The Saudi Crown Prince Mohammed bin Salman, for example, is engaging in sensitive national security conversations with President Donald Trump, even as the Trump family real estate business is in talks with the Saudis about a big construction project. Trump’s artificial intelligence and crypto tsar, David Sacks, has hundreds of tech investments poised to benefit from policies Trump is pushing... While the Trump family’s tentacles have worked their way into many industries, from finance and technology to real estate and defence, digital assets are perhaps the most obvious place to look for conflicts of interest that could infect the larger economy. Consider one complicated example involving the stablecoin of the Trump family crypto venture World Liberty Financial, which was used by Abu Dhabi’s MGX in a $2bn transaction linked to Binance. That company was co-founded by Changpeng Zhao, who received a presidential pardon in late October, after previously pleading guilty to a criminal charge relating to lax money laundering controls. Then there are Trump supporters like the Winklevoss brothers, whose Gemini platform was charged with the unregistered sale of assets during the Biden administration, only to settle with the Securities and Exchange Commission this year. The Winklevoss twins are big Republican donors (they’ve even chipped in for the construction of a new White House ballroom) and, not surprisingly, their platform is embedding itself deeper and more quickly into the US crypto infrastructure than many competitors. This autumn, Gemini announced a Nasdaq partnership.

2. As President Trump fights a weak economy, the largest share of Americans in more than 50 years is saying that the government is mishandling the economy.

A K shaped economy describes a post-crisis recovery where different parts of the economy and society are performing at sharply diverging rates, forming the two arms of the letter “K.”:

- The upper arm (going up): Sectors, companies, assets, and people that benefit from the recovery and, in many cases, are wealthier than before the pandemic. This includes investors in technology stocks, big tech companies, the luxury sectors, high-income professionals, and asset owners.

- The lower arm (going down): Sectors, small businesses, and people that continue to decline or stagnate even as the overall economy appears to improve. Examples include: the hospitality and travel industries, many lower-priced retail outlets, low-wage service workers, small businesses, and many middle-class and lower-income households.

4. China's trade surplus hits $1 trillion in just 11 months.

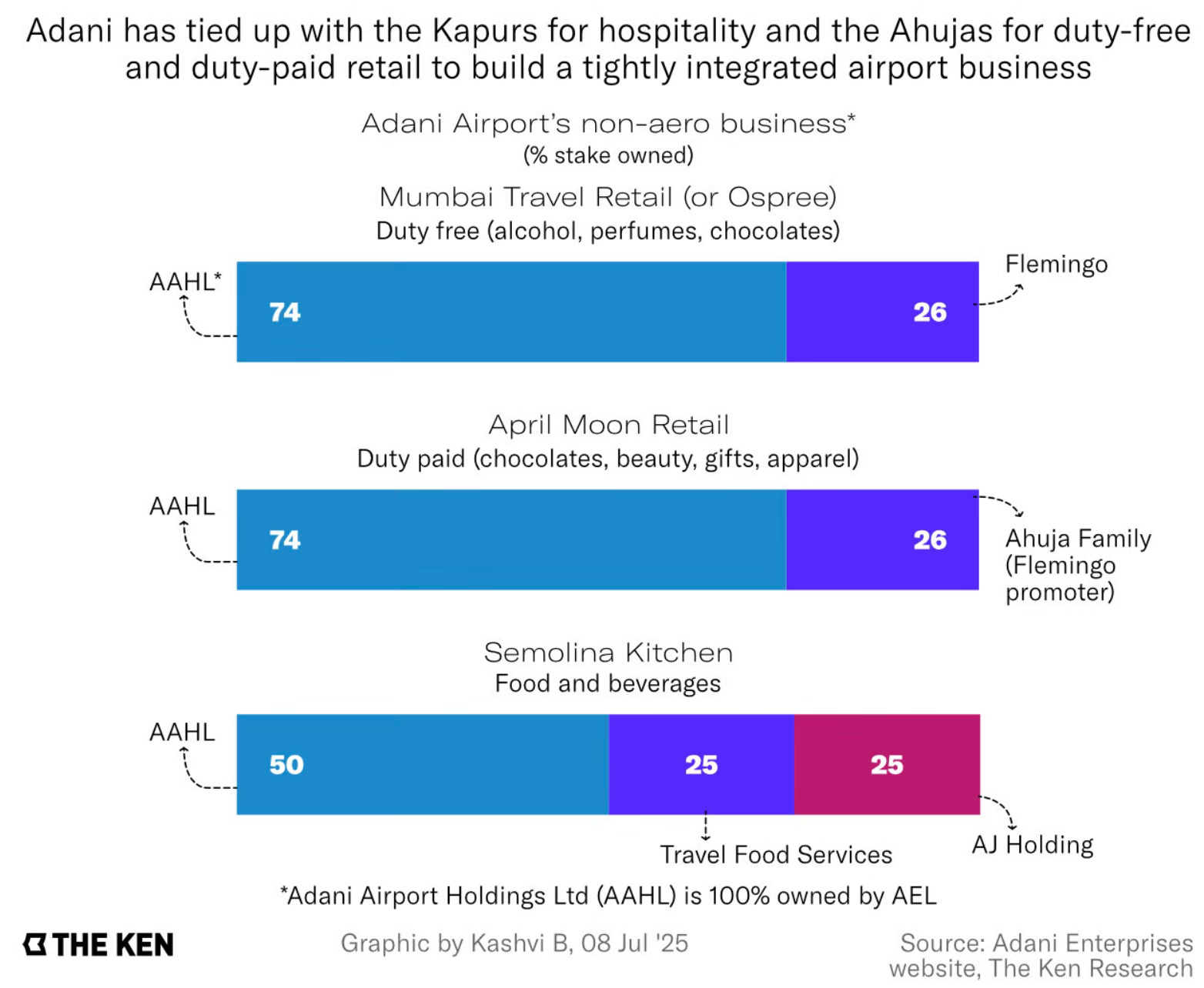

In operational terms, the new flight duty time limitation (FDTL) rules were the most consequential development for any domestic airline heading into 2025. Yet, as The Indian Express has reported, the airline’s Annual Reports for 2023-24 and 2024-25 did not mention the new rules at all, nor did they figure in the airline’s Risk Management Report. This implies that the airline’s management did not anticipate operational challenges arising from these new rules and did not prepare for them adequately, which raises questions about its basic executive capabilities.

India has been the worst-performing major equity market in the world. Flat in US dollar (USD) terms, we have been left behind by global emerging-market (EM) indices, which are up 29 per cent in USD as of end-November 2025. This is the worst relative performance for India since 1993. India has now dropped to third place in terms of EM weighting and is just about half the weight of China... India has also been shunned by foreigners, with foreign portfolio investors (FPIs) selling over $18 billion in 2025 year-to-date, marking five years of zero flows. The saving grace has been domestic flows, which continue to power ahead, with $80 billion invested by domestic institutional investors to date and the number of investors crossing 135 million... Despite 15 months of no returns, mutual fund retail flows continue to track about $3 billion per month.

7. Mexico imposes tariffs of up to 50% on about 1400 goods imported from China and other Asian countries with which Mexico has no trade deal. Chinese cars will be the hardest hit. Mexican imports from China have ballooned by 75% since 2020 to $130 bn in 2024.

8. Oren Cass writes that the Trump administration's greatest challenge is Trump himself.

Is China an adversary or a partner? Sometimes, US policy prohibits the sale of AI chips to China and pushes allies to keep China out of their markets. Other times, Trump promotes the sale of more powerful chips, or muses about Chinese firms setting up shop stateside. Are cheap foreign workers good for the US economy or bad? Sometimes the administration is forcing them out, other times trying to bring more in. Trump’s repeated suggestion to admit 600,000 Chinese students to the same US higher education system he has attacked is a particular head-scratcher. Is industrial policy to rebuild critical domestic production capacity wise? Sometimes the president trashes the Chips Act, other times he celebrates its results and goes even further in his market interventions.

This graphic shows how all the bluster on China, its exports are now on similar tariff lines compared with those from other countries (HT: Adam Tooze).

9. Striking graphic that is a pointer to why the US leads globally in innovation (HT: Adam Tooze)

When Nvidia attempted to acquire Arm in 2020 — a deal that would have locked down the fundamental architecture of chips used for AI — the FTC sued to block it and the deal was abandoned. Because Arm remained independent, Google is now able to compete with Nvidia in the production of AI chips, using Arm’s technology to build its own processors.

11. Electrification in South Asia is a true development success to be celebrated, just as its failure in Africa is one to be deeply disturbed.

The green revolution at BP began on February 12 2020, in Bernard Looney’s second week as chief executive. Looney, a charismatic BP lifer who had run the company’s oil and gas operations, embraced the energy transition with the zeal of a convert... Two former executives claim Looney had been working with consultants from McKinsey for months but had not shared the plan with the other 11 members of BP’s executive team before unveiling it. “It was a big bang approach,” one of them says...To consolidate control and prepare BP for disruption, Looney and McKinsey dismantled the company’s traditional “upstream” and “downstream” divisions, which explored and produced oil and gas and then refined, traded and sold it. Instead, there were 11 new business units, some of which left staff baffled. One new team was called “Cities and Regions” and its job was to imagine how urbanisation would change energy use and consult with cities on what opportunities there might be for BP to play a role. “It looked like a consulting job on a piece of paper rather than something that was really going to fly,” admits one former BP executive. Last year, BP reorganised again to get rid of the Cities and Regions unit and “reduce duplication”.“You could see the mis-steps happening live. The degrees of change were just too fast,” says another. “Changing the CEO is one degree of change. Then the CEO changes the strategy overnight. Then he decimates anybody in divisions that he didn’t think were important.” Later in 2020, Looney set out more details. BP went beyond Shell, and any other oil company, in pledging to actually reduce the oil and gas it produced, with an initial target of a 40 per cent cut by 2030. “No other company followed, so either you are a prophet and others did not get it, or you are the lonely guy on top of a mountain,” observes the second executive. With McKinsey teams embedded across the organisation to offer rebuttals, and amid the chaos of the reorganisation, insiders say it was hard to speak out against the plan. “You could not have a dialogue about this being the wrong thing. If the numbers did not work, you would fit them,” the executive adds.

Both companies increased their spending on green technology rapidly, to a peak in 2022 of nearly a third of overall investment, or $4.9bn, for BP, and nearly a fifth, or $4.3bn, for Shell. BP promised to spend a further $55bn to $65bn between 2023 and 2030... Today, Shell and BP have retreated to be more in line with their US rivals, though still with targets to have net zero emissions by 2050. The grand narrative of transformation has been discarded for renewed focus on shareholder returns. While the world continues to electrify, and to grow the share of solar and wind power generation, the two companies are now focusing on other parts of the transition, such as moving from heavy fuels with high emissions to gas and eventually biofuels and hydrogen. In the first nine months of this year, BP cut its spending on clean energy by 80 per cent compared with last year, to just $332mn. Shell says it is now “focused on disciplined capital allocation in our areas of competitive strength while driving improved returns”.