Now that we are past the first phase of the Gulf War and a ceasefire has taken hold (though with the breakdown of the talks and more sabre rattling by President Trump, it now looks tenuous), it may be a good time to list out a few takeaways from the war. It is also important because, at a broader level, the Trump 2.0 administration, generally and the Gulf War in particular, may have reshaped the world economy and geopolitics in many ways.

Here are some observations:

1. Arguably, the biggest takeaway from the Gulf War is one more reminder about the deeply interconnected nature of the world economy, with dependencies flung far and wide across industries and countries/regions, and associated risks and vulnerabilities. The Covid 19 pandemic was a rude awakening about the risks posed by a globalised supply chain and the extreme dependency on China’s manufacturing prowess. The Russian invasion of Ukraine exposed Europe to an energy market shock that rippled through the economy and unsettled a decades-long dependency. The Gulf War has reignited and amplified the deep energy market vulnerabilities in particular and global economic dependencies in general.

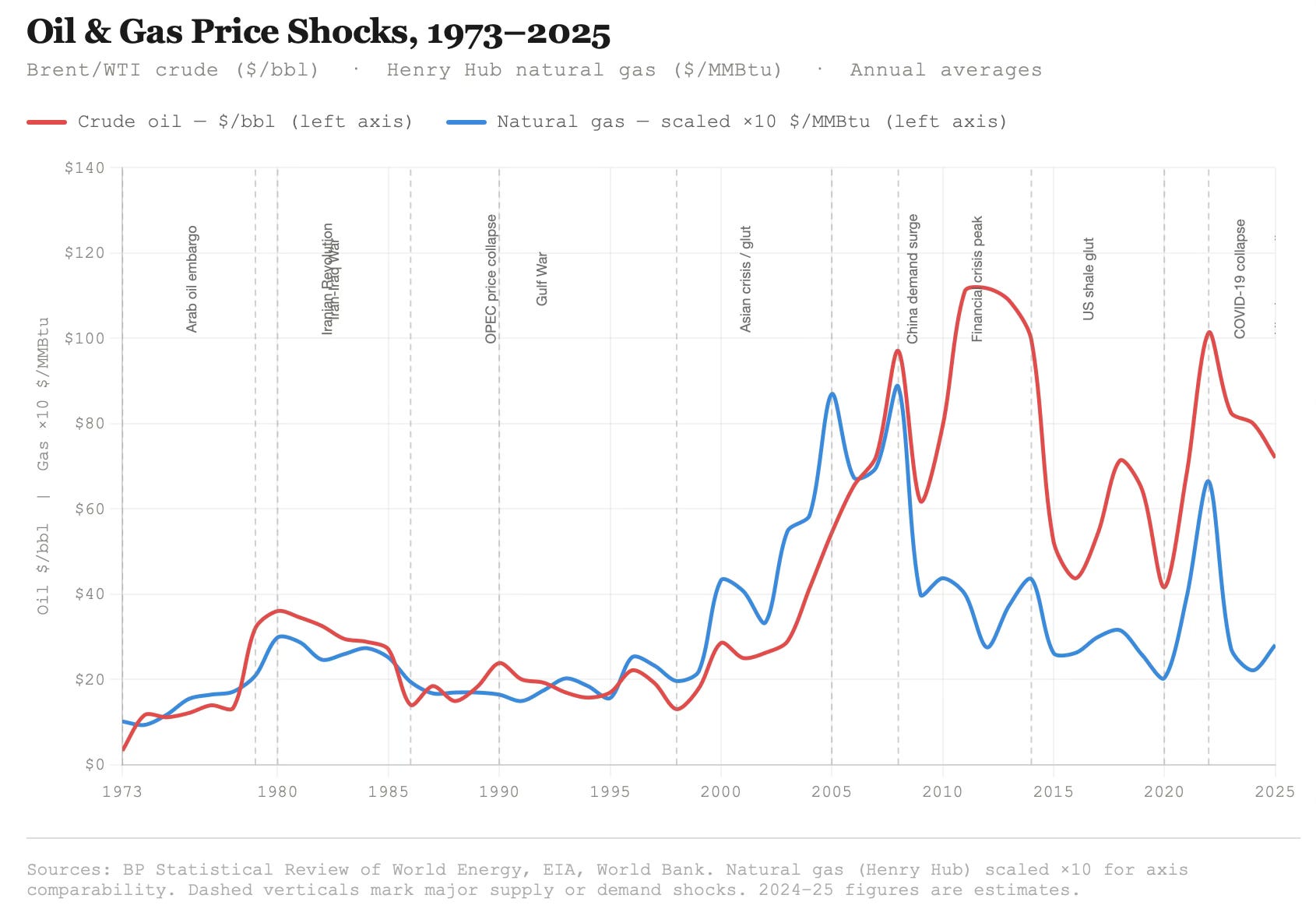

2. The world economy has been witnessing increased volatility in the oil and natural gas markets since the millennium.

Consider this about how the Gulf War may have a long-term negative shock on the global LNG markets.

Iran carried out a retaliatory missile strike on Ras Laffan, Qatar’s vast energy complex. That target produces roughly a fifth of the world’s liquefied natural gas, a transportable fuel used to heat homes, cook food, power factories and generate electricity throughout Asia and Europe… Officials and workers are still picking through the rubble, and the full extent of the damage has not been assessed. Even so, Saad Sherida al-Kaabi, Qatar’s energy minister, said Thursday that it would take up to five years to repair and would reduce the country’s export capacity 17 percent.

And more generally on the global energy markets.

Critical Gulf energy infrastructure that was presumed to be safe is now seen as vulnerable, he said. A precedent has been set. “Buyers will price that risk for longer than the initial outage itself,” Jan-Eric Fahnrich, a senior analyst at Rystad Energy, wrote in an analysis. Countries in Asia and Europe, which depend on L.N.G., are likely to face more expensive gas prices long after the Strait of Hormuz reopens.

The extensive damage suffered by oil and gas infrastructure across the Gulf means that recovery to pre-war production levels is unlikely even if the war ends now. FT Alphaville points to JP Morgan analysts who document the extent of damage, listing the roughly 50 energy infrastructure assets in the Gulf that have suffered varying degrees of damage in drone and missile strikes. Qatar’s Ras Laffan oil and gas complex, for example, may require years of repairs to restore 17% of its damaged capacity.

Even if the war ends now, a big uncertainty will be how long it will take to restore oil and gas supplies to the pre-war status quo.

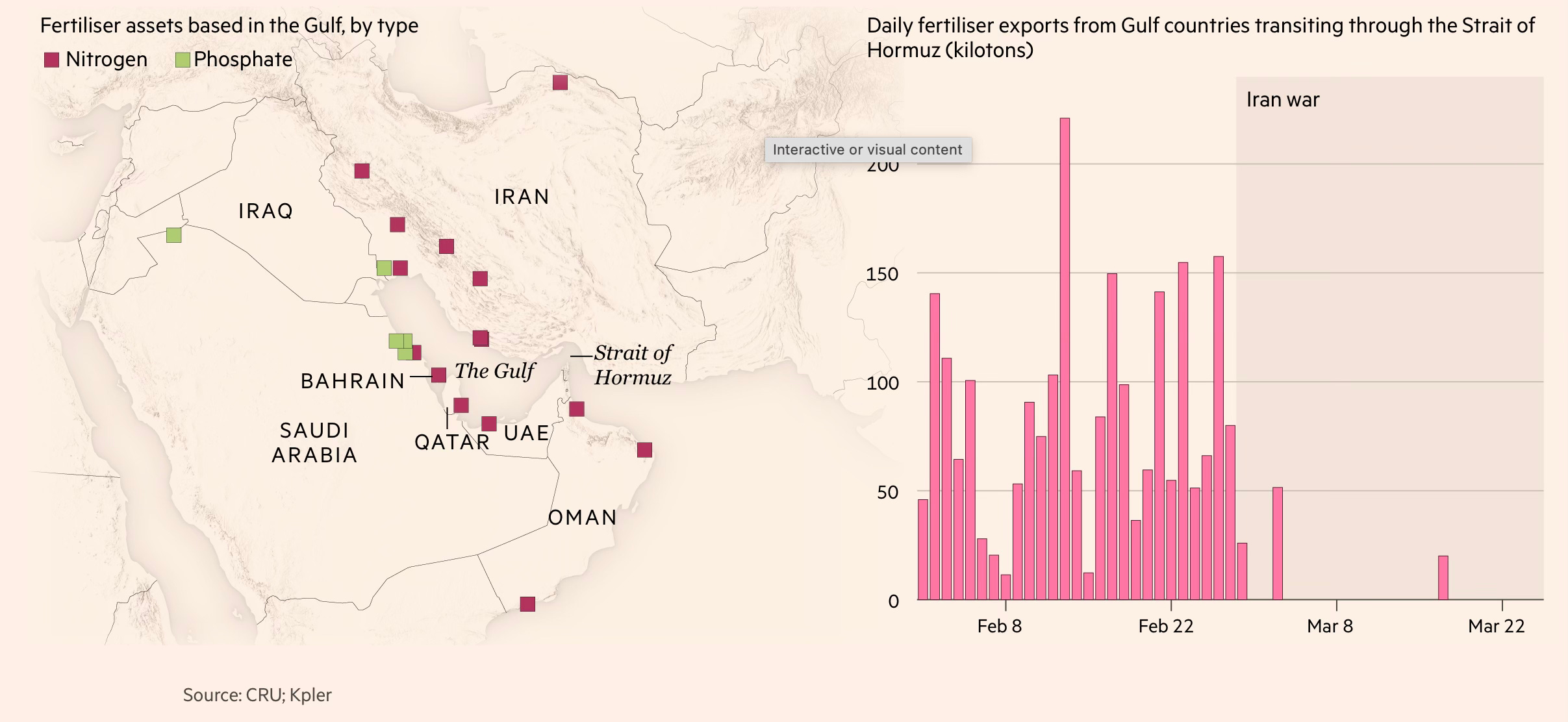

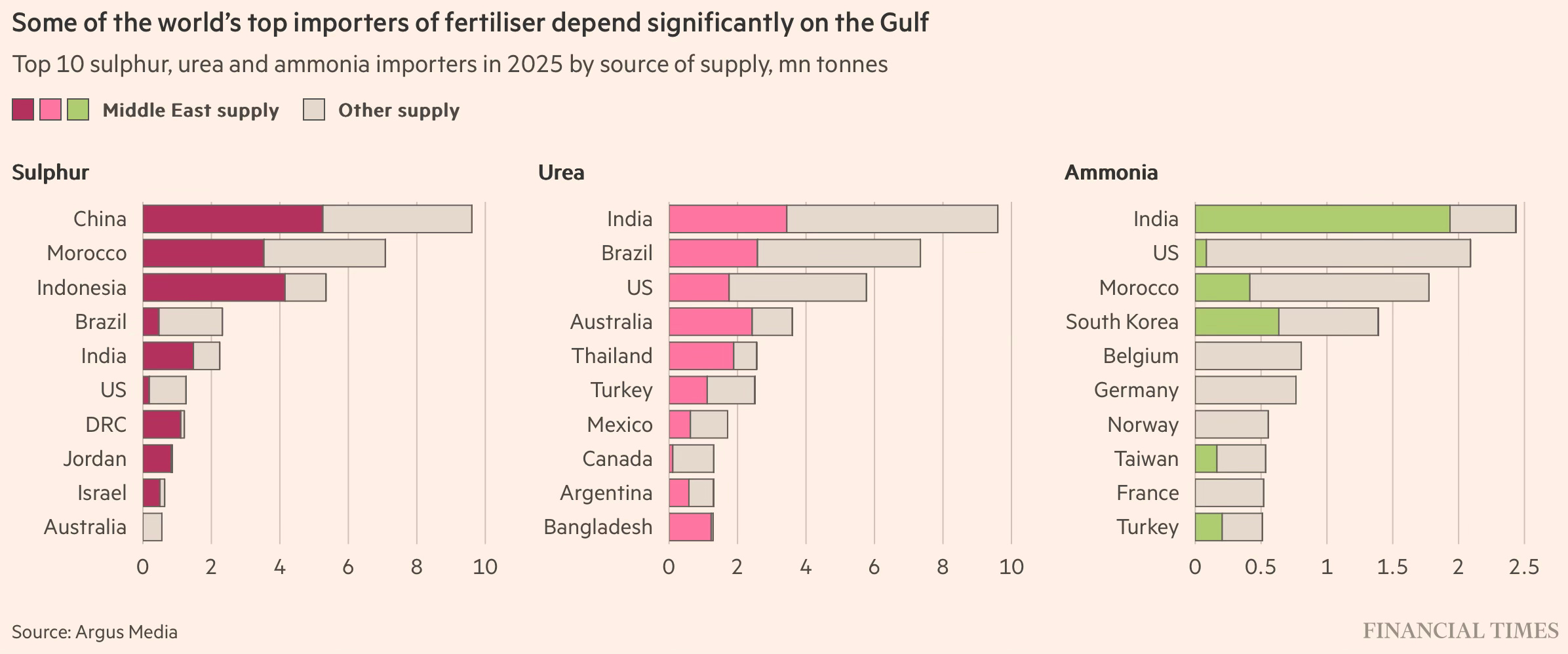

3. The dependencies are not confined to energy markets. For example, it threatens to adversely impact agricultural production.

Gulf states account for 49 per cent of globally traded urea and 30 per cent of ammonia, perishable contributors to the nitrogen cycle that makes high-yield agriculture possible. When that supply chain stops, the effects accumulate quietly in soil chemistry and planting decisions over the months that follow… Before the first strike on Iran, the global food system was already running on reduced redundancy — Ukraine and Russia still represent about a quarter of global wheat trade, and some 400mn people across the Middle East and east Africa have been absorbing that supply shock for three years.

In fact, it is estimated that the impact of the Gulf War on food prices could be bigger than that due to the Ukraine war, with the channel of impact being fertiliser supply. Agriculture depends on three core nutrients - nitrogen, phosphorus, and potassium. Nitrogen fertilisers like ammonia and urea are produced from natural gas, and phosphorus depends on sulphur, a by-product of oil and gas refining.

The level of dependence on the Gulf for sulphur, urea, and ammonia is very high.

This is a striking illustration of how LNG supply disruption has triggered fertiliser plant closures across India in March 2026.

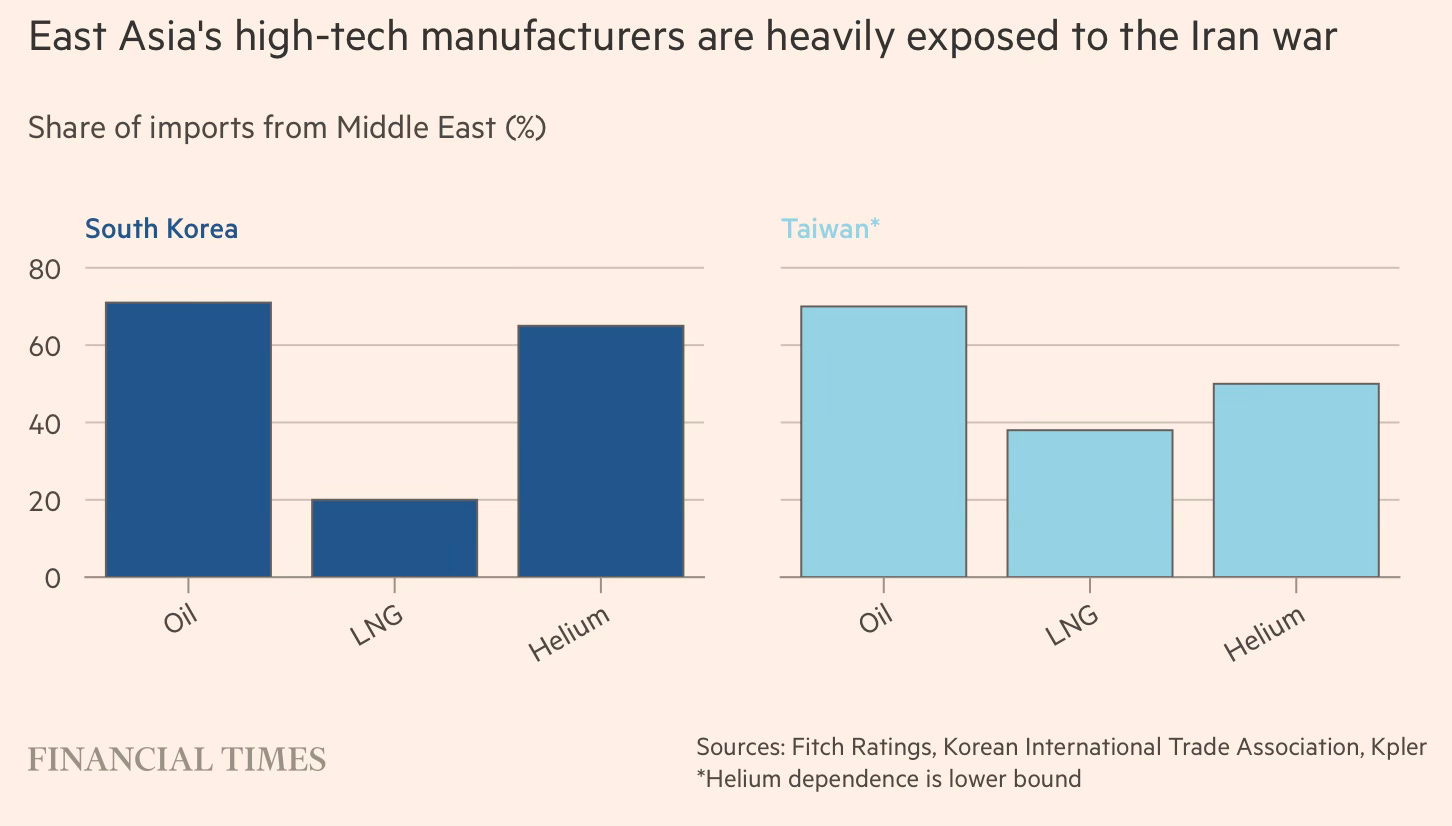

Tej Parikh has a good illustration of the vulnerabilities in the global semiconductor industry, where a chip production line can cross over 70 boundaries before reaching the consumer. The level of risk concentration is extreme and perhaps unavoidable.

South Korea’s Samsung Electronics and SK Hynix dominate memory chip manufacturing, together accounting for 80 per cent of high-bandwidth memory and nearly 70 per cent of dynamic random-access memory… Taiwan’s TSMC makes 90 per cent of advanced semiconductors and virtually all of the high-end AI chips designed by Nvidia, the world’s most valuable company. Both South Korea and Taiwan depend on fossil fuels for energy, which almost entirely come from imports particularly via the Strait of Hormuz. The latter relies on the Middle East for more than one-third of its liquefied natural gas needs.

Asia’s chip industry is reliant on the Middle East for chemicals too. About one-third of global helium supply — a byproduct of natural gas processing that is used to cool silicon wafers — is from Qatar. South Korea and Taiwan get the majority of their helium from the Gulf country, which is a dominant provider of the hard-to-substitute, high-purity variety. Roughly half of global seaborne sulphur — an element used for chip cleaning and etching — transits the strait. Even before the war broke out sulphur was facing a supply squeeze, owing to high demand from the tech and electric vehicle industries. The Dead Sea is also the world’s largest source of bromine, a chemical that helps score patterns on to silicon wafers. South Korea imports virtually all of its supply from Israel.

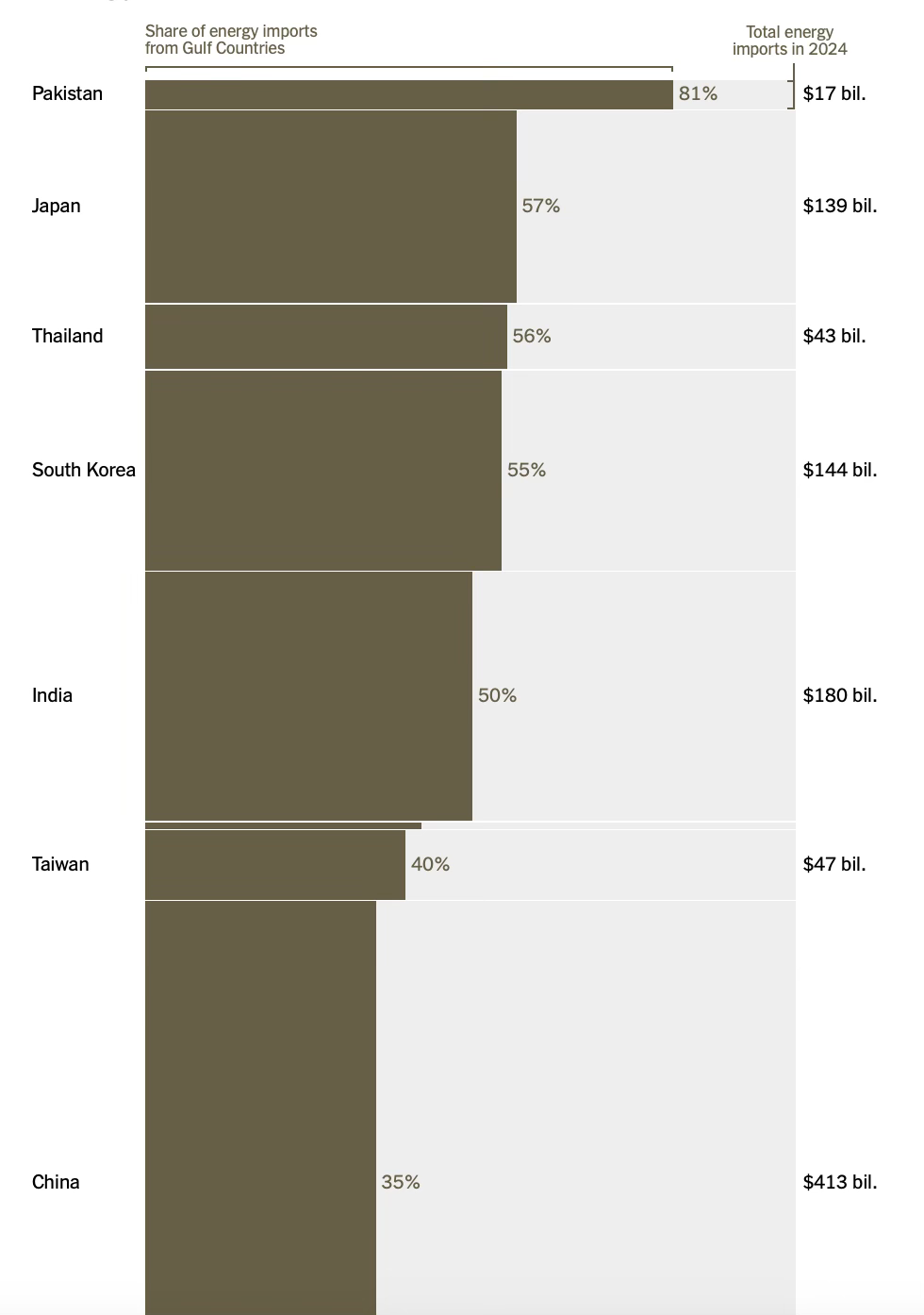

4. The War has also shown how vulnerable the Asian economies are to global oil shocks. Hoarding, price caps, tapping reserves, restrictions on exports, rationing, and other demand management measures have become commonplace across Asia. While Gulf produces a fifth of global oil supplies, Asian countries are among the most dependent.

In 2024, nearly 21 million barrels of oil a day crossed through the Strait of Hormuz, the narrow passageway connecting the Persian Gulf to the world. Four-fifths of that supply went to Asia. China has long been the biggest purchaser of oil and gas from Persian Gulf nations. And with more than a third of its total supply coming from the region, the disruption is significant for Beijing. But other countries are almost entirely reliant on the region for their energy needs.

India’s dependence is especially acute.

Almost 50 per cent of the LPG and 30 per cent of the natural gas that India consumes comes from the Strait of Hormuz.

5. Chokepoints have become the game in global geopolitics. China’s weaponisation of its dominance in the processing and refining of critical minerals and manufacturing of rare earth magnets has single-handedly given it an insurmountable chokehold over the US. It has also clearly demonstrated its intent and success in weaponising its general dominance in manufacturing.

Geopolitically, one of the most important outcomes from the Gulf War is the realisation that the Strait of Hormuz is arguably one of the biggest global economic chokepoints. The Strait is the only passageway out of the Persian Gulf, carries 25% of the world’s seaborne oil and 20% of its natural gas, and the land pipelines can carry only a small share of the oil and gas carried through tankers. Local geopolitical concerns also deter countries from laying pipelines through another country to export their oil products.

Badr Jafar has this description of the vulnerability.

Thirty per cent of global seaborne oil flows and a fifth of the world’s liquefied natural gas trade normally transit a waterway that is 21 nautical miles wide. A third of seaborne traded fertiliser and nearly half the world’s seaborne sulphur exports depend on the same passage, with direct implications for global food security. So do significant volumes of aluminium and helium — the latter essential to semiconductor manufacturing and the global AI supply chain. The concentration of so much global commerce through a single contested corridor is an anomaly the world has tolerated for decades.

This is a good compilation of how the weaponisation of the Strait of Hormuz has impacted important supply chains.

The War has shown Iran that it has a powerful weapon in the form of the Strait of Hormuz, which it can squeeze or close whenever required. This may well also be Iran’s biggest win from a war that has reduced large parts of the country to rubble. As Gideon Rachman has written, “the future dilemma is that Iran now knows that control of the Strait of Hormuz gives it a stranglehold over the world economy. Even if it relaxes its grip in the short term, it can tighten it again in future.”

6. But chokeholds are not permanent, and there may be nothing more powerful than activating the chokehold in triggering efforts to overcome it. By exercising its chokehold over Europe’s energy markets and forcing a rapid shift towards LNG and other energy sources among Europeans, the Russians have lost one of their most important strategic levers over Europe.

As Badr Jafar writes, a similar realisation is emerging among energy producers in the Gulf region about the need to reduce reliance on the Strait and build resilience in the energy supply chain.

Saudi Arabia’s Red Sea ports and expanded pipeline capacity offer an alternative energy corridor. The UAE’s east coast provides deep-water ports and pipeline routes connecting Gulf producers to the Indian Ocean. Oman’s developments at Duqm and Sohar sit well outside the chokepoint. Goods and energy are already moving along these routes — in some cases through cross-border land bridge arrangements that would have seemed improbable just months ago. The Middle East also holds a largely untapped inheritance: pipeline infrastructure built in previous crises and mothballed for decades, road and rail corridors, cross-border electricity grids and water systems that stretch beyond established networks. With renewed co-operation, these assets could deepen regional connectivity to global markets. The crisis is doing what years of summitry could not — creating the conditions for genuine intraregional economic integration. States whose ties were strained only weeks ago are now finding common cause.

This is a repeat of what happened in the early days of the Ukraine war when the Europeans realised the chokehold Russia had on its natural gas supplies. On the same lines, the realisation of the fickleness of the US security umbrella has sent the US allies scrambling to shore up their own defence preparedness and strengthen their non-US alliances. In the long arc of history, the events of the last year may have been just the right impetus to push the Europeans (and Japan) into the pursuit of independent defence strategies.

7. In the grand scheme of things, historians may well come to regard the Gulf War as one with only losers. Iran has been devastated, and its economy has surely been put back several years, if not at least a decade. For all the outward bravado and bluster, it is hard to believe that the loss of a whole generation of leaders has not seriously impacted the country’s politics. Its proxies in Syria and Lebanon have been defanged.

This war, coming on the back of the sustained Gaza bombings, has left an Israeli society that is radicalised to a scary degree, even evoking comparisons with Weimar Germany. Polls suggest that more than 90% of Jewish Israelis back the war, and the country’s political parties have been trying to outbid each other in calling for the extermination of its enemy. History tells us that these trends will not end well for Israel and the world at large.

It has also surely alienated a generation and more of people globally, especially in Europe, including those sympathetic to its cause, who are horrified by the barbarity of the Gaza and Iran attacks. The most lasting damage may well be in the US, where the public opinion against Israel, even among the traditional support base, has suffered sharp declines.

The long period of geopolitical calm and stability that allowed the Gulf economies, especially the UAE, to prosper and become global magnets has been rudely unsettled. It is likely to be a long time before they can aspire to reclaim their pre-war status, if ever.

The fickle and whimsical nature in which President Trump conducted the war allowed Israel to dictate the agenda and subordinate the US interests to its own, and browbeat its own allies, which have all contributed to undermining the US's credibility. It does not help that it has not managed to achieve its primary objective of regime change in Iran, despite eliminating a whole generation of Iranian leadership and the massive bombardment of the country.

To this extent, the Gulf War Trump 2.0 administration may have rung the bell on the definitive decline of the post-war US hegemony in international politics. The US security umbrella is now punctured beyond repair.

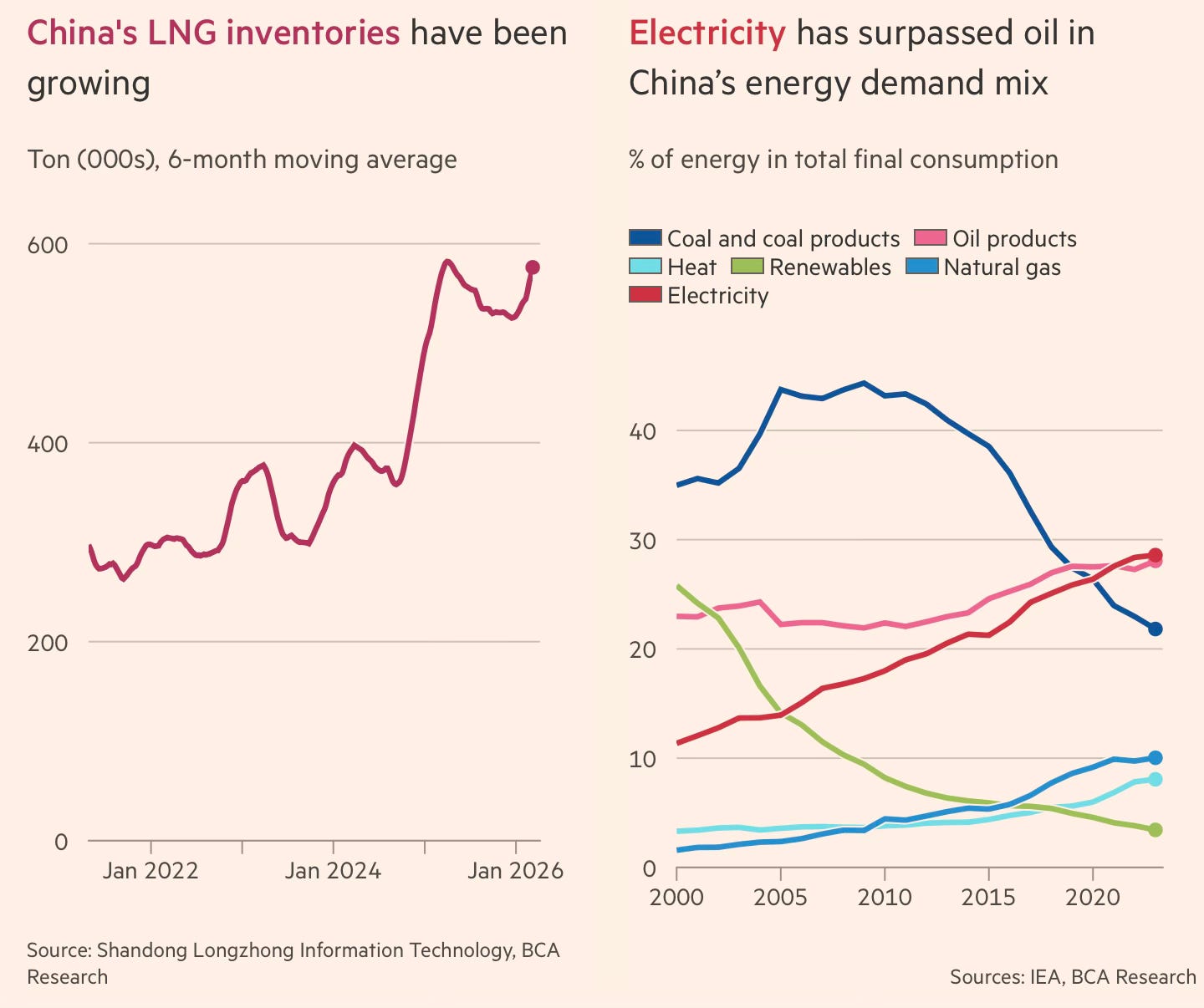

8. While it cannot be said to have emerged as a winner, by staying quiet and allowing its main competitor to make all its mistakes, China may have enhanced its power at least in relative terms. However, due to its own political limitations, it may not have the sagacity to seize the moment.

The war highlighted China’s economic resilience and how it boosts its superpower status. It holds the world’s largest emergency reserves of petroleum, totalling a staggering 1.3 bn barrels. With electricity accounting for 30% of the country’s energy consumption, about 50% higher than the US or Europe, it is significantly insulated from oil shocks. Its firms account for at least 70% of global manufacturing capacity for major green technologies like solar, battery, and EV components, besides also dominating the extraction and refining of rare-earth elements that go into them.

This may well be the most definitive illustration of the declining image of the US and the rising one of China, with the reversals coinciding strikingly with the Trump inauguration.

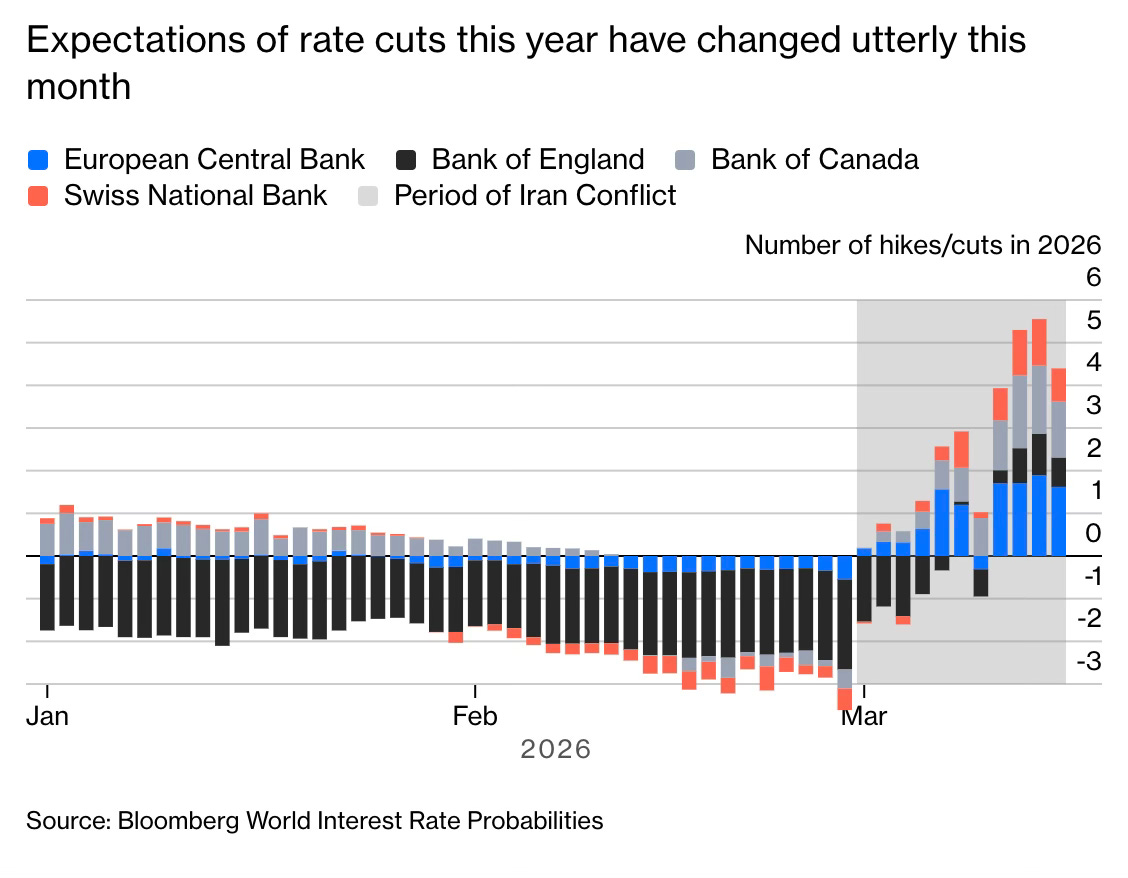

9. On the economic side, the medium-term impact of the war will be on inflation and interest rates globally. The war comes on the back of supply shocks imposed by the Covid 19 pandemic and the Russian invasion of Ukraine. It had taken more than three years for the resultant surge in inflation to decline to normalcy. This process has now been reversed, and with no certainty on what lies ahead (also given the risk that the ceasefire will not hold).

In the US, expectations for at least two rate cuts have declined to just one rate cut. And if the ceasefire is broken and the supply squeeze continues, oil prices will remain elevated, and inflation will surely rise. Instead of rate cuts, the Fed may have to respond with rate hikes. In fact, in Europe, the expectations now are for rate hikes.

10. If one were to look for silver linings, the sheer unpredictability, the staggering hubris, and the utter disregard for all diplomatic norms, the Madman nature of Trump may serve as a deterrent to potential opponents and aggressors. This, coupled with the frightening display of US military prowess and its projection capabilities, is a very important signal. It would be especially relevant to China and any plans it might have to invade and annex Taiwan.

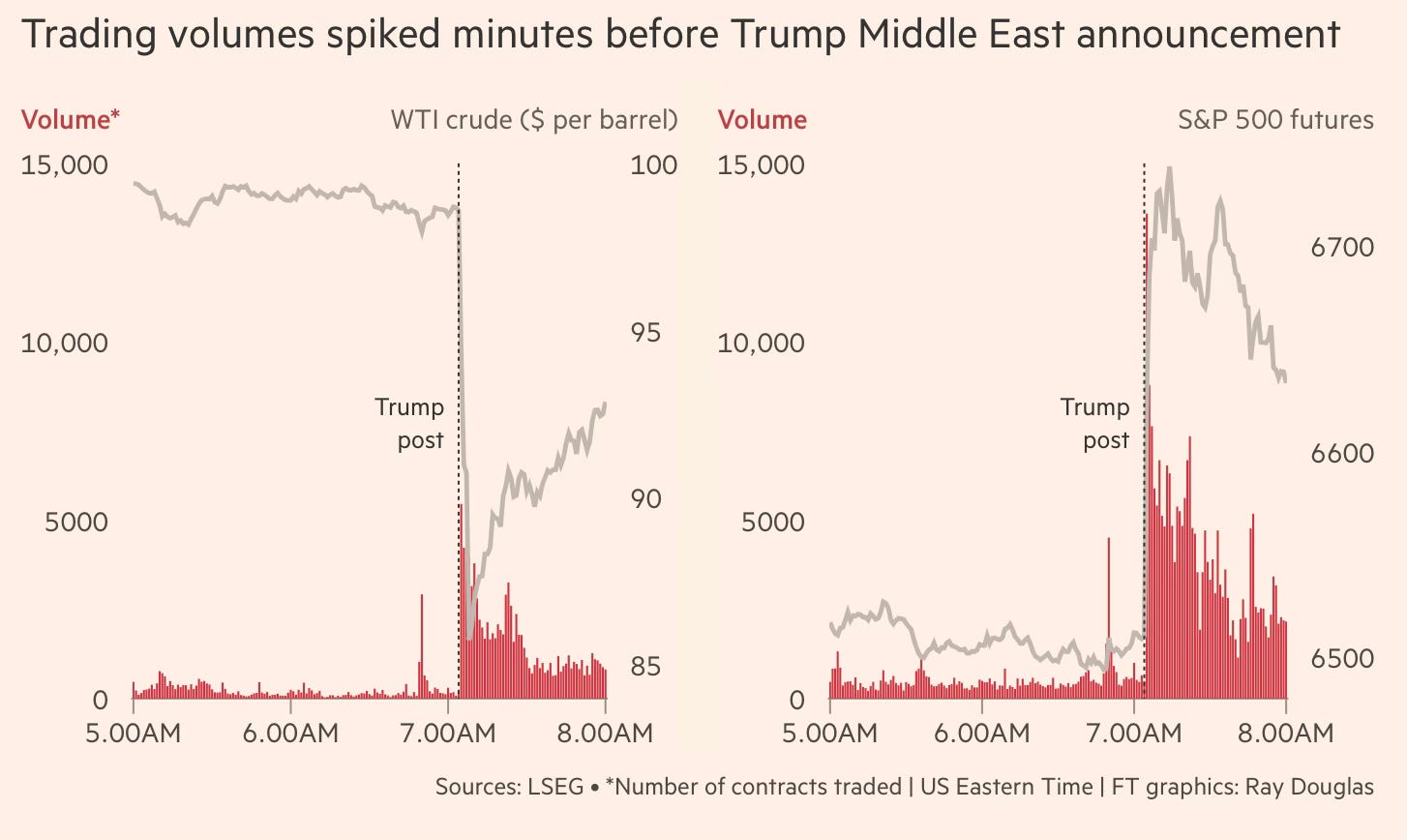

11. The Gulf War has confirmed that the surest test of the TACO (Trump always chickens out) trade is the stock market. Gillian Tett has written, “Donald Trump views equity prices as a key — if not the key — barometer of his success, more than any president before him.” The other TACO triggers are the cascading impact of energy prices on domestic gas prices and inflation. On multiple occasions during the War, including the latest ceasefire, Trump pulled back from the brink as the (equity and bond) markets roiled and threatened to unravel. So much so, one could have predicted with some degree of confidence that the deadline to “wipe out a civilisation” was extreme brinkmanship to extract the maximum concessions before the inevitable pullback.

It is another matter that these Taco episodes may have been used for market abuse and profiteering by those close to the powers that be.

12. The Gulf War offers a reminder that wars have returned to being more common. Conflict zones grew by nearly two-thirds between 2021 and 2024, with 2023 witnessing more violent conflicts than any time since World War II, and over 130 armed conflicts being recorded in 2024, a total that has doubled in just 15 years. There is a greater inclination to use military power to expand national boundaries. This also comes at a time when the Trump administration’s actions have raised serious doubts about the US security umbrella. The Europeans and Japanese, who most benefited from the alliance with the US, are now the most disturbed by the new normal.

All this is unlikely to be lost on countries that the possession of nuclear weapons may offer protection against blackmail and aggression by enemies. It has naturally reignited a wave to go nuclear.

France, whose force de frappe is truly sovereign, said this month that it would increase its stockpile of warheads. In Poland, a rare point of agreement between the prime minister and the president is their openness to going nuclear. In South Korea, public support for a deterrent has gone up to 70 per cent in recent years. Saudi Arabia, which has said that it would get one if Iran did, might not wait for such a cue now that it and other Gulf states are under conventional attack from that quarter anyway. Even the original nuclear powers are chafing at old taboos. As of last month, there is for the first time in over half a century no binding agreement to limit nuclear arms between America and Russia, which have the world’s two largest arsenals.

In 1994, Ukraine gave up the Soviet nuclear weapons that were then on its soil in exchange for certain assurances about its security. Two decades later, Moscow began its long and ongoing war against Ukraine with the annexation of Crimea. The lesson, for some, is obvious. A country with dangerous neighbours should retain or acquire the ultimate deterrent. Another salutary tale is that of Iran. It seems that an unfinished nuclear bomb is the worst of all worlds: a provocation to other states but not a deterrent. A rational government would either abandon all ambitions of that kind or realise them in full.

13. The US-Israeli bombings have clearly been intended at destroying the Iranian economy, achieve through warfare where sanctions have failed. Over 13,000 targets, going beyond military infrastructure, and covering oil and gas facilities, industrial sites, universities, transportation infrastructure have been destroyed in the bombings.

Israeli air strikes forced Iran to shut down its two largest steel plants. One of Iran’s biggest pharmaceutical manufacturers, Tofigh Darou, which produced important cancer treatments, was also destroyed by air strikes last week, the health ministry said. By striking at the heart of Iran’s industrial base, Israel has hit a vital source of non-oil export revenue for the Islamic republic. In the first 10 months of the last Iranian year, which ended in March, non-oil exports totalled $51.6bn, compared with total imports of $58.1bn, according to Iran’s customs administration. Petrochemicals account for nearly half of Iran’s non-oil exports, followed by minerals and industrial goods such as steel… On Monday, Iran accused Israel of striking Sharif University, the country’s most prestigious engineering institute. Last week, Israel bombed Tehran’s more than 100-year-old Pasteur Institute, one of its leading medical research facilities.

This has clearly put the Iranian economy back by decades. The brunt of the economic impact will be on the poor and vulnerable, thereby setting the stage for social discontent at a time of diminished resources and a weakened political system. In the circumstances, any economic recovery cannot begin without some relaxation of the sanctions. It is hard to believe that after such devastation, a country as large as Iran, with 90 million people, can continue to be left as a pariah and squeezed with sanctions, without the political instability spilling over across the region.

14. As the first round of talks has shown, there’s little wiggle room available for both sides in any negotiations. The Iranians cannot settle for anything other than at least some relaxation in the sanctions, at least some assurances in this direction. Further, in light of what has happened, they will find it difficult, even impossible, to now give up on the nuclear deterrent. These are existential issues for the regime. It has chosen to endure the 38 days of bombings instead of acceding to the US demands on the nuclear issue. It is highly unlikely that they will now climb down significantly on this issue after all the losses - over 3500 lives lost, elimination of an entire generation of leadership, and tens of billions of dollars of economic devastation.

This circumscribes the window for negotiations. For one, it would have to be something short of Iran giving up its nuclear option. But Iran will have to concede more than it has so far. The other point concerns the extent of sanctions relaxation. The negotiations cannot move forward if there is disagreement on these basic assumptions. If there’s mutual agreement on the assumptions on both issues, the negotiations would revolve around what would be an acceptable enough climbdown for the two sides.

15. Finally, there are important warfare lessons. The foremost takeaway, reinforcing the impressions from the Ukraine war, is that drones and low-cost ammunition necessitate a reexamination of conventional military strategies. Second, however, this must be contrasted with the importance of advanced technologies in establishing the near-complete air superiority of the US in the two-week war in 2025 and the current war. Third, the reasonably long drawn-out war has given the US armed forces invaluable experience of wartime action, especially compared to the Chinese.

Fourth, the use of AI has reshaped decision-making in wars. The use of Palantir’s Maven Smart System and Anthropic’s Claude model has helped the armed forces rapidly sift through voluminous intelligence data from multiple sources to plan and generate strike options in near real-time. As an illustration, the Pentagon struck more than 2000 targets in the first four days, compared to the six months taken to strike a similar number of targets in Iraq and Syria during the campaign against ISIS. Fifth, the controversy and the tiff between the US Government and Anthropic on the use of AI-generated information to make military decisions highlights the important concern with the use of AI, one that will only increase over time.