China manufactures 80 per cent of all the solar panels produced globally. And, as the IEA notes, China’s dominance is even more pronounced when one examines the entire supply chain. It produces 85 per cent of the global supply of solar cells, 88 per cent of solar-grade polysilicon, and 97 per cent of the silicon ingots and wafers that form the core of solar cells. China’s rise to dominance in solar has been rapid. In 2005, Europeans led this race, with Germany accounting for a fifth of global solar manufacturing. By 2010, while Europe installed eight out of every 10 solar panels in the world, it produced only one. This year, China will make eight of every 10 solar panels produced worldwide and add five of those to its grid. In 2023 alone, China will install more new solar capacity than the US has deployed since Americans bought their first panels in the early 1970s.

China for example last year exported 86.6GW of solar panels to Europe, a 112 per cent increase on 2021’s figure, according to InfoLink Consulting. “If we are going to hit our 2030 [climate] targets we need China,” says Jacob Kirkegaard of the Peterson Institute.

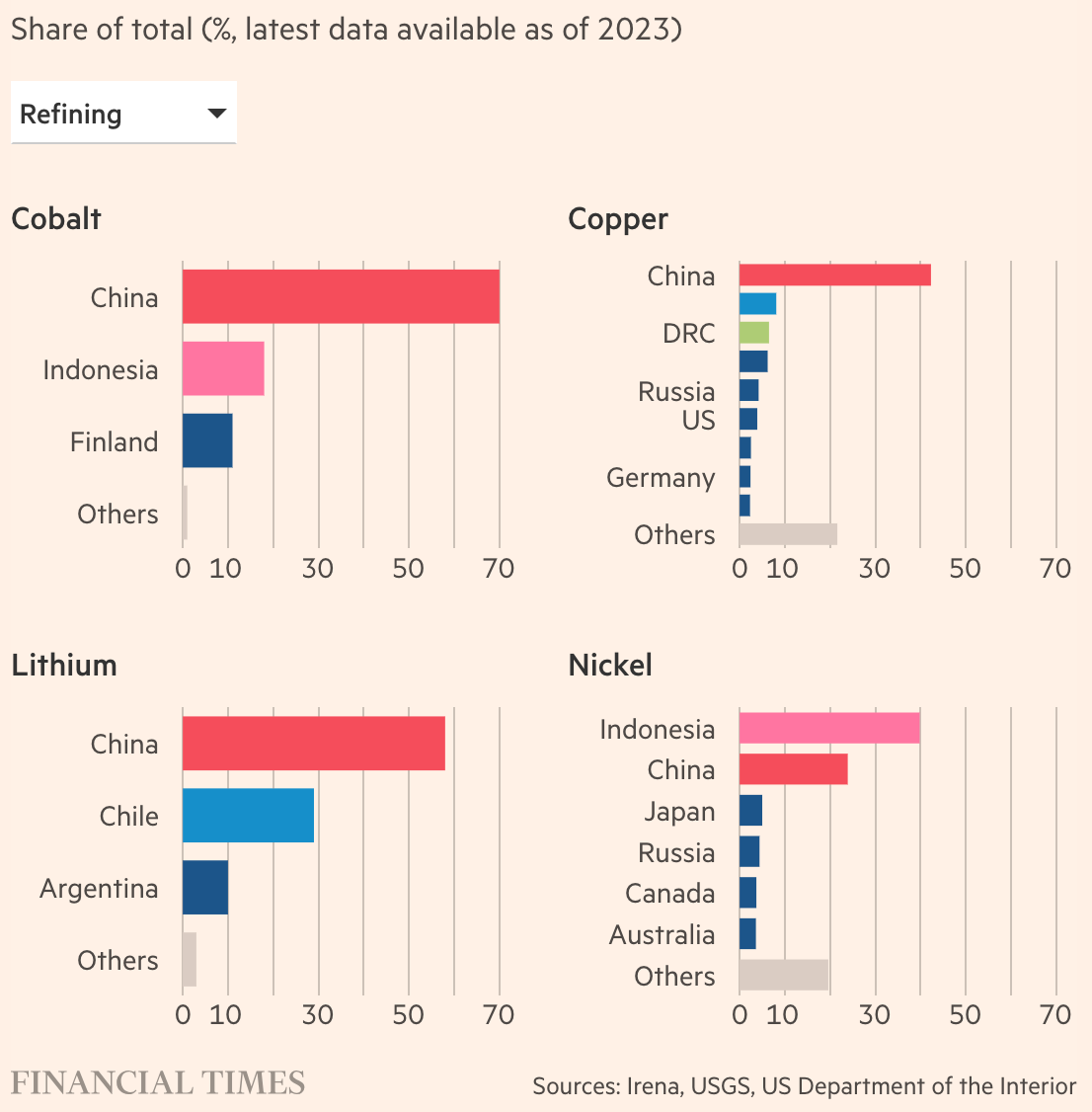

China dominates the EV supply chain as 76 per cent of the world’s production capacity for batteries – they make up 40 per cent of a typical EV’s sticker price – is in the country, with Contemporary Amperex Technology Limited (CATL) and BYD among the world’s top three producers. Fujian-based CATL alone controls a third of the entire global battery market... The country also controls more than two-thirds of the components needed to make them... China is also home to 70 per cent of the global production capacity for cathodes and 85 per cent for anodes, both key battery components, according to the International Energy Agency (IEA). Over half of the world’s lithium, cobalt and graphite processing and refining capacity is located in China... Two-thirds of the 10 million EVs sold worldwide last year were in China, helped by a slew of government policies dating back to 2009 that include subsidies, tax breaks and procurement contracts.

This is a good summary of the different kinds of support the Chinese EV industry has gotten over the years. It has included a ten-year consumer subsidy program that ended in 2022 which reimbursed consumers as much as 60,000 yuan (~$8000), waiver of a 10% levy on smaller EVs till 2025, other tax breaks, manufacturing subsidies, government-funded charging infrastructure (6.36 million chargers, the largest in the world, and 649,000 chargers added in 2022, which is more than 70% of global additions). Several hurdles have been put to disincentivize ICE vehicles - license plate prices in auctions in Shanghai averaged 92,780 yuan last year whereas green license plates can be easily obtained; a tradeable dual-credit system for automobile manufacturers since 2017 that awards points for making clean cars and penalties for those with high fuel consumption, and producers with negative scores may be taken off the market. These were complemented by large purchases by governments at all levels and public transport networks.

The result is that EVs made a quarter of all car sales last year, compared to one in seven in the US and one in eight in Europe. Including plug-in hybrids, clean-car sales hit 5.67 million in 2022, more than half of all global deliveries and 60% of the world’s 14.1 million new passenger EV sales this year.

As the GMF report notes, China controls 61 per cent of global lithium refining, and 70 per cent of the global supply of cobalt for lithium ion batteries comes from mines in the Democratic Republic of Congo, many of which are owned by the Chinese. China controls 100 per cent of the processing of natural graphite used for battery anodes, and 80 per cent of the total rare earth production and processing.

The factors driving China’s success in this arena are the same ones that have made it the uncontested manufacturing workshop of the world. These include low-cost capital, rapid regulatory approvals, protection from foreign competition, lower labour costs, an unparalleled network of suppliers, and fast-growing domestic demand.

In addition, China also dominates the supply chain for critical minerals used for defence purposes, or "war minerals". They include minerals like gallium, germanium, and indium that are critical for military equipment like lasers, radars, and spy satellites. These minerals have little commercial value and are mined and refined only in very small quantities. Sample this from The Economist

Antimony, known in biblical times as a medicine and cosmetic, is a flame retardant used in cable sheathing and ammunition. Vanadium, recognised for its resistance to fatigue since the 1900s, is blended with aluminium in airframes. Indium, a soft, malleable metal, has been used to coat bearings in aircraft engines since the second world war... Long before cobalt emerged as a battery material, nuclear tests in the 1950s showed that it was resistant to high temperatures. The blue metal was soon added to the alloys that make armour-penetrating munitions. Titanium—as strong as steel but 45% lighter—also emerged as an ideal weapons material. So did tungsten, which has the highest melting point of any metal and is vital for warheads. Tiny amounts of beryllium, blended with copper, produce a brilliant conductor of electricity and heat that resists deformation over time... Gallium goes into the chipsets of communication systems, fibre-optic networks and avionic sensors. Germanium, which is transparent to infrared radiation, is used in night-vision goggles. Rare earths go into high-performance magnets. Very small additions of niobium—as little as 200 grams a tonne—make steel much tougher. The metal is a frequent flyer in modern jet engines.

Beyond their varied properties, this group of mighty minerals share certain family traits. The first is that they are rarely, if ever, found in pure form naturally. Rather, they are often a by-product of the refining of other metals. Gallium and germanium compounds, for example, are found in trace amounts in zinc ores. Vanadium occurs in more than 60 different minerals. Producing them is therefore costly, technical, energy-intensive and polluting. And because the global market is small, countries that invested in production early can keep costs low, giving them an impregnable advantage. This explains why the production of war minerals is extremely concentrated. For each of our 13 war minerals, the top three exporters account for more than 60% of global supply. China is the biggest producer, by far, for eight of these minerals; Congo, a troubled mining country, tops the ranking for another two; Brazil, a more reliable trading partner, produces nine-tenths of the world’s niobium, though most of it is sent to China. Many minerals are impossible to replace in the near term, especially for cutting-edge military uses.

The combination of concentrated production, complex refining and critical uses means trading happens under the radar. The volumes are too small, and transacting parties too few, for them to be sold on an exchange. Because there are no spot transactions, prices are not reported. Would-be buyers have to rely on estimates. These vary widely. Vanadium is relatively cheap: around $25 per kilogram. Hafnium might cost you $1,200 for the same amount. All this makes building new supply chains much more difficult.

On July 4, China announced restrictions on exports of gallium and germanium, that are important in semiconductors, solar panels, and missile systems. This has strategic significance since it highlights the vulnerability of US and other western militaries to such sanctions. In the aftermath of the Cold War, the US has run down its large stocks of strategic minerals and confined its strategic stockpiles to only commodities like oil and gas.

China is responsible for the production of about 90 per cent of the world’s rare earth elements, at least 80 per cent of all the stages of making solar panels and 60 per cent of wind turbines and electric-car batteries. In some of the materials used in batteries and more niche products, China’s market share is close to 100 per cent... China’s grip on raw materials is “more than it appears”. This is thanks to equity investments in overseas mining operations by Chinese companies such as metals group Huayou Cobalt, carmaker BYD and battery giant CATL. In lithium, for instance, China only has a small share in mining, yet by next year Chinese interests will control more of the resource than the country needs for domestic purposes...The country’s overseas metals and mining investments are on track to hit a record this year, according to data published last week by Fudan University in Shanghai. Spending in the first six months of 2023 hit $10bn, more than the total in 2022, and investments this year are likely to surpass the previous annual record of $17bn in 2018... China is the leading producer of at least one stage of the supply chain for 35 of the 54 mineral commodities that are considered critical to the US... China produces a “staggering” 98 per cent of the world’s supply of raw gallium, according to CSIS, despite the product’s US military applications, including in next-generation missile defence and radar systems. In electric-car batteries, for example, China’s share of the raw materials they require is lower than 20 per cent but it holds a 90 per cent share of the market for processed versions of the same materials... The production of graphite, used in the anodes in the heart of a lithium-ion battery, is instructive. While China’s market share of graphite reserves is just over 20 per cent, its market share for graphite processing is nearly 70 per cent...More than half of all new wind turbines installed this year will be in China, according to the Global Wind Energy Council, an industry lobby group. In the production of nacelles, which house the turbine’s power generation equipment, China has a market share of 60 per cent. It is currently building more than 60 new nacelle assembly facilities, adding to the 100 already in operation. Further down the turbine supply chain, the GWEC data shows China has more than 70 per cent market share of many crucial components including castings, forgings, slewing bearings, towers and flanges.

This about industrial policy,

Beijing’s cumulative state spending on the EV sector is more than $125bn between 2009 to 2021. Domestic industry was prioritised with heavy-handed local requirements, and from 2016 South Korea’s leading battery makers, LG, SK and Samsung, were cut off from accessing generous subsidies, setting up a boom in CATL and BYD’s battery production.

This about the inherent advantages that completely distort the playing field for foreign competitors,

The advantages that China now boasts when it comes to manufacturing clean tech products are underpinned by massive economies of scale benefits. Goldman data suggests that China can build an EV factory in about a third of the time it takes in other countries while a battery factory in the US will cost nearly 80 per cent more than in China. Bernstein says the cost of some manufacturing in the US can be three times more than in China. This highlights how China’s rivals must grapple with not only limited access to resources and upfront technology costs, but also labour shortages, wage inflation and higher environmental standards...

Buoyed by massive domestic demand, Chinese manufacturing of polysilicon and its processing results in costs that are two-thirds the price of a European-made product, the IEA says. Chinese wind turbines are half the price of western rivals, according to S&P data. Across these industries, Mazzocco says it is important to credit the role of intense private sector competition. “It is something we miss from the outside: we think it’s just about the subsidies. But in reality, it’s also because [companies] have been able to overcome their competitors within China in an extremely cut-throat environment,” she says. “They are the best of the best at squeezing every cent out of their operations.”

And as if extraction and processing was not enough, China is now seeking to control the trading of clean energy metals.

China is making a push to dominate the trading of lithium carbonate futures, as it seeks to wrest the financial plumbing linked to metals vital to the clean energy revolution away from the western dollar-based financial system. Last month the Guangzhou Futures Exchange became the fourth global commodities exchange to launch contracts tracking the price of lithium carbonate, a mineral used in the manufacture of electric-vehicle batteries.Within three weeks open interest — a key measure of the size of the market — had risen to more than 20,000 lots and far outstripped activity at rivals London Metal Exchange, Singapore Exchange and the US’s CME Group, which had launched its own version just days earlier. The proliferation of futures contracts on crucial elements of electric-vehicle products such as nickel, copper and lithium carbonate in part reflects the growing importance of the industry, as companies up and down the supply chains seek to hedge against price swings. But the early lead established by Guangzhou has underscored how China is seeking to seize greater control over trading in what it sees as a group of metals critical for the 21st century. By establishing its own trading hubs and benchmarks priced in renminbi, the drive is part of Beijing’s efforts to lessen the commodities market’s reliance on the US dollar...Even so, China’s drive to convert its dominance over the flow of commodities into global pricing power faces substantial hurdles, including using a currency that cannot be freely traded, and the absence of a global warehousing network for any of China’s five domestic futures exchanges. The LME, which is owned by Hong Kong Exchanges and Clearing, does have a network of warehouses outside of China. It also argues its nickel futures contract — which represents the worst quality piece of metal in the worst part of the world — is more representative of the global market. Its pricing system is based on the value traded on its exchange, supplemented with “regional premiums” to reflect local problems such as distribution.

No comments:

Post a Comment