1.

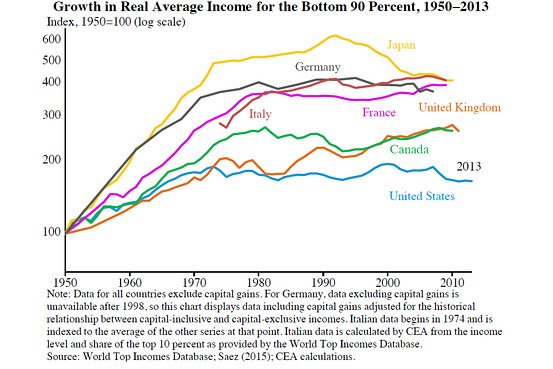

points to latest IMF figures which paint a dismal picture of rising inequality and poverty reduction in India. Net of taxes and transfers, India has the one of the highest inequality rates in the world at 51.36 in 2013, higher than even Latin America, and lower than only Papua New Guinea and China. And inequality rates rose faster than any place other than China. Reflecting on the possible causes, it finds that India does far worse in poverty reduction than China, Indonesia, Vietnam and others

And does a similarly bad job with middle class creation.

Taken together with the fact that China has produced a much larger middle-class, albeit also a much richer top 1%, India's inequality is worser than even China's. It is an inequality borne more out of the richest 1% becoming richer with stagnant incomes elsewhere.

In Austria, Norbert Hofer of the Nazist Freedom Party came close to winning 50% of the vote and narrowly lost the Presidential election run-off. Viktor Orban, the Hungarian Prime Minister, and his Fidesz Party have won the last two elections.

5.

Business Standard reports that distressed assets sales have run into problems with very few deals consummated. Among the 33 assets worth $12.29 bn (Rs 82,343 Cr) put for sale since April 2015 by the Credit Suisse's ten most indebted corporate groups, just six (the value of four is just $379 m) have found buyers.

Such deals face pressure from both sides. On the one hand, the owners are hoping that a revival of the commodities and economic cycle will restore growth back to the heady days and repair their balance sheets. Creditors are reluctant to take haircuts for various reasons, including scrutiny by vigilance authorities. On the other side, buyers are wary of the regulatory concerns, including their ability to control the assets given that most of them are on lien to creditors, not all of whom agree on the way forward. Further, some of the projects are ab-initio unviable and would require significant markdowns.

6. A RBI survey has found that a third of the ATMs in India are not functional. Indian banks expanded their ATM network spectacularly, from 27000 in 2007 to nearly 200,000 by April 2016. As to the

reasons for the non-working ATMs,

Bankers in India say that ATM machines may be out of order for a variety of reasons, from mechanical failure and paper jams, to software malfunction or lack of electricity, a common occurrence in India. If the ATM has run out of cash, then also it becomes temporarily unavailable for use.

One more reminder about the perils of rapid growth in any area in an environment where the capital base (human and physical) to support such expansion is not available.

7. In its efforts to achieve a better work-life balance, the Swedish town of Svartedalens has been

experimenting with six hour work week (from eight hours) with no pay cut for nearly a year now. The Times writes,

Many Swedish offices use a system of flexible work hours, and parental leave and child care policies there are among the world’s most generous. The experiment at Svartedalens goes further by mandating a 30-hour week. An audit published in mid-April concluded that the program in its first year had sharply reduced absenteeism, and improved productivity and worker health.

Apparently, as people get more leisure and less work time, they tend to focus more and shirk far less. The net result is higher productivity, which more than makes up for the reduced work hours.

8. While I am no outright China bear, I completely agree with everything that

Christopher Balding has to say about the implications of China's debt problem. It is very unlikely to have a soft-landing. The RMB-USD crawling peg is a binding constraint on policies to inflate away debt or further increase debt and stimulate the economy.

9.

Switzerland will next month vote on handing out an unconditional basic income of SFr30,000 ($30,275) a year to every citizen, regardless of work, wealth or their social contribution. The idea has been championed earlier in 20th century by thinkers on the left, such as John Kenneth Galbraith and Martin Luther King, as a means of promoting social justice and equal opportunity, and on the right, including Milton Friedman, as a way of restricting the coercive state and restoring individual choice and freedom.

The emergence of technological changes and digital revolution presents both the threats (in terms of job losses and need for social security) and opportunities (in terms of ability to target and transfer cash) for initiating a universal basic income scheme. The Swiss referendum will in all likelihood fail this time. But the underlying idea of a robust social safety net to assure a dignified life for everyone in a world economy buffeted by uncertainties arising from forces like globalization, skill-biased technological changes, and automation is only likely to strengthen with time.

10.

Livemint shines light on credit rating agencies in India. The recent examples of Amtek Auto (CARE) and Ricoh India (India Ratings), where rating agencies abruptly downgraded the firms without assigning any reason have been big blows to the credibility of rating agencies. This is not one bit surprising given the poor corporate governance standards and pervasive corruption.

11. I have blogged earlier about the Thames Tideway Project. Bazelgette Tunnel Limited, the project company established by Thames Water, London's monopoly water supplier, and the UK Government, has

launched a bond sale to to raise £200m-£400m to finance the £4.2 bn Thames Tideway (or "super-sewer) project. The 25km long and 7.2 m wide tunnel, to be completed by 2024, will be built under the Thames and will supply sewerage services to Thames Water on a 125 year concession. About a quarter of the cost of construction will comes from Thames Water through an increase in customer's water bills, and the remaining £2.8 bn will be raised by the project company whose shareholders include Allianz, Dalmore Capital, Amber Infrastructure, DIF, Swiss Life Asset Managers and International Public Partnerships, all of whom have invested £1.2 bn of equity themselves. The remaining finance is to be raised by the company and includes a £700m 35-year loan from the European Investment Bank granted earlier this month, the largest ever for a water project.

Such projects are most certain to suffer delays and cost over-runs. Investors generally bear a major share of the construction risk given that project revenues start to kick-in only after the construction is completed. In order to mitigate these construction risks, the Tideway project is structured in a manner that the investors will receive an income, funded through consumer water bills, from the first day. In other words, the consumers act as "the backstop or insurer on the project, bearing the brunt of any cost overruns or incidents during construction".

12. Conservative commentator

Andrew Sullivan finds a parallel in Trump's rise to Plato's Republic. At the 'late-stage democracy', when democracy has widened enough to make elites lose authority, the populist demagogue enters the vacuum and seizes the opportunity, and democracy turns into a tyranny. He feels that the rise of media democracy during this century by "erasing any elite moderation or control of democratic discourse" strengthens the trend,

And what mainly fuels this is precisely what the Founders feared about democratic culture: feeling, emotion, and narcissism, rather than reason, empiricism, and public-spiritedness. Online debates become personal, emotional, and irresolvable almost as soon as they begin. Godwin’s Law — it’s only a matter of time before a comments section brings up Hitler — is a reflection of the collapse of the reasoned deliberation the Founders saw as indispensable to a functioning republic... We have lost authoritative sources for even a common set of facts. And without such common empirical ground, the emotional component of politics becomes inflamed and reason retreats even further. The more emotive the candidate, the more supporters he or she will get.

He draws historical parallels and concludes with a scathing assessment of the Trump phenomenon,

To call this fascism doesn’t do justice to fascism. Fascism had, in some measure, an ideology and occasional coherence that Trump utterly lacks. But his movement is clearly fascistic in its demonization of foreigners, its hyping of a threat by a domestic minority (Muslims and Mexicans are the new Jews), its focus on a single supreme leader of what can only be called a cult, and its deep belief in violence and coercion in a democracy that has heretofore relied on debate and persuasion. This is the Weimar aspect of our current moment. Just as the English Civil War ended with a dictatorship under Oliver Cromwell, and the French Revolution gave us Napoleon Bonaparte, and the unstable chaos of Russian democracy yielded to Vladimir Putin, and the most recent burst of Egyptian democracy set the conditions for General el-Sisi’s coup, so our paralyzed, emotional hyperdemocracy leads the stumbling, frustrated, angry voter toward the chimerical panacea of Trump... Trump is not just a wacky politician of the far right, or a riveting television spectacle, or a Twitter phenom and bizarre working-class hero. He is not just another candidate to be parsed and analyzed by TV pundits in the same breath as all the others. In terms of our liberal democracy and constitutional order, Trump is an extinction-level event. It’s long past time we started treating him as such.

I am inclined to believe that this rationalization belies Sullivan's conservative bias. In fact, he equates widening of democracy to "our increased openness to being led by anyone; indeed, our accelerating preference for outsiders". The fundamental trigger for Trump's rise is the discontent and anger that the vast majority feel about an establishment that they feel has been captured by the elites. Trump has been peddling his policies to fuel this discontent. The American democracy could have matured without allowing such dramatic widening of inequality and egregious elite capture of the establishment. The conservatives should take the biggest share of the blame for this.

Talk about drawing wrong lessons from a crisis.

The essay though is a great read.

13. Finally,

Ananth is spot on with his assessment. No matter which way you look, the collateral damage inflicted by one individual is immense. If commentators start attributing motives to monetary policy actions and if the same echoes with popular gossip, then monetary policy making becomes fraught with dangers. In a country with a very noisy and cantankerous media, the incentive distortion for future central bankers can be damaging.

India though is not alone in this. Look no further than the

vilification campaigns by the like of Rand Paul, some of which even threatened physical harm on the Fed Chairman, Ben Bernanke, for allegedly debasing the currency with ultra-low rates. Maybe Andrew Sullivan has a point about the debasement of democracy by the democratisation of media.

{kind=link}

{kind=link}