1. Reeling from the impact of the pandemic, Airlines in the US are finding out ingenious ways to raise money. A friend sent this report about airlines mortgaging frequent flier miles.

United Airlines Holdings Inc. will mortgage its frequent-flier program to secure a $5 billion loan from three banks as it seeks to build a cash cushion to see it through the coronavirus pandemic. The scramble for cash has been one of the biggest challenges for airlines in recent months, as the pandemic and the travel restrictions put in place in response caused travel demand to dry up. On Friday, American Airlines Group Inc. made a similar move to United’s, saying it intends to offer its frequent flier program as collateral for a $5.8 billion government loan...

Loyalty programs are a rich vein for airlines to secure cash. Co-branded credit cards associated with the programs essentially allow carriers to book revenue from a slice of all customers’ spending. That comes in handy at times like this, when bookings have nearly dried up, but customers continue to use airline-branded cards for other purchases. United said its MileagePlus program generates over $5 billion in cash a year and is worth over $20 billion. The program earns most of its revenue selling miles to third parties such as JPMorgan Chase, its credit-card provider, which then awards them to customers for making purchases... Airline loyalty programs can be alluring to banks because of their typically high-value membership: United says it has more than 100 million members in MileagePlus program, many of whom earn above-average incomes and spend more than typical customers. United said it expects fewer people to redeem their miles for travel due to the pandemic, which means more money stays within the loyalty program... In past crises, airlines have pulled cash from frequent flier programs by selling big chunks of miles to their bank partners.

Another example of financialisation.

2. A proposal for installing smart meters in discoms by supporting the emergence of meter asset providers.

3. As foreign policy gets politicised and hindsight analysis and blaming takes over, is there a risk of the foreign policy establishment and IFS officers becoming the latest victims of decision paralysis? Read Shyam Saran here.

Phunchok Stobdan has a good article pointing to a pattern in China's border disputes management with other countries. Hitherto, the border disputes on the eastern (Arunachal) and western (Aksai Chin) presented different priorities, with concessions on the former being difficult for India and perhaps the latter for China (given Tibet). Now, with its latest incursion, the Chinese are perhaps seeking to de-link the two parts and then leave it with the opportunity latter to focus exclusively on the eastern front.

China seems to be pushing for a formal settlement along the LAC in Ladakh, where they have nothing to lose. Probably, they also assume that India has accepted fait accompli. And, to our disappointment, it may not involve swapping India’s claims over Aksai Chin for China’s claims over Arunachal Pradesh, which many in India thought to be a pragmatic thing to accept. This time, Chinese may be making a tricky move to let India, in the first step, forego its claim over 38,000 sq km (Aksai Chin), thereby de-link Ladakh from the overall boundary dispute. But, should that happen, India, by implication, will have to give up not only Aksai Chin, but also cede its notional claim over the 5,047 sq km (Skyasgam valley) and the Menser Enclave (five villages) near the Mansarovar Lake. China’s “minimal demand” that Tawang is non-negotiable had been aired through Chinese academics. This tactic was also applied with Central Asian states. If India falls for some kind of Chinese position over Aksai Chin, Beijing will then shift the focus to Arunachal to emphatically claim 90,000 sq km from India. Ceding Aksai Chin would fundamentally alter the status of J&K and Ladakh. By implication, India would have to forget about PoK and Gilgit-Baltistan as well. India should tread carefully unless both sides are willing to make a move for grand bargaining.

As India evaluates its options, Tibet and Taiwan should be on the table. Taiwan's success in dealing with Covid 19 can be an opportunity to engage with them in a reasonably high enough manner.

4. Vivek Agarwal points to the problems with the emerging partnerships in India's telecoms market between telecom providers and tech companies. The article also highlights its similarity with the trajectory of growth of railroads in the US in the 19th and 20th centuries.

The internet, given its increasingly essential role in trade and commerce, may be referred to as the "railroad" of our times. State authorities must learn to break the vicious cycle of allowing the creation of monopolies only to break them to reinstate competition, as was the case with the "railroads" in the 19th century. As a closing remark, I am reminded of what Charles Francis Adams had said about the railroad problem in 1878. He said that the time was nigh “when the railroads would manage the state, if the state did not manage the railroads”. Nothing much seems to have changed since, except that the new railroad of the 21st century is big data which may get concentrated in tech magnates in the absence of apposite regulation of these big tech-telco combinations.

5. As Q4 results indicate, the Indian economy was already slowing when Covid 19 hit. Business Standard reports that the 1002 listed companies - excluding banks, non-bank lenders, insurers, brokerages, and IT companies - reported combined pre-tax loss of around Rs 2700 Cr in Q4 2019-20. It was the first loss in 24 quarters and fell from Rs 1.05 trillion profit before tax in Q3.

6. A feature on cloud kitchens business in India.

Cloud kitchens, also known as dark or ghost kitchens, have been around for a while but have flown under the radar. These are essentially low-cost models where kitchens in places with cheap real estate are rented out, and from which deliveries are fulfilled mostly through an aggregator. Since they’re not attached to a proper restaurant, there are no overheads like lighting, décor, front-of-the-house salaries, and so on. Low capital cost is why cloud kitchens with curious names (Bhookemon, for one) are quickly scaling up to deliver the same menu at different pin codes with consistency. Apart from low rentals, the sourcing of ingredients is centralised, the R&D happens at a base kitchen and once a recipe is finalised, it can be easily replicated at different locations.

7. Neelkanth Mishra writes about a secular decline in food prices due to changing food habits, efficiency improvements and associated lower unit production costs.

8. A new low in solar power rates. The latest tender for 2000 MW by Solar Energy Corporation of India (SECI), which allows the developer to set up the project anywhere, Spain's Solarpack Corporation bid Rs 2.36 per unit for 300 MW. Now the challenge is to get Solarpack to go ahead with fulfilling its bid commitment.

This is important because this is what happened to the previous record low,

The previous lowest bid was Rs 2.44/unit by ACME Solar in 2018 for a 600 mw project to be set in Rajasthan. The project is currently under litigation as ACME wants to withdraw from the same.

It is hoped that SECI has learned from that experience. It ought to have greater bid information clarity to be comfortable that the bids are based on strong economic logic, and stronger contractual terms to ensure that that bidders are likely to fulfil their commitments. It is necessary for bid managers now to go beyond the market knows best approach and also start scrutinising the bid assumptions and satisfy themselves that the bid can be met.

Another interesting this is the composition of bidders. It is reported that SECI received bids for 5280 MW, against the requested 2000 MW, with major global developers too. Amidst them is Ayana Renewable Power, backed by Britain's international DFI, CDC. Wonder what's CDC's capital doing here, competing with market finance, as against its mandate of crowding in market finance. Unless, of course, one argues that competition is also crowding in!

9. An interesting point made by Vivan Sharan in the context of the Indian government's bans on Chinese apps.

According to Ericsson, global mobile data traffic was around 456 exabytes in 2019, of which India accounted for approximately 75 exabytes, or 16%. Around 14% of the global population resides in India, and therefore, it punches slightly above its weight in terms of mobile data consumption. However, India has not begun to generate commensurate economic value from this outsized data consumption yet. In fact, the global digital economy seems to mimic its physical counterpart, with the US and China making up the lion’s share.

According to the United Nations, the US and China account for 90% of the market capitalisation of the 70 largest digital platforms in the world. They also account for 75% of all patents related to blockchain technologies, 50% of global spending on the Internet of Things, and more than 75% of the global market for public cloud computing. It’s clear that the two countries will remain at the forefront of global technological developments, which will feed their dominance in the digital economy. The emergence of this bipolar digital landscape narrows India’s strategic choices. The world’s largest digital democracy must foster innovation, competition and scale in the private sector, as well as increase State capacity to govern new markets in parallel.

In simple terms, India is contributing an outsized share to the absolute usage numbers (albeit not value added usage), whereas its share of the commercial value captured from the digital economy is disproportionately small.

For a country which had all the advantages at the dawn of the digital age, with several leading software companies and the government not being a stumbling block, what has happened? Where did digital entrepreneurship in India go wrong? Where are the Indian TikToks or WeChats?

10. The beneficiaries of Fed's corporate bond buying program includes some of the largest US corporates.

Apple, Verizon and the U.S. divisions of several foreign auto makers are among the largest direct beneficiaries of Federal Reserve efforts to support the corporate-debt market, according to disclosures Sunday. In all, the Fed on Sunday identified 794 companies whose bonds it will be buying directly to support the market for investment-grade corporate debt. In addition to Apple and Verizon, the recipients include AT&T. and the U.S. units of Toyota Motor, Volkswagen and Daimler. Together those six companies accounted for 10% of debt purchased from a broad list of borrowers the Fed is supporting.

11. Staying with Fed, James Grant laments the overprescription of the monetary medicine by the US Fed as addicting the US economy. He writes that Jerome Powell has become Dr Feelgood.

Ultralow interest rates are a financial psychotropic. They induce feelings of neediness (on the parts of savers to reach for yield), grandiosity (by corporate deal-doers to reach for the moon) or fantasy (for any who would try to rationalize otherwise insupportably high stock prices with reference to the tiny cost of a loan). Ground-scraping interest rates turn savers into speculators and quarantined millennials into day traders. They facilitate overborrowing, suppress market signals, misdirect investment dollars, and promote the dubious business of turning well-financed public companies into heavily indebted private ones... With opioids, the habituated patient needs ever higher doses to achieve a constant effect, and so it is with dollars. Massive credit creation (which the Fed achieves by buying bonds and mortgages with money it materializes with a tap on a computer keypad) is a kind of financial painkiller. The record of the crises of the past 20 years, beginning with the post-millennium dot-com crash, is one of lower and lower interest rates, and of greater and more aggressive bond-buying.12, A damaging practice in the power sector in India has been the trend of discoms reneging on power purchase agreements (PPAs) on the face of low spot prices of exchange traded power.

13. A sobering balance sheet of India's public sector units

According to a 2019 report of the Comptroller and Auditor General of India, in 2017-18, there were 184 public sector companies with accumulated losses worth over Rs 1.4 trillion. The net worth of over 70 companies had been completely eroded. Business Standard Research Bureau numbers show PSEs have seen a sharp drop in their market capitalisation, and continue to underperform the broader market. In the last 10 years, the combined market-cap of the top 17 PSEs that were part of the BSE 200 index (excluding banks and financials) has declined over 40 per cent, against a 91 per cent rise in the Sensex. It is also worth noting that over 70 per cent of the PSE profits in 2017-18 came from sectors such as petroleum and coal, where the presence of the private sector is limited.

14. Rathin Roy argues that reduction of imports from China will not hurt India and makes the case for focusing on improving domestic productivity.

Meanwhile data from Credit Suisse tells that India's import share from Chin has been declining.

Of the wide range of policy options available (from non-tariff measures to production-linked incentives (PLI), to import duties), different sectors could see differing tactics. Where India seeks to develop exports (e.g. handsets) or increase share of domestic value-add (e.g. drugs), PLI schemes are likely, and are already in place for handsets (link), and organic chemicals (link). Where import substitution is the objective and India is a large share of global demand, like in appliances or solar panels, import duties are used. These have worked in ACs and handsets, but not in solar panels. Imports of capital goods have fallen only due to a weak local investment cycle.

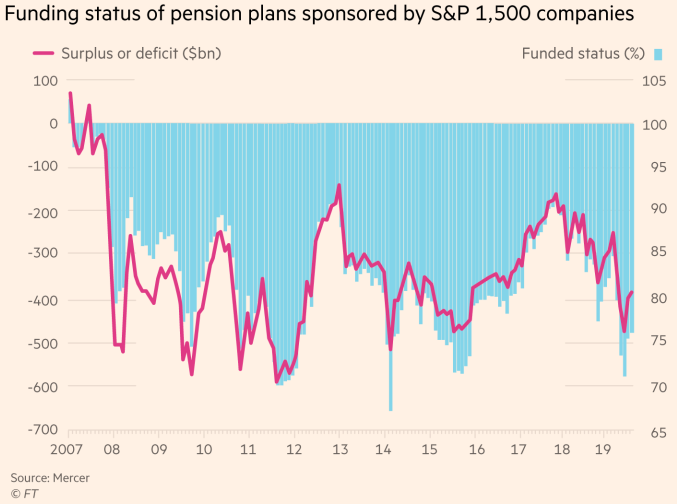

15. An FT article looks at the big crisis facing pension funds globally. It points to a WEF assessment that the retirement savings gap (the shortfall between what people currently save and what they need for an adequate standard of living when they retire) would rise from $70 tn to $400 tn in 2050 in just 8 countries.

No comments:

Post a Comment