The Chinese economy appears cratering under the force of Xi Jinping's zero-covid policy. The hastening of the bad emperor problem comes even as the economy appears to be running into strong long-term headwinds.

It's very difficult to get first person perspectives on China. In that context, Ananth points to a revealing interview of Joerg Wuttke, President of US Chamber of Commerce in China. The intensity of the lockdown is shocking,

The current lockdown is even more extreme than in early 2020... Remember, 2021 was a banner year for China's economy, especially in the manufacturing sector. January started at a high level, February and March were still okay. But from March 28th, with Covid in Shanghai, everything collapsed... While 150,000 new cases per day is no longer a problem in Germany, 20,000 new cases in China are still considered 20,000 cases too many. For the past two years, the party leadership and government have spun the narrative that China has handled the pandemic much better than the decadent West. Now this narrative is blowing up in their faces. The population is genuinely afraid of the virus. Anyone who tests positive here is taken from home like a convict and forced into a camp with thousands of other people. Conditions there are sometimes deplorable, and it is often there that people fall really ill... The mayors, the regional politicians, they all have only one metric right now: Zero Covid.

Wuttke explains that Xi has boxed himself to a corner and will struggle to extricate himself before the Party Congress.

Until the 20th Party Congress, which will take place later this year, they will stick to the Zero Covid policy. President Xi wants to be confirmed for a third term, so he cannot change his narrative this close to the finish line. The president has maneuvered himself into two dead ends at once: He can’t change his Covid policy, and he can’t change anything about his friendship with Wladimir Putin... I can say, however, that people are genuinely afraid of the virus. The authorities do not inform that the Omicron variant is milder, they do not inform that other countries have learned to live with the virus. The authorities have spent a year bad-mouthing Western mRNA vaccines, with the result that people in China don’t trust the vaccination. That’s the problem: The political leadership can’t admit, so close to the Party Congress, that there is another way in dealing with Covid. They can’t admit that people in Europe can fly on vacation again and live largely a normal life. And they can’t admit that it would make sense to use mRNA vaccines in addition to the Chinese vaccines...I don’t see any vaccination campaign, no information campaign, no imports of mRNA vaccines, and I don’t see the population being told that society can live with it. So I have to assume that Zero Covid will result in locking down this city and then that city on a monthly basis, at least until the Party Congress.

There is an acute shortage of drivers, they all leave because they are tired of being tested over and over again. Now ships are clogging up the waters off Shanghai. Average waiting times for container ships there have tripled. Some are being diverted to Ningbo or Shenzhen, but those ports can’t replace the big port in Shanghai. In Europe, you haven’t even begun to see the effects of these problems. The ships coming into Europe today left Shanghai before the lockdown. Only in May and June will we see where the electronic equipment, the machine parts, the pharmaceutical precursors and components are missing. That will then lead to further shortages in the global supply chains. I am now hearing from more and more foreign companies that they are trying to move their supply chains to other countries. China is losing its credibility as the best sourcing location in the world.

For the first time, I see a number of companies looking to other Asian countries for their sourcing. That means their sourcing will be more expensive, because you can’t simply replace the extremely efficient Chinese cluster in many areas. But a more expensive sourcing is better than nothing. That’s also because China maintains an extremely rigid travel policy. As a CEO or as a purchasing manager, you can’t just fly quickly to Shanghai or to Guangzhou, but today you can easily get to Jakarta, Kuala Lumpur or Manila. With the current situation in China comes a huge loss of confidence, which will eventually lead to changes in supply chains. Foreign companies are not packing up and moving out of China, but they are considering moving parts of their investments to other countries. China has lost its nimbus as a base for sourcing and manufacturing, at least for the moment... But the leaders in Beijing don’t realize that Western companies are grappling with the scenario that they would have to leave China – just as they are now leaving Russia – if China tried to forcibly integrate Taiwan. And it doesn’t help, of course, that China is adopting Russia’s aggressive rhetoric. The effect is the same as from the Covid policy: Foreign companies are hitting the pause button. New investments are suspended for the moment.

His conclusion is sobering,

For now, China is not getting out of the corner the president has maneuvered the country into. They are prisoners of their own narrative. It’s rather tragic: China was the first to get into the pandemic, and it’s the last to get out. And in the meantime, they’ve been telling the whole world that they’re the best.

Gideon Rachman talks about how Xi Jinping's Covid and, to a lesser extent, Russia policies and premature triumphalism on both have eroded the party and the government's "performance legitimacy". As another FT report highlights, this has strong echoes with Mao, and is the classic Bad Emperor problem,

Weijian Shan, a veteran China investor, said in a recent recorded video meeting that the country was embroiled in a “man-made” crisis. “Large parts of [the] Chinese economy including Shanghai have been semi paralysed and the impact on the economy is going to be very profound,” Shan said. “[China’s leaders] think they know better than the market and many of [their] actions have done real damage to the market and to the economy.” One government policy adviser, who asked not to be identified, said making Xi understand that his previously successful zero-Covid policy might not withstand the highly contagious Omicron variant without devastating economic costs was now a “key challenge for the system”. “People are telling Xi the lockdowns are a concern but I don’t think they’re saying how big a concern it really is,” the adviser said. “He’s just so proud of China’s accomplishments fighting Covid that I don’t think he worries about the economy.”

Meanwhile, there are signs that the economy may be running out of steam. Daniel Rosen feels that the prospects for China in 2022 look bleak and feels that it'll be difficult to get even a 2% GDP growth rate,

At the annual meeting of the National People’s Congress in March, China’s leaders declared that 2022 GDP growth would be 5.5 percent, a normalization back to 2019, prior to the COVID-19 pandemic, when growth was 5.9 percent... Where could such an expansion come from? There are three possible sources: business investment, household and government consumption, and trade surpluses. The size of China’s economy was $17.7 trillion in 2021, according to official figures, so 5.5 percent growth would mean about $1 trillion more in 2022. Using growth in 2019 as a basis for comparison, business investment in China would need to contribute about 1.5 percentage points toward the 5.5 percent growth Beijing promises this year. Because net exports are likely to be negative and consumption is likely to decrease, investment would need to contribute even more—around 2.5 percent—to growth this year. But nearly half of all growth in business investment in recent years has been related to the property sector... There is no logical way investment can add 1.5 points to GDP growth in 2022, let alone 2.5 percent... Household and government consumption combined would need to add about 3.5 percentage points in 2022 toward the 5.5 percent growth target. But with almost 100 million consumers in lockdown from COVID-19 outbreaks, retail activity is frozen.

On a longer-term perspective, the staple of investment driven growth appears to have reached its limits, hastened by the distress-stricken property developers and indebted local governments.

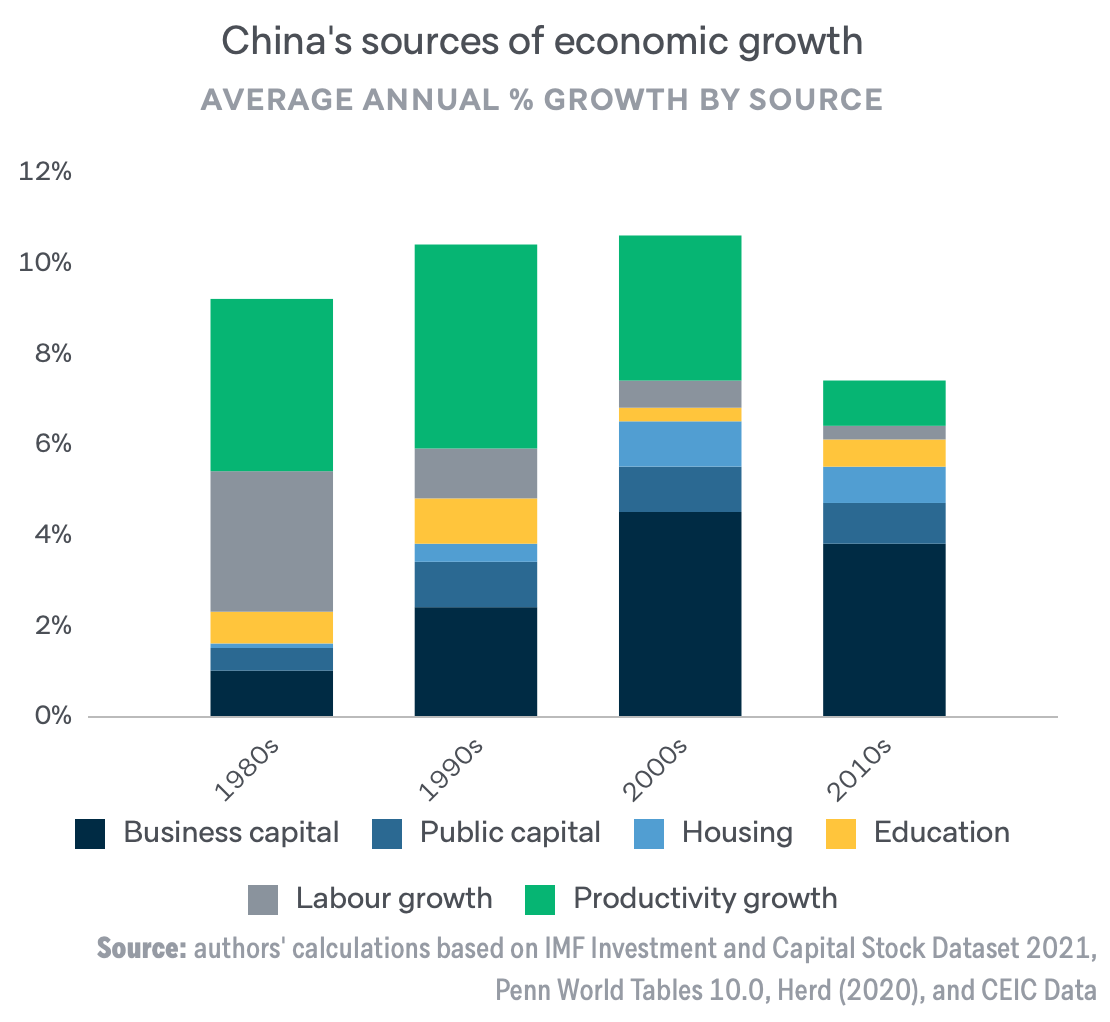

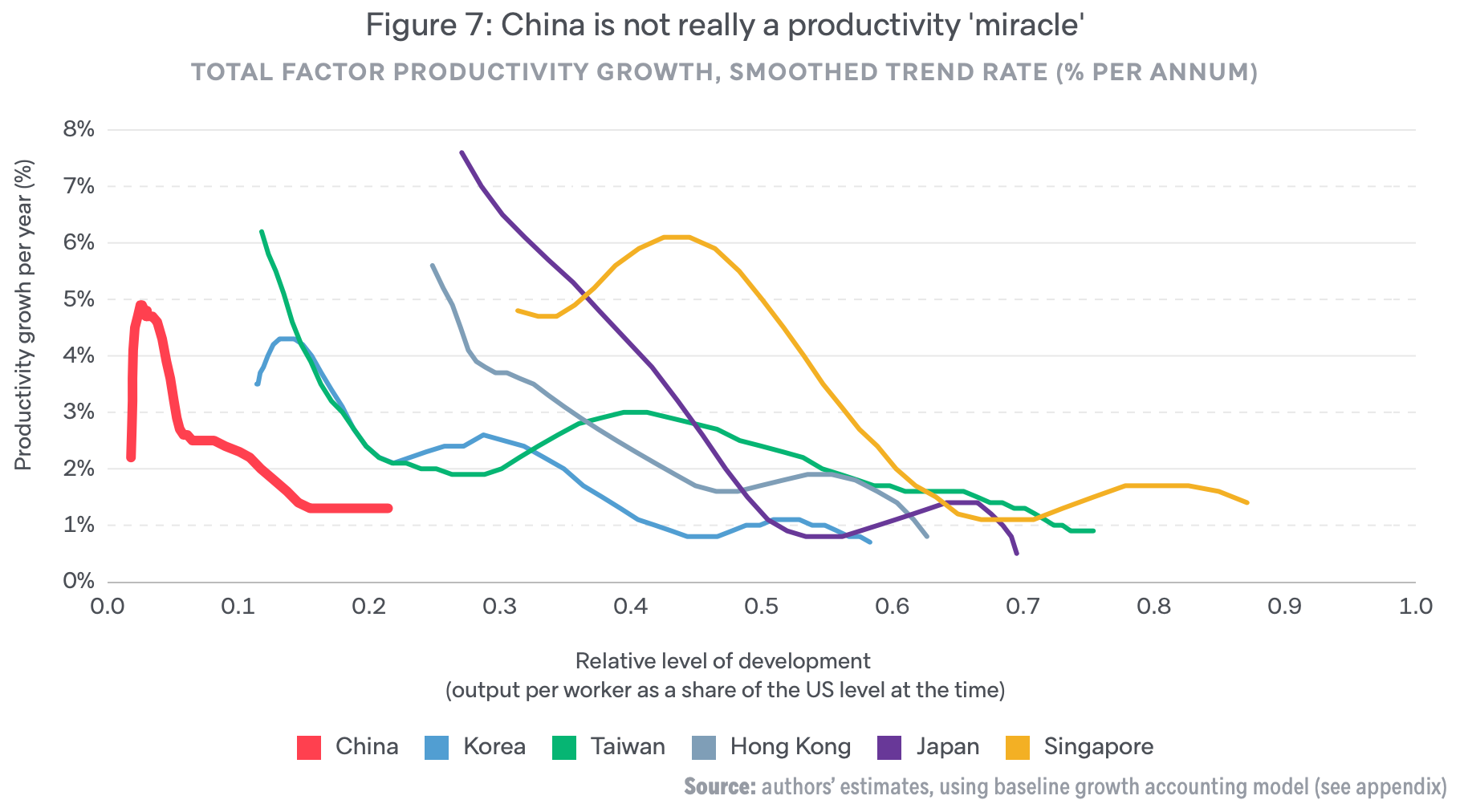

Adam Tooze points to a new Lowy Institute report that revises China's long-term growth prospects. An important point that jumps out is how little productivity growth has contributed to the country's remarkable growth. It's remarkable how little productivity growth has contributed to China's growth in the last decade. This is inputs big time.

By 2050... China would still be much poorer and less productive than the United States, based on current expectations of future US growth at around 1.6% a year on average. By 2050, the average person in China would be 40% as rich as the average person in the United States, while the average worker in China would only be about half as productive (in PPP terms)... Measured on a PPP basis, China’s share of global output would rise modestly over the next decade in our baseline projection before declining to remain essentially unchanged by mid-century compared to today... China’s share of global output measured in nominal US dollars would only rise modestly, from 17% today to a little over a fifth over the coming decades... our projections of slower growth imply that China’s global rise would be considerably muted... China would overtake the United States to become the world’s largest economy in nominal US dollar terms by about 2030, but it would never establish a substantial lead. In our baseline scenario, China’s economy would peak at about 15% larger than America’s.

No comments:

Post a Comment