It has become a canon of economic orthodoxy that lowering corporate taxes will spur investment, and lowering income and indirect tax rates will spur consumption and economic activity, and both will boost tax revenues.

India’s experience with several direct and indirect tax reforms over the last decade may be a test case to evaluate this orthodoxy. This post analyses the impact of these reforms on tax revenues and the economy, especially of corporate taxes.

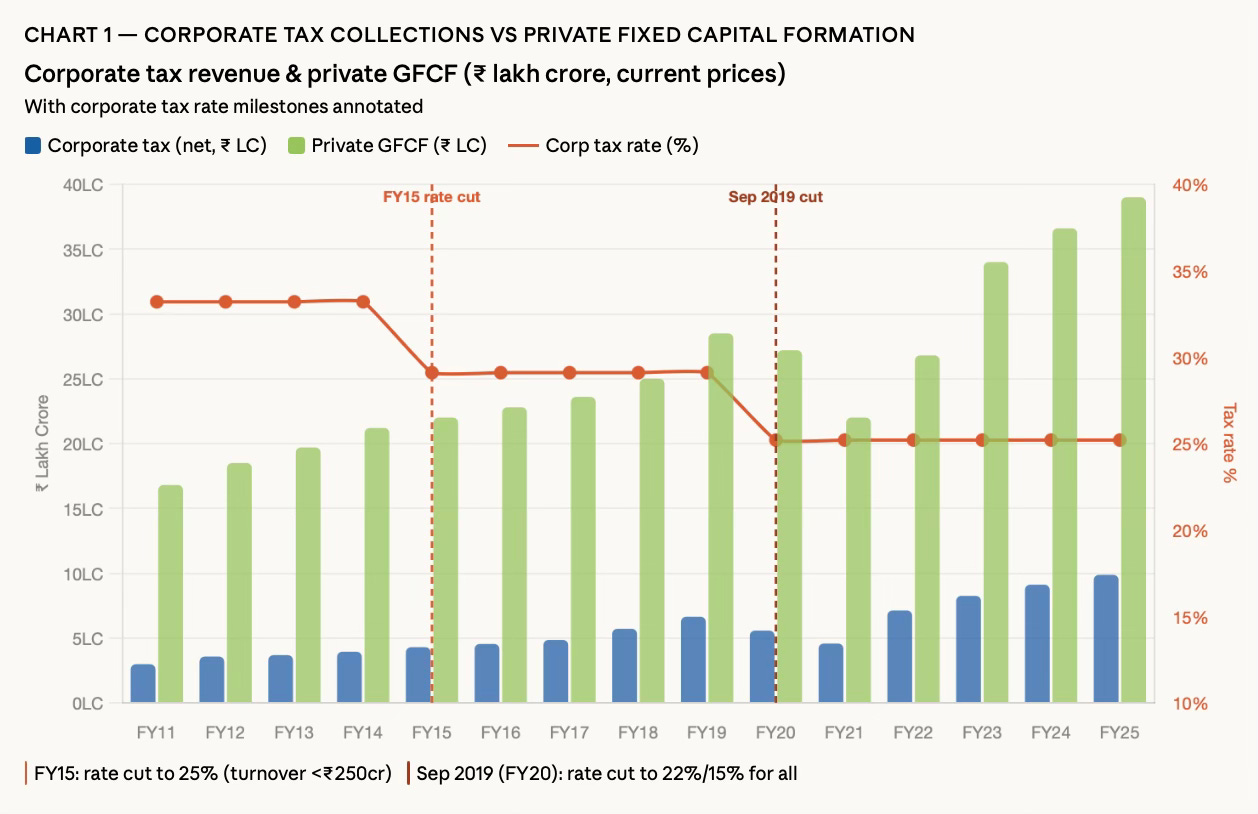

On 20 September 2019, the government slashed the base corporate tax rate from 34.94% to 25.17% (inclusive of surcharge and cess) for existing domestic companies, and to 17.16% for new manufacturing companies — representing a fiscal cost of roughly ₹1.45 lakh crore or 0.7% of GDP.

AK Bhattacharya has this description of the corporate tax rate reductions.

In 2016-17, new manufacturing companies incorporated on or after March 2016 were given the option to be taxed at 25 per cent plus surcharge and cess (compared to 30 per cent plus surcharge, etc.) if they did not claim profit-linked or investment-linked deductions, investment allowances, or accelerated depreciation. Additionally, the tax rate for all companies with an annual turnover of less than Rs 5 crore was brought down to 29 per cent plus surcharge and cess. In 2017-18, the tax rate for small and medium companies with an annual turnover of up to Rs 50 crore was brought down to 25 per cent. This meant about 96 per cent of companies that filed a tax return were brought under a concessional tax rate of 25 per cent plus surcharge and cess... In the following year, 2018-19, the government extended the coverage of the 25 per cent tax rate to cover all companies with an annual turnover of up to Rs 250 crore — a move that would benefit 99 per cent of companies filing tax returns... In 2019-20, the government extended the concessional tax rate of 25 per cent to all companies with an annual turnover up to Rs 400 crore, thereby covering 99.3 per cent of all companies filing tax returns. Subsequently, in September 2019, all companies not availing themselves of the various exemptions and incentives like tax holidays were allowed to be taxed at 25 per cent, inclusive of the 10 per cent surcharge and a 4 per cent cess. Moreover, manufacturing companies starting operations after October 1, 2019, were to be taxed at an overall rate of 17 per cent.

And this on its outcomes in terms of revenue impact.

Corporation tax collections used to be about 34 per cent of the Centre’s gross tax revenues in 2014-15. This share plummeted to 28 per cent in 2019-20 and further down to 23 per cent in 2020-21... the share of corporation tax in GDP has kept falling almost every year in this period — from 3.4 per cent of GDP in 2014-15 to 2.74 per cent in 2019-20 and 2.28 per cent in 2020-21... In 2014-15, about 188,000 companies in a sample size of close to 580,000 paid taxes at an effective rate of over 30 per cent and this cohort accounted for 60 per cent of the total corporation tax collected by the Centre that year. In 2018-19, thanks to the various tax concessions, only about 85,000 companies of a larger sample size of 885,000 paid taxes at the rate of over 30 per cent. And this cohort accounted for only 50 per cent of the corporation tax revenue of the Centre... In contrast, there were just about 24,000 companies in 2014-15 paying taxes at an effective rate of 25-30 per cent, accounting for only 16 per cent of the corporation tax collected by the government. Another 15,000 companies paid taxes at the rate of 20-25 per cent, but their contribution to the corporation tax revenue was only 10 per cent. By 2018-19, the number of such companies saw a huge increase, without, however, a corresponding increase in their share in total taxes collected. Companies paying taxes at 25-30 per cent numbered around 184,000 in 2018-19, but their share in corporation tax was 19 per cent. The number of companies paying tax at 20-25 per cent increased to over 46,000 and their share in total corporation tax rose to 23 per cent.

In short, the story of India’s corporation tax revenues is about how more and more companies have been taxed at a lower rate. As a result, the contribution of a large number of companies to the corporation tax kitty is getting smaller. No wonder, corporation tax buoyancy has suffered in the last seven years.

What has been the impact of corporate tax reductions on the wider economy?

In absolute value trends, there’s no perceptible spike in private sector gross fixed capital formation (GFCF) from reductions in the corporate tax rates. Nor is there any Laffer curve-type rise in corporate tax revenues.

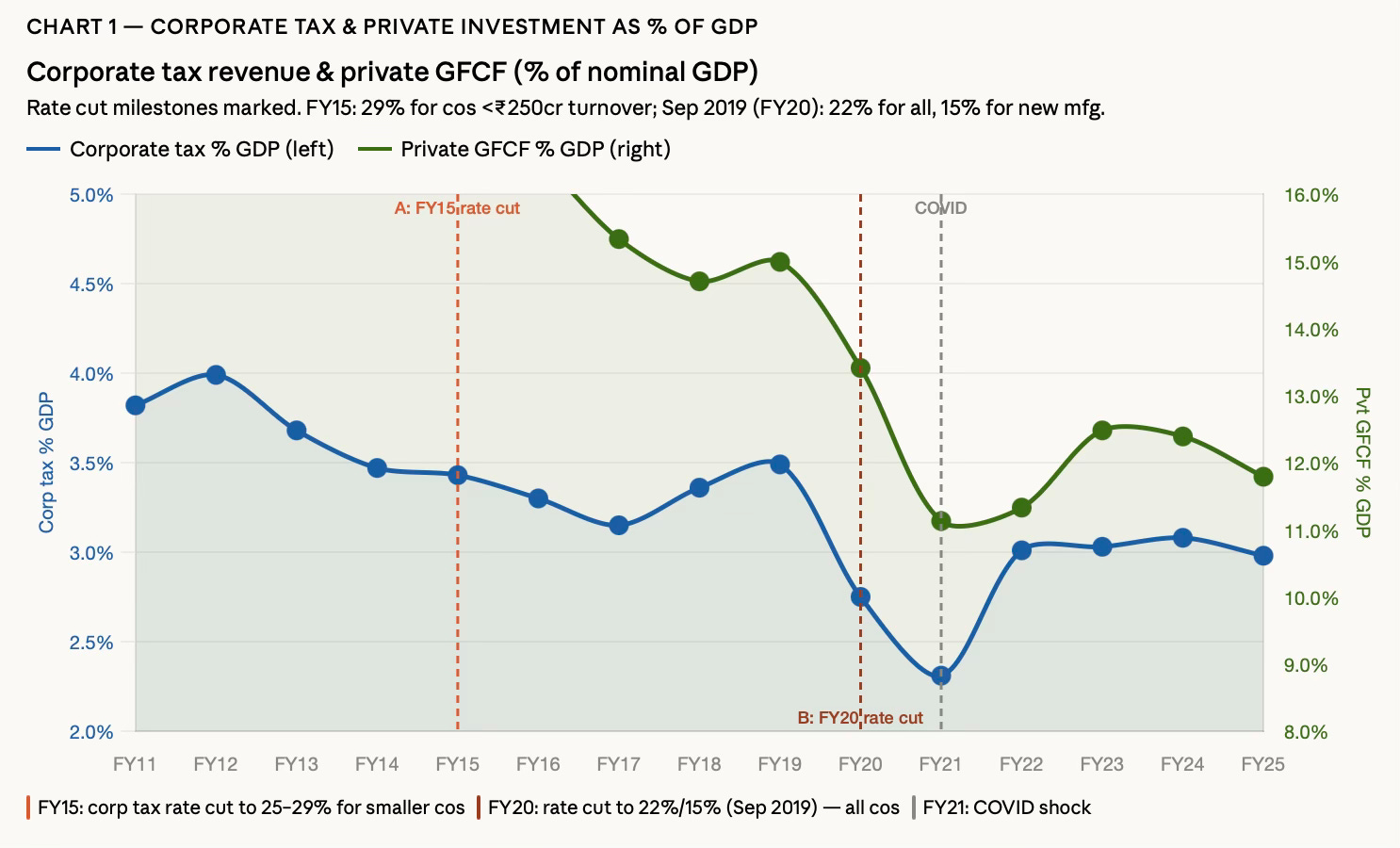

The twin objectives of corporate tax reductions are to spur private investment and, through it, drive up corporate tax collections. However, private sector GFCF as a share of GDP has fallen sharply since the two corporate tax cuts, and corporate tax revenues as a share of GDP have also been declining. It was at 2.98% of GDP in FY25 compared to 4% in FY12!

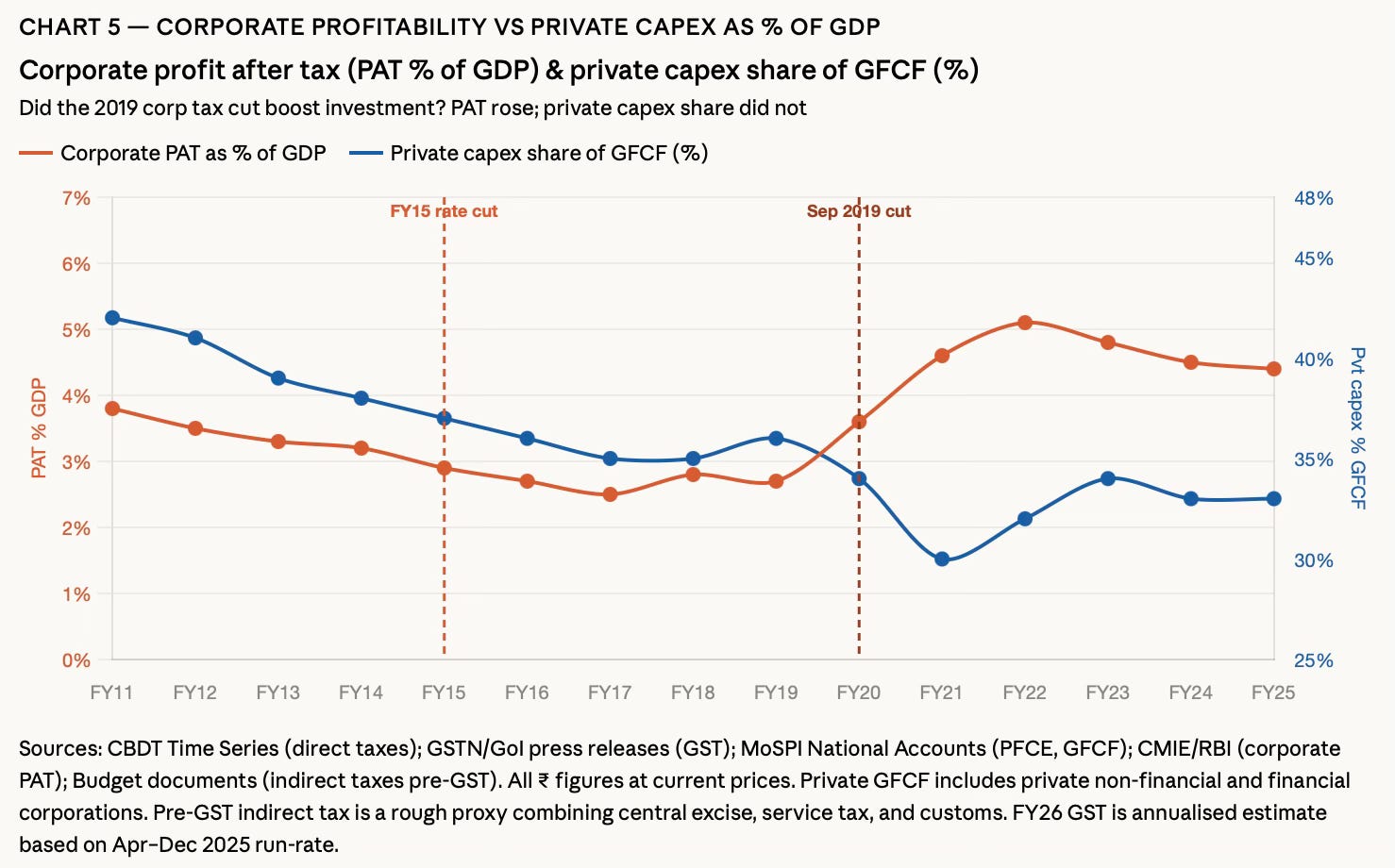

In fact, even as profits after tax rose as a share of GDP, the share of private capex in private sector GFCF declined and has been on a secular decline since 2010-11, apart from a slight recovery from the Covid-19 dip. This should be a matter of concern.

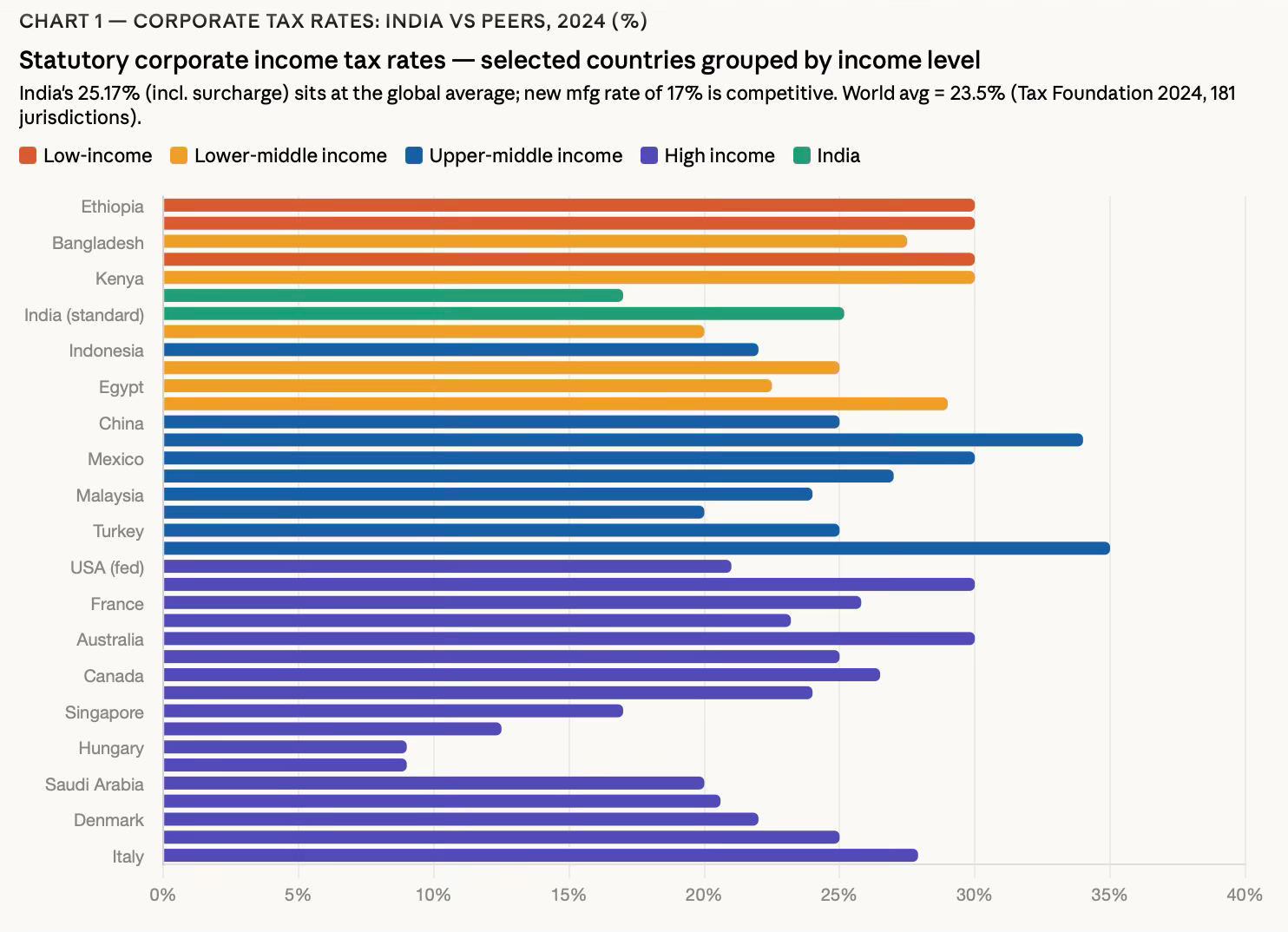

After these reductions, manufacturers in India face one of the lowest corporate tax rates globally today, above only a tiny number of countries. The rates are lower than all major developing country peers.

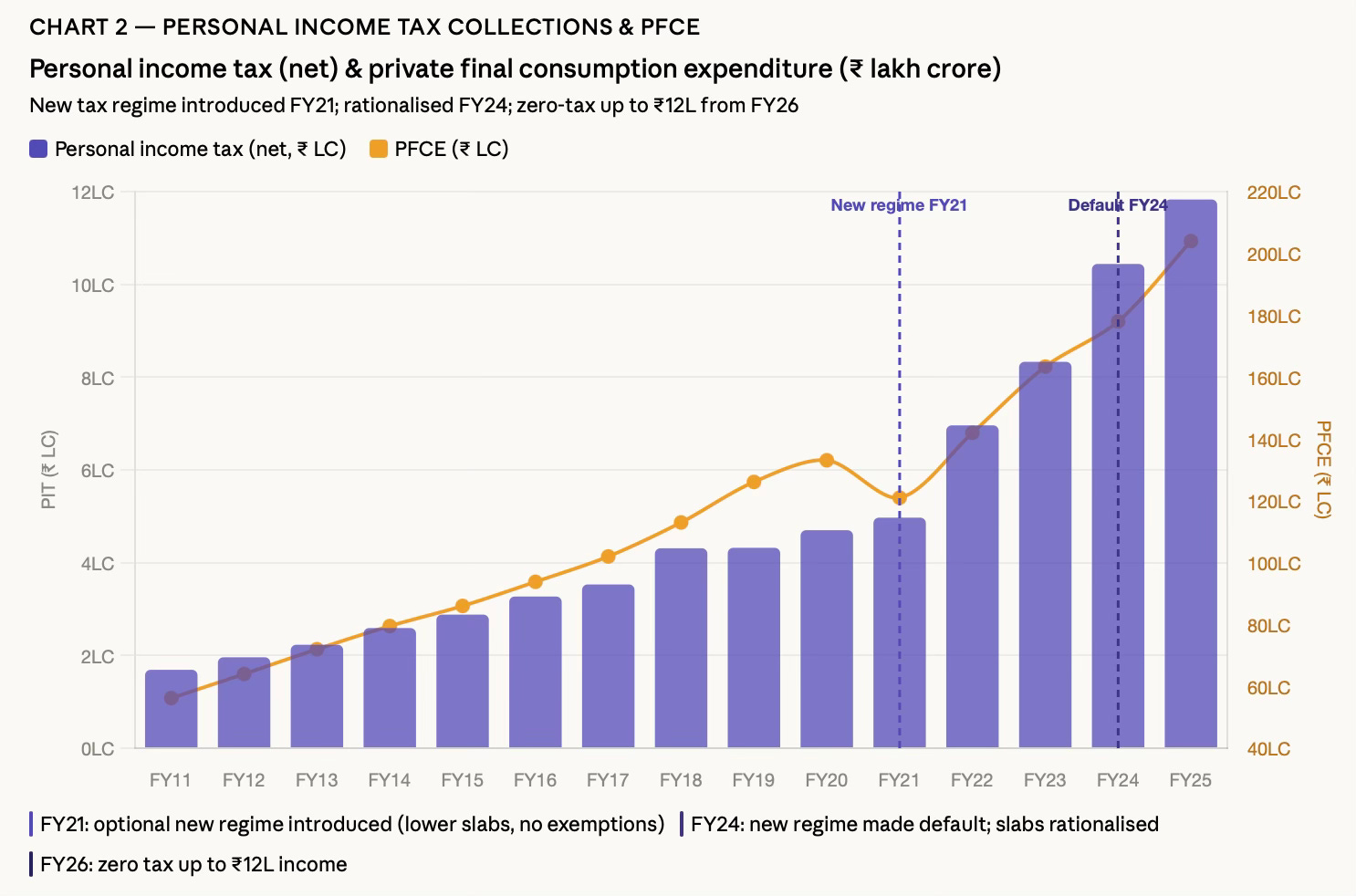

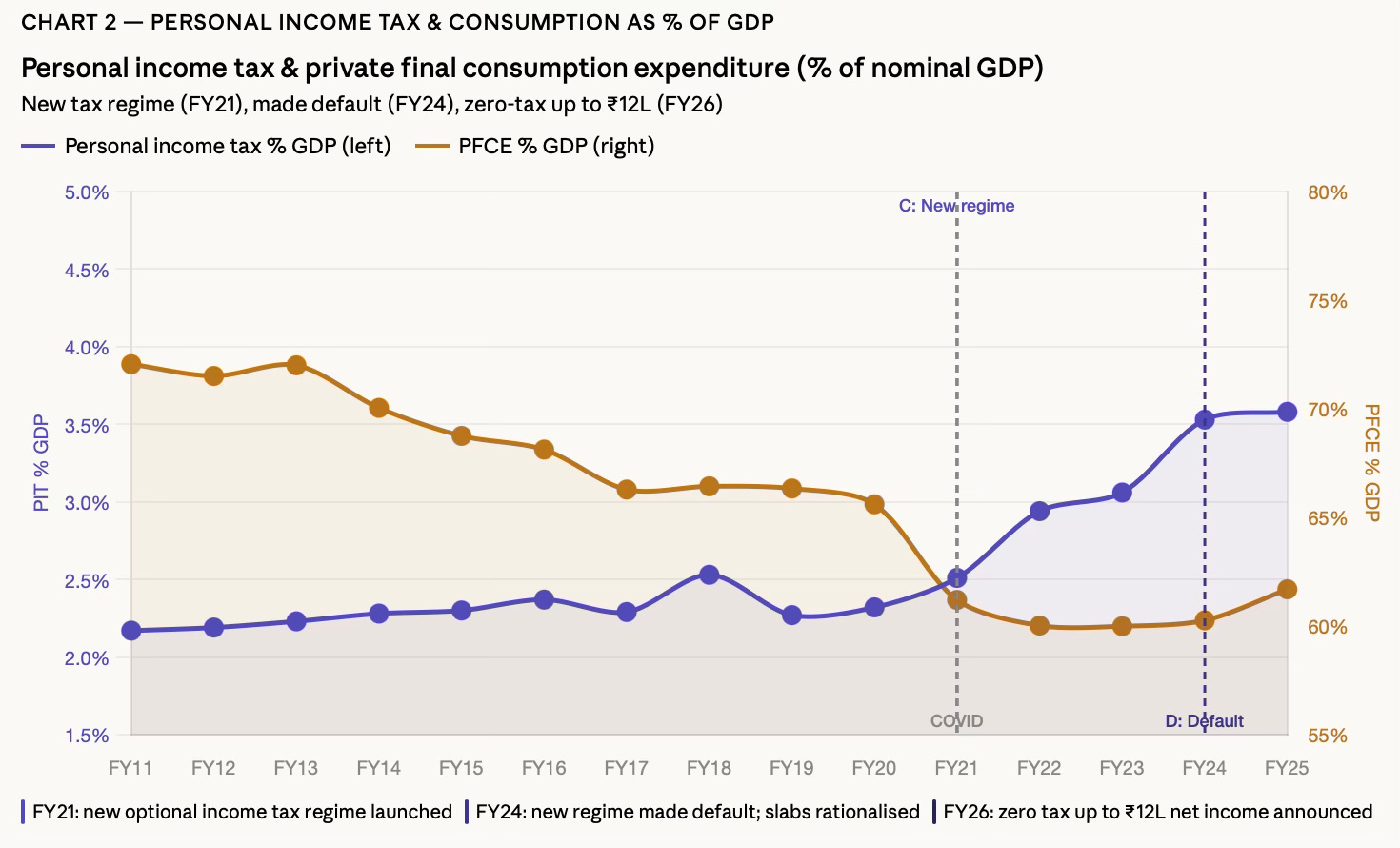

How do personal income tax (PIT) collections look? Encouragingly, it has been rising impressively since the regime shift in FY21. In fact, PIT collections have gone from ₹1.69 LC in FY11 to ₹11.83 LC in FY25 — growing faster than corporate tax every year since FY20, which is a structural reversal.

This performance on PIT is confirmed by its sharp increase as a share of GDP since the regime shift. Clearly, the PIT reforms (coupled perhaps with better detections and enforcement) have been a resounding success in terms of increasing PIT from 2.51% of GDP to 3.58% of GDP, a spectacular 43% increase as a share of GDP over just four years.

However, as a share of PFCE, the trend has been muted, remaining range-bound in the 60-62% of GDP, though there’s a slight uptick since FY24, which must be watched for sustainability.

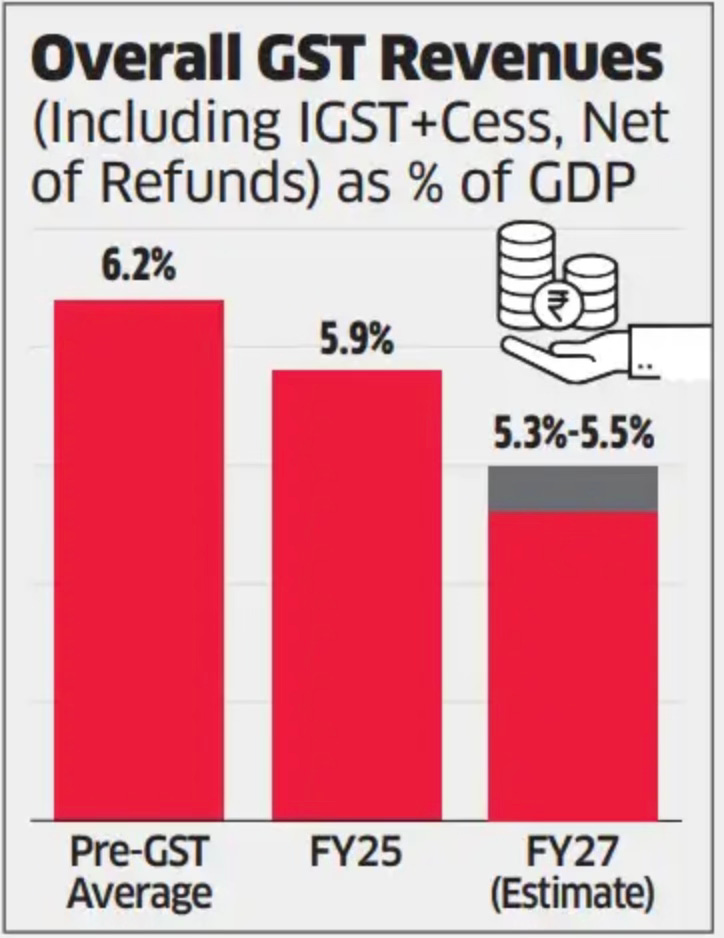

On the indirect taxes front, the revenue collections response to rationalisation and reductions have not been encouraging.

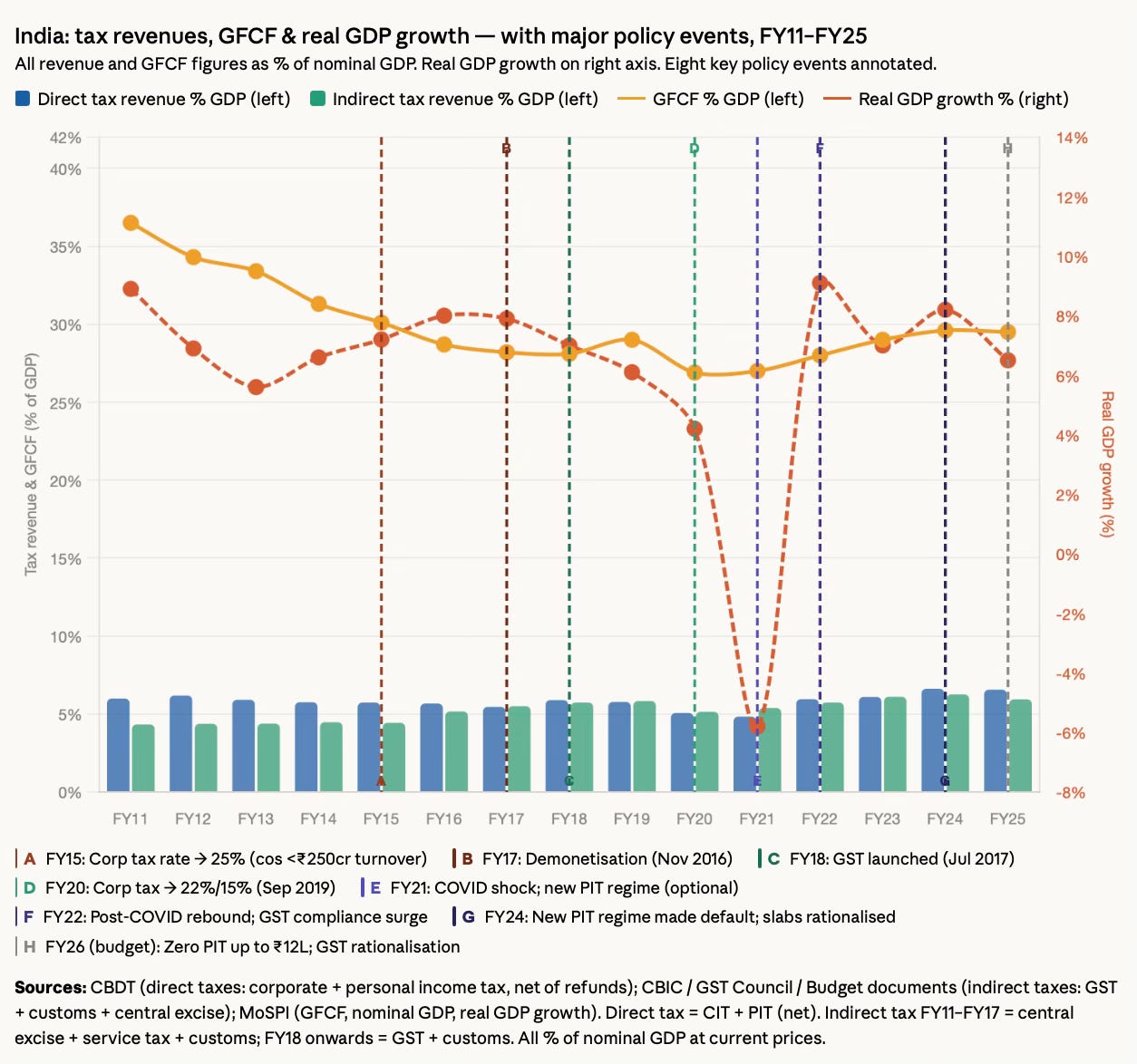

Bringing all of them together, if we take out the pandemic volatility, the decade of direct and indirect taxation reforms and rate reductions (eight episodes in total) does not appear to support the economic orthodoxy on tax reduction’s impact on investment, output, and revenues.

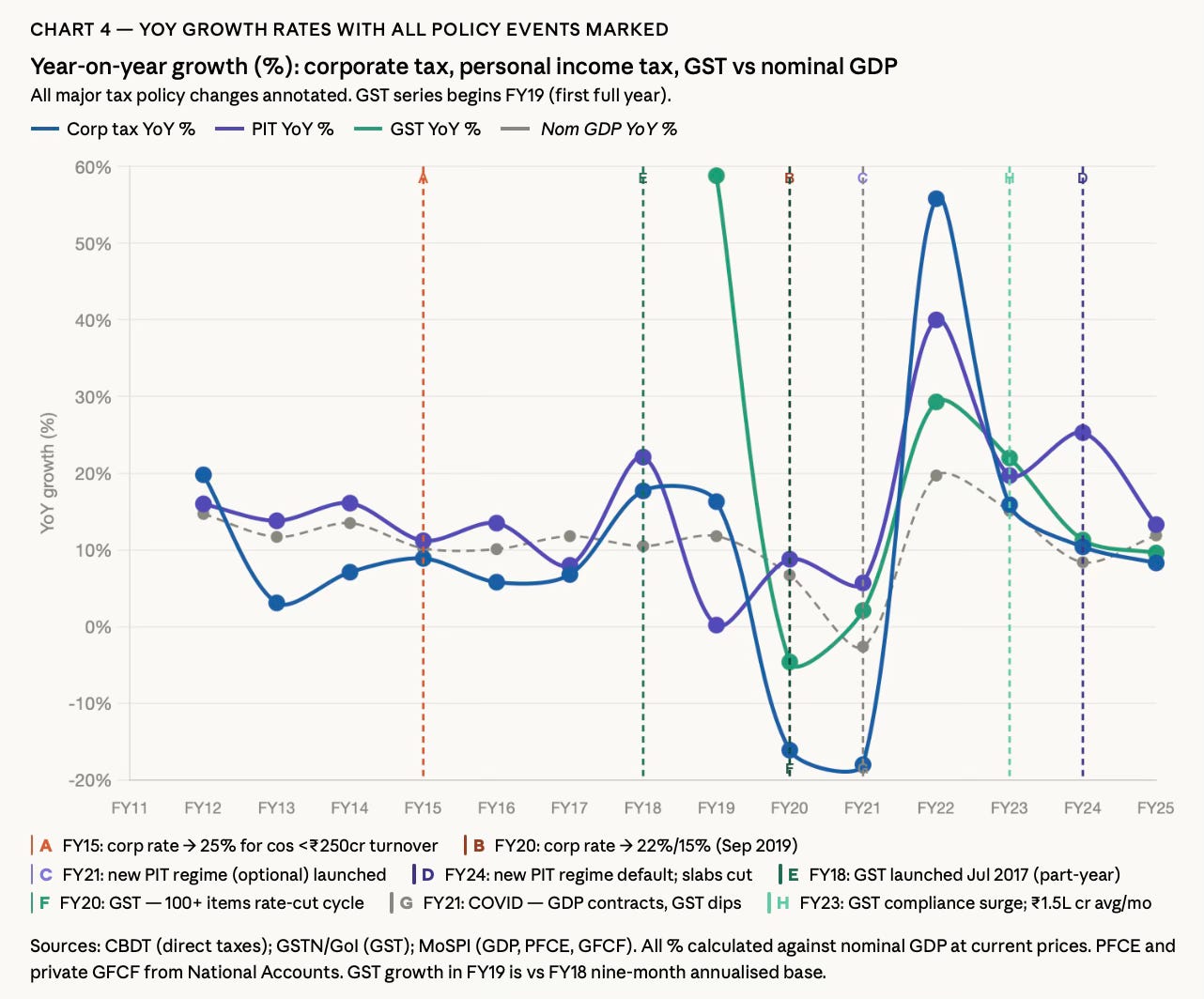

The launch of GST in July 2017 initially caused a dip in indirect tax collections in FY18, as businesses adjusted. The subsequent compliance surge (event F, FY22 onward) then drove indirect taxes to record levels — monthly GST collections averaging over ₹1.5 lakh crore from FY23.

The GFCF line tells a sobering story. From a peak of 36.5% of GDP in FY11, it fell steadily to 26.9% in FY20 and has recovered only modestly to about 29.5% in FY25 — still well below the FY11 peak. Neither the corporate tax cut (D) nor the post-COVID rebound has restored investment to its earlier trajectory, a point highlighted here.

The most notable pattern is that corporate taxes have shown the highest volatility among all tax revenues.

Post-COVID (FY22 onward), PIT has consistently grown 20–40% annually — far outpacing corporate tax — making personal income tax the engine of direct tax buoyancy. GST's 29% surge in FY22 and 22% in FY23 (H region) may be a reflection of the compliance dividend of digitisation and e-invoicing, more than any rate changes.

The positive revenue response of PIT compared to corporate tax is perhaps due to corporate tax cuts being a one-time rate reduction that reduced the base but boosted profitability without proportionally boosting investment, while PIT benefits from a widening formal employment base. It is also perhaps understandable that the problem with corporate tax is less about base expansion and more about avoidance and evasion, neither of which is directly addressed through rate reductions.

The private corporate sector's savings have consistently gone up — from 9.5% of GDP in FY12 to over 11% — while its investment as a share of GDP has been falling, indicating that companies have been using higher post-tax profits to build reserves rather than to invest in fresh capacity. It is not incorrect to argue that the 2019 corporate tax cut largely transferred fiscal resources to shareholders and balance-sheet strengthening rather than to productive fixed investment. This also says something about the economy’s aggregate demand growth expectations.

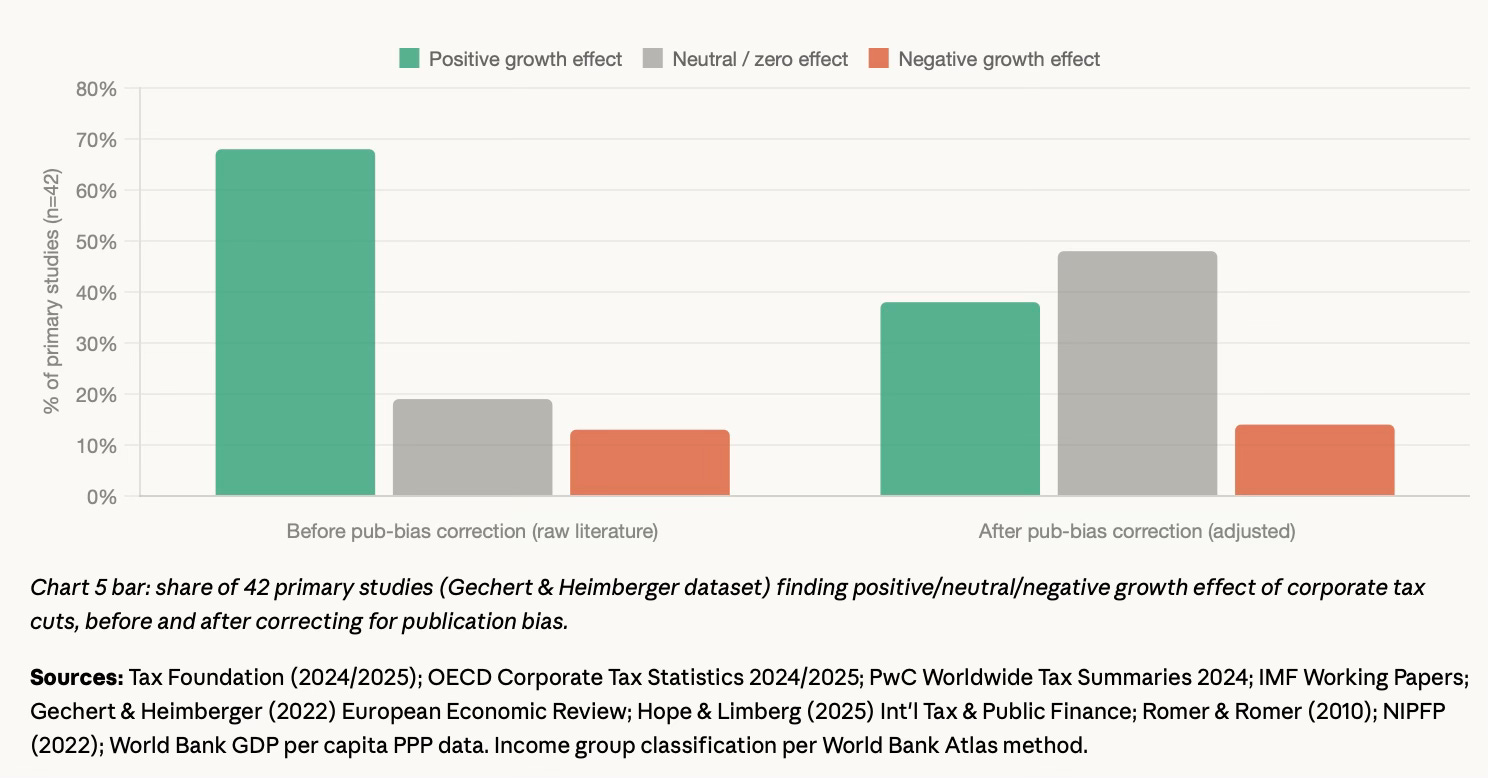

This experience on corporate tax reductions is in line with global experience. A meta-study of 441 estimates from 42 primary studies by Sebastian Gechert and Philipp Heimberger corrected for publication bias — which favours reporting growth-enhancing results — and found that the average effect of corporate tax cuts on GDP growth cannot be rejected from zero. The raw literature (before correction) shows 68% of studies finding a positive effect, but once publication selectivity is accounted for, this falls to about 38%, with nearly half finding a neutral result.

Interestingly, they show that “it is about 2.7 to 3 times more likely to publish a result showing a statistically significant positive impact of corporate tax cuts on growth compared to a significant negative result.” This positive bias is a big problem across economics and elsewhere, and does not get the attention it deserves.

Their main findings are worth quoting:

First, corporate tax cuts tend to be even less growth friendly when considering a short time horizon. Second, considering both rate and base changes by looking at an effective average corporate tax rate may lead to slightly more positive growth rates in response to tax cuts. However, this is an outlier as compared to the rest of the literature using effective marginal tax rates, corporate tax shares in GDP or statutory tax rates, and the result is also not entirely robust to variations in the meta-regression estimator. Third, there does not seem to be a substantial difference between OECD and non-OECD countries regarding the growth effects of corporate tax changes. Fourth, explicitly controlling for other types of taxation (personal income taxes, capital income taxes, property taxes, sale taxes) does not affect our main findings. Fifth, more recent studies tend to find less growth enhancing effects of corporate tax cuts. Finally, it matters what happens to other budgetary components in conjunction with a corporate tax change: if we hold government spending fixed, a corporate tax hike will be slightly more detrimental to growth, implying that using the additional revenues for government spending instead of fiscal consolidation may foster growth, in line with theoretical arguments from endogenous growth models and empirical evidence on substantial productivity of public capital.

The key conditional findings are: corporate tax cuts reliably attract FDI (semi-elasticity ~-2.9, robust across studies), but their effect on domestic investment is weaker. When product markets have imperfections — which is increasingly the case given rising corporate market power — firms respond to tax cuts by increasing savings and reserves rather than investment. India’s equivalent experience — corporate PAT rising to record levels while private GFCF as a share of GDP fell — is a near-perfect illustration of this theoretical mechanism.

See also this earlier blog post on the questionable virtues of lowering corporate tax rates.

To conclude, let me add to Dan Neidle’s nice description of the tax populism of right and left-wing politicians.

The tax populism of the right is that we can cut tax without anyone (or at least anyone the populists care about) being hit by cuts in services or benefits. There’s a magic money tree of government waste that can be harvested without consequence. The tax populism of the left is that we can fund services without anyone (or at least anyone these populists care about) being hit by increased tax. There’s another magic money tree, where trade-offs don’t exist.

The enduring tax populism among economists (and market experts) is that we can cut taxes and harvest a triple-win of an increase in investments, a rise in output, and higher revenue collections. There are no such free lunches. India is only the latest in the series of data points that invalidate this tax populism.

No comments:

Post a Comment