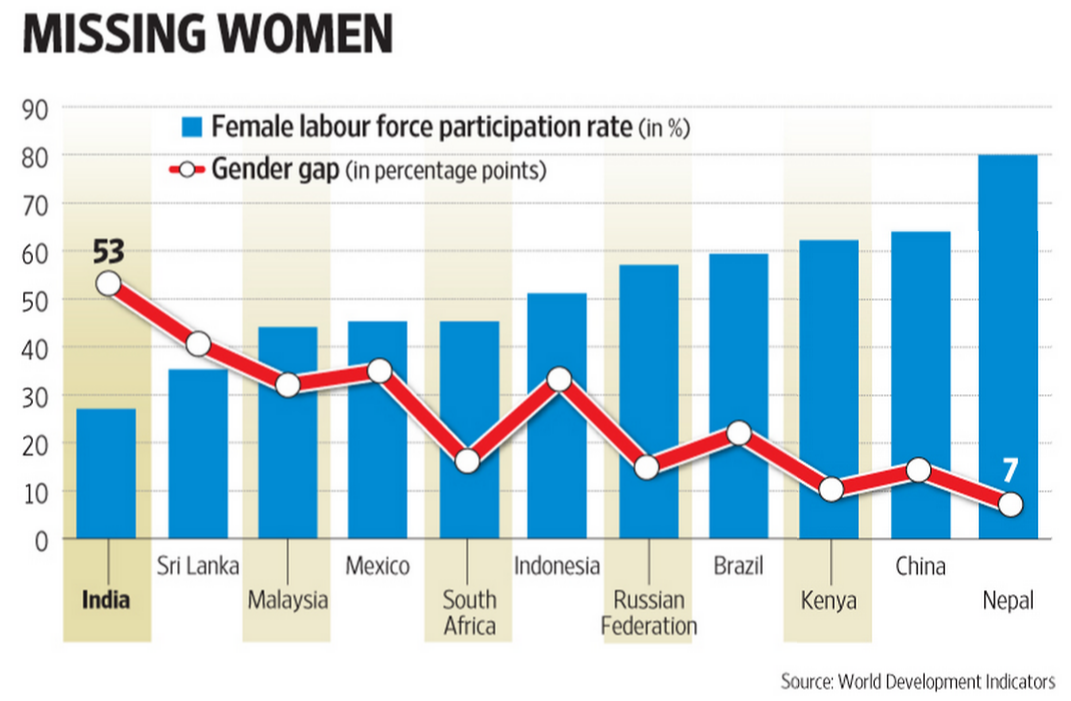

1. Livemint points to one of the biggest structural concerns for India's economy and society, the skewed female workforce participation rate. At 27%, it is easily the lowest among all major developing economies, including neighbors. Further, if the female participation rate were the same as that for males, then India would have had an additional 217 million women in the workforce, or a 53% labor force participation gender gap.

The IMF chief Christine Lagarde recently said that India's output would be boosted by 27% if the female labor participation rate matched that for males.

The IMF chief Christine Lagarde recently said that India's output would be boosted by 27% if the female labor participation rate matched that for males.

2. John Thornhill points to the changing contours of international diplomacy, with the growing predominance of technology. In a reference to 'techno-geopolitics', he writes,

2. John Thornhill points to the changing contours of international diplomacy, with the growing predominance of technology. In a reference to 'techno-geopolitics', he writes,

Craig Mundie, Microsoft’s former chief research and strategy officer, says: “People still talk about the geopolitics of oil. But now we have to talk about the geopolitics of technology. Technology is creating a new type of interaction of a geopolitical scale and importance.” It is significant, he notes, that cyber security, data protection and privacy concerns will top the list for discussion when China’s President Xi Jinping visits the US this month. Mr Mundie argues that government institutions around the world will need to be reconfigured to deal with techno-geopolitics. “We are trying to retrofit a governance structure which was derived from geographic borders. But we live in a borderless world,”

3. This graphic from Credit Suisse disaggregates the total stressed assets in the Indian banking system at 13.5%, into five categories - NPAs, restructured loans, security receipts of asset reconstruction companies, strategic debt restructuring (by taking equity ownership), and those refinanced under the 5:25 scheme.

4. A RBI study estimates that total corporate investment (based on the financing plans submitted to financial institutions) in India fell 27% in 2014-15 to Rs 1933 bn, precipitously from Rs 3680 bn in 2011-12. More disturbingly, based on the capital investment plans made so far for 2015-16, the total croporate capex for the entire year is estimated at just Rs 1114 bn. Further, the share of new projects fell in value from 84.2% in 2011-12 and 65.2% in 2012-13, to 39.7% in 2014-15. Envisaged capex financed by banks/FIs and ECBs decreased by 30.8% and 18.5% respectively.

The case for public investments to stimulate growth grows ever more compelling with each such news.

5. One of the surprises with the prolonged monetary accommodation has been the inability of cheap capital to translate into investment spending. An FT article points to atleast three contributors to this reluctance to invest. One, the medium and long-term growth prospects are not considered attractive enough to generate the demand required to stimulate investment. Two, the financial market uncertainty has driven up the equity-risk premia, and thereby the returns demanded on equity. This, in turn, keeps the WACC for the project high. Three, despite the long-period of ultra-low rates, businesses have been reluctant to lower their investment 'hurdle rates' (which is generally above 10%, and often between 15-20%). It writes,

“There is no stimulation from cheap money to invest more,” says Kurt Bock, chief executive of BASF, the German chemical group. “We orientate [our spending] towards growth prospects . . . and in Europe those growth prospects are modest"... “The influence of [low] interest rates is limited,” says Wolfgang Schaefer, chief financial officer at Continental, the German car parts supplier. “The equity risk premium has increased over the last three or four years . . . so the WACC has slightly increased for the automotive industry, which goes against people’s gut feeling"...

“A low cost of debt doesn’t mean a low hurdle rate,” says Marc Zenner, co-head of corporate advisory at JPMorgan. “It’s a slow process from QE and cheap money to getting firms to invest more.” Indeed, corporate boards rarely adjust the hurdle rate, meaning the impact of lower borrowing costs is not immediately passed on. Richard Dobbs, director at the McKinsey Global Institute, the consultancy’s research arm, says he has “yet to come across a corporation that has adjusted their hurdle rate or WACC to reflect the fact that we’ve had QE. Executives seem to think something funny is going on in the bond market. They’re getting these very low rates, but don’t think their true cost of capital has changed. So we’re not seeing an uptick in investment because of QE.”

6. It is well-known that India chronically under-invests in urban infrastructure, almost a seventh of what China spends per-capita. There are several reasons. Apart from the lower per-capita incomes itself, there is little or no devolution of the major direct and indirect taxes, and property tax base and rates are very narrow and low respectively. The last is captured in this graphic from an Oxfam study,

This is a matter of great concern given that property tax (in the graphic, it includes stamp duty and registration fees and wealth tax) forms nearly half of all the revenues of urban local governments. All our efforts to be smart in technology and urban planning, would come to naught without resources. So how about being 'smart' with detecting under-assessed and un-assessed properties, and dramatically improving collection efficiency? Unfortunately, even when this is acknowledged, we stray in pursuit of technology-based solutions like GIS mapping of urban areas, instead of acknowledging these as simple administrative deficiencies which require plain good governance (which technology can complement).

7. On a related note, the last municipal bond offering by an Indian city was for Rs 300 million by Visakhapatnam in 2010. Even more staggering is that this has been the only bond issuance by a city in the last ten years! Commentators who wax eloquent about bond and other alternative urban financing mechanisms would do well to keep this in mind.

8. How about software writing software? A member of a University College London team pursuing the future of software programming has this to say,

I predict that the next computing language will not be computer language but natural language, human language. If you say to your computer ‘write me a computer game in which a shark chases a man’ the computer should know what you want and create the game before your eyes. Then maybe you say ‘make the shark fiercer and faster’ and the computer will revise the code... In such a world, most programmers would be more accurately described as “trainers”. You would teach a computer to write code and to understand your intent by chatting to it.

Queue Software, a firm at the frontier of the code-that-writes-code movement, is set to release its first automated code-writing platform, Dropsource,

Dropsource writes applications based on the function and intent a user inputs. With this information, the system selects the optimum design and development approach from the same options a developer would normally consider when programming an application to, say, keep score, move between pages or gather account details. Whereas Dropsource will write the code in tenths of a second, the normal process requires a designer and/or project manager to work with a developer and write the code from scratch, even if almost identical work had been done many times over in the past.

Is repetitive, grunt-work software programming, the next frontier to fall to automation?

9. Finally, a MGI report points to a striking fact that 46% of the equity capital raised in India in the 2011-14 period came from private equity, ahead of IPOs and equity FIIs. It finds that a significant share of the more than $100 bn that has been raised in the past 13 years has flowed into small and medium enterprises and 43% of the $77 bn that flowed in the 2007-13 period went to infrastructure sector.

Contrary to conventional wisdom about asset stripping fund managers, the report finds that private equity backed firms had higher revenues and profits growth, greater job creation (6% faster), higher exports (60% faster growth), and was a more stable source of financing.

This graphic about the comparative opportunities in India and other BRICS, is reflective of our very narrow organized sector business base,

However, the report finds that the returns from Indian market has so far been disappointing. Not only have the returns been lower, very few have exited. The fact that nearly three-quarters of the PE investments in the last 15 years were made when the equity markets were trading above the period's media PE ratio, the sharp depreciation in rupee, and limited exit opportunities, and the economic weakness may have contributed to this.

No comments:

Post a Comment