The annual Asian Development Outlook 2012 (pdf here), which talks about rising inequality in Asia, has some interesting graphics about the Indian economy, especially in comparison to its counterparts in emerging Asia.

Note the sharp fall in investment as a contributor to GDP growth in 2011. Though government consumption has contracted, so has private consumption. Interestingly, the share of private consumption has risen in China.

The Reserve bank of India (RBI) has been easily the most aggressive Asian central bank. It cut interest rates vigorously when the recession struck and raised rates with similar aggression when inflationary pressures became unhinged. On the positive side, there exists considerable cushion for monetary easing if the RBI feels inflation is under control.

The Reserve bank of India (RBI) has been easily the most aggressive Asian central bank. It cut interest rates vigorously when the recession struck and raised rates with similar aggression when inflationary pressures became unhinged. On the positive side, there exists considerable cushion for monetary easing if the RBI feels inflation is under control.

But inflation in India has been a persistent problem for the past four years. India's current inflation rate is more than twice that of any other major Asian economy. This means that the RBI will remain reluctant to indulge in any significant monetary easing anytime in the immediate future. At best, it is not likely to raise rates any further.

But inflation in India has been a persistent problem for the past four years. India's current inflation rate is more than twice that of any other major Asian economy. This means that the RBI will remain reluctant to indulge in any significant monetary easing anytime in the immediate future. At best, it is not likely to raise rates any further.

I have blogged earlier that the inflationary pressures were clearly the

result of an overheating economy. As the graphic shows, the Indian

economy's scorching pace of growth in the mid-2000s blazed the economy

well beyond its potential output frontier. Though growth has slowed, it

is now merely at its potential output frontier. This is yet another

reason why the RBI may desist from moving down the path of monetary

accommodation. Massive investments to ease the supply side is the need

of the hour.

I have blogged earlier that the inflationary pressures were clearly the

result of an overheating economy. As the graphic shows, the Indian

economy's scorching pace of growth in the mid-2000s blazed the economy

well beyond its potential output frontier. Though growth has slowed, it

is now merely at its potential output frontier. This is yet another

reason why the RBI may desist from moving down the path of monetary

accommodation. Massive investments to ease the supply side is the need

of the hour.

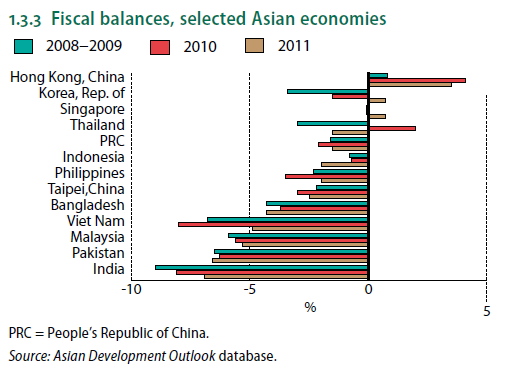

However, the government appears to have limited fiscal space to play an aggressive role in any supply side easing. India is easily the most fiscally constrained country among all major Asian economies. This means that two things will have to happen simultaneously. One, fiscal spending on subsidies will have to be reined in and the savings routed into infrastructure, agriculture, human resource development and so on. Two, private investments will have to be catalyzed in large amounts. Foreign capital investments will have to supplement the domestic private partners in boosting private investment in the economy.

The graphic below highlights the nature of distribution of gains

between labour and capital. In the period 1990-2007, while real wage

rate did not even double, labor productivity increased three-fold, from

about 80,000 to about 250,000 rupees. In fact,

the average annual growth rate of labour productivity was 7.4% during

1990–2007, while the average annual real wage growth rate was only 2%.

This implies that gains in productivity were not passed on to wages and,

consequently, the labor share of India’s organized manufacturing sector

declined significantly.

The graphic below highlights the nature of distribution of gains

between labour and capital. In the period 1990-2007, while real wage

rate did not even double, labor productivity increased three-fold, from

about 80,000 to about 250,000 rupees. In fact,

the average annual growth rate of labour productivity was 7.4% during

1990–2007, while the average annual real wage growth rate was only 2%.

This implies that gains in productivity were not passed on to wages and,

consequently, the labor share of India’s organized manufacturing sector

declined significantly.

Note the sharp fall in investment as a contributor to GDP growth in 2011. Though government consumption has contracted, so has private consumption. Interestingly, the share of private consumption has risen in China.

However, the government appears to have limited fiscal space to play an aggressive role in any supply side easing. India is easily the most fiscally constrained country among all major Asian economies. This means that two things will have to happen simultaneously. One, fiscal spending on subsidies will have to be reined in and the savings routed into infrastructure, agriculture, human resource development and so on. Two, private investments will have to be catalyzed in large amounts. Foreign capital investments will have to supplement the domestic private partners in boosting private investment in the economy.

No comments:

Post a Comment