1. It's disingenuous to describe the modern capitalist economy as one which promotes meritocracy. A better description would be one that entrenches the established order. The main channel to access life's opportunities, education system, is full of subtle entry-barriers. These barriers include the vastly greater non-school learning opportunities, expensive and elite private schools, higher admission probabilities to the best colleges, patronage networks that open entry-level positions in high-paying occupations like finance and management consulting etc.

This from a current student at Stanford University describes how private school students are disproportionately represented in Ivy League colleges.

2. Surprising that India has the second largest abortion rate among large economies.

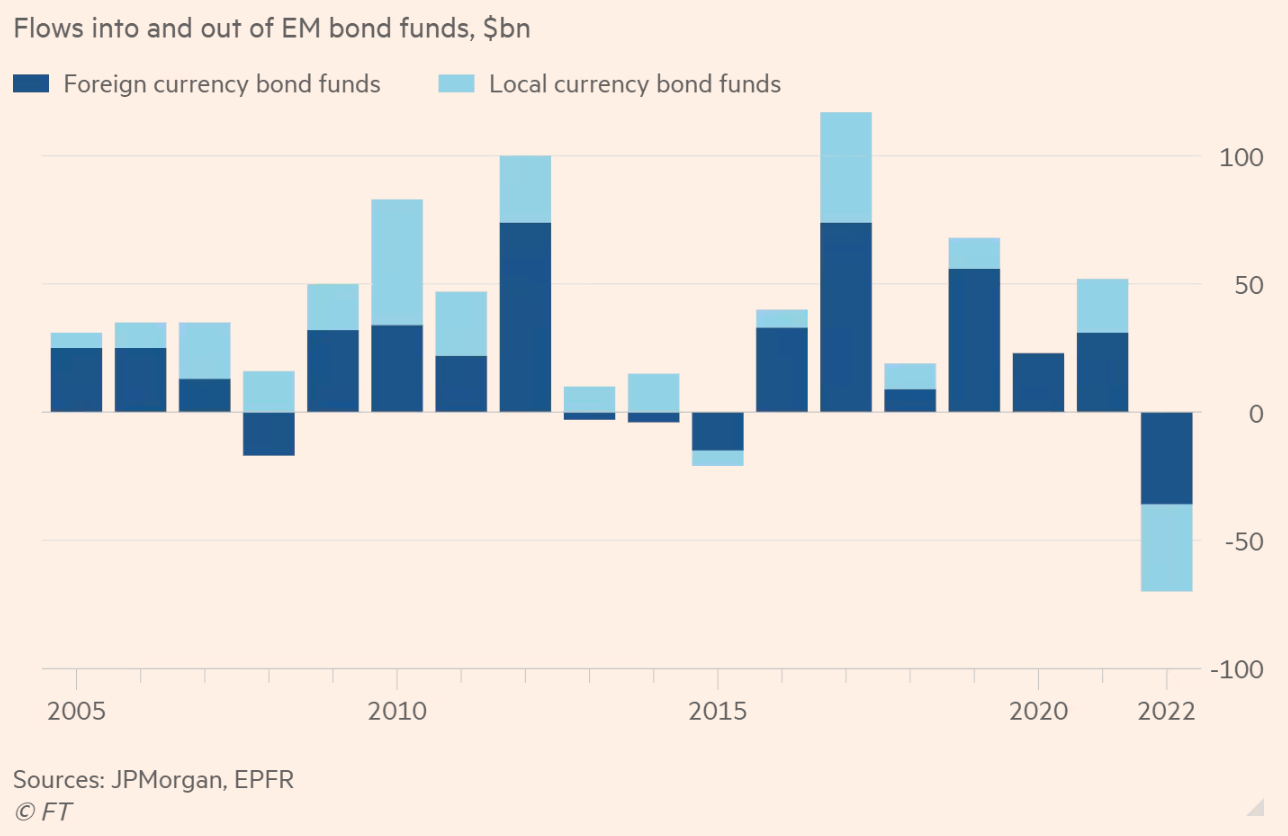

The investor flight underscores how emerging markets are facing mounting risks from surging interest rates in developed markets, which make the typically high yields on EM debt look less attractive... Rather than weighing the relative risks of currency exposure, investors are simply getting out. It marks a sharp turnround: flows were positive into both types of bond funds for each of the previous six years, at a combined average of more than $50bn a year.

3. FT writes on the controversies surrounding Edtech decacorn Byjus, whose $22 bn valuation is now masked by accusations of revenue recognition frauds, mis-selling and toxic work culture, and suffered a loss of $560 million in 2021.

Evidence that tax cuts for higher earners create incentives for broad-based economic growth is weak. A recent study by two researchers at King’s College London, which examined 50 years of tax cuts for the rich in advanced economies, found that those cuts did not have a significant effect on economic growth or unemployment and did increase income inequality. Studies of former President Donald J. Trump’s 2017 tax cuts suggest that they did not deliver the steep gains in investment and productivity as promised.

FPIs now hold around $600 billion of Indian equities. Of this, mutual funds and hedge-funds (MFs/HFs) hold 68 per cent, sovereign wealth funds (SWFs) 16 per cent, pension and insurance funds 8 per cent, and others 8 per cent. SWF flows have very low volatility... Flows from pension and insurance funds are also less volatile... While MFs and HFs are two-thirds of FPI holdings, they accounted for three-fourths of FPI outflows that India saw between September 2021 and June 2022. To understand this better, we analysed monthly data on 6,300 such funds, which have total assets under management of just under $4 trillion. Despite their heavy selling of India, the India weight in their portfolio remained unchanged at 13 per cent, indicating that these funds were only trimming their India positions as their funds saw outflows.

7. Vodafone India CEO, Akshaya Moondra, suggests that 58% of the telecom revenues end up as government taxes,

“We have 18 per cent goods and services tax (GST) and 12 per cent licence fees and spectrum use charges. This 30 per cent is very visible to everyone. What is not visible is the price of spectrum, if converted to an annuity value and calculated as a percentage of revenue. It adds another 28 per cent of industry revenue (as a cost). So, if you take the industry revenue of Rs 231 crore and you calculate the total value of spectrum given out — which is close to Rs 6 trillion today, the annuity value comes to 28 per cent of the revenue. This is on top of the visible costs. Therefore, 58 per cent of revenue is reflected as government levies in a country where the tariffs are the lowest."

8. China's share of all mobile phones production was 67% in 2021, compared to India's 16%. The respective numbers were 74% and 9% in 2016.

Financial Times analysis suggests India’s monetary tightening and foreign exchange market interventions in defence of the rupee have helped prevent much larger depreciation of the kind suffered by most other leading Asia-Pacific currencies this year.... The RBI’s intervention in the currency market appears to have been most intense in March, the first month after Russia’s invasion of Ukraine. India sold a net $20bn that month to support the rupee, as the war fuelled a rise in commodity prices... India sold a further net $19bn in July, the most recent month for which data are available, when the US Federal Reserve raised rates and signalled further increases to come, piling the pressure on emerging market currencies. The RBI’s intervention has helped the rupee outperform most other Asian currencies this year, falling less than 10 per cent against the US dollar, compared with declines of more than 15 per cent for the Korean won and Japanese yen...

“Given the circumstances, and despite the very aggressive tightening by the RBI, the rupee should have depreciated more,” said Priyanka Kishore, head of India and south-east Asia at Oxford Economics. “But the bank’s foreign exchange intervention had kept it quite stable until recently.”... Analysts said India’s limited capital controls might have helped reduce the volatility of trade in the rupee, but the RBI’s selling of reserves and the economy’s relatively strong growth prospects had played a larger role in easing pressure on the currency.

Despite being small and densely populated with expensive land and labour and a cool damp climate, Netherlands has become the world’s second-biggest exporter of tomatoes — in fact the second-biggest global agricultural exporter overall by value. Dutch growers have a history of raising plants in greenhouses, thanks to the flower industry, and of agricultural innovation more generally. For decades they’ve been building a fertile ecosystem of research, development and production. Specialist companies have produced complementary products for high-tech indoor vegetable and fruit farming such as innovative lighting and climate and water management systems... How did the government help? Well, it wasn’t through shelling out market-distorting subsidies or relying on heavy trade protection. The Dutch government has supported farmers in various ways, not least by financing the public Wageningen University, one of the world’s best agribusiness research centres... Unlike the UK, the Netherlands has remained very firmly in the EU with its complex web of rules on food hygiene and horticultural standards. It also has high labour costs and a commitment to reduce carbon emissions. Dutch growers pride themselves on their low environmental impact. EU regulations are among the world’s toughest, so being practised in complying with them helps their farmers to meet standards in markets elsewhere.

The point being that UK-type deregulation is unlikely to help trigger economic growth.

11. The decision by South African Naspers-owned Dutch technology investor, Prosus, to pull back in its advanced acquisition process for India's payments market leader BillDesk raises several interesting issues. The $4.7 bn deal announced in August 2021 would have been the second biggest technology company acquisition in India after Walmart's 2018 acquisition of Flipkart for $16 bn. Prosus was proposing to buy BillDesk through its Indian payments company, PayU.

Livemint has characterised the decision as an example of "buyer's remorse" taking over and forcing Prosus to back out. India's fintech sector has been red hot, attracting $29 bn in funding since 2017, which forms 14% of global VC funding to the sector. As of July 2022, India had 23 unicorns in the fintech space.

Now that the tide has fallen and the funding winter is on us, those swimming naked are being exposed. At the global level, the valuation of Swedish Buy Now Pay Later (BNPL) fintech, Klarna AB, collapsed spectacularly by 85% from a stratospheric $46 bn in June 2022 to just $6.7 bn as it raised $800 million in fresh funding. In India, the valuation of fintech darling PayTm has dived by 70% since its IPO. While not a fintech, the problems at another iconic technology firm, Byju's, has also added to the negative sentiments about technology investing.

The Prosus decision is important since the combination of PayU and BillDesk would have created an entity with nearly half the market share in the payments space. Currently PayU has a 15% market share and BillDesk 25-33%. With EY predicting India's fintech sector to hit $1 trillion in throughput and $200 bn in revenues by 2030, the combined entity would have been in a pole-position to capitalise on a rapidly growing market segment.

In this context, apart from the valuation, the decision conveys questions about the market growth and the business profitability assumptions. It's also a teachable example of how bad practices by market leaders (PayTm and Byju's here) can have externalities on the sector as a whole. Just as when the market was going up, their booming valuations were drawing investors, their evident weaknesses are now putting off capital from technology companies.

No comments:

Post a Comment