The announcement that grocery chain Kroger would be buying Albertsons for $24 bn has raised a controversy. For one, the combined entity would be the second largest supermarket chain in US after Walmart, with 15% of national grocery business, employ over 700,000 people, have over $200 bn in revenue, and more than 40,000 private label brands.

This is the major source of controversy,

The merger announcement said that, as part of the transaction, Albertsons Companies will pay a special cash dividend of up to $4 billion to its shareholders of record on October 24, 2022... This dividend equals about a third of the supermarket chain’s market value. Almost 70 percent of this special dividend will go to its former private equity owners plus Apollo Global Management, which purchased a minority share in Albertsons last year. This will be a spectacular windfall for Cerberus, enriching the PE firm and its owners while putting the future of the Albertsons chain and its workers at risk... While the general view of financial markets is that the FTC and the courts will not let the merger go through, the payment of this special dividend sets Albertsons up for failure and provides Kroger with a powerful “failing firm” defense of its merger proposal. Kroger can argue that Albertsons will face bankruptcy if the merger is not approved.

Matt Stoller points to the problems with the $4 bn special dividend,

The problem is that in this case, that cash is pretty much all the liquidity that Albertsons has. According to the firm’s latest 10Q, Albertsons has $3.213 billion of cash and $565 million of receivables, which can be quickly sold to raise cash. There’s your special dividend right there.

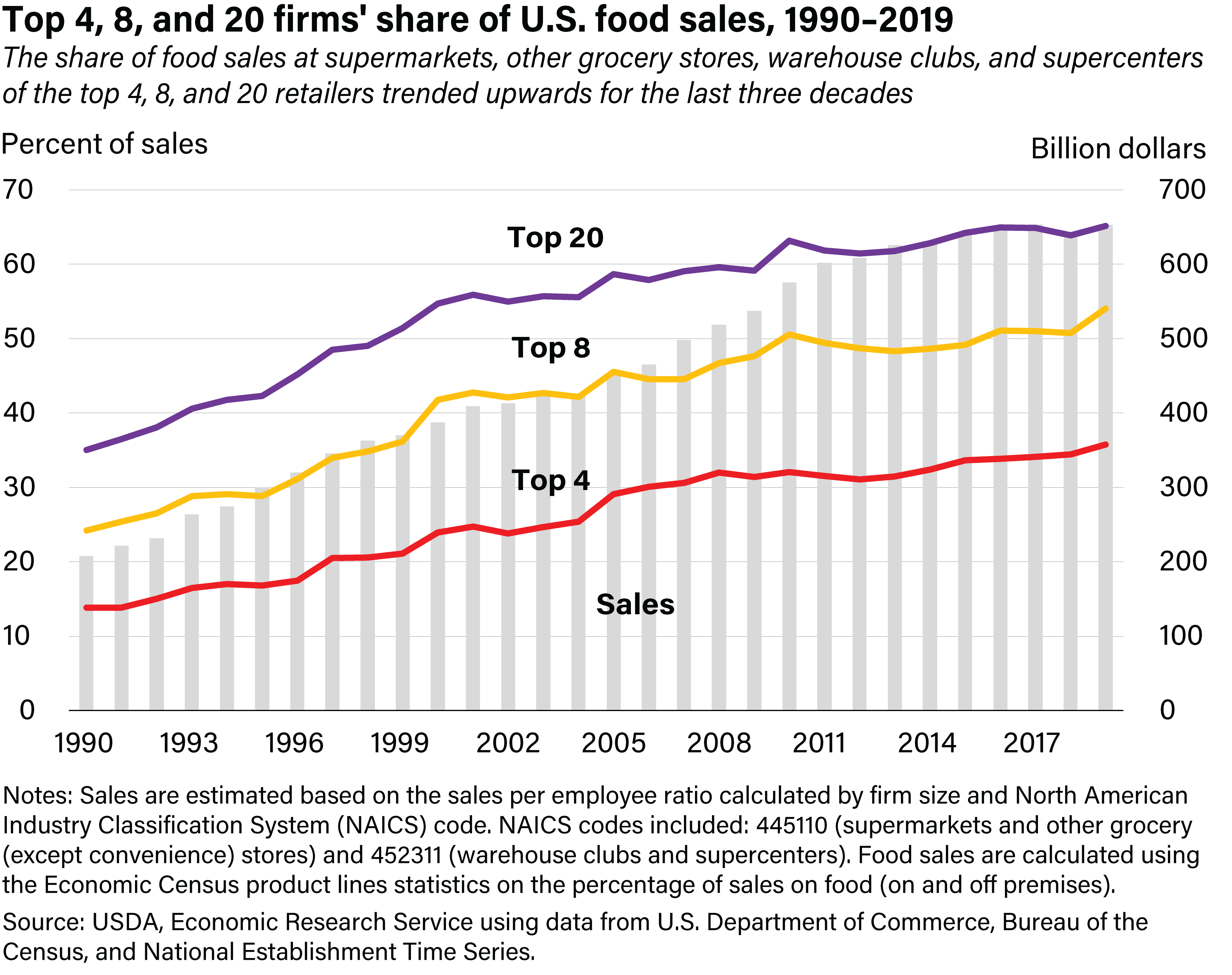

He also writes that the merger is the latest in a trend over the last thirty years whereby supermarket chains have consolidated the nearly $1 trillion grocery industry, which provides the source for what Americans eat. The consolidation in the industry has been steep.

{kind=link}

There has been tremendous concentration on both a national and local level already. As Errol Schweizer at Forbes noted in an excellent piece published immediately after the deal came out, “There are already 30% fewer grocery stores than a few decades ago and most major metropolitan areas (with the exception of New York City) are heavily concentrated among just a handful of grocery chains.” That means large chains not only secure better prices for goods than their smaller counterparts, but can also increase prices faster than costs, contributing to inflation. Suppliers, consumers, and workers will all feel the pressure from Kroger/Albertsons, and since suppliers buy from farmers, farmers will feel it too, at least indirectly...There will be layoffs in white collar jobs such as “office-based marketing, procurement, analytics, digital sales and category management roles,” which the firm calls ‘synergies.’ Kroger will have more bargaining power over suppliers, as it will have 5,000 stores and can “more easily set payment terms, negotiate shelf space and assortment, and extract better costs and greater trade allowances for promotions, couponing, ad placement and slotting fees.” In addition, deals like this concentrate grocery shelves with the goods of certain dominant firms in packaged foods categories, such as “Pepsico, Kraft Heinz, Nestle and Kelloggs, as well as meat and poultry barons such as Tyson, JBS and Smithfield, centralizing industrial agricultural supply chains.” This will further centralize the food supply overall and could potentially prevent the stocking of more seasonal and local food. Finally, Kroger and Albertsons are combining their data hoards and advertising network, which could be quite significant.

The deal attracted action from state governments across the US. A group of six state attorneys asked Albertsons to delay the payment of $4 bn dividend until officials reviewed the deal. Albertson's rejected the request saying that the dividend was part of a strategy to return capital to shareholders and was not part of the merger. The attorney's approached a Washington state court which has, in a very rare step, temporarily blocked the dividend payout.

No comments:

Post a Comment