Whether it revives US manufacturing or not, these developments are certain to impact the global energy geo-politics.

The most dramatic period of improvement in human health in history is often taken to be that of late-19th-century Japan, during the remarkable modernisation of the Meiji transition. Bangladesh’s record on child and maternal mortality has been comparable in scale.This is a very impressive achievement, especially given that Bangladesh with a population of more than 150 million is no small country. The fact that it was achieved without proportionate improvements in income levels and alongside extreme poverty runs contrary to much of mainstream thinking that social development follows economic growth.

The real magic of Bangladesh, though, was not microfinance but BRAC — and NGOs more generally. The government of Bangladesh has been unusually friendly to NGOs... BRAC is now the largest NGO in the world by the number of employees and the number of people it has helped (three-quarters of all Bangladeshis have benefited in one way or another)... BRAC does practically everything. In the 1980s it sent out volunteers to every household in the country showing mothers how to mix salt, sugar and water in the right proportions to rehydrate a child suffering from diarrhoea. This probably did more to lower child mortality in the country than anything else. BRAC and the government jointly ran a huge programme to inoculate every Bangladeshi against tuberculosis. BRAC’s primary schools are a safety net for children who drop out of state schools. BRAC even has the world’s largest legal-aid programme: there are more BRAC legal centres than police stations in Bangladesh...

BRAC is a sort of chaebol (South Korean conglomerate) for social development. It began with microcredit, but found its poor clients could not sell the milk and eggs produced by the animals they had bought. So BRAC got into food processing. When it found the most destitute were too poor for micro-loans, it set up a programme which gave them animals. Now it runs dairies, a packaging business, a hybrid-seed producer, textile plants and its own shops—as well as schools for dropouts, clinics and sanitation plants.Though the role and contribution of BRAC and other NGOs was huge, it is undeniable that such progress could not have been made without active role of the government. India, more than anyone else, has the most to learn from Bangladesh. Why has East Bengal, which is much more poorer and with a much more dysfunctional administrative system, managed to achieve so much more than West Bengal? What explains the massive differential in achievements, despite similar baseline figures, on both sides of the Indo-Bangladesh border?

The annual wage growth rate for men working in agriculture being 3.1% in the most recent period (2004-09) compared with just 1.8% in the previous period (1999-2004). The difference is even starker for women at 5% annual growth for 2004-2009 and a meagre 1.2% for 1999-2004... But these figures cannot be analysed in isolation. They must be looked at under the light of changing agricultural conditions across the two periods... the increase in foodgrain yield in 2004-2009 of 2.5% per year, while it was at a record low level of 0.1% per year during 1999-2004... The net increase in men’s agricultural wages (subtracting the foodgrain yield growth rate from real agricultural wage growth rate) stands at 1.7% for the period of 1999-2004 and 0.6% for 2004-2009. Thus, 2004-2009 effectually experienced a lower rate of increase in agricultural wages once the growth rate in yield is netted out... at the all India level, growth in net female agricultural wages is a modest 2.4% in 2004-2009 in comparison with the 1.1% in the 1999-2004.

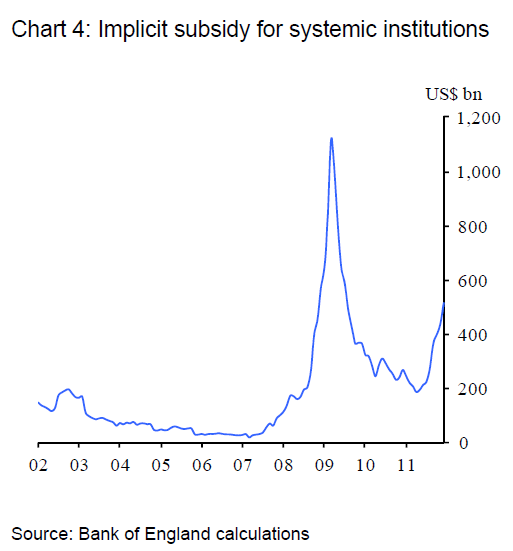

But this finding is based on estimates of banks’ funding costs which take no account of the implicit subsidy associated with too-big-to-fail. Removing this subsidy raises banks’ funding costs, lowers estimates of bank value-added and thereby reduces measured economies of scale. Once an allowance is made for the implicit subsidy, the picture changes dramatically. There is no longer evidence of economies of scale at bank sizes above $100 billion. If anything, there is now evidence of diseconomies which rise with bank size, consistent with big banks becoming “too big to manage”.