1. New research by Emma Harrington, Natalia Emanuel, and Amanda Pallais shows that remote work is adversely impacting mental health. They paraphrase Robert Putnam to argue that Americans "typing alone" brings serious social consequences.

In 2024, nearly 80 percent of workers said they would be happiest if they could work remotely... Surveys of over half a million Americans from the last decade and a half revealed an uncomfortable truth: Despite its advantages, remote work has significantly deepened Americans’ isolation and distress. Our estimates indicate that remote work explains a third of the deterioration in mental health between 2011 and 2024... Our study compares workers in jobs that could be done remotely, such as finance and software engineering, with workers in jobs that must be done in person. People in remote-capable jobs worked from home three times as often in 2024 as in 2019. As they did, their days became far more solitary. Eighty-four percent of remote workers spend their workday entirely alone. Over half report feeling less connected to their colleagues. Even when communicating online, people working from home receive less feedback from their co-workers and contact fewer people outside their immediate teams.These workers did not compensate by socializing more outside work. More days passed with no social contact of any kind... In one study, when commuters were instructed to connect with a stranger near them, they reported being happier than those who continued in silence as usual, much to their own surprise. With fewer social encounters, workers in jobs that can be remote saw steeper increases in distress, mental health visits and prescriptions for antidepressants than other workers did... The pain was not evenly shared. People who lived with their spouse and kids saw their mental health hold fairly steady, while those who lived alone experienced a 20 percent decrease in mental well-being. Overall, we found that the rise of remote work increased distress by 7 percent, which accounts for a third of the total increase over the 13-year period we measured.

They argue that face-to-face time with colleagues has no substitute.

2. Katie Martin points to the different ways in which bonds and equities are reacting to Trump policies.

US government bonds, or Treasuries, have never recovered from the drop in price they suffered around the start of the war. Investors in this market, who broadly consider themselves a more cerebral bunch than those in stocks, never bought the hints of a ceasefire with Iran. Bond prices have still not returned to square one, leaving borrowing costs markedly higher. With the prospect of interest rate rises ahead to douse inflation pressures exacerbated by the Iran war, and relentless more borrowing, this is likely to remain the case for some time.

3. As AI threatens to bring down India's tech sector, this is a good article.

On the whole, Indian IT companies spent around 3.7 per cent of their total revenue on R&D in the year that the report covered. This is minuscule compared to around 15 to 25 per cent that Silicon Valley companies spend on R&D. The top IT companies are laggards of first order. For example, in 2022-23, Infosys spent just 0.9 per cent of its total revenue on R&D. The figure for TCS was 1.30 per cent. For Wipro it was 0.5 per cent while for HCL it was 1.60 per cent. The other big companies don’t fare all too well. Reliance, a giant in every way, spent only 0.53 per cent of its total turnover on R&D in 2022-23. Tata Steel is at 0.67 per cent. Maruti Suzuki spent 0.65 per cent on R&D.

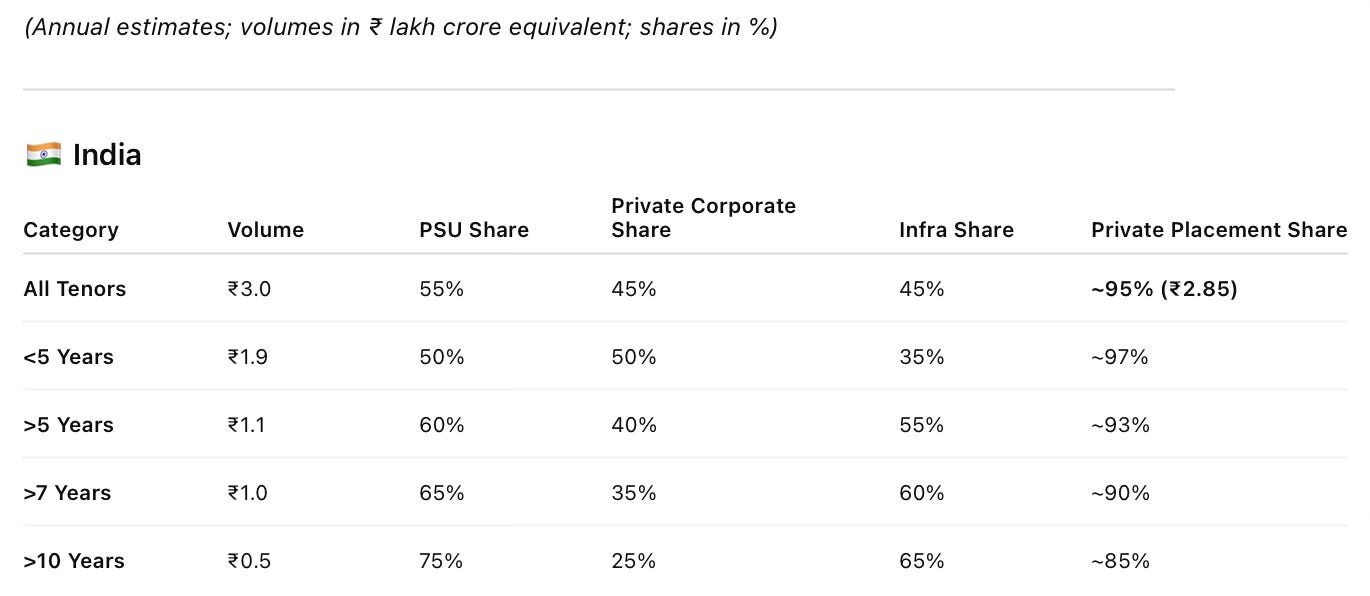

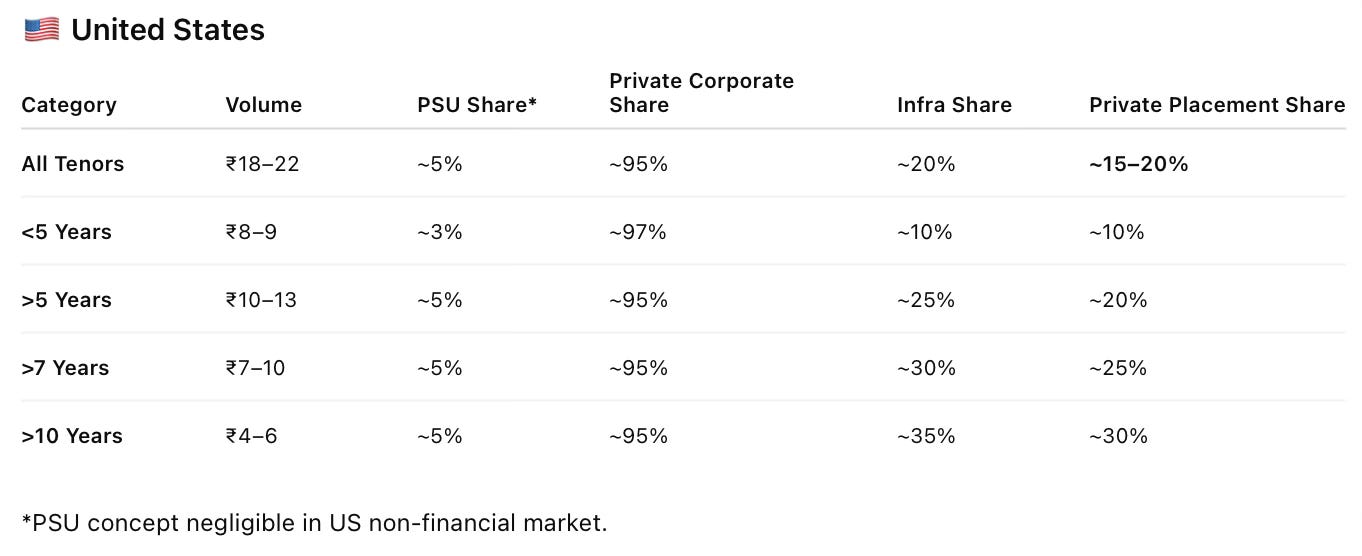

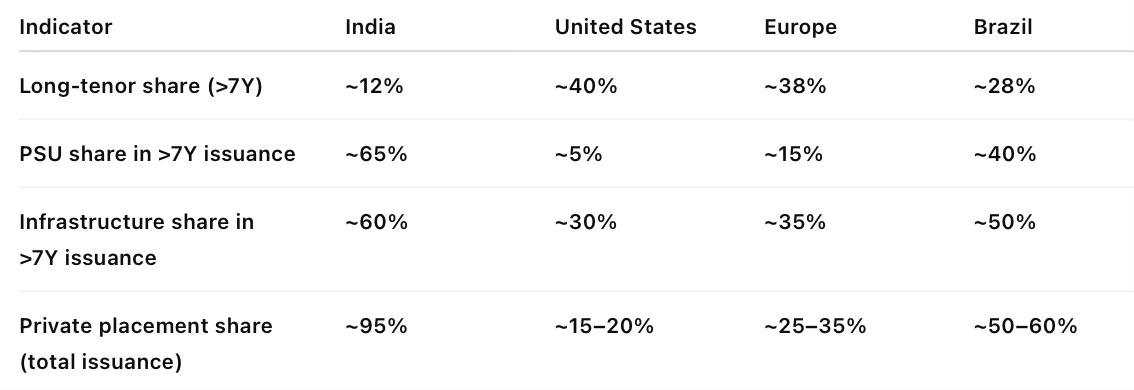

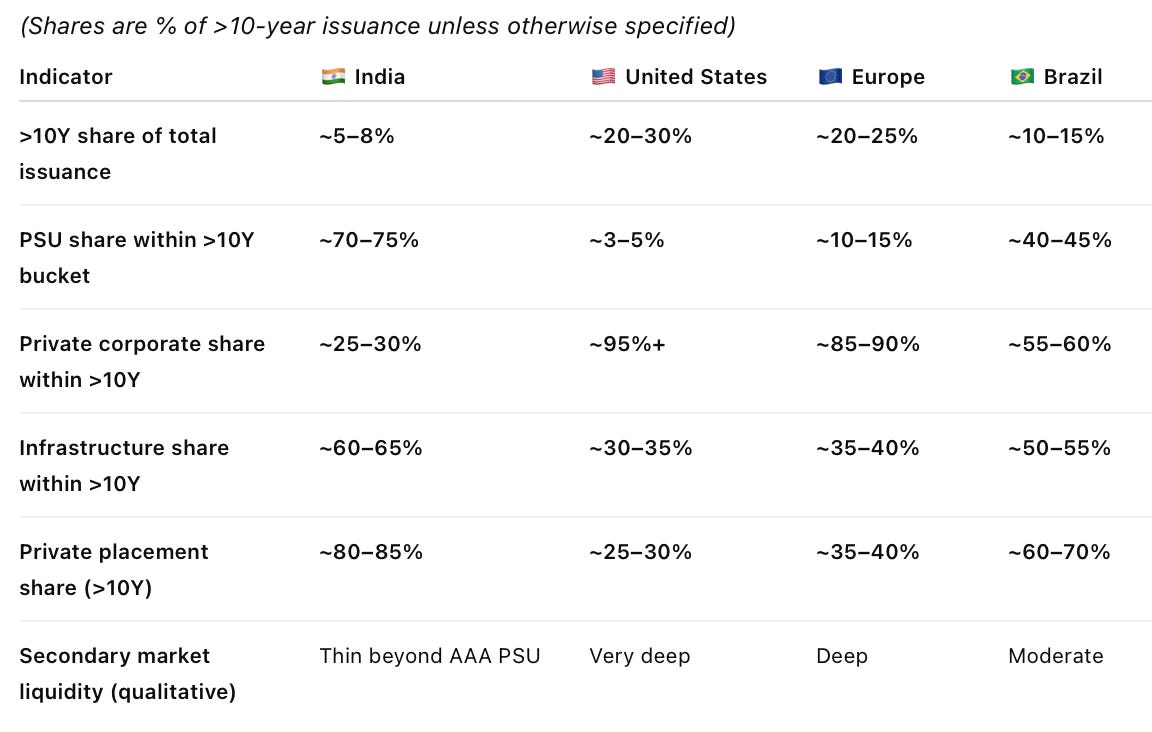

4. Indian markets have more to fall before they become competitive.

If the scheme were to attract $50 billion of FCNR (B) deposits and $20 billion of foreign borrowing by banks and public-sector enterprises, the mark-to-market loss on the RBI’s swap position could approach ₹64,000 crore at current market prices, besides increasing the RBI’s balance-sheet risk. This is not merely an accounting cost. The subsidy is real and will be monetised by participating non-resident Indians (NRIs), banks and borrowers.

Large Indian banks are raising five-year FCNR (B) deposits in dollars at 6 per cent. Their attractiveness is evident from the willingness of overseas banks to lend against the same deposits at around 5 per cent. This, in turn, will allow wealthy NRIs to achieve double-digit leveraged dollar returns against India cross-border risk. Indian banks can further transform the FCNR (B) deposits into clean five-year rupee funding at around 6.4 per cent, below comparable government bond yields.

Banks are being permitted to offer leverage to NRIs. The currency risk on such deposits will be borne by the RBI. As reported by this newspaper, State Bank of India is offering leverage of up to nine times on deposits of more than $1 million. Calculations indicate that this could translate into returns of over 14 per cent. Other banks are likely to come up with similar schemes for NRIs.

6. A new large-scale survey experiment of EU companies shows that firms substantially underestimate competitors' current AI investment, and when updated about their competitors' future AI investment plans they increase their own AI investment plans in a statistically significant manner. But this effect, while strong for domestic peers, is weak for information on foreign peers.

We documented large underestimation of competitor AI investment, substantial belief updating in response to information, and a clear asymmetry in how firms react to domestic versus foreign competition... A 1 pp increase in the expected share of domestic peers investing in AI raises a firm's own expected AI investment rate by 0.570 pp. These complementarities are absent across borders: the effect of an increase in the expected share of foreign peers investing in AI on a firm's own expected AI investment rate is statistically insignificant... Firms update both domestic and foreign beliefs when informed, but their own expected AI investment rate responds primarily to domestic posterior beliefs. These findings suggest that strategic complementarities in innovation weaken with distance, broadly understood to include not only geography but also informational, cultural, and market frictions... This asymmetry helps explain why AI diffusion may remain geographically uneven, even within an integrated economic area like Europe. While firms may observe and learn from foreign competitors, their behavioral response to such foreign signals is much weaker compared to domestic competitors.

7. Aswath Damodaran makes a great point about hedge funds, private equity, and private credit - all niche businesses which had a role, but have vastly overextended themselves and set themselves up for failure.

Each one began as a genuinely good niche business solving a real problem. Hedge funds 30 years ago produced positive alpha, beating passive investing by 3 to 5 percent annually. Today they look like expensive mutual funds, underperforming passive by roughly 1.5 percent. Private equity started as a focused, disciplined strategy for a small set of operators and has grown into a sprawling category that now struggles to deliver the returns that justified its emergence. Private credit had a legitimate original purpose, which was lending to borrowers that banks structurally could not serve. What killed each of these businesses was the same disease. Overreach. A $200 billion niche business gets sold as a $20 trillion opportunity. When that scaling happens, sloppiness follows, bad actors enter the space, and the average quality of every participant deteriorates. The original alpha disappears not because the strategy stopped working, but because too much money chased too few good deals. The danger with private credit is far more severe than the parallel problems in private equity and hedge funds. Equity investors take their losses and move on. Lending businesses, when they overreach, take others down with them. Banks. Pensions. Insurance companies. Sovereign wealth funds. The systemic linkages run far deeper than most participants understand, and the social costs of a real default cycle in private credit would extend well beyond the funds themselves.

8. Friedrich Merz initiates measures to address Germany's rising pension burden, which took up 41% of all federal government welfare spending in 2024. The proposals came from a bipartisan committee of MPs who were appointed to examine and make suggestions.

Germany’s pay-as-you-go system is facing widening deficits, with 16.5mn baby boomers retiring by 2036 and only 12.5mn new workers joining the workforce, according to the Cologne Institute for Economic Research. The government in 2024 paid €118bn to plug holes in the system, or about a quarter of the total federal budget. That share could double to 50 per cent within the next two decades, according to economists... Under the proposal, a compulsory individual contribution of 2 per cent of salaries would “be managed centrally and invested in capital markets”... The move would be a novelty for risk-averse and cash-loving Germans, who have been more reluctant than European peers to embrace capital markets to invest their large savings... Other recommendations include linking the statutory retirement age — currently 67 — to the country’s life expectancy and withdrawing early-retirement incentives. For every year gained, people should work eight months longer, the commission proposed. The experts also suggested raising the age — currently 64 — at which people who have made contributions for 45 years are able to go into retirement with their full pensions. Unions are likely to oppose the measure.

9. India has been a laggard in attracting FDI.

The Brexiteers persuaded a small majority — the vote was 52 percent to 48 percent — that Britain could throw out the austerity that had followed the 2008 global financial crash, reverse the hollowing out of well-paid manufacturing jobs and trade freely and profitably on international markets. Immigrants who had flocked to Britain from Eastern and Central Europe would be sent home. Europe merely held Britain back, and to choose to leave was to believe, as Britons had before, that the nation was meant for more...It was, of course, a fantasy... The economy has stalled and trade has shrunk. Britain is poorer than it might have been. Its gross domestic product is at least 4 percent — but could be as much as 8 percent — lower, according to independent calculations, while business investment is more than 10 percent lower. It added new frictions to the lives of Britons: new border checks when traveling to E.U. countries, stricter residency rules for living there, fewer opportunities for students to study abroad. Even just using a cellphone while “roaming” often costs more than it used to. There have been other costs, one of them a weakening of the glue between the nations of the United Kingdom itself. The referendum result was more a statement of English than of British nationalism — majorities in Scotland and Northern Ireland voted to remain. Forced to leave, Scottish nationalists claimed stronger cause to promote their case for full independence from England, and the complex political arrangements for Northern Ireland needed to protect the Good Friday peace agreement between Irish nationalists and British unionists in the province have weakened the cause of the unionists.Rather than a newly independent Britain cutting a swath on the international stage, economic realities forced cuts in spending on foreign aid and diplomacy. The hopes among Brexiteers for a new Anglosphere, adding the English-speaking Commonwealth nations of Canada, Australia and New Zealand to Britain’s “special relationship” with the United States, turned to dust, and Britain’s privileged place in Washington was lost to Mr. Trump’s disdain for traditional alliances.

11. Fascinating graphic that maps the values of AI models.

The models’ answers, in English, on topics ranging from political petitions to God, suggest values that are different from those of most people. In fact, the models are often more extreme than the average respondent in every country included in the polling. On the survey’s “cultural map”, " AI models fall overwhelmingly into the quadrant populated by rich countries. The worldview of GPT models, created by OpenAI, is more secular than any country on earth (see chart 1). Gemini models, made by Google, place more weight on individual freedom (for example, “homosexuality is justifiable”) than people do anywhere. No model reflects the worldviews of most African or Muslim countries.

12. The Economist looks at the issue of popular backlash against AI. This scenario in particular is important.

Scenarios in which some countries give in to popular rage but others forge ahead are also worrying. If America succumbs, it could cede the global ai frontier, and the attendant cyber and military capabilities, to authoritarian China. Europe and Canada are more risk-averse than America. If they choked off ai while the rest of the world kept pushing forward, their losses could be unrecoverable. More than two centuries after the Industrial Revolution, few countries have managed to catch up with the first movers.

13. Rolex SA is a profit-making company with $12-13 bn in revenues and $3-4 bn in profits whose ultimate owner is a spiritual holding company (SHC), a charitable trust called the Hans Wildorf Foundation. Rolex SA has no public shareholders, investors, or owning family, and has been so since 1960. A similar example is Robert Bosch GmbH, the German engineering giant, which has 94% ownership by the Robert Bosch Foundation (SHC) holds 94 per cent and the Bosch family the rest. In both cases, the management and ownership have been clearly separated.