1. A stand out winner from the Russian invasion of Ukraine is Qatar. With its massive gas reserves, it has become the most important source of incremental gas supplies for Europe.

Europe’s clamoring for liquefied natural gas, or LNG, comes after Qatar started a $30 billion project to boost its exports by 60% by 2027. The extra demand means more competition among buyers for long-term supply contracts and, most likely, better terms for Qatar. Before the outbreak of the Ukrainian war, some analysts doubted there’d be enough business to justify the expansion plan. Now, Qatar is sounding out customers about an even bigger enlargement... Qatar is reaping benefits already. The $200 billion economy is set to grow 4.4% this year, the most since 2015, according to Citigroup. Gross domestic product per person will soar to almost $80,000, back up toward levels in places like the Cayman Islands and Switzerland. The start of what could be a gas “supercycle” comes just as the World Cup construction boom that powered the economy in recent years comes to an end, according to Ziad Daoud, chief emerging markets economist at Bloomberg Economics. “The timing is fortunate for Qatar, which could see a new driver of growth for this decade,” he said.

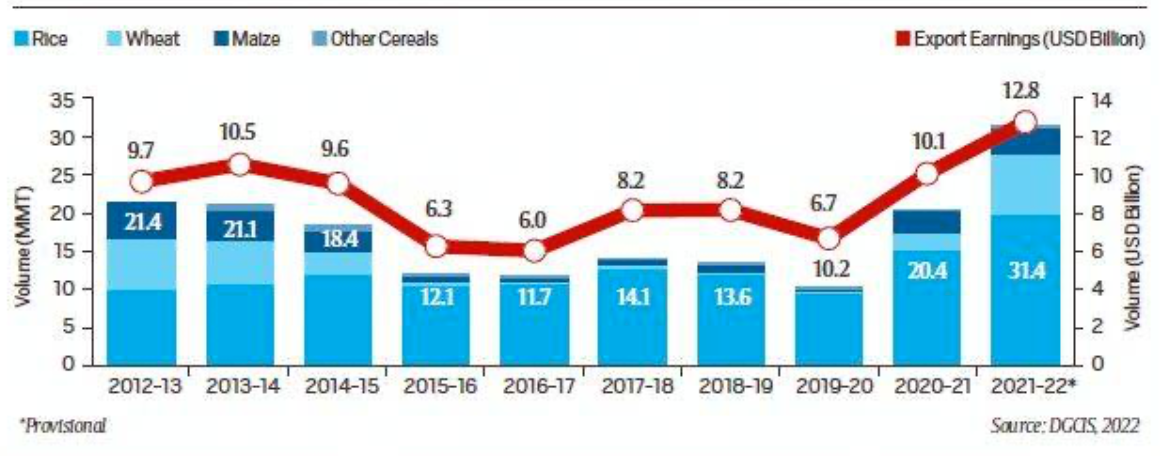

2. India's cereal exports have been rising.

March alone saw the sixth consecutive month of FPI outflows, which was the most severe since March 2020 (after the pandemic scare) on the back of continued geopolitical risks, elevated inflation led by supply side issues, rising commodity costs... Apart from India, other emerging markets, including Taiwan, Korea and the Philippines also saw massive outflows so far this fiscal. The record fall was mainly due to the massive outflows of USD 5.4 billion in March and a whopping USD 15.7 billion in FY22. Such a massive pullout came after they pumped in USD 23 billion in 2020 and USD 3.7 billion in 2021.

4. Striking numbers about the Mathew Effect in school education in UK

All fee-paying (private) schools... collectively educate about 6% of the British school-age population. They also make up a disproportionate share of the student body at top universities (40% at Oxford, 35% at Cambridge, 32% at the London School of Economics) and of elite British professions (65% of senior judges, 29% of members of Parliament, 43% of journalists... Adjusted for inflation [at the time this was written in March 2020], British private schooling has become three times more expensive since 1980. The rise owes in part to a facilities arms race that ran unimpeded until the financial crash of 2008, as schools once synonymous with character-forming privation became increasingly luxe.

The article describes how England's private schools are increasingly establishing their franchises abroad, especially in Eastern Europe, East Asia, and Middle East.

As fee escalation put private schools beyond the reach of their traditional demographics, they started admitting more students from overseas, but the gambit had limits. Bringing in too many foreign students risked diluting the Harry Potteresque cachet that had attracted their parents in the first place. “They don’t want to have lots of internationals. They want lots of British kids,” says Lorna Clayton, whose company Academic Families places foreign students in U.K. schools. So the schools came up with franchising, which would bring in money and spread tradition without altering the original product, while also providing overseas parents with a more affordable way for their children to attend internationally reputable schools.

5. India middle class fact of the day

India’s movie-loving, value-conscious customers have already humbled streaming godfather Netflix, which initially priced too high and had to shelve plans for India that included building a wholly owned post-production facility. It had to ratchet back ambitions to sign up 100mn subscribers — according to Media Partners Asia, they ended last year with fewer than 6mn.

If India did indeed have a middle class in the 250 million range, then the number of Netflix connections should have been several multiples of the lowly 6 million!

6. From the same article above, Amazon is trying to get its business model right in India.

Unlike other countries, where Amazon Prime subscribers mostly sign up to get faster deliveries, India’s Amazon Prime subscribers are primarily paying to watch movies and TV. “In developed markets, Prime service is sold primarily on the back of privileged delivery,” Shah said. “In India it’s the other way round, more people subscribe for video than for delivery benefits.” The big difference between Amazon and Netflix or Disney Plus Hotstar is that Amazon has many other things to sell you besides light comedies and cricket. If the company can convert watchers into customers in one of the world’s fastest growing ecommerce markets, then it will have hit the jackpot. “Amazon clearly sees video as a way to monetise India’s ecommerce opportunity,” Shah added.

I'm not sure that the video subscribers will buy much through Amazon.

7. A reflection of the fragmented nature of the natural gas market comes from the relative prices in Europe and US.

More than 40 million people left their jobs last year, many in retail and hospitality. It was called the Great Resignation, and then a rush of other names: the Great Renegotiation, the Great Reshuffle, the Great Rethink. But people weren’t leaving work altogether... What workers realized, though, is that they could find better ways to earn a living. Higher pay. Stable hours. Flexibility. They expected more from their employers, and appeared to be getting it... Many of last year’s job quitters are actually job swappers, according to data from the Bureau of Labor Statistics and the census, which shows a nearly one-to-one correlation between the rate of quitting and swapping. Those job switchers have tended to be in leisure, hospitality and retail. In leisure and hospitality, the rate of workers quitting rose to nearly 6 percent from 4 since the pandemic began; in retail it jumped to nearly 5 percent from 3.5. White collar employers still struggled to hire, but they saw far fewer resignations... When workers switched jobs, they often increased their pay. Wages grew nearly 10 percent in leisure and hospitality over the last year, and more than 7 percent in retail. Workers were also able to increase their shift hours, as rates of those working part-time involuntarily declined. A slim share of people left the work force entirely, though for the most part that was driven by older men retiring before age 65 — and some of them are now coming back to work.

10. US stock market ownership fact of the day,

According to an analysis by the New York University economics Professor Edward Wolff, the top 5 percent of American wealth holders own 72 percent of all stocks.

11. On the possibility of imported inflation from China for US consumers,

Goods made (in whole or in part) in China made up less than 2% of American personal consumer spending in 2017, according to economists at the Federal Reserve Bank of San Francisco. China’s covid-related bottlenecks could have larger ripple effects, say by allowing rival manufacturers to raise their prices. Most American inflation, however, is made in America.

12. India's cash transfer system fact of the day,

India has also found a workaround to redistribute more to ordinary folk who vote but rarely see immediate gains from economic reforms: a direct, real-time, digital welfare system that in 36 months has paid $200bn to about 950m people.

13. The Economist has a rare bullish story on India,

As the pandemic recedes, four pillars are clearly visible that will support growth in the next decade: the forging of a single national market; an expansion of industry owing to the renewable-energy shift and a move in supply chains away from China; continued pre-eminence in it; and a high-tech welfare safety-net for the hundreds of millions left behind by all this.

There is a dilemma lurking behind the industrial growth story - reconciling the need for large scale private investments and the threat of business concentration

Saurabh Mukherjea of Marcellus, an asset manager, calculates that India’s top 20 firms earn 50% of corporate India’s cashflows. They are making money fast enough to take risks with their earnings instead of having to borrow to excess. The ambitious giants include conglomerates—Adani (energy, transport), Reliance Industries (telecoms, chemicals, energy, retail), Tata (it, retail, energy, cars)—and more focused giants such as JSW (mainly steel). Those four firms alone plan to invest more than $250bn over the next five to eight years in infrastructure and emerging industries; in doing so they intend to develop local supply chains, which fits with government goals. Mukesh Ambani of Reliance says he will cut the price of green hydrogen to $1 per kilogram by 2030, for instance, from about $5 today. Tata is rolling out battery plants, electric vehicles and semiconductors. These are huge, risky bets that few other firms would dare take.

Finally, some figures on the national social safety net

In the year to March, payments reached $81bn, or 3% of GDP, up from 1% four years earlier. Payments have totalled $270bn since 2017. Roughly 950m people have benefited, at an average of $86 per person per year. That makes a difference to struggling households: India’s extreme poverty line is about $250 per person per year at market exchange rates. Mr Modi has not managed to initiate a national jobs boom, but he has created a national safety-net of sorts.

No comments:

Post a Comment