Today’s two dominant organisational forms are practically the same: the one-man autocratic state and the one-man autocratic company. Both have the same vulnerability: the idiosyncrasy of an overpraised loner... One-man states and one-man companies have similar cycles. At first, even if the autocrat’s aim is self-enrichment, he wants approval, so he avoids self-sabotage. Being unbound by rules, he seems more agile than his collectively ruled rivals. With success, he acquires an aura. He stabilised Russia/invented Facebook/built electric cars. Why, he’s a genius! If he wants to become president for life or assign himself stock with 10 times the voting rights of other shares, well, what could possibly go wrong? Having defied gloomsters the first time around, the autocrat ignores them the second time But the initial success was generally due to a unique confluence of luck, person and moment. Few humans are two-trick ponies. Worse, hubris takes hold. Having defied gloomsters the first time around, the autocrat ignores them the second time...The investor Chris Sacca tweeted last week: “One of the biggest risks of wealth/power is no longer having anyone around you who can push back . . . A shrinking worldview combined with intellectual isolation leads to out-of-touch shit . . . I’ve recently watched those around him become increasingly sycophantic and opportunistic . . . agreeing with him is easier, and there is more financial & social upside.” Sacca was talking about Musk but he might as well have meant Putin.

3. The UK government has announced windfall taxes on oil companies who have raked in multi-billion dollar profits from the high oil and gas prices even as governments struggle to subsidise consumers,

The logic seems straightforward. Energy suppliers are benefiting from an unexpected bonanza because of Europe’s sudden move away from Russia’s gas and oil after its invasion of Ukraine, as opposed to any savvy strategy by the companies themselves. Shell, based in London, recently reported that it had earned $20 billion in just six months, its biggest haul on record, while BP earned $16.6 billion. TotalEnergies, based in Paris, reported profits of nearly $29 billion over the same period. American energy companies are also taking in gobs of profit. Net income for the world’s oil and gas suppliers will reach $4 trillion, the International Energy Agency estimated, double last year’s total...

On Thursday, Jeremy Hunt, Britain’s chancellor of the Exchequer, announced that he would raise $16.5 billion next year by increasing the windfall tax on oil and gas companies to 35 percent from 25 percent and introducing a temporary 45 percent levy on electricity producers. Many of these producers — including those that use solar, wind and nuclear power — have enjoyed enormous profits even though their costs haven’t increased. The European Union last month announced a temporary tax — euphemistically labeled a “solidarity contribution” — on some fossil fuel producers. An additional 33 percent levy will apply to “surplus” profits and is expected to raise $145 billion. There is also a cap on electricity profits. Individual nations have gone further. Last week the Czech Parliament approved a measure to impose a 60 percent tax on energy companies’ and banks’ windfall profits. Germany is considering taxing by 90 percent profits that electricity companies generated above the cost of production...

Yet as several economists have pointed out, whatever the drawbacks, a windfall profit tax makes the most sense when energy companies are making gargantuan profits and families and businesses are facing financial ruin from staggering energy costs. Concerns about crimping investment may also be overstated, they noted, when so many of the oil and gas companies are using the newfound revenue to increase payouts to shareholders and buy more of their own stock to nudge up its price... In a survey of more than 30 European economists conducted in June by the University of Chicago Booth School of Business, half agreed that a windfall tax on excessive oil and gas profits should be used to help households afford high energy costs. Seventeen percent were opposed, while a third were undecided.

Spain followed suit with its lawmakers approving imposition of windfall taxes on banks and energy companies.

Spain wants to raise a total of €3bn from big banks over the next two years via a 4.8 per cent tax on their income from interest and commissions. From utilities, it is aiming to raise €4bn over the same period with a 1.2 per cent tax on their sales.

4. The hypocrisy surrounding calls to boycott the Qatar World Cup because its stadium construction involved exploited migrant labour is staggering. For countries which have a history of colonial exploitation of the worst kind, and that too not many decades back, and which have supported much worse Chinese genocide in Xinjiang, this concern is very rich. Gianni Infantino was right to call this out.

Worst of all, the arguments about LGBT rights etc can rightfully be construed by Qataris as an attempt to impose emerging western cultural norms on the Conservative Qatari society.

5. FT has a long read which highlights Apple's dependency on China,

Apple’s reliance on the country as its manufacturing base — with responsibility for 95 per cent of iPhone production, according to Counterpoint, a market intelligence group — leaves the business vulnerable to supply chain shocks... Operating profits in greater China — which includes Hong Kong, Macau, Taiwan and mainland China — have shot up 104 per cent over 24 months to $31.2bn in the financial year to September, eclipsing the $15.2bn earned by Tencent and the $13.5bn from Alibaba in their most recent 12-month period, according to S&P Global Market Intelligence... As Huawei’s share of the Chinese market plummeted from a high of 29 per cent in mid-2020 to just 7 per cent two years later, Apple’s share jumped from 9 per cent to 17 per cent, according to Counterpoint. Virtually all of the US group’s sales were in the premium segment, where its dominance climbed from 51 per cent to 72 per cent in three years.

6. Fascinating twitter thread on how Peru has in less than 10 years risen to become the world's second largest blueberry grower and largest exporter (HT:Adam Tooze).

Carlos Gereda was the spark that lit Peru's blueberry boom of the past decade. He asked a simple question: "can blueberries grow in Peru?" In 2006, he brought 14 varieties from Chile to see which ones adapted well to the Peruvian climate. He narrowed it down to four and, in 2009, founded Inka's Berries. The company's service consisted of assisting the development of plantations that adhered to the growing standards Carlos had conceived. The blueberry revolution ensued. In a very short time, Peru became the world's number two producer of blueberries and the world's number one in exports and per capita production. Seriously, the growth resembles that of bitcoin's value. In 2010, Peru produced 30 tons of blueberries; in 2020, 180K. This new industry ($1B in 2020) that was born seemingly out of nowhere is being led by corporations that can afford the high cost of entry. Most notably, Camposol and Hortifrut hold a combined 34% of the market. Peru's climate allows for year-round production, giving the country a competitive edge over seasonal agriculture. The productivity of Peruvian land is 13 tons per hectare. The world's top player, the USA, produces 8 tons per hectare.

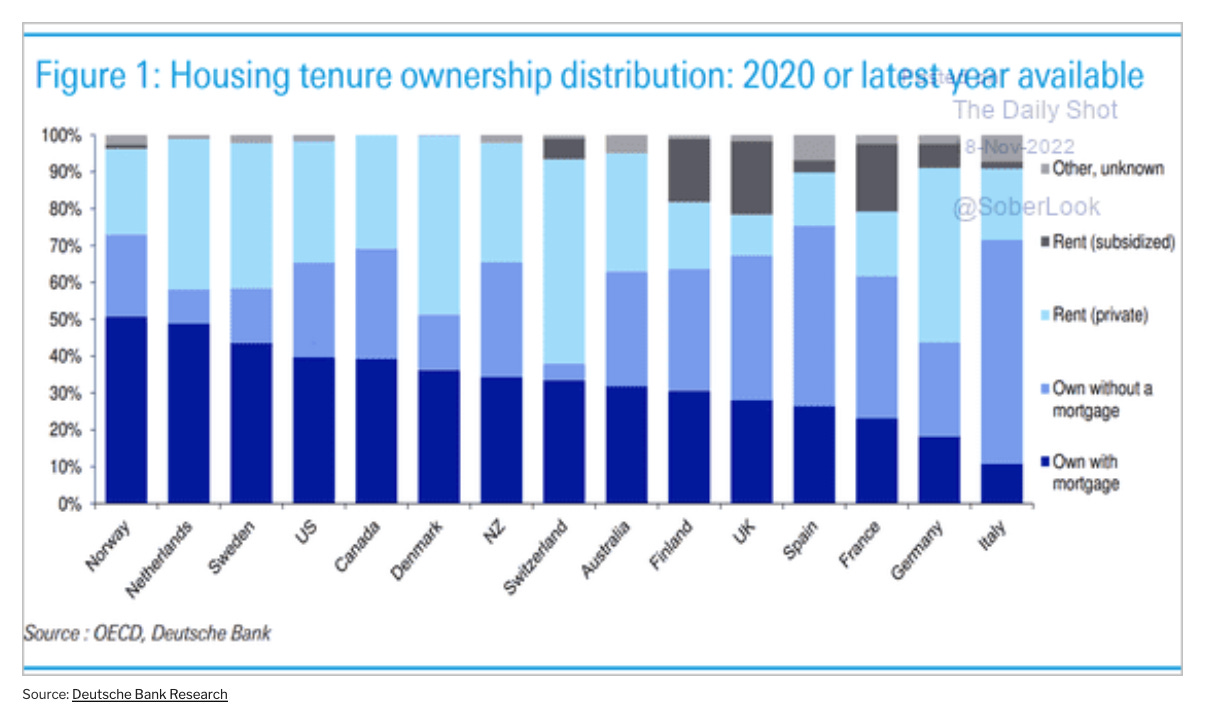

7. Housing tenure ownership patterns across advanced economies

{kind=link}

Visa last month reported annual net income of $15bn, up 21 per cent year on year. Both it and Mastercard are trading close to record highs. They have a combined market cap of $765bn, unchanged over the past year, even as the broader market has declined sharply. Ironically, it is the challengers, big and small, that are suffering more. The core explanation is simple: even the smartest fintechs are not fundamentally disrupting the market; they are merely slotting themselves into the existing payments architecture. Yes, they may make life easier for the consumer or the merchant with faster back-end processing or slicker point of sale interfaces. But this is not at the expense of Visa and Mastercard, whose electronic “rails” they nearly all rely on. The big old card companies might look ripe for disruption, facilitating as they do high “interchange” fees levied via merchants (averaging 2 per cent in the US). But thanks to the spread of their operations into every corner of the world, it has been either impossible or economically unappealing for potential competitors to build new kinds of networks.

9. Agricultural crop yields in India remains much lower than elsewhere

Soy yields in India are three-four times lower compared to the US and Argentina, while mustard yields are almost half compared to canola grown in Canada (mustard and canola belong to the same Brassica genus). India imports both varieties of edible oils to meet its large domestic shortfall. India is among the top producers of cotton in the world but yields are less than a fourth when compared to China. Average rice yields in India are 57% of China and lower than even Bangladesh and Vietnam. India is the largest producer of milk in the world but cattle milk yields (per animal per year) are 60% of China and less than a fifth of the US.

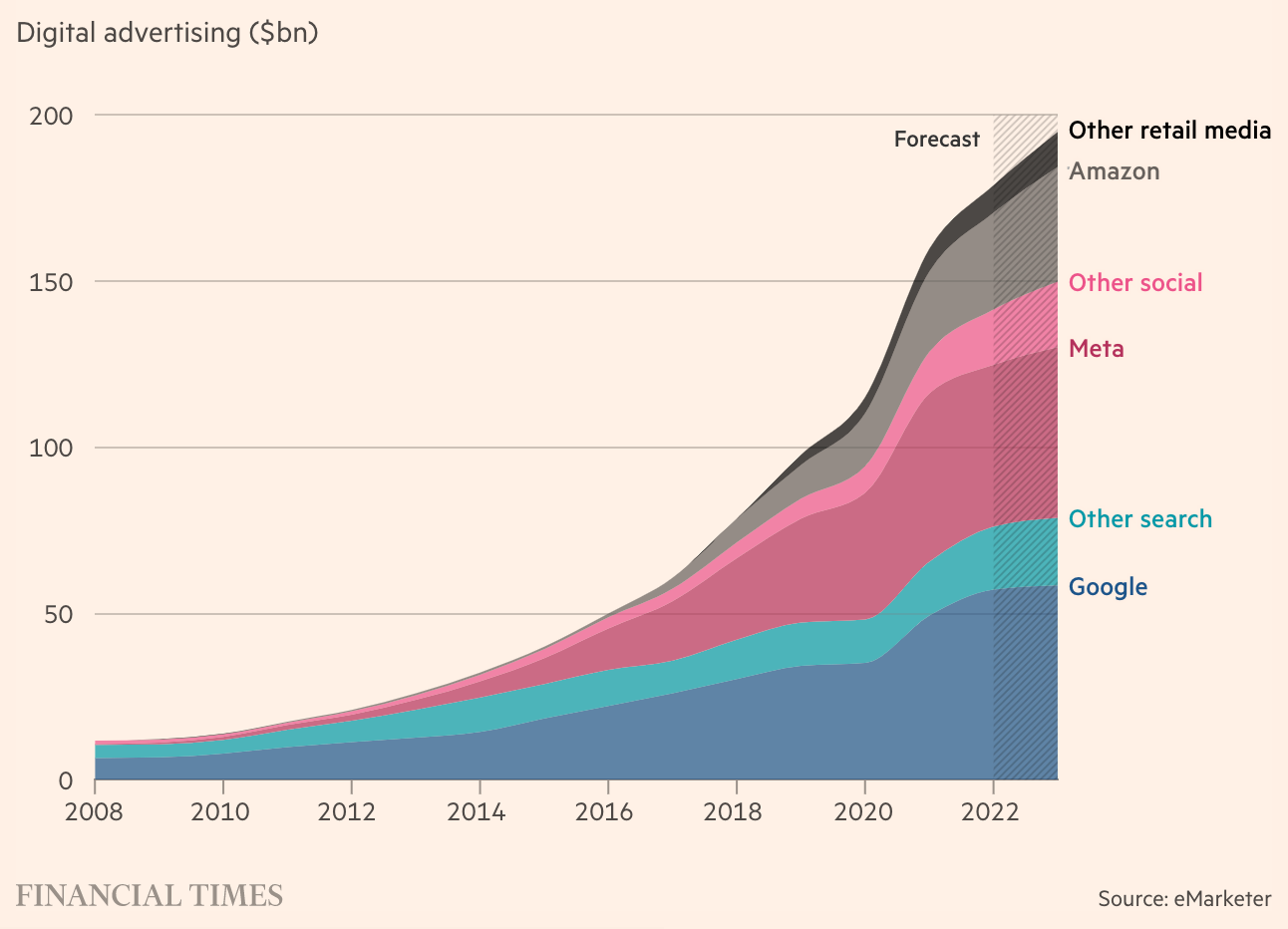

Amazon’s earnings report showed that its revenue from advertising was higher than fees from its Amazon Prime membership scheme, audiobooks and digital music combined, as well as more than twice the sales from its physical stores, including the Whole Foods grocery chain.

11. Bradford De Long makes an important point about the inflation target,

I think that [former Federal Reserve chair] Paul Volcker, who’d stopped [tightening monetary policy] when inflation was down to 4 per cent, was right. And Alan Greenspan [his successor], who said we should be happy that it has fallen to 2 per cent and stick there, was wrong. You really do, given the difficulties and getting your fiscal policy ducks in a row, want to have the ability to deliver a major stimulus to the economy when it falls into recession, to be able to cut interest rates by five percentage points or so. It really does require that the average inflation rate be something significantly higher than two, for interest rates to be in a configuration so that you can respond, rather than finding yourself once again at the zero lower-bound and you’re unable to convince people to spend to get the economy back to full employment. That reversing the shift from Volcker’s 4 per cent to Greenspan’s 2 per cent is something that really needs to be done.

He admits that the Russian invasion may have had the effect of raising inflationary pressures, but also feels that some inflation post-pandemic may be useful,

Right now, we have succeeded in reopening the economy after a plague, in a different, much more delivery-and-goods-production orientation, relative to in-person sales. More people driving delivery trucks, making goods and programming websites than before. And as always, when you wheel the economy into a new configuration — 1947 and 1951 are my stock examples — you need a little bit of a burst of inflation to grease things. If things go well, you just get a short transitory burst, after which things return to normal because everyone understands that this isn’t that monetary policy has lost its anchor. It’s more that the market economy is doing its thing by putting high prices on things that are [stuck in] bottlenecks. And offering higher wages to workers who will move into expanding industries.

12. Finally, Hal Brands has a series of articles on the importance of a US-led Indo-Pacific alliance involving Japan, India, Australia, and UK in deterring any Chinese invasion of Taiwan. He quotes US officials in pointing to the possibility of a war in 3-5 years. He writes,

A war that the US fights in the Western Pacific without allies is a war it runs a very high risk of losing. A war that it fights at the head of a large democratic coalition is one China probably cannot win. The more Beijing fears the latter scenario, the better deterred it may be from using force in the first place. The Chinese-American rivalry is a contest for Indo-Pacific hegemony. But in what they do and don’t do, an array of middle powers will have their say in who wins.

So how might India react if China attacked Taiwan? Although India can’t project much military power east of the Malacca Strait, it could still, in theory, do a lot. US officials quietly hope that India might grant access to its Andaman and Nicobar Islands, in the eastern Bay of Bengal, to facilitate a blockade of China’s oil supplies. The Indian Navy could help keep Chinese ships out of the Indian Ocean; perhaps the Indian Army could distract China by turning up the heat in the Himalayas. Even short of military assistance, India could rally diplomatic condemnation of a Taiwan assault in the developing world...New Delhi has a real stake in the survival of a free Taiwan. China has a punishing strategic geography, in that it faces security challenges on land and at sea. If taking Taiwan gave China preeminence in maritime Asia, though, Beijing could then pivot to settle affairs with India on land... a world in which China is emboldened — and the US and its democratic allies are badly bloodied — by a Taiwan conflict would be very nasty for India... What India would do in a Taiwan conflict is really anyone’s guess. The most nuanced assessment I heard came from a longtime Indian diplomat. A decade ago, he said, India would definitely have sat on the sidelines. Today, support for Taiwan and the democratic coalition is conceivable, but not likely. After another five years of tension with China and cooperation with the Quad, though, who knows?

The Economist has an article which describes India's foreign policy as "reliably unreliable"

Ever since India won independence in 1947 its foreign policy has prioritised developing its economy, defending its territory and maintaining influence and stability in its neighbourhood. And it has done so imbued with a profound fear of being dominated by a more powerful country as it was for so long.

No comments:

Post a Comment