The valuations of the US AI stocks and its public debt binge are not the only bubbles waiting to pop. An equally big bubble that could pop is China’s investment-driven and debt-fuelled growth model. Of the three bubbles, the last could well be the most consequential.

I had blogged here explaining the hard limits to China’s current growth trajectory. This post highlights the unsustainability of the country’s credit-driven growth.

The Economist has a very good read on China’s economic growth strategy, with its latest focus on high-technology sectors.

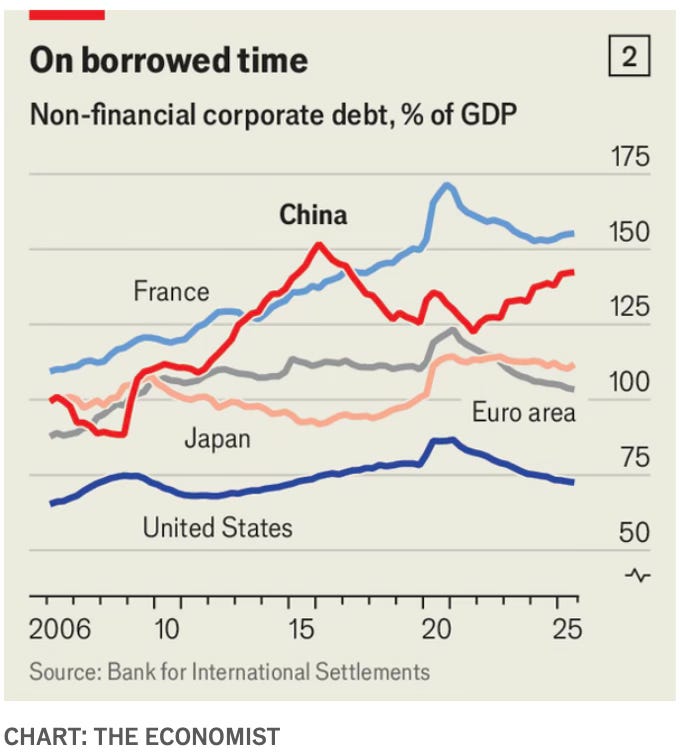

This puts China’s infrastructure investments in perspective.

The old model of growth took shape on China’s coasts before spreading to the interior. Factories in the wealthy east employed poor migrant labourers from the hinterland. Those migrants in turn, unable to obtain residency in metropolises, often used their earnings to invest in property back home. Towering apartment blocks erected during the two-decade property boom have sprung up in the smallest towns, employing tens of millions of construction workers each year and hoovering up low-end manufactures. High-speed rail has penetrated the poorest counties.All this investment was fuelled by local-government borrowing. One tally puts these debts at around 60trn yuan ($9trn), or 43% of GDP. The comparable figure in America is 12%. The poorest regions often relied the most on debt-fuelled construction of houses, roads and bridges. This has left some places, such as Guizhou province in the south-west, with dazzling infrastructure (including a bridge 626 metres high, the world’s tallest) along with insurmountable debts. Few of these costly public works have so far come close to generating the revenues needed to pay back creditors.

As the Cold War with the US and the West intensifies, President Xi has set the goal of global leadership in advanced technologies - EV, batteries, semiconductors, AI, robotics, fusion, etc. This has set the stage for a new round of competitive investments by governments across the country, with enabling credit supply measures.

A national semiconductor fund has raised roughly 687bn yuan over the past 12 years. Government-backed fund managers watched their coffers swell to nearly 400bn yuan last year, an increase of 75% from 2024. In December the state launched a 100bn-yuan national venture fund with a mandate to invest in aerospace, semiconductors, brain-linked machines and quantum technology. Many local governments, including in small cities, are creating similar vehicles using tax revenues and capital from local state companies. They are setting up “high-tech zones” and “AI parks” to lure innovative companies with tax breaks and other perks. These new tech businesses are meant to generate tax revenue and help local governments grow out of their debts, says Jean Oi of Stanford University. While officials wait for their homespun DeepSeek, the AI lab that stunned the world last year with its powerful model, the central government relaxes the rules to give them more time to repay their debts.

The massive expansion of investments and intense competition have generated spectacular failures.

In 2021 the city government of Yichun invested 2.3bn yuan to help build an EV factory in a sprawling National High-tech Development Zone. But in contrast to successful EV clusters like those in Shenzhen and Hefei, the facility was isolated from suppliers and expertise required to build cars efficiently. It has since halted production. The rest of the industrial zone looks just as lifeless… A decade ago a fund with local- and central-government money poured around 150bn yuan into Guizhou, a mountainous province in central China, mostly into data storage and cloud-computing. But these ventures could not be integrated with local industry. The companies building the data centres are based on the coasts, the server parts are made elsewhere and local demand for the data capacity is scarce… The north-western industrial city of Lanzhou has invested in commercial space flight and a “drone economy” project even as it struggled to pay its bus drivers for several years (asking them to take out personal bank loans to tide them over)…

Mr Xi’s industrial policy promotes fierce competition in which companies and their host places, sometimes down to city districts, duke it out. This competitive pressure pushes down prices and elevates quality. The best businesses which emerge from this free-for-all, like BYD in carmaking, Huawei in electronics or Xiaomi in both, are formidable and ready to take on the world. They are also rare—and concentrated in established commercial centres, with deeper talent pools and pockets. Profits are even rarer. Investment returns accrue less to individual companies and more to integrated supply chains, which lower costs and speed up product cycles and innovation, says Chi Lo of BNP Paribas, a bank.

The share of industrial firms generating losses has shot to a record high of around 32% in April, up from 10% in 2011 and above the previous peak during the Asian financial crisis in 1998. Corporate debt is also high and rising. Mark Williams of Capital Economics, a consultancy, notes that Chinese firms owe twice as much to domestic banks and bond investors today as they did in 2019. In that period, GDP has expanded by a third. Companies may move away from productive activities and instead chase subsidies that are available for centrally supported sectors, he says… a trio of IMF economists calculated last year, China’s “total factor productivity” (which captures how efficiently both capital and workers are used) was 1.2% lower than it would have been in the absence of industrial policy over the past decade or so. GDP was 2% lower, equivalent to forgoing around $400bn in value added each year. The more companies get caught up in the chase for subsidies and, by slashing their prices, for customers, the harder it will be for them to wring out profits.

China faces a confluence of headwinds - slowing economy; weakening aggregate demand and consumer sentiments (with persistent low domestic consumption); ten quarters of factory deflation (PPI −2.6%) (involution or neijuan); the property market still in crisis and recovery perhaps still a few years away; local governments deeply indebted; large excess capacity across industries; growing backlash among trade partners against surging Chinese exports; intense competition among domestic companies squeeze margins and are leaving companies running losses; and zombie firms kept alive by local and central government subsidies, cheap credit, and debt repayment rescheduling.

Each panel below is a single number with its recent track. Red is contracting or dangerous; amber is stalling; green is the part still running hot, which is exactly where the next overcapacity is building.

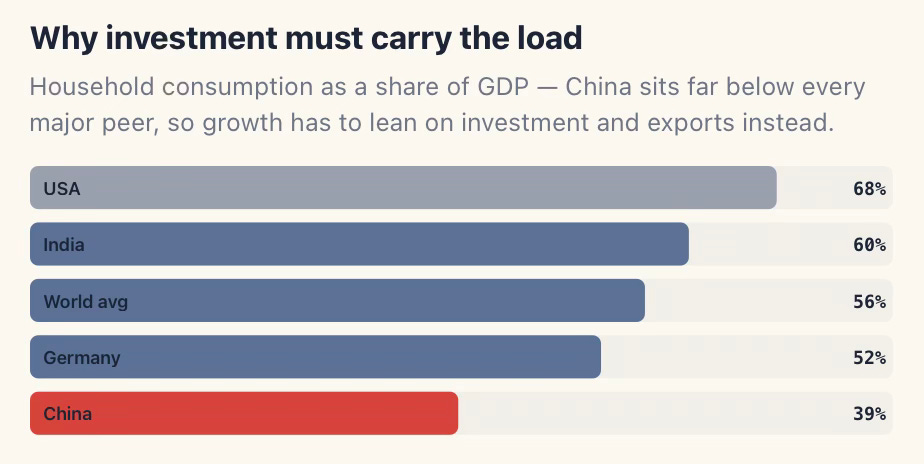

In an environment where consumption is weak, any squeeze on investment and reduction of exports (due to rising backlash among trade partners) will only lead to job losses and social discontent. This has increased the reliance on investments to achieve the 4.5-5% GDP growth rates.

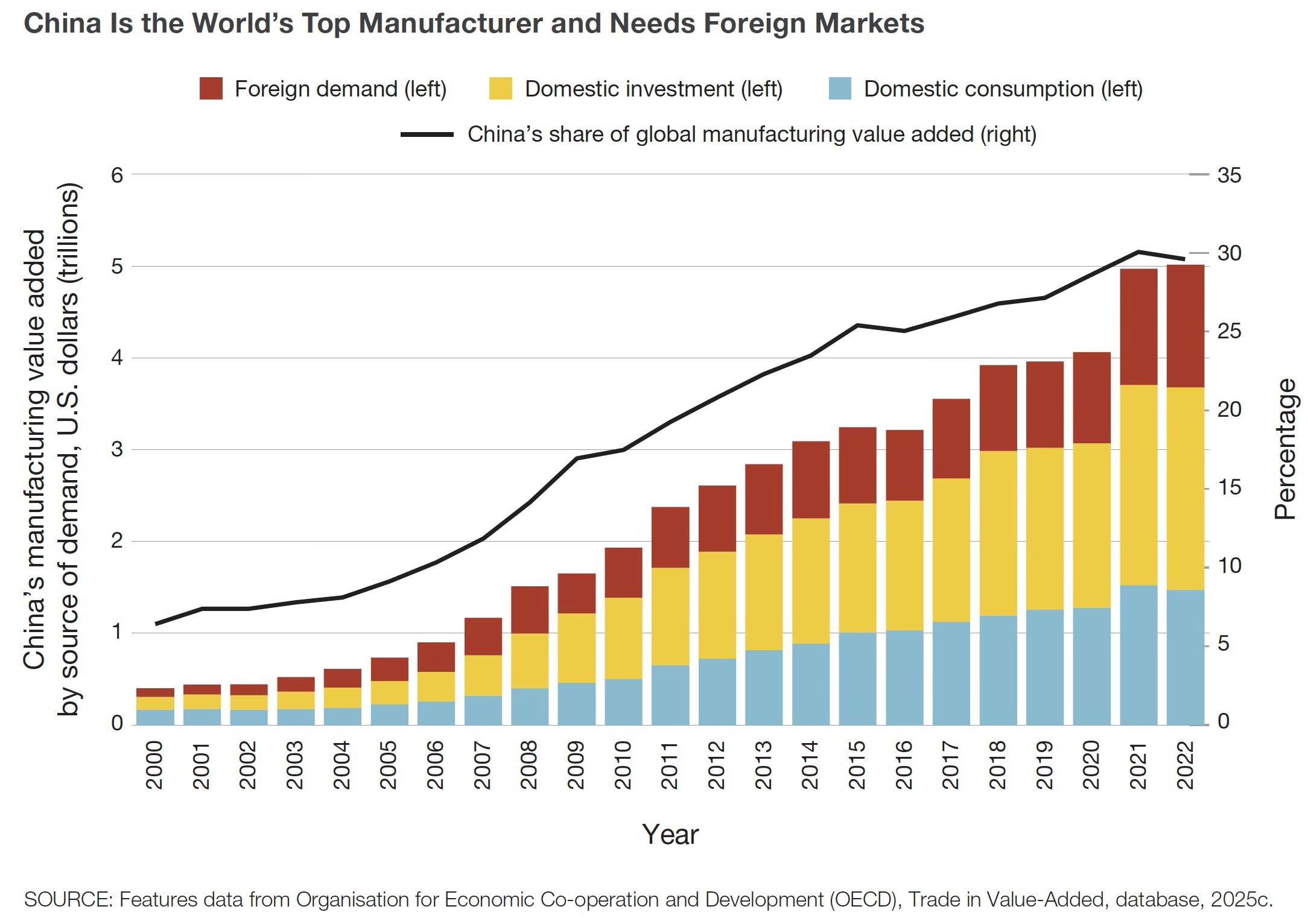

And exports are critical to absorb the excess capacity that has been built up.

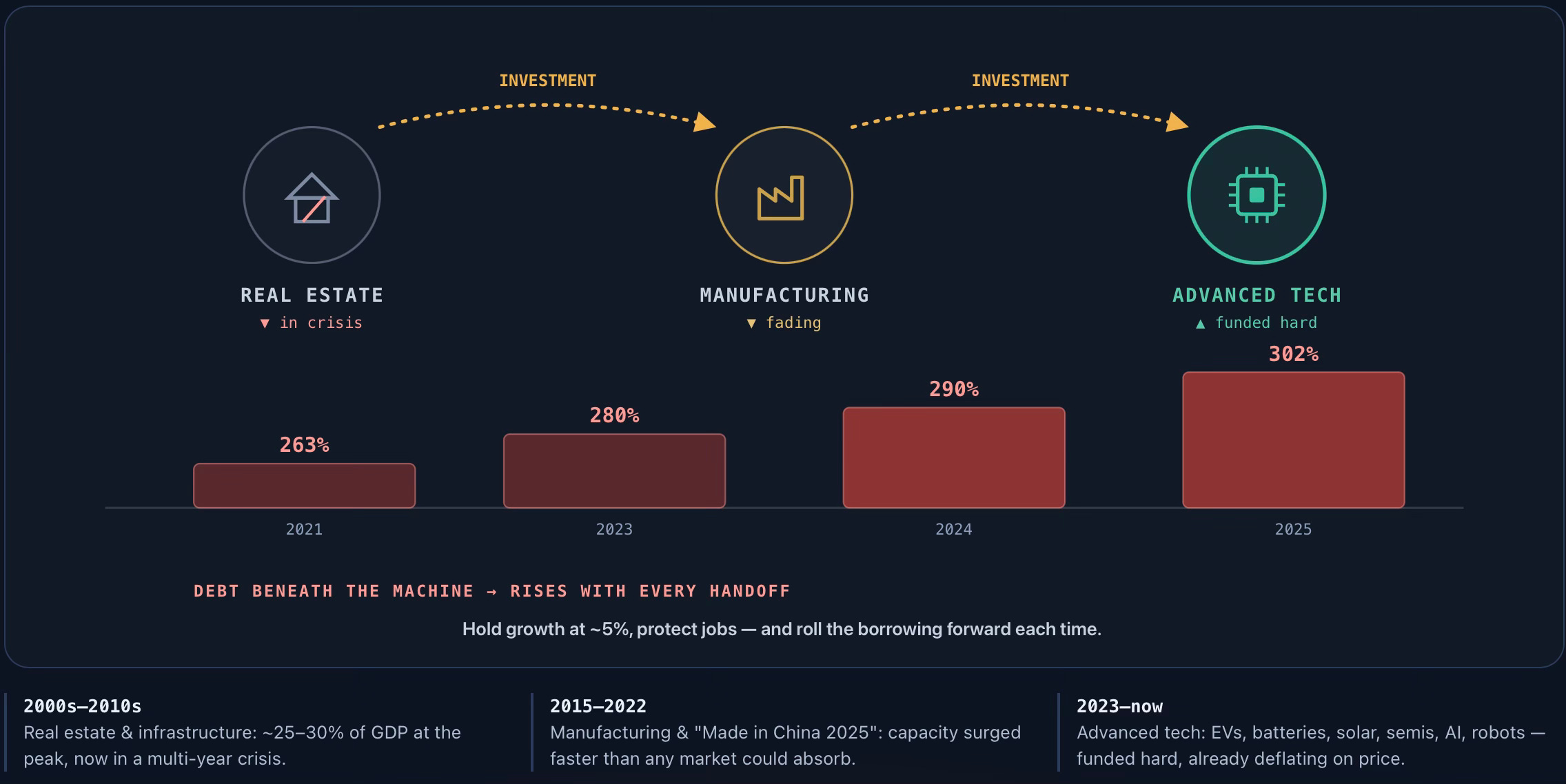

After infrastructure, real estate, and manufacturing in the first two decades, the current focus of the investment-driven growth model has been advanced technology sectors like EVs, batteries, semiconductors, robotics, AI, etc., where there is also a geopolitical imperative arising from the Cold War with the US. The macroeconomic policy mantra has been to “hold growth at ~5%, protect jobs, and roll the borrowing forward each time.”

All this points to the model of a giant economy-scale Ponzi scheme where investment is shifting from one sector to another in order to sustain a target GDP growth rate and prevent job losses, while also accumulating a growing pile of massive debts.

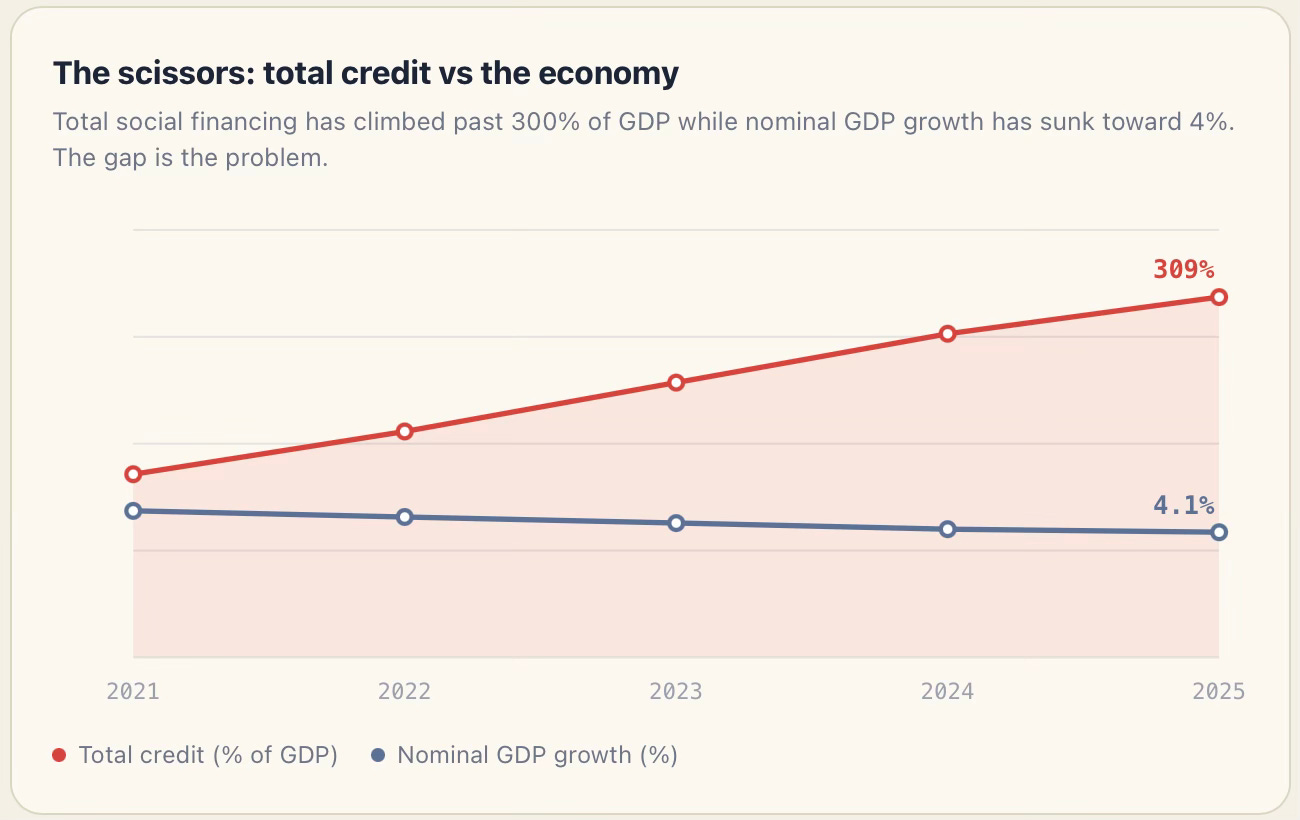

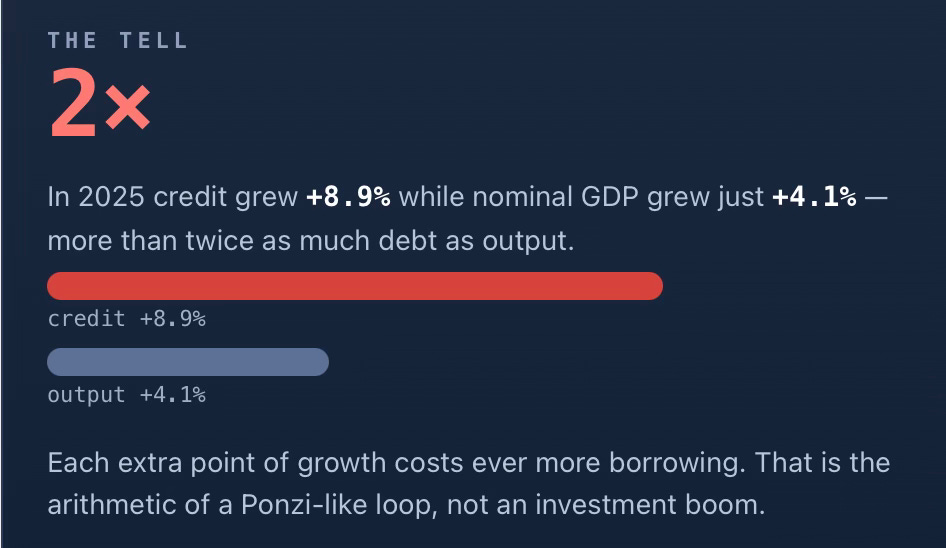

A debt-funded model works only while each new yuan of credit produces enough output to service it. In China, that link has snapped: credit keeps compounding while nominal growth fades - the classic signature of a system paying old debts with new ones.

The cleanest unsustainability signal isn't the debt level per se but its productivity: total social financing has passed 309% of GDP, and in 2025 credit grew +8.9% while nominal GDP grew just +4.1% — more than twice as much debt as output. When each extra point of growth costs ever more borrowing, new credit is increasingly servicing yesterday's liabilities rather than funding tomorrow's, which is the arithmetic that ends the loop. And this is also reflected in the continuously rising fiscal deficit, especially in the off-balance sheet side.

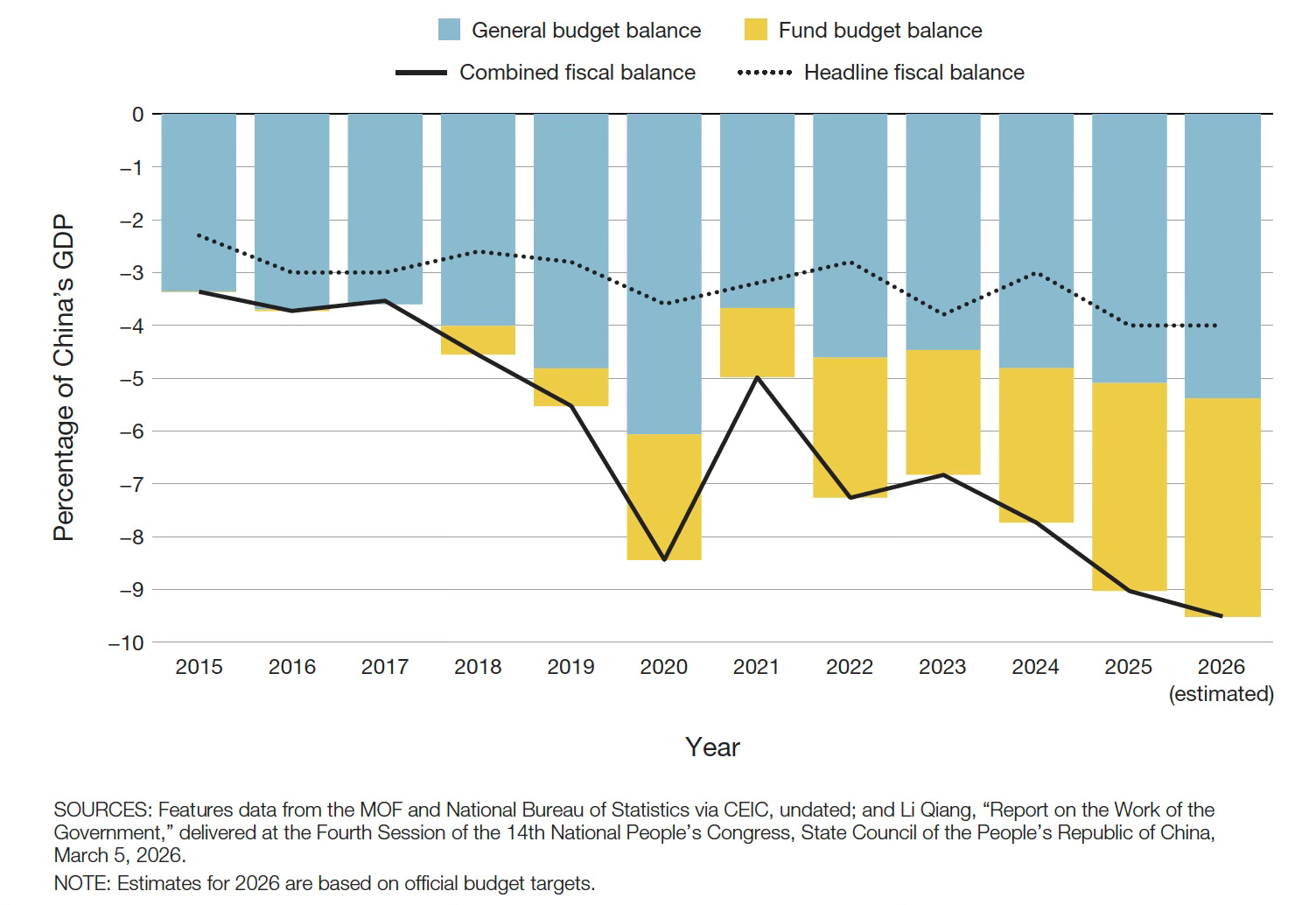

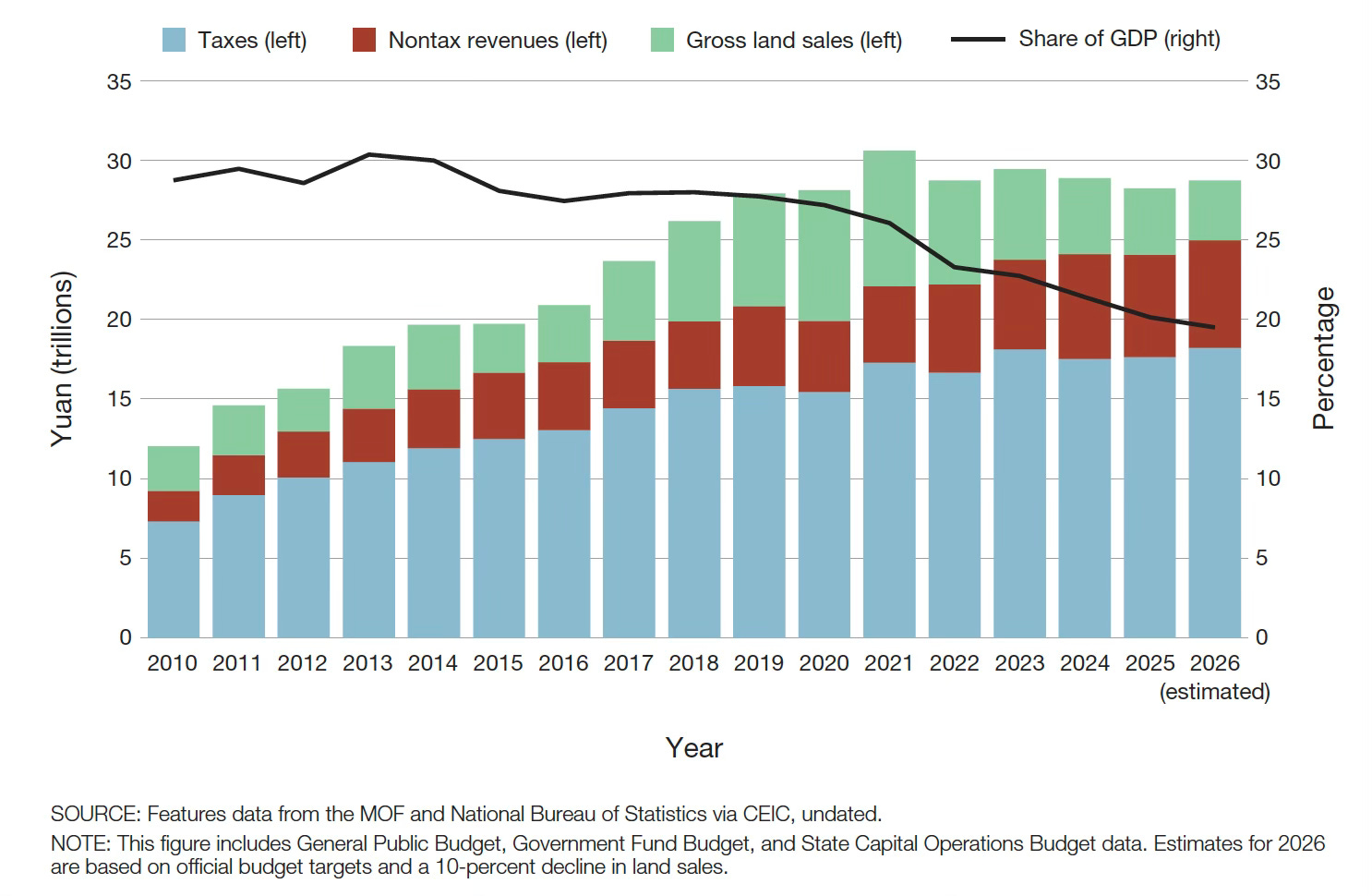

Worsening matters, these trends coincide with a period in which fiscal revenues have flatlined in nominal terms and declined relative to the economy since 2020.

As the RAND report writes, with the fiscal space disappearing, the government has relied on credit and mandates to keep the wheel spinning.

Beijing can still mobilize large-scale borrowing for industrial policy. The central government and policy banks retain substantial capacity because Beijing can expand bond issuance, and national commercial or policy banks raise trillions of yuan annually in quasi-sovereign debt to finance strategic sectors. By contrast, local governments are squeezed; bond quotas are capped, land sale revenue has fallen, and off–balance sheet LGFV borrowing is under regulatory pressure. The most important immediate trigger was Beijing’s “three red lines” policy introduced in 2020, which sharply curtailed developer borrowing and land sales. Because land sales to developers had long been a major source of revenue for local governments, the resulting property downturn led directly to a collapse in land sale proceeds and fiscal capacity at the local level. A correction was likely inevitable because of the structural exhaustion of a land finance model that relied on perpetually rising property values to fund local growth. Therefore, localities are less able to cofinance subsidies or guidance funds.

Policy is shifting as a result. Centrally directed (or funded) credit and investments remain important. Meanwhile, traditional cash subsidies and local incentives play a reduced role. Government procurement has fallen relative to GDP. Instead, Beijing is leaning on lower-cost directives and mandates (including procurement requirements, regulatory obligations, and selective credit guidance) that require less fiscal outlay but effectively spread the costs of industrial policy across firms and institutions required to comply.

There are hard limits to how far this can go.

Since around 1980, the political bargain between the Communist Party and the Chinese people was simple - rising prosperity in exchange for political acceptance. With consumption weak, any squeeze on investment, or a real loss of export markets to a rising trade backlash, flows straight into jobs. Youth unemployment is already near 18%. The flywheel is kept spinning not only for growth, but to keep that bargain intact. How long can the flywheel keep spinning?

1 comment:

May be a case study of the perlis of perfect competition conditions

Only question is if china is capable of solving liquidity crisis once again

May be yes in my view

Could they avoid a Japanese zombification, Not sure !

Post a Comment