1. In terms of annualised returns for several time periods, the Indian stock market tops, slightly superior to even the S&P 500.

But the big worry is the nature of its growth. In particular, the widening inequality and the relatively low growth in incomes for the vast majority is the problem. In other words, is the growth broad-based enough to sustain the high growth rates?

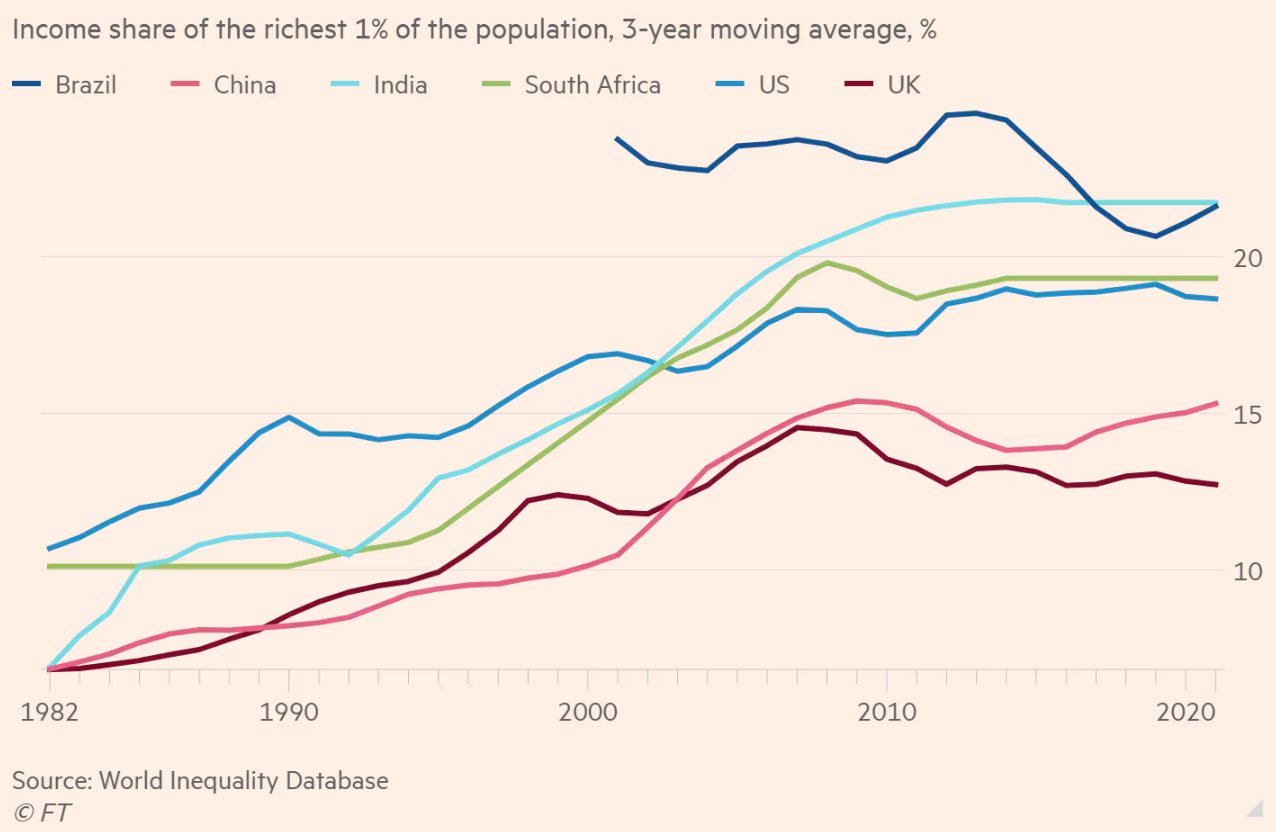

Whereas the share of GDP going to the top 1 per cent grew in China between the 1980s and the 2010s from 7 per cent to 13 per cent, in India it rose from 10 per cent to 22 per cent. India today is more unequal than post-apartheid South Africa and in the same ballpark as Putin’s Russia.

Yes, there is an Indian upper middle class that invests in the local stock market and that group is growing. But it accounts for 3 per cent of India’s population. By comparison, 13 per cent of Chinese hold some investment in the stock market, as do 55 per cent of Americans. And, as we know from the US, the vast majority of those retail investors have tiny holdings...In 2020 on the World Bank’s Human Capital Index — which measures countries’ education and health outcomes on a scale of 0 to 1 — India achieved a score of 0.49, below Nepal and Kenya, both poorer countries. China scored 0.65, putting it on par with Chile and Slovakia, which have higher GDP per capita. Most dramatically disadvantaged are India’s women. Since 1990, Indian women’s labour market participation has fallen from 32 per cent to about 25 per cent. And behind them come hundreds of millions of underskilled youngsters. In 2019 less than half of India’s 10-year-olds could read a simple story, compared with more than 80 per cent of Chinese children and 96 per cent of Americans. In the coming decade, 200mn of these poorly educated young people will reach working age. A large share of them will probably end up eking out a living in the informal sector and getting by on handouts. Unemployment amongst the under-25s already runs at more than 45 per cent.

The article makes very good points, but it also makes some bloopers.

Political connections may not give you the technological edge. But what they do deliver is easy credit. India’s growth has been heavily debt fuelled. Today it is Adani’s financial engineering that makes the headlines. But if you remember back to before the coronavirus pandemic, India was in the grips of a widespread bank crisis. Raghuram Rajan took on the job as governor of the Reserve Bank of India in the hope of cleaning house. By 2016 he was gone.

This is very bad analysis. For one, to extrapolate from the debt-fuelled rise of Adani to other corporate groups itself is wrong. In fact, the top Indian companies must be among the least leveraged and best performing in terms of return on equity etc globally. But to extend it to the Indian economy itself is ridiculous. The corporates have deleveraged and the banks have cleaned up their balance sheets. The household leverage is low, and sub-national government entities like municipalities are deeply under-leveraged. And Raghuram Rajan having initiated cleaning up the banking sector is more a lazy regurgitation of the popular social media narrative than any half-serious analysis.

This is also the problem with commentators like Adam Tooze and Tyler Cowen who write on a very wide range of topics, based on secondary readings. It's one thing to write on Germany and European history, and point to good articles on the widest range of issues, but to start commenting about the fine details of Indian economy or African history is where they go terribly wrong and lose credibility.

2. Times has a great story on Nepal's Pokhara International Airport which was built with Chinese debt and by Chinese companies, which is one more example of how the Belt and Road Initiative has thrust unnecessary infrastructure on low income countries and indebted them.

The Pokhara airport highlights the pitfalls for countries that import China’s infrastructure-at-any-cost development model, which spins off money for Chinese firms, often at the expense of the developing country. In Nepal, China CAMC Engineering, the construction arm of a state-owned conglomerate, Sinomach, imported building materials and earth-moving machinery from China. The airport, built to a Chinese design, is packed with security and industrial technology made in China... an investigation by The New York Times, based on interviews with six people involved in the airport’s construction and an examination of thousands of pages of documents, found that China CAMC Engineering had repeatedly dictated business terms to maximize profits and protect its interests, while dismantling Nepali oversight of its work. This has left Nepal on the hook for an international airport, at a significantly inflated price, without the necessary passengers to repay loans to its Chinese lender...CAMC’s winning bid of $305 million, almost twice what Nepal had estimated the airport would cost, raised the ire of some Nepali politicians, who called the price outrageous and the bidding process rigged. CAMC then lowered the price about 30 percent, to $216 million. China and Nepal signed a 20-year agreement in 2016; a quarter of the money would be an interest-free loan. Nepal would borrow the rest from the Export-Import Bank of China, a state-owned lender that finances Beijing’s overseas development work, at 2 percent interest. Nepal agreed to start repaying the loans in 2026.

The lack of local oversight is shocking

Nepal’s aviation agency was supposed to have teams of domestic and international experts as consultants, critical for a project of this magnitude, he said. But key roles were vacant, and the positions that were filled relied on recent college graduates with almost no experience. The initial construction budget had earmarked $2.8 million for Nepal to hire consultants to make sure CAMC was abiding by international construction standards, according to documents. As the project went on, the Chinese firm and Nepal lowered that allocation to $10,000, using the money elsewhere...CAMC had started work before any consultants were in place, and that the work CAMC had done did not meet international standards. CAMC completed earth-filling work for the 8,200-foot runway, but it had no documentation that it had tested the soil density... no one on the Nepal side “knew how the foundation of the runway was built.” Without proper soil density, the runway could become bumpy or littered with cracks and potholes in the future... CAMC designed the airport drainage system without taking into account historical rainfall data in locations across Pokhara and the sloping topography near the site, forgoing a standard practice in international construction... There was also no paperwork ensuring the quality of Chinese-made building materials or information on the Chinese vendors providing the components... contrary to the stipulations in CAMC’s contract with Nepal... China’s Export-Import Bank, which had provided the loan, had appointed China IPPR International Engineering, a consulting firm, to track the quality, safety and timetable of the construction.

3. From an FT investigation on the hot-button topic of over-invoicing by the Adani Group

In January 2019, the DL Acacia, a 229m-long bulk carrier with a South Korean owner and Panamanian flag, departed the Indonesian port of Kaliorang in East Kalimantan carrying 74,820 tonnes of thermal coal destined for the fires of an Indian power station. During the voyage, something extraordinary occurred: the value of its cargo doubled. In export records the price was $1.9mn, plus $42,000 for local costs. On arrival at India’s largest commercial port, Mundra in Gujarat run by Adani, the declared import value was $4.3mn. The DL Acacia cargo was one of 30 shipments imported into India by Adani Enterprises that the FT examined in detail. In each case, the vessel’s customs records in India were matched with those filed in Indonesia. The records cover the period between January 2019 and August 2021, after which time Indonesian records ceased to be available...

According to the Indonesian declarations, these 30 representative sailings — totalling 3.1mn tonnes — cost $139mn, plus $3.1mn in shipping and insurance costs in Indonesia. The values declared to customs officers in India came to $215mn, suggesting the voyages made up to $73mn in profits, far in excess of plausible shipping costs. Coal trading is typically a high volume competitive business with profit margins in the low single digits. Priced in dollars per tonne, one expert in the Indonesian trade said “anything more than a couple of dollars above the market rate raises an eyebrow”. Adani Enterprises, the group’s oldest and most valuable company, generates the lion’s share of its sales and profits from its coal trading division called Integrated Resources Management...

Three “middlemen” companies that supplied the Adani group with coal appear to have made more substantial amounts: Hi Lingos in Taipei, Taurus Commodities General Trading in Dubai, and Pan Asia Tradelink in Singapore. Indian import data since July 2021 indicates Adani paid a total of $4.8bn to the three companies for coal sourced at substantial premiums to market prices... Senior industry traders questioned the use of little-known trading houses, as large buyers of coal generally prefer to partner with big trading houses that have strong credit ratings and a reliable record for commodity deals involving the exchange of hundreds of millions of dollars... Of the Indian import records reviewed, 311 shipments originating from Indonesia listed the calorific content of coal supplied to Adani by the middlemen. All but a few were priced at a premium to what the closest Argus benchmark price had been two to four weeks earlier, the typical shipping time from Indonesia to Gujarat. The median premium was 14 per cent.

4. The protest democracy that South Korea is

Protest rallies have been a fixture of this capital city of Asia’s most vibrant democracy for decades, born during South Korea’s difficult march toward democracy in the 1980s when massive crowds, often armed with rocks, firebombs and even stolen rifles, clashed with riot police, tanks and paratroopers. Distrustful of their government, South Koreans have a penchant for taking all manner of grievances to the streets, so much so that it has turned demonstrating into a kind of national pastime.As the coronavirus pandemic has receded, protest rallies have returned to Seoul with a vengeance. Barely a weekend passes without the city center turning into a raucous bazaar ringing with livestreamed protest songs, slogans and speeches that reveal a country increasingly polarized over its president. The vast majority of protests now are organized by rival political activists who use social media, especially YouTube, to mobilize supporters and livestream their gatherings. With churchgoers and other elderly citizens on the right, and mostly younger progressives on the left, they have become a public referendum on President Mr. Yoon Suk Yeol and his policies...A typical demonstration features colorful banners and dance troupes romping on a temporary platform as concert speakers dangling from crane trucks blare protest songs. Organizers lead the crowd in chanting slogans, pumping their fists in unison or waving national flags. Peddlers weave through the throng hawking rain cover in summer and plastic cushions in winter. The hourslong rally usually ends with a march. Police officers walk alongside the demonstrations to keep order. Most of the rallies don’t make national news. But when they grow in size and intensity, they can herald a political storm ahead. Massive protests spearheaded by progressives in 2017 triggered the impeachment of Park Geun-hye, who was then the country’s conservative president. Monthslong protests led by Christian evangelicals galvanized a conservative pushback against Ms. Park’s progressive successor, Moon Jae-in, and helped Mr. Yoon win election as a conservative candidate in 2022...Protest rallies in South Korea share elements of the populism sweeping much of the world. Both right- and left-wing activists accuse traditional news media of spreading fake news and political bias. They rely on social media platforms like YouTube for alternative news sources, using them to spread fears that South Korea is being dominated by a deep state (of corrupt conservatives or pro-North Korean progressives, depending on which YouTube channel one listens to). Livestreaming protest rallies has become a staple for partisan YouTube channels.

5. An article that explains how hard it's to diversify away from China for production of iPhones and how Chinese employees are assuming higher value added jobs in Apple's value chain,

Chinese companies with operations in India will still play a key role in Apple’s plan to make some iPhones in the country. In Chennai, India, the Taiwanese supplier Foxconn, which already manufactures iPhones in factories throughout China, will lead Indian workers’ assembly of the device with support from nearby Chinese suppliers including Lingyi iTech, which has subsidiaries to supply chargers and other components for iPhones, according to two people familiar with the plans. China’s BYD is setting operations to cut glass for displays, as well, these people said... The company is now increasingly tapping China to supply high-wage workers to do these jobs, these people said. This year, Apple has posted 50 percent more jobs in China than it did during all of 2020, according to GlobalData, which tracks hiring trends across tech. Many of those new hires are Western-educated Chinese citizens, these people said.The change in the way Apple works has coincided with an increase in the number of Chinese suppliers it uses. A little over a decade ago, China contributed little value to the production of an iPhone. It primarily provided the low-wage workers who assembled the device with components shipped in from the United States, Japan and South Korea. The work accounted for about $6 — or 3.6 percent — of the iPhone’s value, according to a study by Yuqing Xing, an economics professor at the National Graduate Institute for Policy Studies in Tokyo. Gradually, China nurtured homegrown suppliers that began to displace Apple’s suppliers from around the world. Chinese companies began making speakers, cutting glass, providing batteries and manufacturing camera modules. Its suppliers now account for more than 25 percent of the value of an iPhone, according to Mr. Xing.

6. FT long read on US Treasury basis trade by hedge funds, that involves paying two very similar debt prices against each other - selling futures and buying bonds - and extracting gains from the small gap using borrowed money.

The basis trade works by exploiting the gap in prices between Treasury futures, which commit users to buying at a certain price on a future date, and on cash bonds. Hedge funds sell the futures and buy the cash bonds, which they can deliver to the counterparty when the futures contract comes due. The difference between Treasury and futures prices is small, often just a few fractions of a percentage point, so the return is minuscule. But hedge funds can magnify their bets that the gap will close by using borrowed money to fund the trade.Because Treasuries are considered the highest quality collateral, the prime brokerage divisions of major Wall Street banks are happy to lend against them, often at their full face value rather than a slight discount. In the repo market — short-term lending that facilitates a lot of Treasury trading — hedge funds need to post only small amounts of cash against their credit lines, sometimes levering up by more than 100 times. There is borrowing on the other side of the trade too; futures are inherently leveraged products and again, hedge funds need to put up only a small amount of collateral to satisfy the margin requirements of futures exchanges. Ten-year Treasury futures offered by US exchange group CME allow trades of up to 54 times the cash margin posted, for instance. By taking advantage of the ability to borrow on both sides of the trade, hedge funds can deploy huge leverage. The head of one fund that has engaged in this trade says traders have in the past been able to lever up to 500 times.

7. Is Xi Jinping China's latest Bad Emperor?

A Chinese reprint of a book about an emperor who ran his realm into the ground before committing suicide nearly 400 years ago has abruptly disappeared from book shelves in China and searches for it have been censored online. The Book Chongzhen: the Diligent Emperor of a Failed Dynasty, republished last month, recounts how the last emperor of the 1368-1644 Ming dynasty purged senior officials and mismanaged his kingdom before finally hanging himself on a tree outside the Forbidden City as rebels closed in on Beijing. The blurb on the book’s cover declares that the harder Chongzhen worked, the faster he brought about the collapse of the empire. “A series of foolish measures [and] every step a mistake, the more diligent [he was] the faster the downfall,” it says.

No comments:

Post a Comment