1. The low level of industrial R&D has been a persistent problem for India. From an interview of Naushad Forbes, sample this about the software industry,

In the software industry, which is this huge profitable industry that we have in India, we invest roughly one percent of sales in R&D. The top 10 firms in China, which, again, are software services firms, invest 8%. Why do we invest one-eighth as much as Chinese software firms? It’s clear to me that we underinvest in R&D, but when I’ve gone around and talked to my friends in industry, they don’t think so. They think we invest a lot in R&D. The first thing that needs to change is this mindset, and to recognize that there’s this big gap between where we are in Indian industry and where the world is and where the top firms in the industry are.

Forbes also describes an analytical framework to think about innovation in the economy,

Firms largely learn by looking at what other firms do and learning from them, and then you do something better. Then learning by analysis also includes analyzing what you do, so, documenting work processes. Turning tacit knowledge that reflects the skills that are in people’s hands into something that’s more documented and scripted, and because when you write something down, then that’s a basis for further improvement... They (South Koreas firms) disassemble and reassemble the cars, and then they did the same thing with microwave ovens from GE. It’s this crazy thing where they’re literally disassembling and reassembling the same product. They practice this until they can do it as efficiently as the Japanese company that they got the car from and the American company that they got the microwave oven from. That kind of learning by a very clear, focused attention is quite unusual, but it’s very powerful in fostering that competitive approach to manufacturing. The last category is R&D because R&D is also a form of learning... You need to invest in a certain amount of knowledge creation yourself to be able to understand the cutting edge of knowledge creation elsewhere, so R&D becomes the firm’s formal learning unit. It then also becomes the firm’s formal creating unit, but before it can create, it has to be the firm’s formal learning unit...If we talk about a new technology, artificial intelligence, robotics, et cetera, I think we should think in terms of that learning hierarchy. Start with learning by doing, then learn to do efficiently by analyzing. Then learn through looking at what others are doing, and taking things apart, and reverse engineering, and so on. Then learn by some actual explicit practice to become more efficient, and then R&D.

He points to the utility of a productivity metric,

For many, many years, our company mission statement was to be a developed company in a developing country... The enterprises will need to get there first, and that means that, in terms of value-added per person, individual productivity, our value-added per person needs to catch up with the world as a company first. And if it happens for enough companies, then it will start happening for India, and value-added per person at the country level, as we know, is GDP per capita. It’s the same thing, it’s productivity per person. It’s a clear productivity metric... I use value-added per person and compare different industries, different firms. It’s a very powerful metric. It really tells you how well you are doing as a company on all the key elements—margin, productivity—does your margin, does your value-added percentage keep rising? That’s a reflection of how good one’s R&D is, how innovative one is.

But for some ideological blindspots, the interview is a good read.

There is one thing which caught my attention. In supporting the 2% CSR funding, Forbes writes,

We’re India with very limited state capacity, which means the state has less ability to implement useful policies at the last mile on the ground. There’s a role, it seems to me, for those who have implementation capability, which is the firms in the country, to engage with education and education outcomes for schoolchildren, public school children, the most disadvantaged public school children; to engage in public health issues; to engage in women’s empowerment issues... we need to get enough companies in India that converge with the world. As that happens, India will converge with the world. It needs to happen across industry, across enterprises

The substitutability of project execution in private sector and program implementation in public sector contexts is a common blindspot among those in the private sector. Since the private sector can execute a business model well, it's argued, they are also well-placed to support or even implement programs in school education, public health, or women's empowerment. This misplaced belief is a major contributor to private sector's illusions about themselves and their perceptions about governments (and public policy issues in general).

As a comparison of misplaced hubris, I am tempted to think of Esther Duflo's claim that economists are better placed to understand and diagnose the plumbing of public policy and program implementation than bureaucrats. This is another interesting snippet which reveals more about entrenched mindsets,

I don’t think India would have survived the COVID lockdown without the CSR money, to be very honest.

Smoking dope?

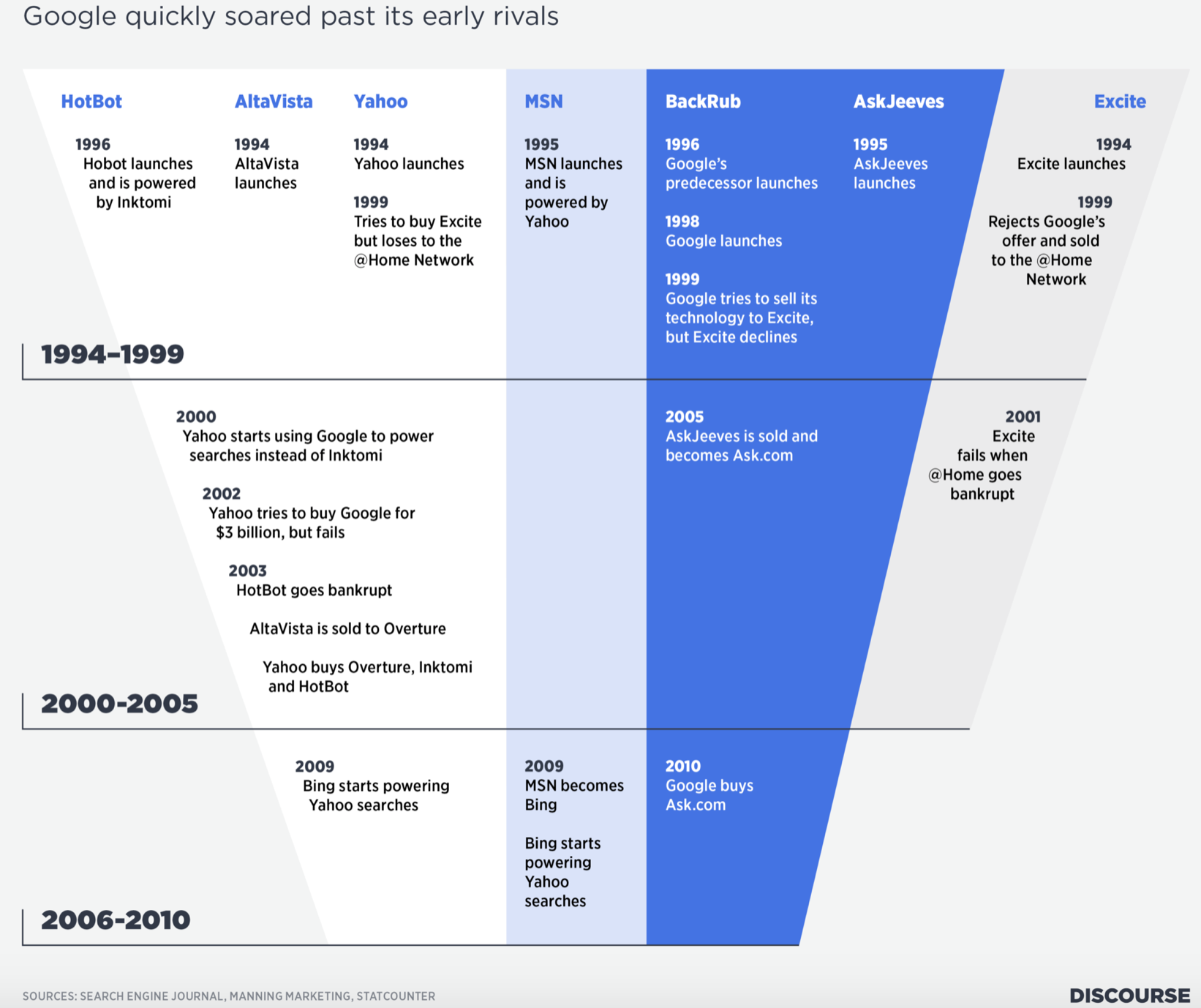

2. On the anti-trust case against Google

In 2020, the U.S. Justice Department and 38 states and territories filed antitrust lawsuits against Google, charging that it was abusing its dominance in online display advertising (ads that appear on other websites, not on Google results pages). They claim that Google holds a monopoly in display ads because it owns the biggest platform for ad buyers, the biggest ad exchange and the biggest platform to publish ads. That makes them the biggest buyer, seller and broker of display ads.Hosting the largest ad exchange gives Google access to the bids and bidding histories of other ad buyers and sellers. The suits claim that Google uses this information to undercut rival bids when the company buy ads to market its own brands and services, and to raise the auction floor when selling ads. Google, in its role as an ad broker, is also accused of charging publishers exorbitant fees... The case is scheduled to go to trial in September of 2023.

Consider, for example, how the landscape of public company stock ownership has changed in recent decades. In the US in 1950, only 6.1 per cent of such stock was held by institutions — the rest was owned outright by individuals who voted on matters such as who should sit on a board. Today, institutional middlemen like pension funds, mutual funds, hedge funds and so on, own 70 per cent of those shares.

5. Good summary of the supply and demand-side contributors to the current bout of inflation.

6. I've blogged earlier expressing scepticism about fintechs. I had blogged (here and here) that while they can offer some services to traditional banks, their limitation is on the asset side and fee services.

In this context, TT Rammohan has this article where he feels apart from forcing banks to pull up their socks and improve productivity, fintechs are unlikely to do much. He's not convinced by the threats likely to regular banks from full-fledged digital banks

Digital banks don’t quite take banks head-on. They typically target high risk customers that banks tend to avoid. These include: Individuals with lower incomes or lower credit scores, commercial real estate and unsecured lending. Despite the higher risks they take, digital banks have a lower provision coverage than traditional banks. Their yields on loans are about the same. They have a less loyal depositor base but their liquidity ratios are lower. Digital banks’ potential for fee income is lower because they deal with lower income clients. You might think they would have lower operating expenses because of the absence of brick-and-mortar. Not at all. What they save on branches is more than offset by huge marketing expenses. Not surprisingly, most are loss-making. So much for digital banks threatening traditional banks and taking away market share from them. Digital banks are connected with banks through the inter-bank market and also through the various services they provide. They are lightly regulated at the moment. But as they grow bigger, regulation will have to be tightened, as the GSFR report observes. Digital banks are a threat, not so much to banks, as to banking stability on account of the systemic risk they pose.

7. John Gapper points to the decision by the European Parliament this week to harmonise charging standard on all mobile devices (phones, cameras, headphones, portable game consoles etc) by adopting USB-C connector port by 2024.

It estimates that it could save European citizens €250mn and eliminate thousands of tonnes of environmental waste each year... The European Commission has been on a long campaign against consumer electronics groups to end this frustration, starting with a voluntary agreement in 2009 to converge towards USB industry standards. This has had an effect: there were more than 30 proprietary chargers in use then and it has nudged that down to three. Now it wants to ensure what Thierry Breton, EU single market commissioner, calls “full harmonisation”.

Gapper questions the legislative harmonisation process

While the EU believes in enforcing unity, consumers are complex: we favour a single charger, except for when we don’t... for all the appeal of USB-C, it is imperfect. USB may one day unveil a magnetic standard that both charges and connects devices but until then, it is preferable to have a choice... I prefer simplicity but I also like innovation, even in the mundane business of power. As technology goes wireless, a tussle over connectors may become less pressing, but the principle is important. A harmonised world that only had a single charger is very tempting, but we would not know what we were missing.

This is a classic dilemma. The pursuit of pure efficiency (and profits) maximisation means that large companies like Apple will be encouraged to offer different connector ports for its own different devices. It creates the problems that we face today. Addressing this is a co-ordination issue which will not get solved through market-based approaches. In the real world it requires regulatory engagement. It can be argued that instead of themselves choosing the standard, the regulators should lay down some broad principles and nudge the industry to choose from among the standard and make the choice only if the industry fails to reach a consensus.

But this accommodation of the market preferences over regulatory engagement is a slippery slope. In the last several decades, we've slipped considerably down that slope to arrive at a world where this fig leaf (and its efficiency maximisation ideal) has become the default test for regulatory interventions. And its outcomes have not been pretty.

8. FT has a good interactive inflation tracker for several countries. Interesting that it's perhaps a rare time in history when global inflation is higher than India's inflation.

9. More from an FT review of David Gelles' new book on Jack Welch.

The Man Who Broke Capitalism, which will be published in the UK next month, is good at tracing former GE executives’ trajectories after they moved on to run other companies: a sharp upward tick in the short term, as job-cutting and GE-style efficiency measures took hold, followed by a slow decline in the share price, the culture, or both. GE alumni tried to apply Welchist management at organisations as varied as Boeing, manufacturer 3M and do-it-yourself chain Home Depot. At the last, Bob Nardelli, a runner-up in the race to succeed Welch, oversaw a decline in the retailer’s share price and a surge in his own pay, culminating in the award of a $210mn exit package. Gelles even finds the former GE boss’s fingerprints on the chain of mistakes that led to the fatal Boeing 737 Max crashes in 2018 and 2019. Former GE executives occupied key roles at the aircraft maker.

No comments:

Post a Comment