, co-author of The Future of the Professions, says consultants are more vulnerable than other mainstream professions in part because the work of junior staff “can now be taken on, with mild supervision, by increasingly capable AI systems”. The sector now has two new competitors, he adds: “the AI-empowered client and disruptive start-ups. Both challenge the conventional model.”... AI also threatens one of professional services’ foundational economic models: billing by time. When a bot can review thousands of contracts in minutes and draft complex documents in seconds, the relationship between hours worked and value delivered begins to break down. Increasingly, clients are demanding pricing linked to outcomes rather than labour inputs.

16.