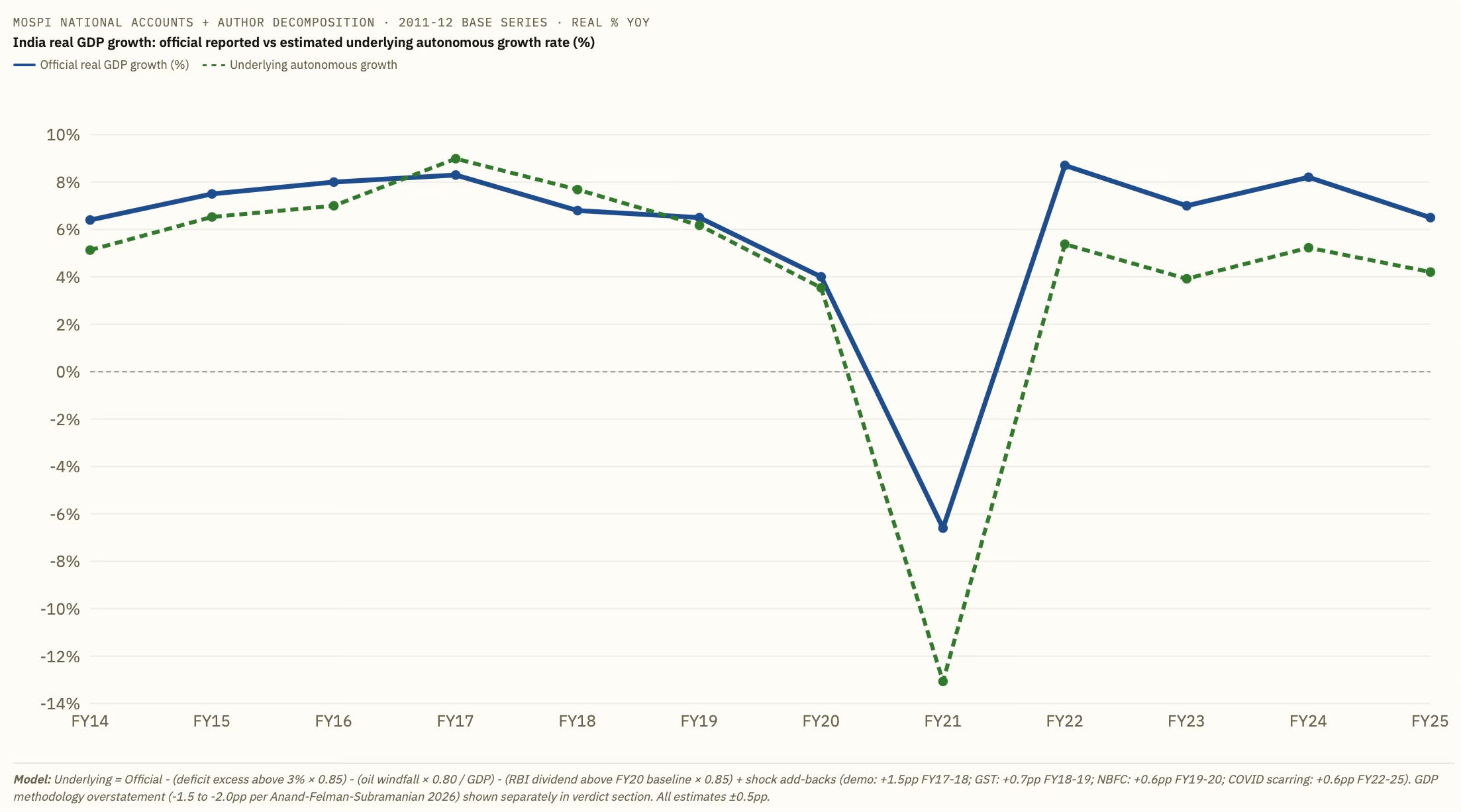

The sustainable growth rate of any economy is that which strips out the positive effects of the government’s fiscal interventions and the negative effects of economic shocks. This blog has held that, given its deficient human, physical, and financial capital, India’s neutral growth rate is about 5-5.5%.

This post provides a framework to figure out the underlying economic growth rate by stripping these positive and negative contributors.

So, what has been India’s underlying neutral (stripped of the impact of policy interventions) economic growth rate?

Answering this requires us to identify the specific interventions and events that have contributed to the positive and negative shocks, and to try to figure out their respective economic impacts.

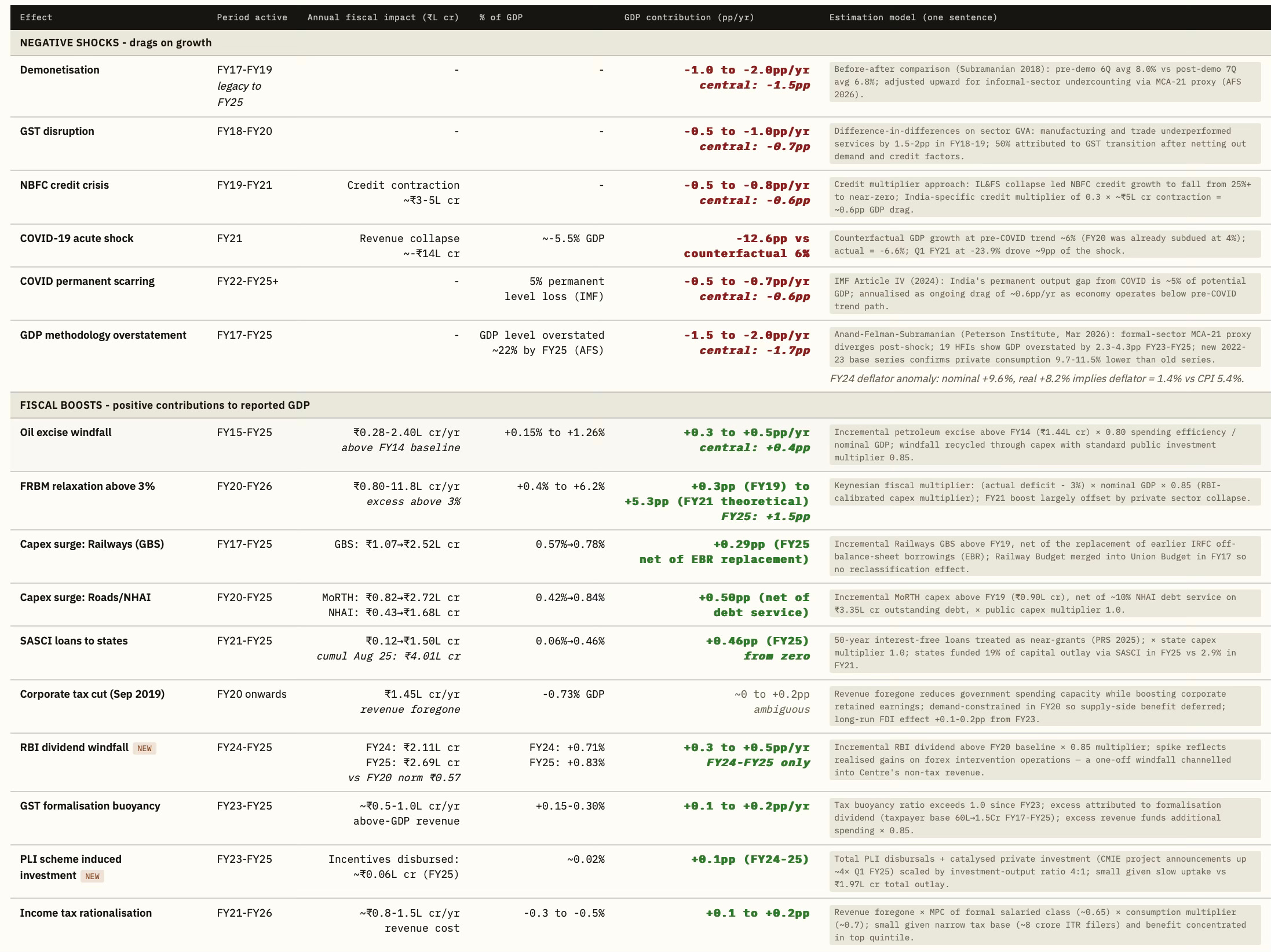

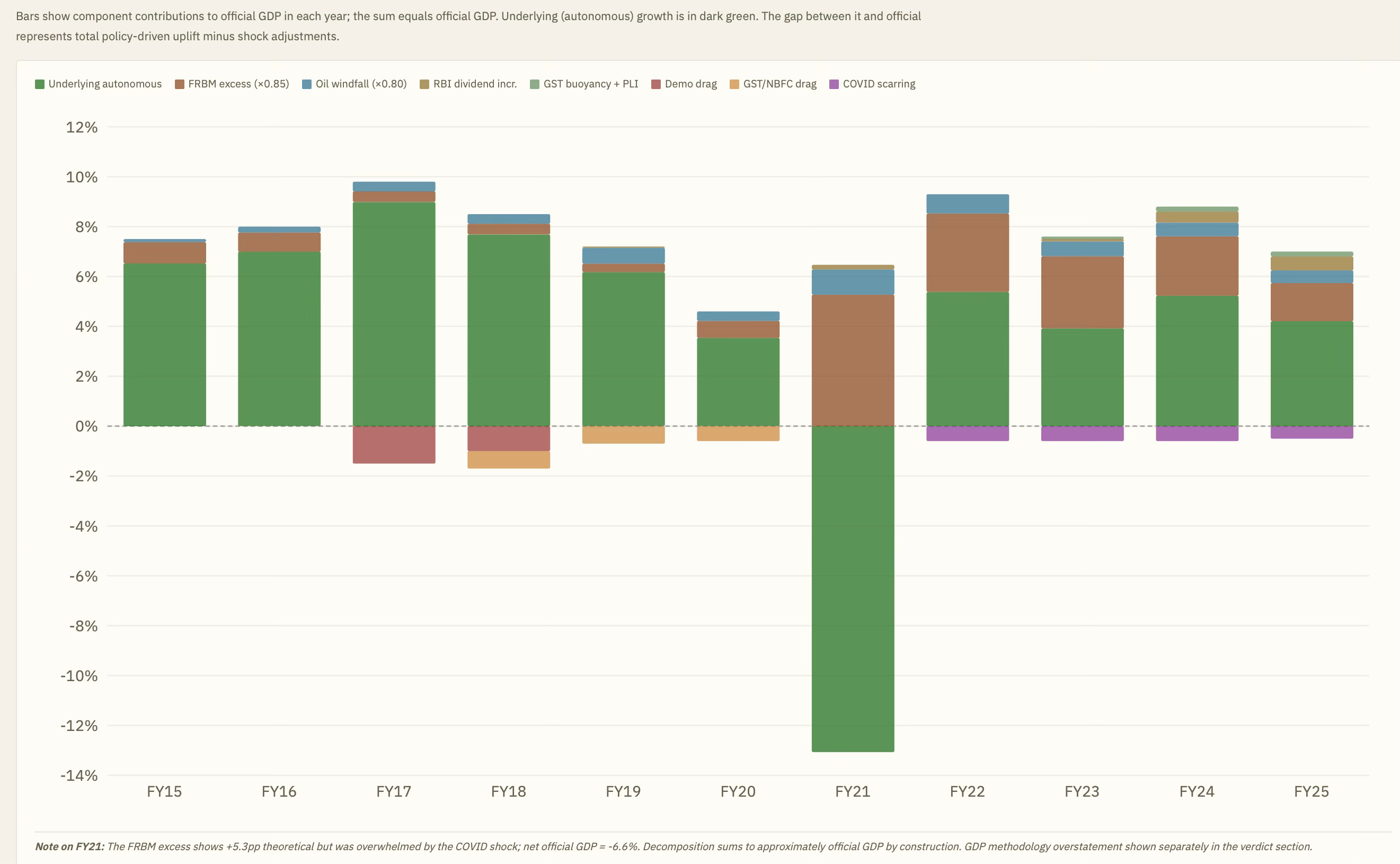

In the last decade or so, the economy has faced three large negative shocks: demonetisation, the introduction of GST and associated efforts to formalise the economy, and the pandemic. In addition, on the external front, it has faced the oil shocks from the Ukraine and Iran wars, and the Trump tariffs.

The economy as a whole has benefited from three fiscal events - corporate tax rate reduction, income tax rate reduction and rationalisation, and the GST rate reduction.

While it is now clear that the government suffered revenue loss from the corporate tax rate reduction, the income tax rate reduction, and rationalisation appear to have boosted the tax base and increased revenues. It appears (at least for now) that the existing corporate tax rate was on the left side of the Laffer curve, whereas the direct tax rate was on the right side.

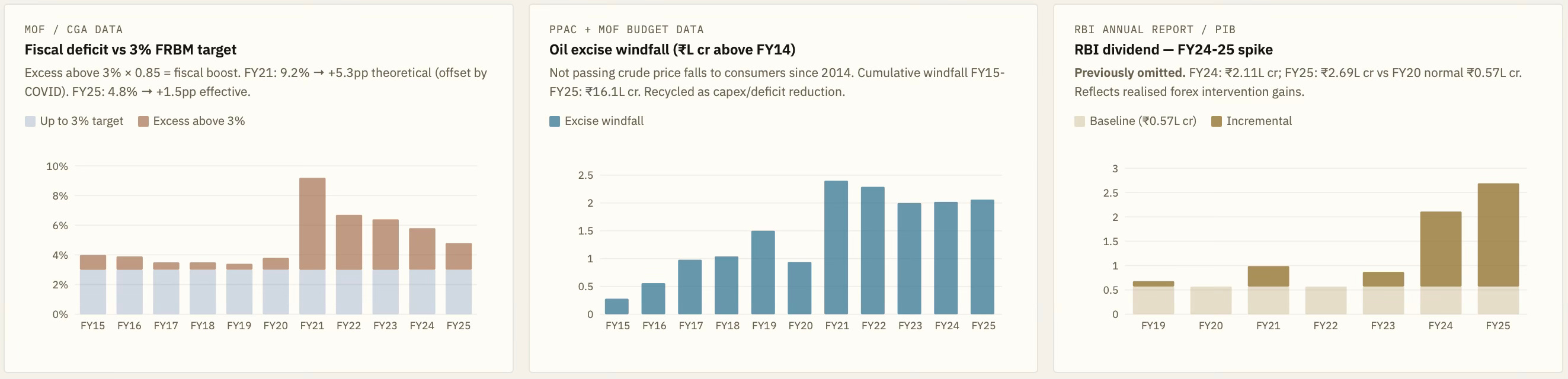

The government clearly benefited from three positive fiscal events: the long period of low oil prices (increased excise tax revenues due to not passing through the reduced oil prices), the surge in RBI dividends, and the large additional fiscal space from discarding the FRBM framework.

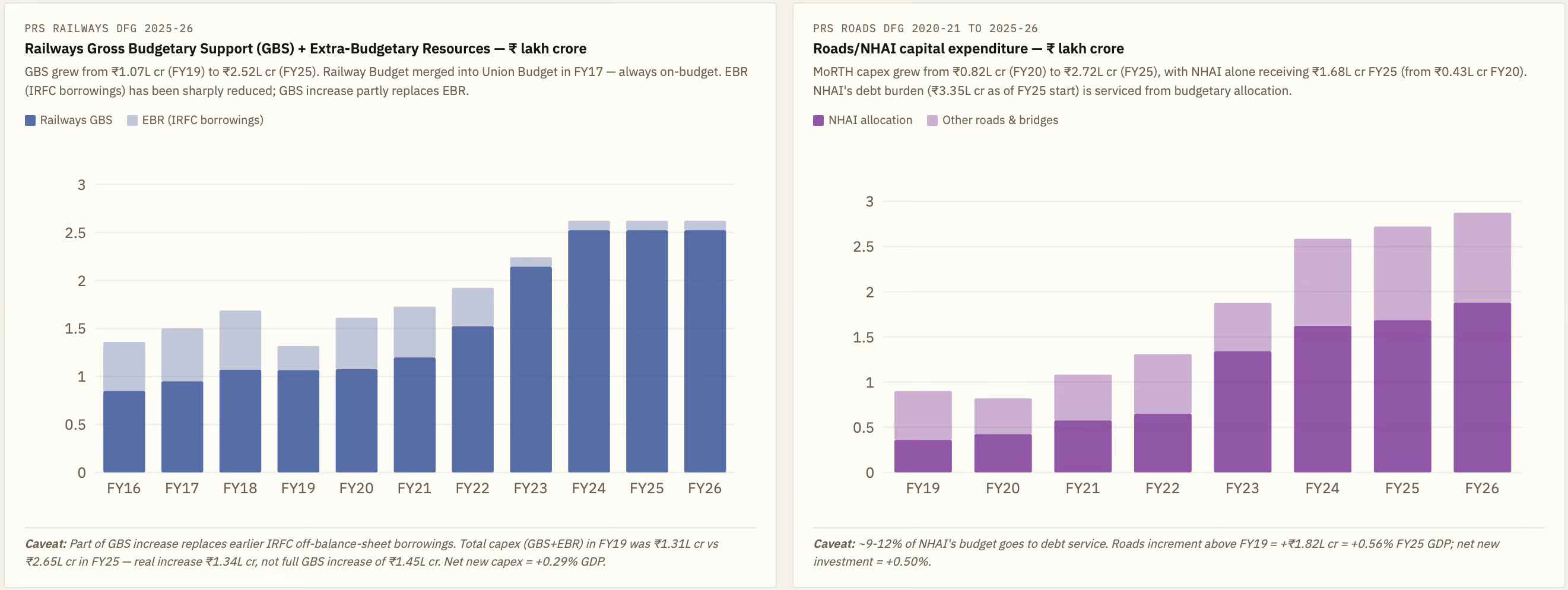

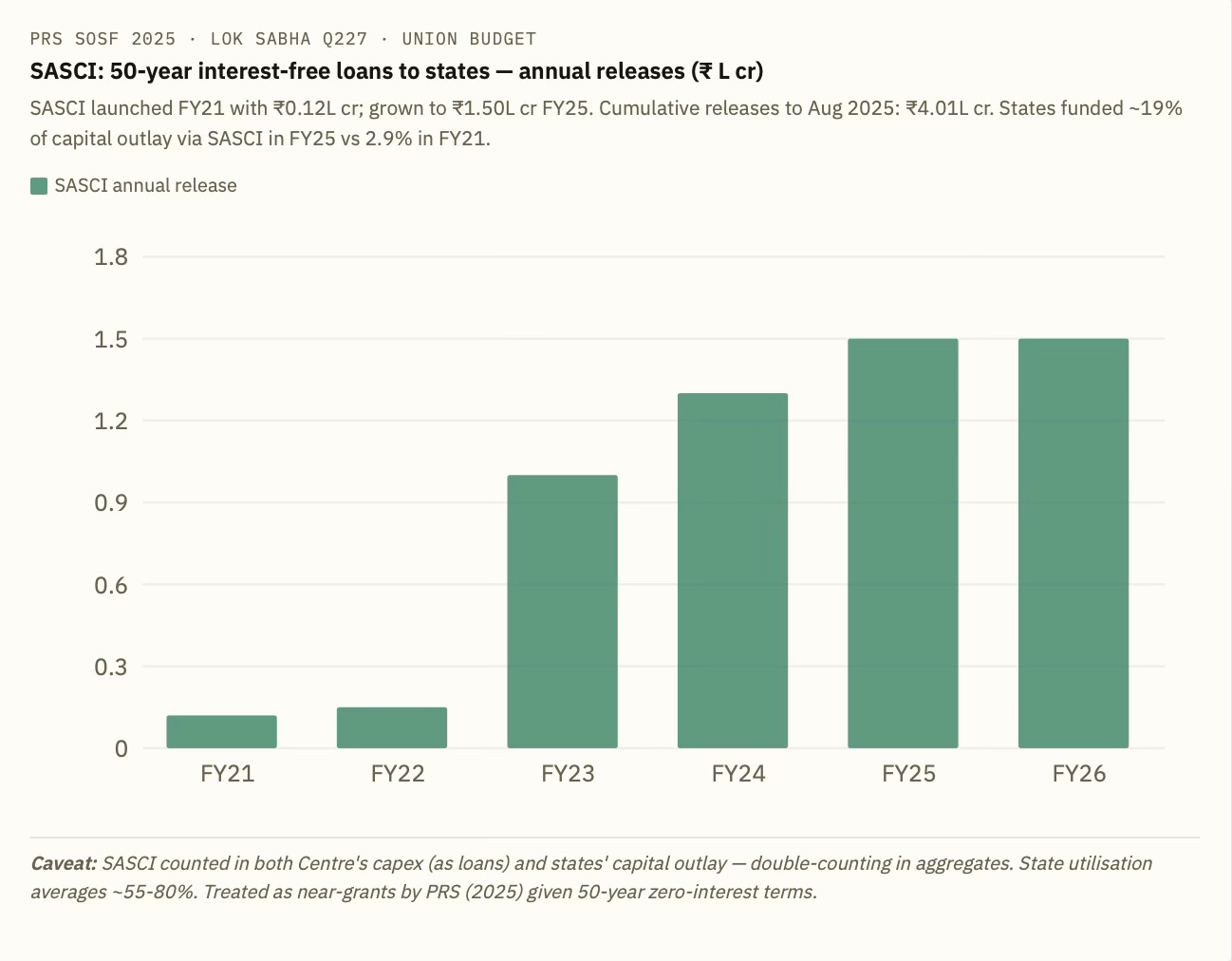

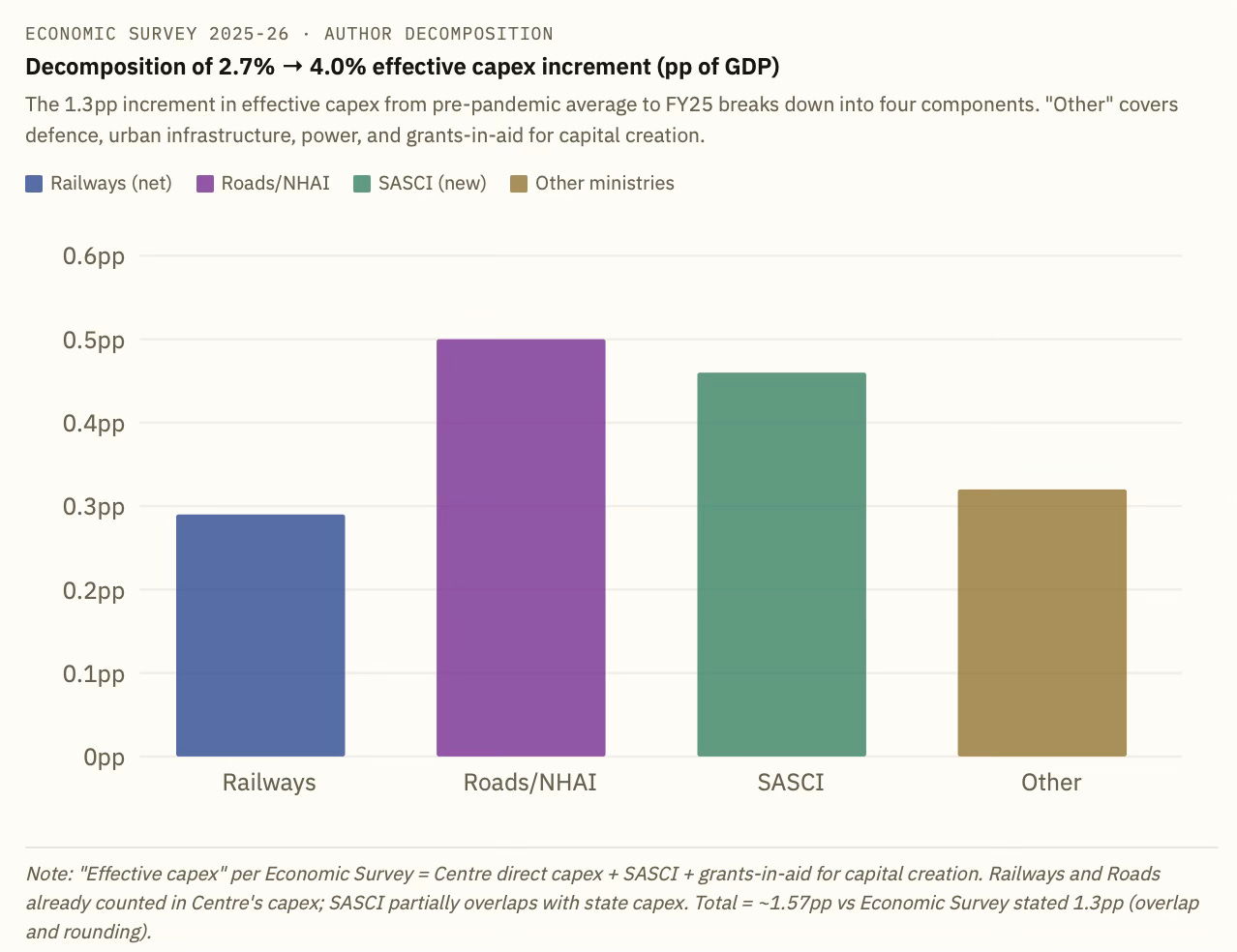

The net boost to fiscal balance resulted in a sharp spike in capital expenditure. It is to the credit of the government that it eschewed the subsidies and revenue expenditure route. This increase in capex includes taking on the budget account capital expenditures of NHAI and Railways. In addition, there has been the introduction of the zero-interest 50-year loan to state governments under the Special Assistance to States for Capital Investments (SASCI).

What have been their respective contributions to the output growth? Here is a graphical summary.

This table captures a brief description of the assumptions and estimations used.

On the positive boosts to the government’s fiscal position, the contributions of the three factors are shown below.

On the capital expenditure side, the government assumed in the budget the expenditures on railways and highways.

The fifty-year interest-free loan to states under SASCI was a new addition, amounting to about Rs 1.5 lakh Cr each year.

This explains how the increase in capex could be disaggregated and distributed among the different parts discussed above.

The disaggregated impact of the positive and negative factors on the economic output is shown below.

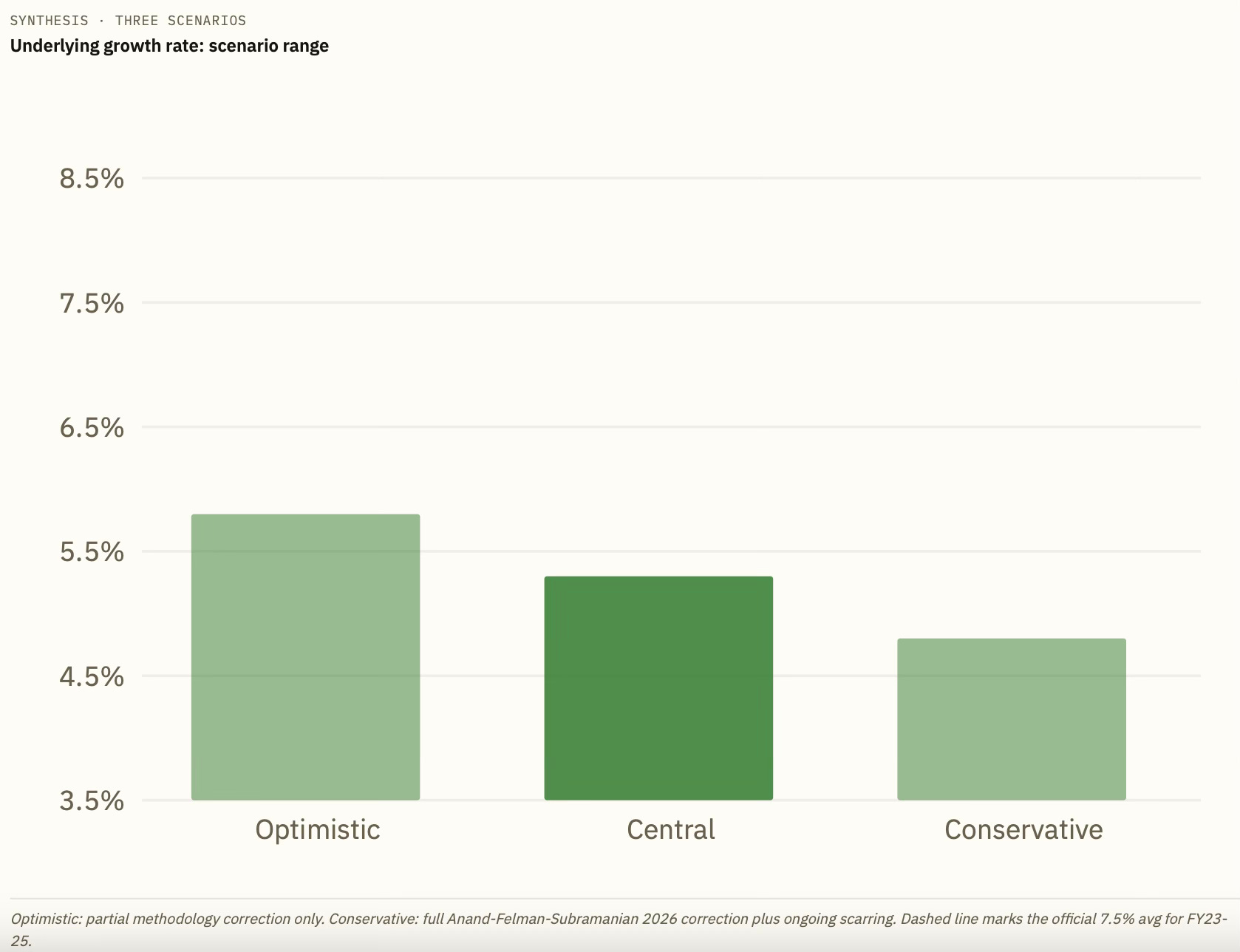

Based on the above, the underlying neutral economic growth appears to be in the range of 5-5.5%.

Clearly, since the pandemic, policy interventions have played an important role in boosting the economic output.

The important point here is that while policy interventions may have boosted economic growth for some time, it remains to be seen in the coming years whether they have shifted the economy onto a higher underlying steady state growth trajectory. This is especially important since the headroom for further interventions, like fiscal space for more capex or tax cuts, may have shrunk, and we may be entering a world of increasing uncertainties and headwinds for the foreseeable future.

In the final analysis, the balance sheet of the policy interventions will boil down to this question. Did the fiscal transfers of the last few years create the conditions (by broadbasing economic growth or increasing capital accumulation, for example) for a shift to a higher trajectory of growth, or was it a case of merely providing a temporary boost to the national output?

No comments:

Post a Comment