1. The pandemic has been associated with massive liquidity infusion by the central bank. However, the majority of the liquidity has found its way back to government securities,

According to RBI data, banks invested Rs 7.2 trillion in government bonds as compared to Rs 5.8 trillion extended as loans in 2020-21... The RBI went for government borrowing of a record Rs 12 trillion in the previous financial year. At the same time, credit demand remained anemic and grew by 5.6 per cent in FY21... FY21 ended with a total credit expansion of Rs 5.8 trillion by scheduled commercial banks, a shade lower than the Rs 6 trillion in the previous year. Banks’ investment of Rs 7.2 trillion in government securities, was nearly twice their investment in the previous year. “Banks’ investment in 2020-21 outpaced overall credit extended – a phenomenon not seen in nearly twenty years, barring the year of demonetisation,” the RBI observed in the state of the economy report in April... The RBI report said the ‘feeble’ credit growth of 5.6 per cent pointed to continuing risk aversion amidst pandemic-linked impairment to their balance sheets.

2. Business Standard reports that Blackstone has paid Rs 5250 Cr to buyout Embassy Industrial Parks from Embassy Group and Warburg Pincus.

Embassy Industrial Parks comprises 22 million square feet of modern logistics and warehousing facilities, as well as yet-to-be-built assets, located across Bengaluru, Delhi-NCR, Hyderabad, and Pune. These are leased to leading e-commerce and retail players... For Blackstone, warehousing seems to be a new focus area, after it entered office properties in 2011 and then malls. Blackstone floated two REITs (real estate investment trusts) with its partners Embassy and K Raheja Corporation and listed them. It is the largest owner of offices in the country. With the latest deal, Blackstone will have a portfolio of over 40 million sqft of developed and yet-to-be-developed assets with its partners Hiranandani and Allcargo. This is similar to what another logistics developer Indospace has... Since 2010, Blackstone has acquired more than 1.2 billion sqft of logistics globally.

According to Colliers International, the sector has attracted interest from multiple large institutional investors, with investment inflows of Rs 27,800 crore ($3.7 billion) since 2017. Between 2017 and the first half of 2020, the sector garnered a 17 per cent share of the total PE investment in the country.

3. The Serum Institute of India (SII) is a large contract manufacturer of vaccines and should not be compared with drugs manufacturers. As an illustration, in the 2010-11 to 2019-20 period, it made just Rs 17,176 Cr in profits, with margin of 44%, mainly by exports at higher margins, and invested just Rs 900 Cr in R&D. It's licensed to manufacture over 20 vaccines in India. It's therefore no wonder that unlike the likes of Moderna, or even Bharat Biotech, SII remains a contract manufacturer and has done little to move up the value chain despite its long history.

4. This is a list of 56 mails, SMSes, and WhatsApp messages sent by David Cameron to various Ministers and officials to lobby for government support to Greensill Capital, where he held a large share, once worth tens of millions. In a delicious irony FT had this to write,

In 2010, when David Cameron was UK prime minister, he made a speech criticising lobbyists. “We all know how it works. The lunches, the hospitality, the quiet word in your ear, the ex-ministers and ex-advisers for hire, helping big business find the right way to get its way.” Eleven years later Cameron’s own relentless lobbying has been exposed in a treasure trove of private messages sent to senior members of the Tory government.

5. Fascinating profile in the NYT of Bayern Munich's Polish striker Robert Lewandowski, widely acknowledged as the best goal scorer in club soccer today. He's two goals away from breaking Gerd Mueller's longstanding Bundesliga record of 40 goals in a season.

6. Even as the Israel-Palestine conflict erupts, The Economist points to changing trends in the actions of Saudi Arabia's Mohammed Bin Salman,

So far this year he has held two rounds of talks with Iran in Baghdad, the Iraqi capital, and spoken of his hope for “a good and special relationship”. His officials have met his Yemeni foes, the Iranian-backed Houthi rebels, in the Omani capital, Muscat. The Saudis offered to lift the kingdom’s siege of Yemen and to help rebuild the country his jets have bombed. He has also stopped funding the rebellion against Syria’s ruler, Bashar al-Assad; earlier this month he sent his intelligence chief to Damascus to discuss restoring ties. Prince Muhammad is mending fences with Turkey and Qatar as well. Both had irritated him by backing Islamist groups that he dislikes, such as Egypt’s Muslim Brotherhood. But the prince has lifted a three-year blockade of Qatar and bought arms from Turkey. On May 10th he hosted Turkey’s foreign minister, Mevlut Cavusoglu, and Qatar’s emir, Tamim bin Hamad al-Thani.

The change of guard in US, with Biden even calling Saudi Arabia a "pariah" during the election campaign, and setbacks in Yemen and attacks on Saudi oil installations, may be the triggering factors for these reversals.

7. The Economist examines the issues in the rising momentum on harmonising corporate tax rates globally.

The foundations of the global corporate-tax system were laid a century ago. It recognises that overlapping taxes on the same slice of profits can curb trade and growth. As a result, taxing rights are allocated first to wherever profits are produced (the “source”) and then to wherever the parent company is headquartered (or “resident”). A multinational based in America but with an affiliate in Ireland, for example, typically pays taxes in both places. Where the company makes its sales is irrelevant. Payments between an individual firm’s various legal affiliates are recorded using the “arm’s-length” principle, supposedly on terms equivalent to those found on the open market.These principles, now baked into thousands of bilateral tax treaties, have had two unintended consequences. First, they have encouraged governments to compete for investment and revenue by offering tantalisingly low tax rates. In 1985 the global average statutory corporation-tax rate was 49%; in 2018 it was 24%... There is a huge mismatch between where tax is paid and where real activity takes place. Analysis by the OECD suggests that multinationals report 25% of their profits in investment hubs, although only 11% of their tangible assets and less than 5% of their workers are based there. Parents can allocate paper profits to affiliates in tax havens by having them hold intellectual property that is then licensed to other affiliates in high-tax places.

The two solutions that the Biden administration has put forth to address the problem,

The first would reallocate taxing rights so that a slice of profits could be levied according to, say, the location of a company’s sales. That right could be incurred even if the company had no physical presence in the country. Mr Biden’s negotiators have proposed a reallocation that would apply to the 100 biggest and most profitable companies worldwide; in return, the Biden administration wants all the digital-services taxes to be dropped. The second element would apply a minimum rate of corporation tax, putting a floor on the race to the bottom. The Biden administration is gunning for a global minimum tax rate on foreign earnings of 21%, applied to profits within each jurisdiction separately.

8. As the Covid 19 rages on in India, an issue that has assumed prominence is of temporary waiver by the WTO of TRIPS that would allow others to manufacture patented vaccines. While India and South Africa have been leading efforts in this regard, it got a big boost with the recent decision by the US to back temporary patent waiver.

However, several people are sceptical of rapidly increased production even with patent waivers. They point to challenges in setting up manufacturing facilities, technology transfer, limited supplies of critical inputs like lipid nanoparticles and equipment like bioreactor bags, and easing of various types of export restrictions on inputs.

Tread the middle path points me to this article by Monica de Bolle and Maurice Obstfeld who point to the legal challenges,

Since August 2003, the WTO has explicitly allowed emergency departures from the TRIPS agreement, enabling countries with manufacturing capacity to suspend IP protections to produce life-saving drugs and vaccines, not just for domestic use but also for export to countries that lack manufacturing capacity of their own. However, the process of negotiating the August 2003 decision—which created a temporary procedure for export waivers—took 14 months, and it was not until January 2017 that two-thirds of WTO members had ratified it as a formal amendment to the TRIPS agreement. Because of this painful negotiation process, the bureaucratic procedures for exercising IP flexibility are so cumbersome that there are very few instances of its use.

Then there is the technical challenge,

True, patent protection is the main obstacle to creation of generic small-molecule drugs, which chemists can synthesize. But other major obstacles exist for vaccines, which are biologics. For the latter category of drugs, an identical product requires an identical production technology, with most steps categorized as hard-to-replicate trade secrets rather than patentable innovations. Thus, Moderna announced in October 2020 that it would not enforce its COVID-19-related patents during the pandemic. But this step, however laudable, is of limited immediate help to would-be producers of a "generic" version of the Moderna vaccine. Without precisely replicating all steps of Moderna's production process, including the many quality controls, a generic version would have untested immunogenicity (the ability to induce the body to generate an immune response) and thus would require extensive clinical trials before release... The replication hurdle is especially high for the new and more sophisticated messenger ribonucleic acid (mRNA) vaccines, which have proven most effective against SARS-CoV-2 (the virus that causes COVID-19) and which are likely to provide the most adaptable platforms for the vaccines of the future. The genetic vaccines produced by Pfizer-BioNTech and Moderna require considerable technical knowledge and sophisticated techniques to generate a version of the viral spike protein that elicits a strong immune response.

Interestingly, even as India is fighting for patent waiver at the WTO, it submitted an affidavit in the Supreme Court opposing patent waiver as being counterproductive. It remains to be seen how it would affect its WTO case.

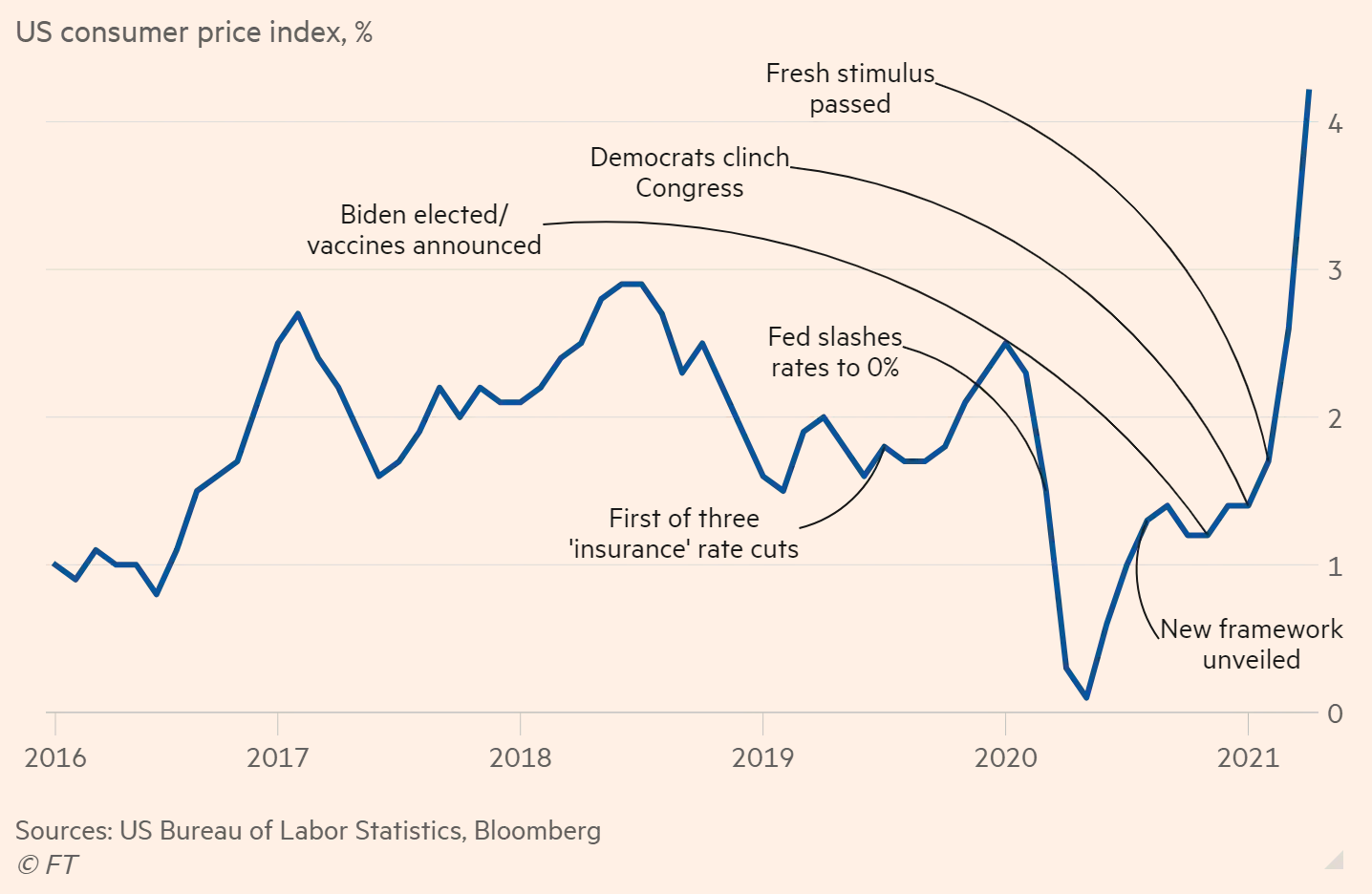

9. The latest in one of the most important watched indicators in the global economy and financial markets, US headline inflation. Last week the US CPI flashed 4.2% annual increase. But Fed played down the increase, describing it as transitory.

After countless false alarms over the last four decades, will this time be different?

No comments:

Post a Comment