1. McKinsey is facing new challenges following the expansion of its digital practice.

In the 2010s, as many chief executives grew increasingly nervous that their companies would be the next victims of digital disruption, McKinsey invested to broaden its offerings. Between 2013 and 2023 it acquired at least 16 specialist technology consultancies, giving it the ability to assist clients not only with their digital strategies, but everything from developing prototypes of new products to building whizzy data-crunching tools. That points to the final source of the firm’s recent expansion, as it has pushed more widely into implementing its own advice. Having counselled a client to spruce up its technology, sharpen its operations or squeeze its suppliers, McKinsey will often now hold their hands through the process. That has meant muscling in on a segment of the consulting market traditionally dominated by Accenture and the “big four” professional-services giants, which charge considerably lower rates, notes Tom Rodenhauser of Kennedy Intelligence. To compete, McKinsey has had to rethink how it charges clients (fees are now often tied to the results of a project) and whom it hires (focusing less on generalists, more on geeks and grizzled executives).

And there's the threat from the newbies like Palantir.

As bosses look to AI to transform their businesses, they are asking McKinsey and other consultancies for help. But they are also turning to less conventional partners. Palantir, an analytics firm, offers tools to feed enterprise data into AI models, and embeds its so-called forward-deployed engineers with its clients to get them up and running. Its revenue is still small (just under $3bn in 2024) but is growing at a blistering pace (48%, year on year, in the second quarter of 2025). Although it began by serving governments, it now makes over two-fifths of its revenue from businesses. Its market value has septupled over the past year, to more than $400bn. Analysts at UBS, a bank, describe Palantir as “McKinsey meets Databricks”, alluding to a software firm whose tools also help enterprises connect their data with AI models. That sounds a lot like QuantumBlack, McKinsey’s own AI unit and the crown jewel of its digital practice. Other AI companies are taking inspiration from Palantir, too. OpenAI, maker of ChatGPT, has begun offering a consulting-like service to help businesses deploy its models.

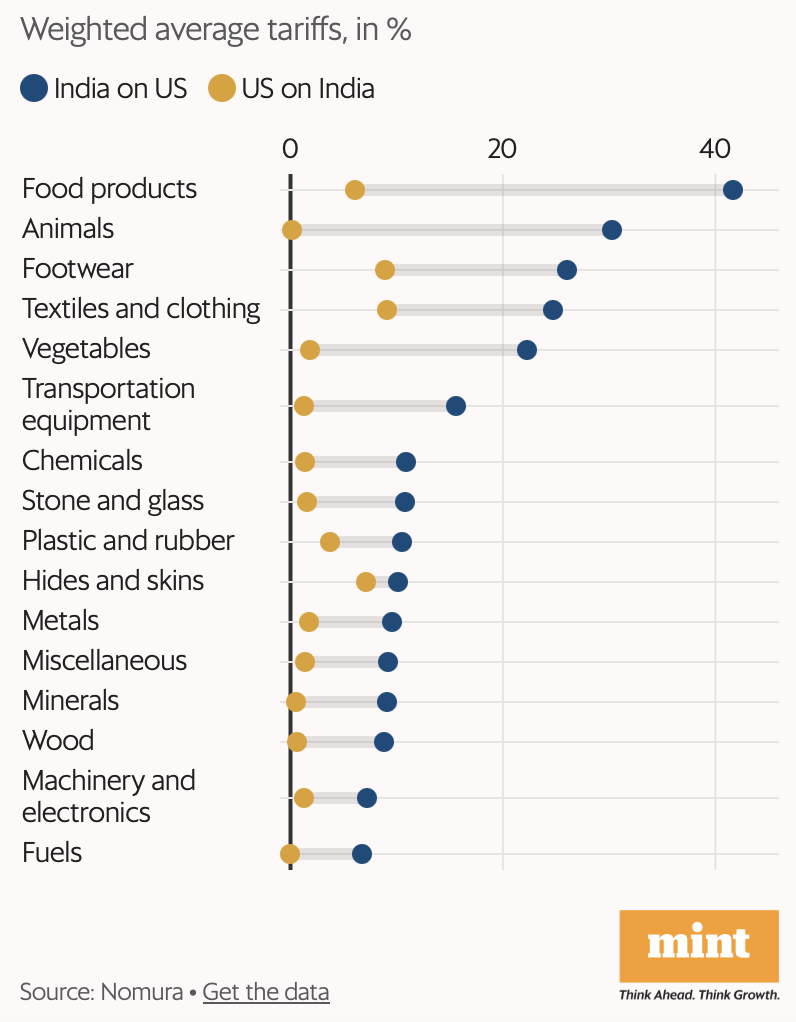

2. Impact of Trump tariffs on India's $86.5 bn exports to the US.

We invest 0.3 per cent of gross domestic product (GDP) in in-house R&D to a world average of 1.5 per cent. Our 10 most successful non-financial firms (highly profitable firms in refining, information technology services and consumer goods) invest 2 per cent of profit in R&D; whereas their 10 most successful peers in the United States, China, Japan and Germany invest between 29 and 55 per cent. And Indian firms are completely missing in five of the 10 most technology-intensive industrial sectors worldwide… Our hundredth largest spending firm invested about ₹97 crore in R&D in 2022–23; our two-hundredth largest, about ₹33 crore; and our three-hundredth largest, about ₹16 crore. These are small numbers relative to the world’s leading firms.

5. China seeks to consolidate its semiconductor chip making industry.

Consolidation in the chip equipment space would help boost China’s bid to build a self-sufficient semiconductor supply chain and replace equipment from US groups such as Applied Materials and Lam Research, said Edison Lee, semiconductor analyst at Jefferies. Currently, a Chinese fab buying local equipment has to use multiple vendors, whose technology is not well integrated. “In the equipment industry, it is difficult to be very successful as a single-product company. Fabs prefer to buy multiple machines from the same vendor, which makes it easier to use,” he added. By consolidating, Beijing also hopes to better direct funding to firms deemed strategically significant... Little progress has yet to be made in consolidating China’s sprawling network of foundries — a segment that remains highly fragmented and politically sensitive. The past decade saw a surge in foundry projects backed by local governments, many of which built capacity in parallel, resulting in a glut of supply of mature chips and steep price competition. Chip experts note that China could also benefit from streamlining its advanced fabrication market, to concentrate talent and the most advanced chip equipment machinery in one place instead of being spread across disparate projects.

6. Some details of where Apple will source its US components from

For example, Apple said that all of its cover glass for iPhones and Apple Watches would be made by Corning in Kentucky, and that it would spend $2.5 billion on that effort... Apple also highlighted its partnership with Coherent, a longtime supplier of lasers for Apple’s facial recognition hardware, which is made in Texas... The iPhone maker said it expanded a partnership with Texas Instruments to make chips in Texas and Utah. Texas Instruments has long supplied chips for the iPhone, such as circuits to control USB interfaces or power displays... Other partnerships are with Applied Materials, a tooling company, GlobalFoundries, a chip foundry, and GlobalWafers America, which is supplying Taiwan Semiconductor Manufacturing Co. and Texas Instruments with made-in-USA wafers, the starting point for a batch of chips. GlobalFoundries manufactures chips for Broadcom, which supplies wireless chips for iPhones. Both will work with Apple to develop and manufacture 5G components in the U.S. Meanwhile, Apple will buy millions of advanced chips made by TSMC in Arizona, where it will be the factory’s largest customer... Apple said it would invest in and become a customer at an Arizona Amkor facility, which packages and tests chips, the final stage before installation in a computer. Apple also said it would expand existing data centers for artificial intelligence in North Carolina, Iowa, Nevada and Oregon.

This is a break-up of Apple's spending a year

In Apple’s fiscal 2024, the company spent $210 billion globally on cost of goods sold, $57.5 billion on operating expenses and $9.45 billion in capital expenditures for nearly $275 billion in global spending during the period.

7. Global rice prices plunge to an eight year low on the back of record harvests and India's resumption of exports.

Indian refiners had gained $16bn in extra profit from importing discounted Russian oil, with almost $6bn of that going to Reliance... Before Moscow’s full-scale invasion of Ukraine in February 2022, India imported a minimal amount of Russian seaborne crude. Indian government data shows it has since bought discounted Russian oil worth nearly $140bn, which Ambani’s Reliance and others have processed into petrol and diesel for sale in both domestic and international markets... the country’s refineries operate by the book and that oil from Russia, unlike Iran and Venezuela, has not been subject to direct sanctions. Washington previously made no objection to the trade, as long as purchases were priced below the $60-a-barrel G7 price cap intended to limit Russian revenues while keeping oil flowing into the global market... Energy Aspects estimates that since the start of the war in Ukraine, India has received an average discount of $11 for each barrel of Russian oil compared with the international price of crude, though the discount has fluctuated and is now about $2 before freight costs.

Yet it is shocking to realise that the medieval feudal lords had more of a stake in ensuring their new towns were sustainable than most property developers today. “The private sector has no financial interest in the sort of heavyweight placemaking you need to build at scale,” argues Hugh Ellis, director of policy at TCPA. “Even mining companies in the 1920s cared more about providing a decent home for their workforce than modern property development does.” Thrift adds: “If you look at the private sector housebuilding model, their necessity is to get the highest possible price for that house on the day they sell it. If it all goes downhill afterwards, it really doesn’t matter, because they’ve gone somewhere else by then.”By contrast, the postwar new towns had a strong stewardship model of “owning the shops in the town centre and the business premises in the industrial area, having that money coming back in and being able to reinvest it for the good of the town and its maintenance,” says Congreve. But Ellis adds that the model “was deliberately broken in the 1980s by an ideological decision to basically vandalise the programme by forcing a fire sale of most of their assets to the private sector”. One reason why Milton Keynes — often held up a model new town — still has such good green spaces is that when its development corporation was wound up in 1992, a trust was created with an endowment to continue to manage the parkland.

10. Turmoil in the Chinese military as Xi replaces officials accused of corruption.

Three of the seven seats on the Central Military Commission — the Communist Party council that controls the armed forces — appear to be vacant after members were arrested or simply disappeared... Mr. Xi has set a 2027 target for modernizing the People’s Liberation Army, or P.L.A... In the first years after Mr. Xi came to power in 2012, he launched an intense campaign to clean up corruption in the military and impose tighter control, culminating in a big reorganization... The most jarring absence in the military leadership is that of Gen. He Weidong. The second most-senior career officer on the Central Military Commission, General He has disappeared from official public events and mentions, an unexplained absence that suggests he, too, is in trouble and may be under investigation. Another top commander, Adm. Miao Hua, who oversaw political work in the military, was placed under investigation last year for unspecified “serious violations of discipline,” a phrase that often refers to corruption or disloyalty. He was among around two dozen, if not more, senior P.L.A. officers and executives in the armaments industry who have been investigated since 2023, according to a recent tally by the Jamestown Foundation. Both men had risen unusually quickly under Mr. Xi’s patronage...

Since Mao Zedong’s era, the military has served not only as a fighting force but also as a lever of political control for Chinese leaders, as their ultimate protection against potential rivals or popular uprisings... Mr. Xi is the only civilian party leader who sits on the Central Military Commission, which ensures his singular power over the military. That also means that he cannot turn to other civilian officials to help him... The purges are likely to disrupt coordination, weaken confidence in commanders and prompt Beijing to be more wary of considering an amphibious assault on Taiwan

11. Excellent NYT editorial video advocating a change in the air ticket tax to fund the Federal Aviation Authority (FAA) that ends up as a case of taxing the regular air travellers to subsidise private jets.

12. How the surge in gold exports provoked Trump's 39% tariff on Switzerland.

America’s trade deficit in goods with Switzerland was just over $38 billion last year. In the first six months of this year, the deficit ballooned to nearly $48 billion... In recent months, two-thirds of Switzerland’s exports to the United States were accounted for by various forms of gold. These bars of gold are often sent from London, a trading hub, to Switzerland, a refining hub, where the metal is forged into bars sized for the standards required by U.S. warehouses and then shipped across the Atlantic. Surging demand for gold in the United States as Mr. Trump threatened to upend the global trading order fueled a spike in Swiss gold imports — and greatly expanded the U.S. trade deficit with Switzerland. Excluding gold, Switzerland’s mammoth pharmaceutical industry accounts for half the value of Swiss products shipped to America. In 2024, Swiss drug companies, which include the pharma giants Roche and Novartis, exported around $35 billion worth of medicines, cancer treatments, vaccines and other drugs.

13. Some facts and observations about GCCs.

There are over 1,000 global organisations that collectively operate over 1,700 GCCs across India. They employ over 2 million professionals. They generate over $40 billion in annual value, set to surpass $100 billion in another five years. So, what’s the problem? Well, most GCCs are technically doing work that could have been outsourced to Indian outsourcers like Infosys, TCS, Wipro, HCL, etc. In fact, GCCs are so successful a strategy that they’re growing much faster than Indian outsourcers. And as if taking away potential revenue from Indian outsourcers weren’t enough, GCCs are now also taking away talent. That’s right. They’re hiring experienced and talented professionals using higher salaries, better brands and the promise of better work.

It's time somebody analysed the nature of the work done by in-house GCCs and that done by outsourced service providers like the Indian software firms. Is it significantly a case of the multinational firm (a) vertically integrating its activities and bringing them in-house, or (b) identifying more outsourceable work and relocating them to India, or (c) doing non-outsourceable, higher-skilled work in India?

14. Fascinating statistic from Ruchir Sharma on wealth-creating companies.

Since 2015, the world has generated a total of 444 companies with average annual returns in dollar terms of more than 15 per cent, and a market cap that today exceeds $10bn. A solid majority of these — 248 — emerged outside the US... Countries such as Japan, Canada, Taiwan, Switzerland and Germany have their fair shares but the big numbers are in China, with more than 30 such compounders and... India has produced 40 steady compounders in that time. Most of the compounders have arisen in manufacturing, tech or finance... More than 50 — and thus more than one in five — of the steady compounders are European. And after a long slumber, signs are emerging of an entrepreneurial awakening: the number of tech start-ups in Europe more than quadrupled in the last decade to 35,000... Since 2015, the global billionaire population grew by 1,200 to over 3,000, and seven out of 10 new ones surfaced outside the US. While the number of names on the Forbes list grew by 70 per cent in America, it grew by 90 per cent or more from India and China to Canada, Israel and even Italy... Another cloak obscuring wealth creation worldwide is the market for private equity, credit and other assets, also widely seen as a US preserve. Nearly half of the $13tn in these private assets, and more than half in categories such as venture capital and infrastructure projects, is held outside the US. Unicorns — private firms valued above $1bn — are not an exclusively American species either; roughly 40 of the top 100 are based in other countries.

15. In a remarkable arrangement, the first such one, Nvidia and AMD have agreed to pay 15% of the revenues from chip sales in China to the US government in return for export licenses for their chips.

The two chipmakers agreed to the financial arrangement as a condition for obtaining export licences for the Chinese market that were granted last week, according to people familiar with the situation, including a US official. The US official said Nvidia agreed to share 15 per cent of the revenues from H20 chip sales in China and AMD will provide the same percentage from MI308 chip revenues... According to export control experts, no US company has ever agreed to pay a portion of their revenues to obtain export licences... Nvidia tailored the H20 for the Chinese market after President Joe Biden imposed tough export controls on more advanced chips used for artificial intelligence.

16. India's exports to the US and their share of the country's exports of those products.

EU defence commissioner Andrius Kubilius told the FT that since Moscow’s invasion, Europe’s annual capacity to produce ammunition had increased from 300,000 to reach about 2mn by the end of this year Rheinmetall’s expansion will account for a big part of this growth: the company said its annual production capacity for 155mm rounds was set to rise from 70,000 in 2022 to 1.1mn in 2027.