A very informative report on profit shifting by multinational corporations and rich individuals has been published by EU Tax Observatory.

As financial markets have globalised, the share of global household offshore financial wealth (bank deposits, equities, bonds, and mutual funds held outside the country) has risen.

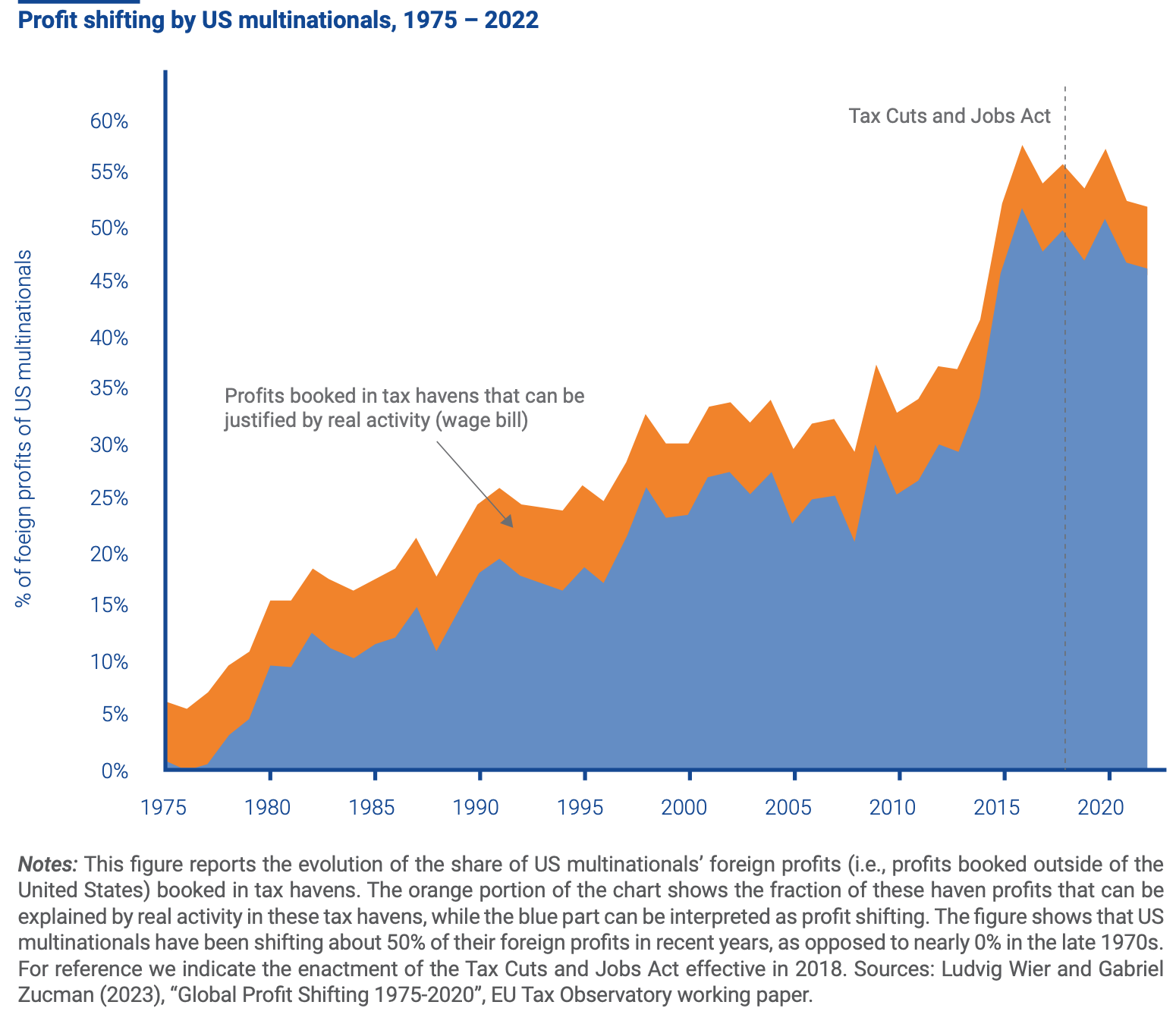

A snapshot of the global profits shifting in 2022 shows that of the 18% of foreign profits, a third is shifted to tax havens, and the effective corporate income tax paid is 17%.

Netherlands, Ireland, and Switzerland have consistently stood out as the largest profit-shifting destinations for multinational corporations. And in the case of the first two, the amounts have been rising over the years.

Ireland is the standout rogue economy on profit shifting.

Reflecting an extremely regressive taxation system, billionaires enjoy the lowest tax rates.

The wealthiest French billionaires are large shareholders of publicly listed, dividend-paying corporations. Yet, they do not appear to pay significant amounts of income tax, suggesting that their dividends go largely untaxed. How is this possible? In a nutshell, the dividend tax can be avoided by owning shares indirectly through a personal wealth-holding company. Dividends paid out to individuals directly cannot avoid or evade the income tax (which is withheld at source in France). The direct shareholder of a company like LVMH pays, in general, a 30% tax on the dividends distributed by this company (although exceptions exist, for instance for shares held on tax-favored saving accounts). But the mere act of interposing a holding company can be enough to avoid the tax. The use of such holding structures appears systematic among French billionaires...The fundamental problem is that income flows are difficult to measure and tax for very wealthy individuals, who can easily structure their wealth so that it does not generate much taxable income. In the United States, billionaire owners of listed companies sometimes instruct these companies to retain all their earnings, making it possible for their shareholders to avoid the individual income tax without the need for interposing a holding. The most famous example is probably the example of Warren Buffett, the main shareholder of Berkshire Hathaway, a listed company that has never paid any dividend. But some of the largest businesses in the United States do not pay dividends too, including Amazon, Facebook, and Alphabet, allowing their owners (such as Jeff Bezos, Mark Zuckerberg, Sergei Brin, and Larry Page) to benefit from relatively low effective income tax rates.

The gains for some countries from the implementation of the two pillars of Base Erosion and Profits Shifting (BEPS) project of OECD are as follows.

Interesting that Indians are the largest foreign owners of real estate in Dubai, one of the major tax havens.

No comments:

Post a Comment