Donald Shoup, the famous urban planner, posed this great question that goes to the heart of infrastructure finance: “How do you finance a project that has a return much higher than its cost, but nobody wants to pay the upfront cost?”

The answer lies in land value capture (LVC), a topic that I have blogged on numerous occasions (see here and here). Specifically, two instruments, betterment levy on existing developed properties, and impact fee on those which are undergoing development, have the potential to raise significant revenues.

In theory, LVC spans the spectrum from appropriating directly through ownership of a part of the developed land (through the likes of land pooling) and indirectly through one-time and/or recurring charge (betterment levy or impact fees).

The former, the best example is Gujarat’s historical town planning schemes (TPS), is perhaps the most ideal approach, insofar as it cleanly appropriates a share of the land itself (typically 40-60% of the total land). The problem is that it is an engagement-intensive activity requiring both high credibility and state capability, both deficient across state and local governments. The best illustration of this is Andhra Pradesh’s struggling experiment to develop its capital at Amaravati by pooling land through a TPS.

TPS entails that the state takes over the lands, develops infrastructure, and leaves developed plots for the landowners, all this within some defined period of time. The combination of the political economy of real estate and weak state capability creates a time inconsistency problem that erodes the credibility associated with such schemes.

It is also for this reason that, despite numerous efforts over the last three decades, there are still very few instances of genuinely successful slum housing redevelopment schemes in Indian cities. And there are numerous examples of badly delayed and poorly executed such projects.

In the circumstances, the best bet with LVC in the context of countries like India is to collect a share of the incremental value as a charge on some urban planning instrument. It is the instrument with the fewest implementation difficulties.

Consider the numerous ongoing infrastructure projects across the country, ranging from national highways and expressways to metro railway projects, airports and ports, data centres and industrial clusters, and generally any large investment that leads to the development of an area. In all these cases, there’s an immediate spike in property prices, which is almost completely appropriated privately. If some share of the property valuation increase can be appropriated through the LVC instruments, then it can be securitised to fund the projects themselves, at least a significant share of the cost.

Illustrative examples will include the nodes in the Delhi-Mumbai industrial corridor, stations in the Mumbai-Ahmedabad high-speed rail and the Regional Rapid Transit System(RRTS), vicinity of Navi Mumbai Airport, the corridor abutting Bharatmala pariyojana, the vicinity of several new airports like Jewar and Bhogapuram, and so on. None of these has any specific betterment levy or impact fee charged on properties in their influence zones. These are all massive missed opportunities and large revenues foregone.

The formally reported claims of LVC revenues from all these are either in the form of unlocking value through sales or lease of government properties, or, in a few cases, they include the sale of lands acquired through TPS.

In every one of these projects, the intent of capturing land-value gain from the project announcement onwards exists somewhere on paper. In practice, though, the only meaningful capture has come from in-kind land pooling, lease revenue/premia from sale of publicly-owned land, and a few development/impact-fee tweaks. The second one (lease revenue or premiums from sales of public lands) is pure monetisation and should not be confused with LVC.

A true betterment levy or impact fee, in the form of a charge on existing private property in the influence zone, payable from the first transaction after project announcement, has effectively not been deployed at scale in any of these projects. Therefore, the aggregated, publicly disclosed revenue from "pure" LVC instruments (betterment levy + impact fees, excluding land sales/leases/concession fees/toll/UDF) is very small, even negligible, relative to project cost in every case here. The genuine “capture” that has occurred is overwhelmingly through public-land monetisation or in-kind retention of pooled land, where the former leaves the increment on third-party private property untouched.

Perhaps the only true significant examples in India are the impact fees in a corridor of 1 km abutting the Hyderabad Outer Ring Road (ORR) (though its success in terms of realisation is a matter of debate), and the 1% metro cess on property purchases in Mumbai to fund the metro railway project. A promising effort with the Navi Mumbai Airport Notified Area (NAINA) was that of the 50% betterment levy on the increased property value notified in 2013, which was immediately reduced to a notional 0.05% following political opposition.

The political economy is an important consideration. Every such big public investment immediately invites large speculative purchases, especially by politically and bureaucratically connected individuals. They are an important sink for the large volumes of black money that slosh around the local economy. Vast sums are invested in the name of third parties (benamis) who front the local connected and influential. Throwing sand in the wheels of this speculative activity, much less appropriating a part of the windfall increments as public revenues, will be resisted to the hilt by the aggrieved interests.

It is therefore important to be careful while designing the LVC instrument. It should depend on the nature of the infrastructure project. The objective should be to capture the increment in land value that the incumbent land owner enjoys from the public investment by charging the first transaction after the project announcement (which triggers the spike). Ideally, it should also try to avoid penalising the buyer, who has internalised and paid for the land increment. However, if the increment is ongoing, like with a corridor that undergoes continuous development, there’s a case for also capturing the increment flows over time through an appropriate instrument.

It is also important to differentiate between brownfield (betterment levy) and greenfield (impact fees) areas.

Accordingly, the most appropriate betterment levy on existing (developed or brownfield) property owners (who are not likely to transact) comes from a cess on their property taxes. In theory, if the property taxes are indexed to the market value, there would be no need for a separate cess. However, this is never the case since the property prices are generally linked to the guidance or ready reckoner rates fixed by the local authorities, which are always lower than the market value, and the wedge widens after local property booms.

For properties undergoing development, the ideal option would be to charge from those selling the property. However, this is complicated and can be captured, and that too only partially (given the aforesaid wedge between market value and guidance value) from capital gains taxes. Administering this is infeasible (imagine two kinds of capital gains tax for land, where there’s land value increment from public investment and the rest). In the circumstances, for such properties, the options are to levy a charge on either the registration fees, the change of land use fees, the layout development fees or the building permission fees. The assumption would be that the charge shapes market expectations and cascades across the property market and is internalised by everyone in the property transactions chain.

It may be useful to keep in mind some principles while designing the LVC instrument. In theory, it can be charged on the first transaction for a property in the influence zone after the project announcement as a significant windfall fee, or on all transactions for a period (that reflects the time for the project to realise its benefits). A simple and practical strategy would be to impose a one-time cess (on the property value) on the first transaction on the property. A flat levy/fee, while administratively appealing, does not address the diversity in the types of development projects and their widely varying land value impacts.

An analysis of the projects mentioned above points to a few problems, even where some LVC framework exists. For one, the first transaction after the project announcement rule is not legally embedded. Most Indian betterment-levy provisions trigger at project completion (e.g., Section 37 of the DD Act 1957; Section 66 of the Bombay/Gujarat TP Act 1954/1976). By then, the original landowner has typically already transacted, and the increment has been captured privately. This is not only economically inefficient but also invites public discontent and political opposition.

Policy makers create confusion and skirt accountability by conflating land monetisation with value capture, as is the case with CIDCO, YEIDA, or DSIRDA. Alternatively, user-side instruments like User Development Fees (UDF) in airports, and tolls and concession fees on highways, also get lumped as LVC.

As the aforesaid discussion shows, designing an efficient (in terms of capturing value from the incumbent land owner at the time of project announcement) and least distortionary (in terms of not adding unreasonably to property development costs) LVC instrument requires careful thought and design.

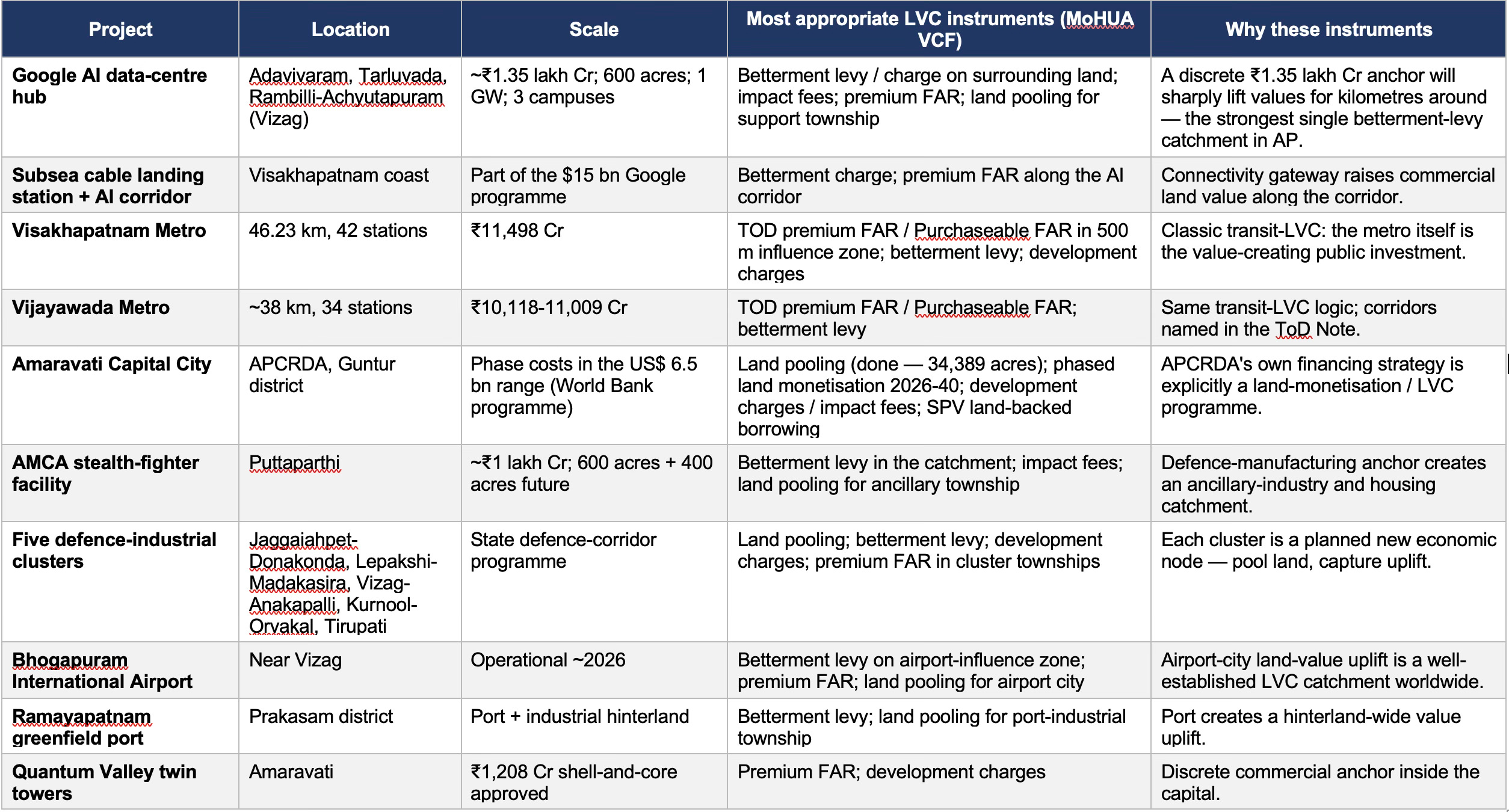

As an illustration, I asked Claude to estimate the likely LVC revenues from the development of the newly announced data centre projects in the Visakhapatnam area in Andhra Pradesh, and other investments in the state.

It estimates a realisation of Rs 700-1500 Cr annually from the application of LVC instruments to the Google AI hub catchment, Bhogapuram airport zone, defence clusters, and metro corridors. Even half of this would be greater than the combined property tax revenue collection of all the state’s 117 municipalities.

As an implementation strategy, it may be useful to align incentives and design a revenue-sharing mechanism among all public stakeholders, especially the local government. So, for example, instead of all the LVC revenues from a national highway or other central government project going to the project development entity, a part should be shared with the local government. This creates the required local incentives to enable effective adoption of any LVC scheme.

In terms of policy mandates, it is time to mandate that all large public investment projects be accompanied by the adoption of LVC instruments by the local governments. This would entail the following: (a) notification of a LVC influence zone around the project, (b) notification of the appropriate LVC instrument and the LVC rate, (c) enabling a statutory framework and a physical mechanism for its collection, and (d) a transparent and public accounting of the realisations.

As a first step, all states should be encouraged to adopt an LVC policy, borrowing from MoHUA’s LVC policy. It may be useful for the Government of India to build on this policy and formulate a model document on both betterment levy and impact fees that can be issued as administrative orders by the state governments. To incentivise this, the Ministry of Finance should consider making this a mandatory requirement to access the 50-year interest-free capex loans being given to state governments under the Special Assistance Scheme for Capital Investment (SASCI).

The model documents and guidance on each of the betterment levy and impact fee instrument options may be useful to ensure that LVC instruments are adopted in letter and spirit. The documents should contain the detailed implementation design of the instrument, and the same should be incorporated into the financial closure, state support, and all other agreements associated with the project, and should be institutionally coded into the system along with the project announcement. All project appraisals should have tightly defined and enforceable requirements on LVC.

Finally, the central government's support for any project should be made contingent on the realisation of the LVC proceeds in both letter and spirit. This should become an integral part of the financing culture of all large projects in India. This is one of the very few big bang low-hanging fruits in the mobilisation of public revenues, especially for fiscally strapped urban local bodies.

No comments:

Post a Comment