1. I have blogged on several occasions urging caution that the solar generation bids were characterised by irrational exuberance. The spectacular decline in tariff quotes rings several alarm bells. And I am surprised at the lack of serious research and commentary on this issue. But this article by Sajal Ghosh and Rohit Prasad is a welcome contribution,

International peer-reviewed studies suggest another series of winners’ curses in the making. J.J.C. Barros and others in 2016 estimated that the levelized cost of electricity for solar is around Rs9/kWh (converted from euro to rupee using average exchange rate for 2015-16) while that for coal is approximately Rs4.8/kWh... India’s solar programme is heavily dependent on imported solar cells and modules, mainly from China. In 2015-16, India had imported $2,34 billion worth of cells out of which 83.61% were from China... Under such circumstances, Indian solar project developers may find their projects unviable in the event of currency fluctuations or changes in China’s policy on solar cell and module exports. Project developers should also keep in mind the effects of declining output. In a recent study, Mike Bergin of Duke University along with others has found that dust and particulate matter might reduce the energy yield of solar power systems in north India by 17-25%.

The authors suggest changes in the auction design by introducing dynamic open reverse auctions as against the current sealed price reverse auctions. But that is unlikely to change anything. The issue here is that bidders just want to win the tender at any cost. It has been the case with such infrastructure contracts over time and across the world. Renegotiations are therefore passé.

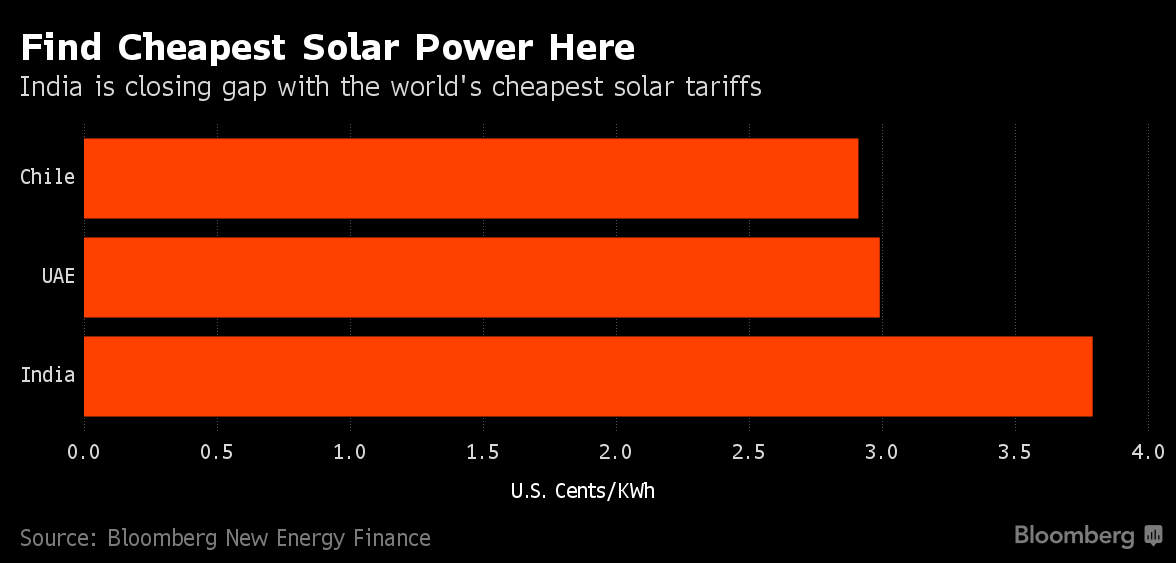

2. Staying with solar, the latest bids make India the third cheapest solar market in the world at Rs 2.62 or 3.8 cents per unit.

3. Interesting Buttonwood column highlights the challenges facing the investment management industry from proliferation of cheaper index funds; automation trends that dispense with brokers who intermediate between fund managers and savers, and with fund managers themselves (robo-advisors); and changes in investment channels. On index funds,

Big tracker funds can drive down fees through economies of scale. The expense ratio for Vanguard’s S&P tracker is just 0.04% of its assets. The average active American equity fund, which tries to beat the index, charges 0.8%. Such fund managers may claim they can outperform the market but in practice few do so consistently. Over the 15 years to the end of December 2016, less than 8% of American equity funds managed that feat. As an old quip has it, “you make your money working in active management but invest the proceeds passively.”

As companies shift pension strategies, there is the likelihood of more consolidation among asset managers,

Another challenge for fund managers is a change in the corporate-pensions market. Fewer companies are offering defined-benefit (DB) pensions, which are linked to a worker’s salary; new employees now have a defined-contribution (DC) pension, the benefits of which are not guaranteed. Employers offering DB pensions need to generate a high return to keep contributions down, so many tend to use specialised “boutique” managers. But DC plans often offer a default fund, chosen by most employees; these usually employ a more limited range of fund managers. The market tends to be concentrated in the hands of big fund-management groups and insurance companies, which can handle the administration of the scheme as well as the investing. The result is that the industry seems bound to consolidate.

4. Another article in Economist points to the declining number of listed companies in the US as well as the trend of start-ups to stay private for longer causing an IPO drought.

A big trend in American business is the collapse in the number of listed companies. There were 7,322 in 1996; today there are 3,671. It is important not to confuse this with a shrinking of the stockmarket: the value of listed firms has risen from 105% of GDP in 1996 to 136% now. But a smaller number of older, bigger firms dominate bourses. The average listed firm has a lifespan of 18 years, up from 12 years two decades ago, and is worth four times more. The number of companies doing initial public offerings (IPOs), meanwhile, has fallen from 300 a year on average in the two decades to 2000 to about 100 a year since... Although the total population of companies in America has been steady, their propensity to list their shares has roughly halved... Private markets, meanwhile, have become more sophisticated at supplying the funds they do require. Many big, mainstream fund managers, such as Fidelity and T. Rowe Price, are investing in unicorns, meaning private firms that are worth over $1bn, of which there are now roughly 100.

Several reasons have been attributed ranging from fear of red-tap to the reduced capital intensity of technology intensive firms (one of the basis of secular stagnation hypothesis) to the belief that private markets are better at allowing firms to take a long-term perspective. The last strikes at the heart of the conventional wisdom, nay holy cow, on financial intermediation. And one more reason for the shrinking universe of listed firms is disturbing,

Exits from the stockmarket by established firms—the second factor behind listed firms’ shrinking ranks—are growing in number. About a third of departures are involuntary, as companies get too small to qualify for public markets or go bust. The rest are due to takeovers. Some firms get bought by private-equity funds but most get taken over by other corporations, usually listed ones. Decades of lax antitrust enforcement mean that most industries have grown more concentrated. Bosses and consultants often argue that takeovers are evidence that capitalism has become more competitive. In fact it is evidence of the opposite: that more of the economy is controlled by large firms.

5. Staying on the issue of private markets allowing firms to take a long-term perspective, John Asker and colleagues have a new working paper which finds supporting evidence,

We evaluate differences in investment behavior between stock market listed and privately held firms in the U.S. using a rich new data source on private firms. Listed firms invest less and are less responsive to changes in investment opportunities compared to observably similar, matched private firms, especially in industries in which stock prices are particularly sensitive to current earnings. These differences do not appear to be due to unobserved differences between public and private firms, how we measure investment opportunities, lifecycle differences, or our matching criteria.

6. Greg Ip strikes a contrarian note to the conventional wisdom that robots are destroying jobs,

7. Is the hub-and-spokes model of airline industry under threat,The U.S. has many problems, but job creation isn't one of them. In April, nonfarm private employment rose for the 86th straight month, the longest such streak on record. Monthly job creation has averaged 185,000 this year, more than double what the U.S. can sustain given its demographics... If automation were rapidly displacing workers, the productivity of the remaining workers ought to be growing rapidly. Instead, growth in productivity -- worker output per hour -- has been dismal in almost every sector, including manufacturing. In a compelling study released this week, the Information Technology and Innovation Foundation demonstrates that the supposed gale of technology-driven job destruction a myth.

Rob Atkinson, president of the industry-supported think tank, and researcher John Wu examined government data back to 1850 to measure jobs lost in slow-growing occupations and jobs created in fast-growing occupations, their proxy for job creation and destruction driven by technology and other forces. By this measure, churn relative to total employment is the lowest on record.

Two new aircraft—the Boeing 787 and the Airbus A350—make it profitable to carry smaller numbers of passengers over long-haul routes. Secondary cities half a world away from each other can increasingly sustain direct connections. That eliminates the need to change planes in the Middle East. Big legacy carriers, in addition to long-haul, low-cost pioneers such as Norwegian and AirAsia X, are buying these planes in huge numbers. The fact that Airbus has 750 outstanding orders for its A350, compared with just 107 for the A380s that Emirates flies, shows where airlines think the future of aviation is heading.

No comments:

Post a Comment