The Trump chaos has been a godsend to China by deflecting attention from the world economy’s China problem. It has allowed the country the space to continue flooding the world with its heavily subsidised exports.

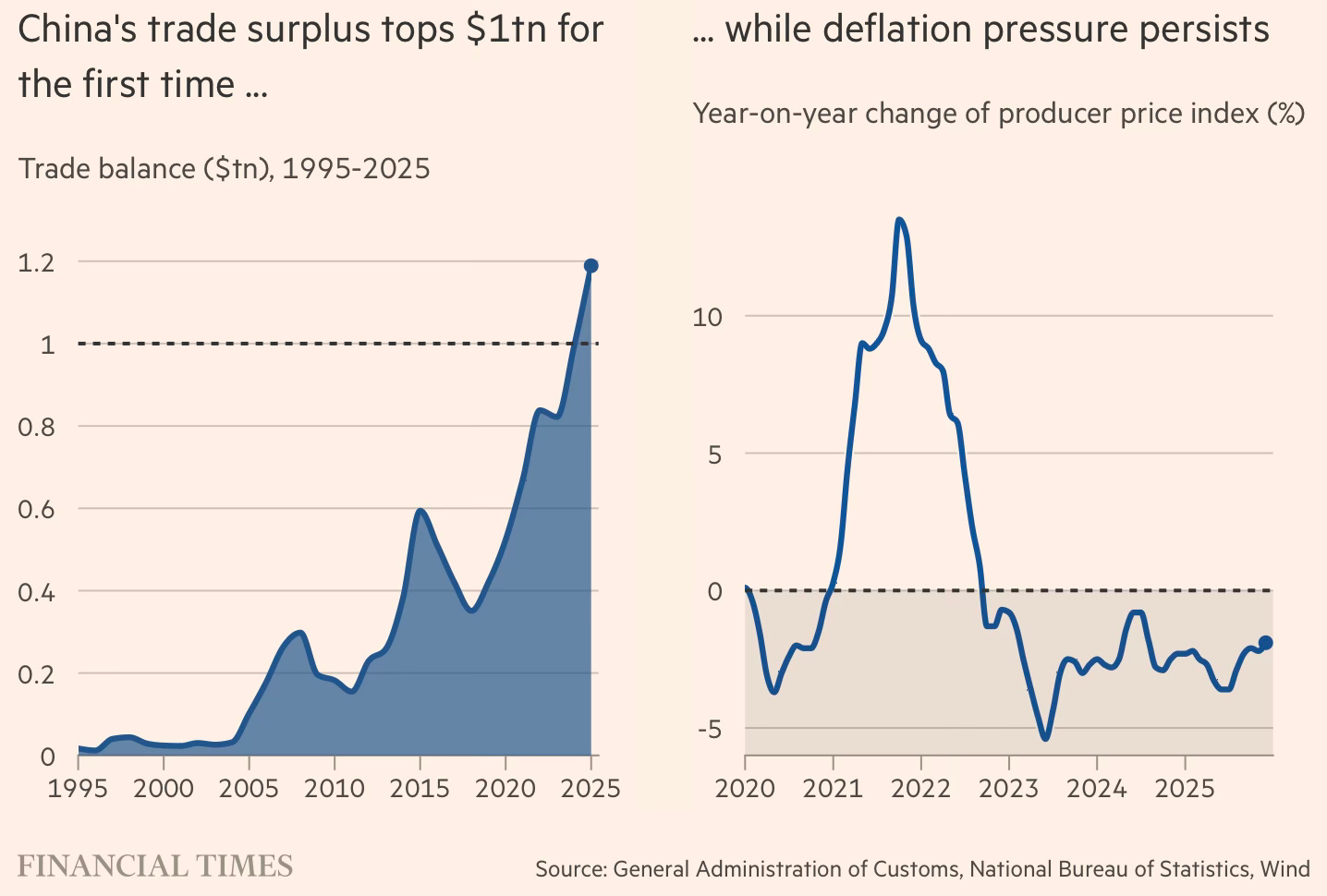

1. Ruchir Sharma has an excellent description of the fundamental problem with China’s growth model. First, some facts about its rising trade surplus.

This decade, Beijing has dropped export prices by nearly 20 per cent, producing a 40 per cent surge in volume. Booming exports along with weak imports increased China’s trade surplus last year by 20 per cent to a record $1.2tn. Net exports accounted for almost a third of its 2025 GDP growth, a bloated share even by China’s standards. As a share of global GDP, no nation has ever had a larger trade surplus, and that includes Japan during its 1980s heyday. China’s dumping offensive is deindustrialising rival exporters the world over, idling car factories in Thailand and textile plants in Indonesia. Across Asia, nations where Chinese imports are rising fastest also tend to have the weakest job growth. More than 50 of the world’s 70 largest economies have taken steps to defend themselves against Chinese dumping.

This has come at a prohibitive cost and engendered economy-wide distortions.

The root of the problem is the country’s growth target. Of the nearly 40 nations that rose into the developed ranks after the second world war, none faced the twin hurdles confronting China today: depopulation and massive debt. No other major nation in history has managed to sustain growth above 2 per cent with a shrinking labour force. And at 340 per cent of GDP, China’s total debts are higher than any other emerging economy by far. Beijing is trying to engineer a historically implausible miracle. Given its demographic decline, China can hit its target only by raising output per worker, but maintaining overall productivity growth near 5 per cent would be an unprecedented feat at this stage of development. Lately China has been moving in the opposite direction. Productivity growth includes contributions from labour, capital, and a critical “total factor” that aims to capture how much growth labour is squeezing out of the investment. The Conference Board estimates that this key third factor has fallen to near zero this decade, implying that China is generating growth only by investing more heavily.

China keeps pumping out credit to fund more investment, but mostly it’s getting a bigger debt pile. To generate $1 of GDP growth in China, it now takes $6 of new debt, up from $1 two decades ago. Beijing is counting on investment in new technologies including AI to boost productivity, but it’s highly unlikely that boost will be big enough to sustain productivity growth near 5 per cent. China’s real potential growth rate is probably between 2 and 3 per cent… The real problem is that investment keeps growing faster than consumption, compelling China to flood the world with its excess production. Chinese exports, now $3.8tn a year, recently surpassed US imports for the first time.

2. The record $1.2 trillion trade surplus in 2025 and the claim of having achieved 5% GDP growth rate for the year should not detract from the increasing pile of problems facing the economy. This is a good summary of the signatures of China’s faltering economy.

The growing dichotomy between China’s thriving trade-focused sector and its anaemic domestic economy. While China’s world-conquering exporters and powerhouse innovation clusters can make the country seem like an unblemished economic success, painful technology transitions and faltering domestic demand mean that for many businesses and citizens, these are times of increasing hardship. Cities such as Shenyang, which turned itself from a centre of heavy industry to an automotive hub during market reforms in the 1990s and 2000s, are struggling to evolve. Shenyang now wants to pivot into electronics and other industries but, like many Chinese provinces, is unwilling to let favoured businesses die…

Yet investment was the weakest since the 1990s as property prices fell and new construction starts declined… A four-year real estate slump has undermined domestic demand and added to deflationary pressures. In November, retail sales growth hit a three-year low. Meanwhile, Beijing’s interventionist policies from currency depreciation to subsidies to support for favoured industries are driving overcapacity in sectors ranging from automotives and batteries to solar panels. Plunging profitability — industrial profits fell 13 per cent year-on-year in November — has made companies reluctant to hire or pay high salaries.

Zombie companies now account for more than 12 per cent of total registered companies, more than double the level in 2018 and nearly double the global proportion, according to a study led by Alicia García-Herrero, chief Asia-Pacific economist at French investment bank Natixis… Unemployment among those aged 16-24 was 17 per cent in November compared with about 11 per cent pre-pandemic. While China’s overall official unemployment rate remains stable at about 5 per cent, many ordinary Chinese people say the figures do not mirror reality.

Ironically, the rising trade surplus may carry the seeds for the weakening of the domestic economy,

As long as Beijing can rely on exports for growth, analysts expect it to let the housing market continue to deflate and to concentrate on boosting the high-tech sector to compete with the US — choices that will only deepen the economic divide.

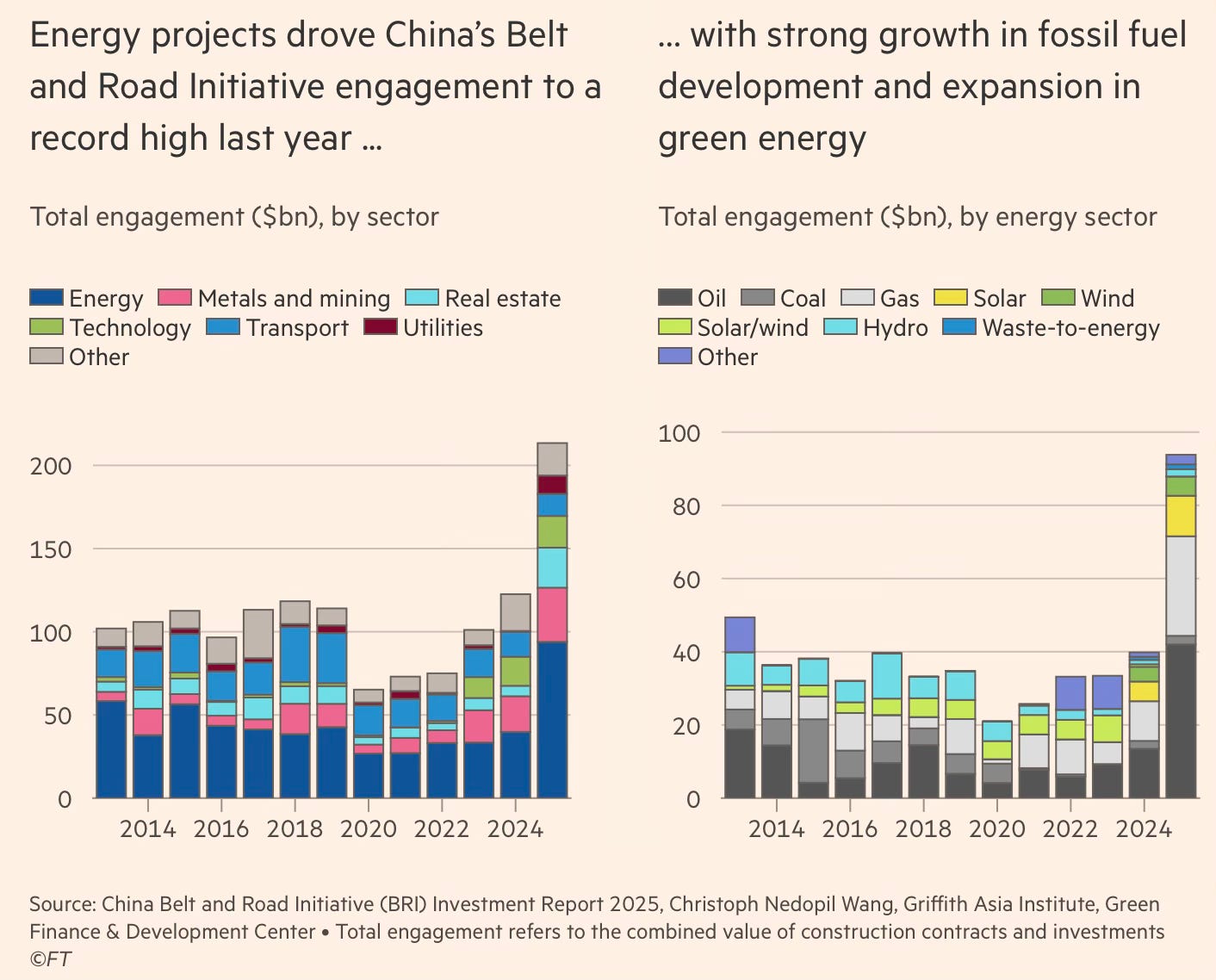

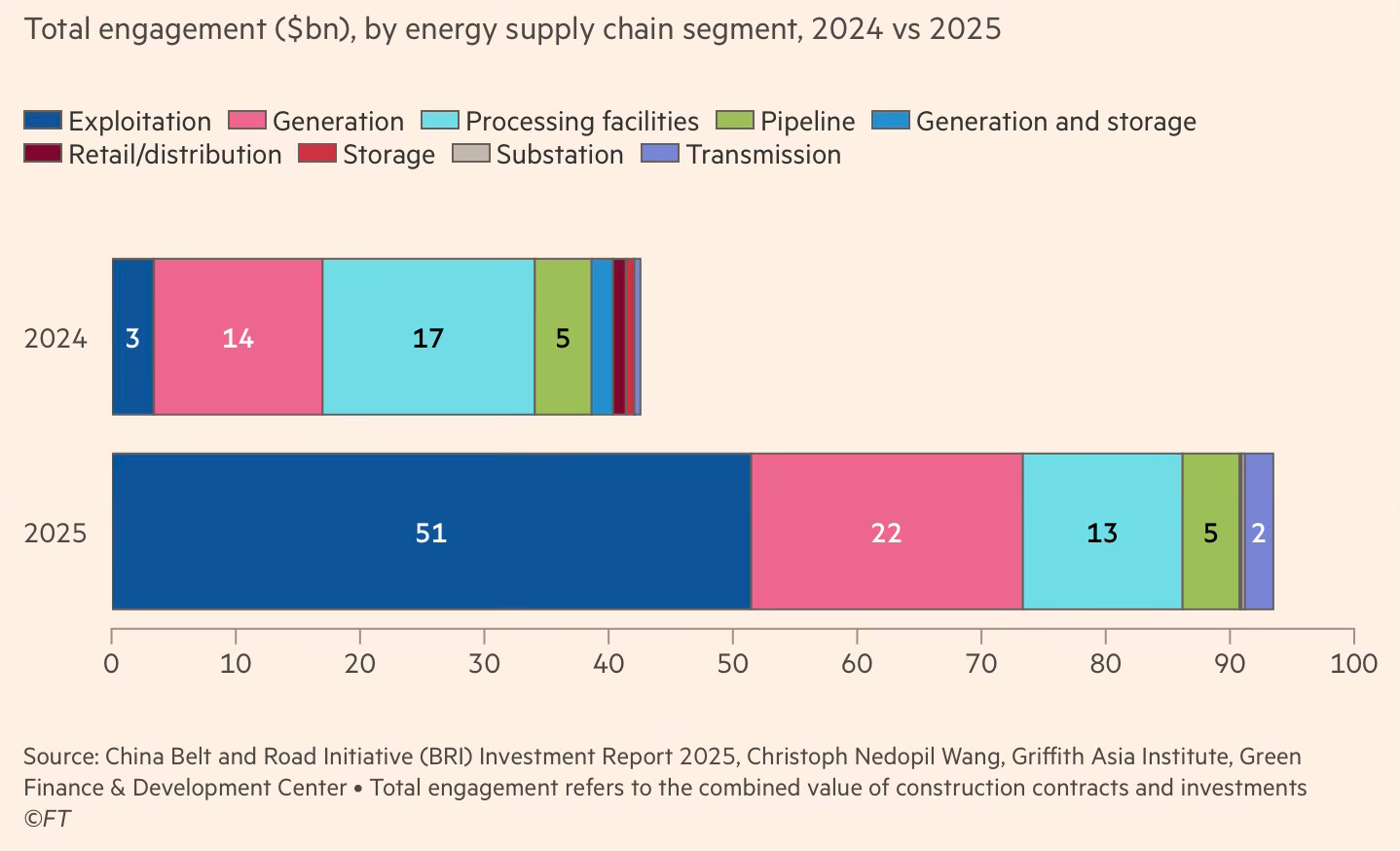

3. Another outlet to channel domestic capacity on the face of weakening domestic demand is the projects under the Belt and Road Initiative (BRI). China’s investments under the BRI Project surged in 2025.

The surge in new investment and construction deals was dominated by gas megaprojects and green power, according to research by Australia’s Griffith University and the Green Finance & Development Center in Shanghai. Beijing signed 350 deals last year, up from 293 worth $122.6bn in 2024... Last year’s figures brought the total cumulative value of BRI contracts and investments since its launch to $1.4tn, the study found. The growth in 2025 was driven by multibillion-dollar megaprojects including a gas development in the Republic of the Congo led by Southernpec, Nigeria’s Ogidigben Gas Revolution Industrial Park led by China National Chemical Engineering and a petrochemical plant in North Kalimantan, Indonesia, led by a Chinese joint venture of Tongkun Group and Xinfengming Group.

Fossil fuel exploitation became the main focus of China’s energy engagement with its BRI partners.

The value of energy-related projects last year was $93.9bn, the highest since the BRI’s inception and more than double the 2024 level. It included $18bn in wind, solar and waste-to-energy projects, underscoring China’s lead in clean technology. Metals and mining also hit a record at $32.6bn, including a majority of spending on minerals processing abroad, highlighting how Beijing has used the BRI to secure long-term access to resources. That included a surge of investment in copper in the second half of the year.

The scale and direction of the shift in 2025 point to China tightening global mineral supply chains toward itself and excluding the US.

4. The NYT writes that China’s campaign to dominate rare earths has its origins in the 1960s. In April 1964, China discovered that an iron ore mine near Baotou, 50 miles from the Mongolian border, held the world’s largest deposit of the 17 metals that belong to the rare earth family. Today, China produces 90% of the world’s rare earths and rare earth magnets.

Deng Xiaoping, then a high-ranking Chinese Communist Party official, visited the remote desert mine, owned by a military steel maker, to inspect the massive cache.“We need to develop steel, and we also need to develop rare earths,” declared Mr. Deng, who over a decade later would emerge as China’s top leader… China’s centrality in rare earths didn’t happen by accident. It is the result of decades of planning and domestic and overseas investment, often directed from the highest levels of the party and the Chinese government. In the early 1970s, the People’s Liberation Army launched a little-known research program to develop potential military uses of rare earths.

Mr. Deng kept pushing China’s rare-earth advancement forward in the 1980s and 1990s together with Wen Jiabao, a geologist by training who went on to serve as China’s premier from 2003 to 2013. Under Mr. Wen, China consolidated what was a highly splintered web of mostly private companies into a tightly run arm of the Chinese government. Mr. Wen closed mines run by smugglers and cleaned up the industry’s most severe pollution. The sector grew in size and expertise. In 2019, seven years into his reign as China’s top leader, Xi Jinping described rare earths as “an important strategic resource.”.. In April and again in October, 2025 China enacted new export controls that allowed it to withhold supplies of rare earths and rare-earth magnets and force Mr. Trump to compromise on tariffs…

This is a fascinating account of how Deng and Co stitched together the rare earths industry in China.

The father of the industry was Xu Guangxian, a tall, thin man from Shaoxing, a town near Shanghai… Shortly after World War II, Mr. Xu completed a doctorate in chemistry at Columbia University. He returned home to teach and do research at Peking University in Beijing… Purifying rare earths is extraordinarily difficult. Early chemists named them rare not because they were hard to find — they are not — but because of the challenge of separating them from one another… At Peking University, Mr. Xu and his wife, Gao Xiaoxia, also an accomplished chemical engineer… had a revolutionary breakthrough: Rare earths could be purified using inexpensive hydrochloric acid and cheap plastic holding tanks rigged together.

Mixed rare earths were poured in one end, and specific kinds of rare earths, after binding to various solvents, emerged from different outlets at the other end. It was the first rare-earth assembly line, a crude version of a process still used today. Production costs plummeted with Mr. Xu’s techniques. Mr. Xu installed his first production lines, in Baotou and at a chemical plant in Shanghai, and started training engineers from all over China… A Five-Year Plan drafted by Mr. Deng and Vice Premier Mr. Fang Yi, covering 1981 to 1985, ordered that China “increase the production of rare-earth metals.” More than 100 towns and villages across China built rare-earth refineries in the 1980s, many of them state-owned and few with meaningful pollution controls. By 1986, China was the world’s largest producer of rare earths.

Rare earths were then used in low-tech manufacturing. Thanks to research in the US and Japan, rare earths became central to advanced manufacturing. But Chinese expertise in rare earths also owes to the strategic short-sightedness of the US.

In 1983, engineers at General Motors and the Japanese magnet maker Sumitomo Special Metals each announced they had developed powerful rare-earth magnets. The magnets were immediately put to use in electric motors in the auto industry and beyond. China lacked expertise to turn rare earths into magnets. It would purchase that know-how from the United States. General Motors had turned its discovery into a thriving magnet manufacturing subsidiary in Indiana, called Magnequench. But a decade later, G.M. decided to stop making many of its own auto parts.

Magnequench was sold in 1995 to a consortium of investors that included two Chinese companies led by sons-in-law of Mr. Deng: Wu Jianchang and Zhang Hong. Under President Bill Clinton, the U.S. government allowed the transaction to proceed because a majority of the owners were American. The American owners were mainly institutional investors. Mr. Deng’s sons-in-law had led companies with deep ties to low-cost magnet manufacturing in China. Magnequench started moving its equipment in 2001 to Tianjin and Ningbo, China, and shut down in Valparaiso, Ind., by 2004… the Chinese magnet factory at Tianjin had previously been using processes “that were at least 10 years behind” what Magnequench had developed in Valparaiso. The move by Magnequench, which was then bought in 2005 by a Canadian rare-earth processor with operations in China, taught China how to make rare-earth magnets.

Under Wen Jiabao, China focused on the pollution stemming from rare earth refineries, which were contaminating the Yellow River. In 2006, China imposed annual quotas on exports to limit processing and stem pollution, and has since consolidated companies under state ownership. Its dominance also stems from capabilities

Today, China is working to cement its lead in rare earths by churning out more trained technicians and researchers than any other country. Programs in rare earths are offered by 39 universities. The United States and Europe have no such programs — not even at Iowa State University, an institution that once trained generations of American engineers in rare earths. Iowa State has not offered a course in rare earths for the last several years and has one graduate student doing independent study in the field. It plans to offer a course next year. China has hundreds of scientists exploring rare-earth technologies.

Technicians at a refinery in Wuxi, a city near Shanghai, spent seven years doing experiments to refine dysprosium, a rare earth, to extraordinary purity. The refinery is now the world’s sole source of that rare earth, which is used in capacitors — tiny devices to control electricity — found in Nvidia’s Blackwell artificial intelligence chips. Most of the refinery’s shares were until this year owned by Neo Performance Materials, the Canadian company that acquired Magnequench in 2005. A Chinese state-controlled company bought most of the shares on April 1. Then on April 4, Beijing halted exports of dysprosium and six other kinds of rare earths to the United States and its allies… Beijing has halted most exports of rare-earth processing equipment. It has also taken away the passports of rare-earth technicians to prevent them from leaving the country with valuable information.

5. In a good illustration of regulation with Chinese characteristics, Beijing manages to strike a balance between strictly controlling sales of unregulated drugs inside the country, while allowing their massive and growing illegal exports.

FT has a story about the burgeoning trade in injectable peptide drugs that have become popular in the West due to the success of GLP-1 weight-loss peptide drugs like semaglutide and tirzepatide.

Industry insiders estimate there are about 1,000 Chinese sellers targeting overseas customers, a figure that has climbed sharply in recent months. Rising competition has pushed prices down. Sellers quoted prices such as $65 for 10 vials of BPC-157 at 10mg, or $70 for the same quantity of semaglutide — which compares to $110 and $1,000 for the same quantities on US websites… Most peptides are produced by about a dozen factories clustered in Shenzhen and Changsha, the capital of Hunan province. These facilities originally manufactured active pharmaceutical ingredients for the pharmaceutical industry before pivoting towards the grey market.

Multiple layers of intermediaries now sit between factories and consumers. “We never touch the product. We don’t know who makes it,” said one seller… one seller said he had no intention of trying the products himself. “I’m overweight, but I wouldn’t dare take these drugs,” he said, laughing. “It’s westerners who are obsessed with them. I just sell them.”… Chinese authorities have been cracking down on domestic sales of unregulated GLP-1 weight-loss drugs, arresting scores of sellers. A review of court records shows at least 40 cases of people being charged with black-market peptide sales…

Finding sellers online is easy. They advertise openly on cross-border ecommerce platforms such as Global Sources, as well as on Facebook, Telegram and WhatsApp… The FT visited the registered addresses of eight suppliers and found that most used false locations, with no functioning phone numbers or email contacts… Inside one office in China visited by the FT, a group of young women chatted with customers in Brazil, the US and Canada. They used ChatGPT to draft sales copy for WhatsApp messages and worked with western influencers who promote the products on TikTok and Facebook in exchange for commissions… Sellers also shoulder the risk of shipments being seized by logistics companies or customs authorities…

6. Scott Kennedy has a very good paper on China’s high-tech sector—some headline facts.

Chinese industrial policy spending was estimated to be 4.9 percent of GDP. More recently, an International Monetary Fund (IMF) study, applying a similar methodology to data from 2011 to 2023, found that Chinese industrial policy spending ranged between 4.0 and 5.5 percent of GDP. The authors did not compute a parallel estimate for the United States, but they found that China’s spending was over three times the amount outlaid by the European Union…

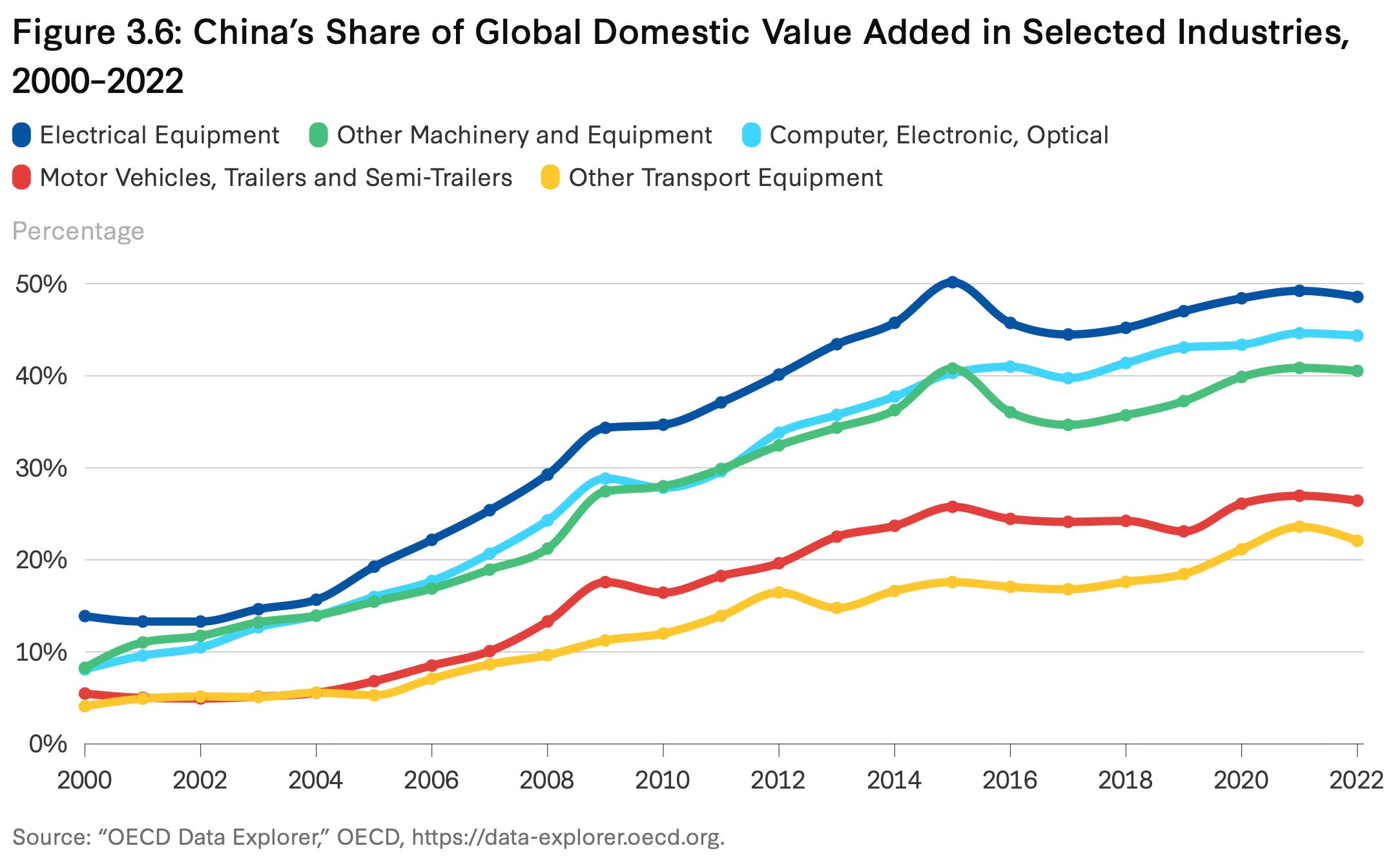

According to the World Bank, China contributed $625.2 billion in domestic value added to manufactured goods in 2004, just 8.5 percent of the world total. By 2024, China’s output had jumped to $4.7 trillion, accounting for 28.0 percent of all manufacturing value added globally… China’s share of domestic value added in manufacturing has risen across multiple industries since 2000… Critically, the share of China’s exports by foreign-invested domestic firms has dropped over the same period, from nearly 60 percent to 27 percent, meaning that this shift toward higher domestic value added is not a reflection of the influence of foreign-invested firms in China.

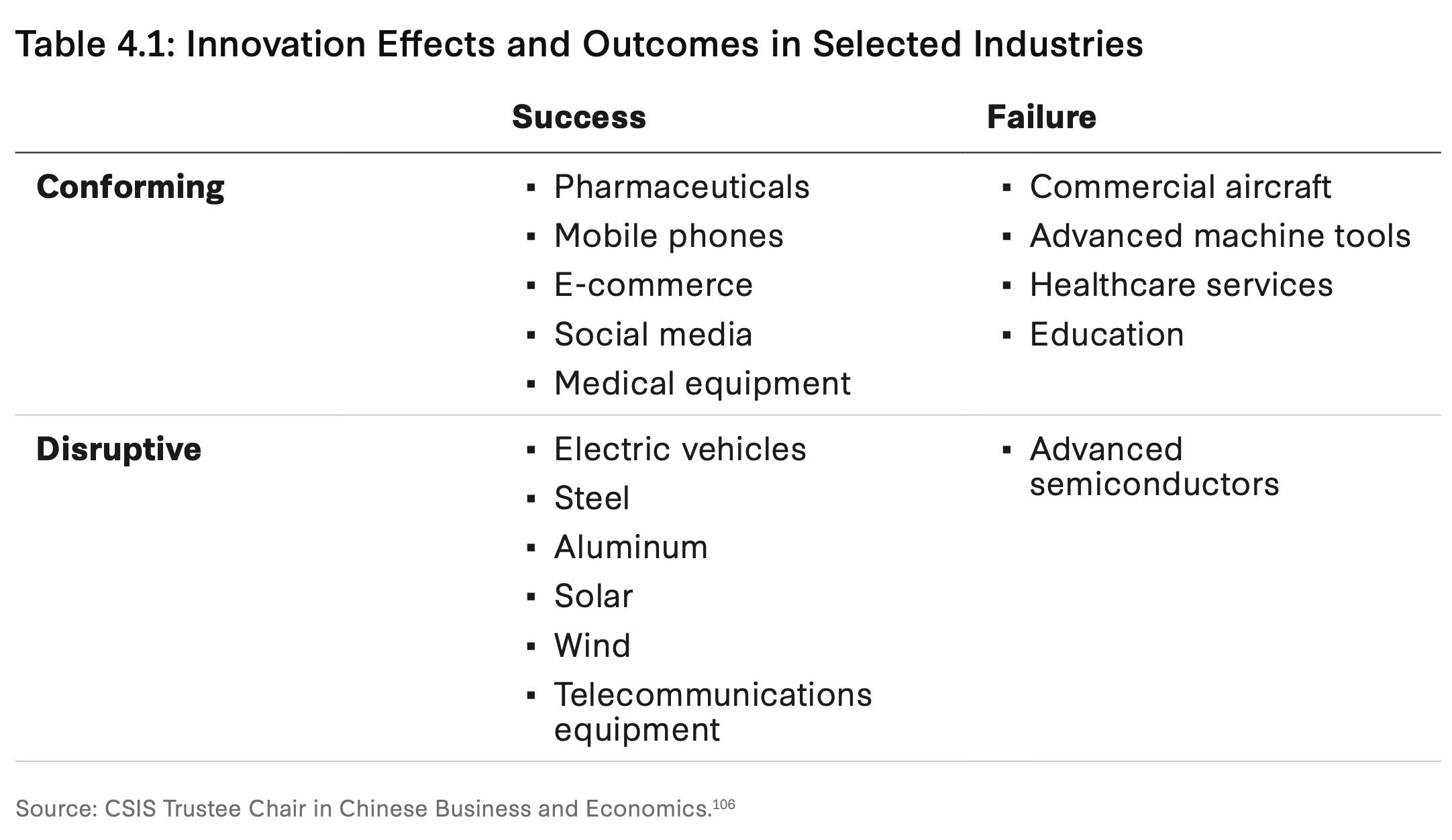

The report points to the wide variations in the outcomes of China’s industrial policy interventions. It uses a four-fold framework to categorise them.

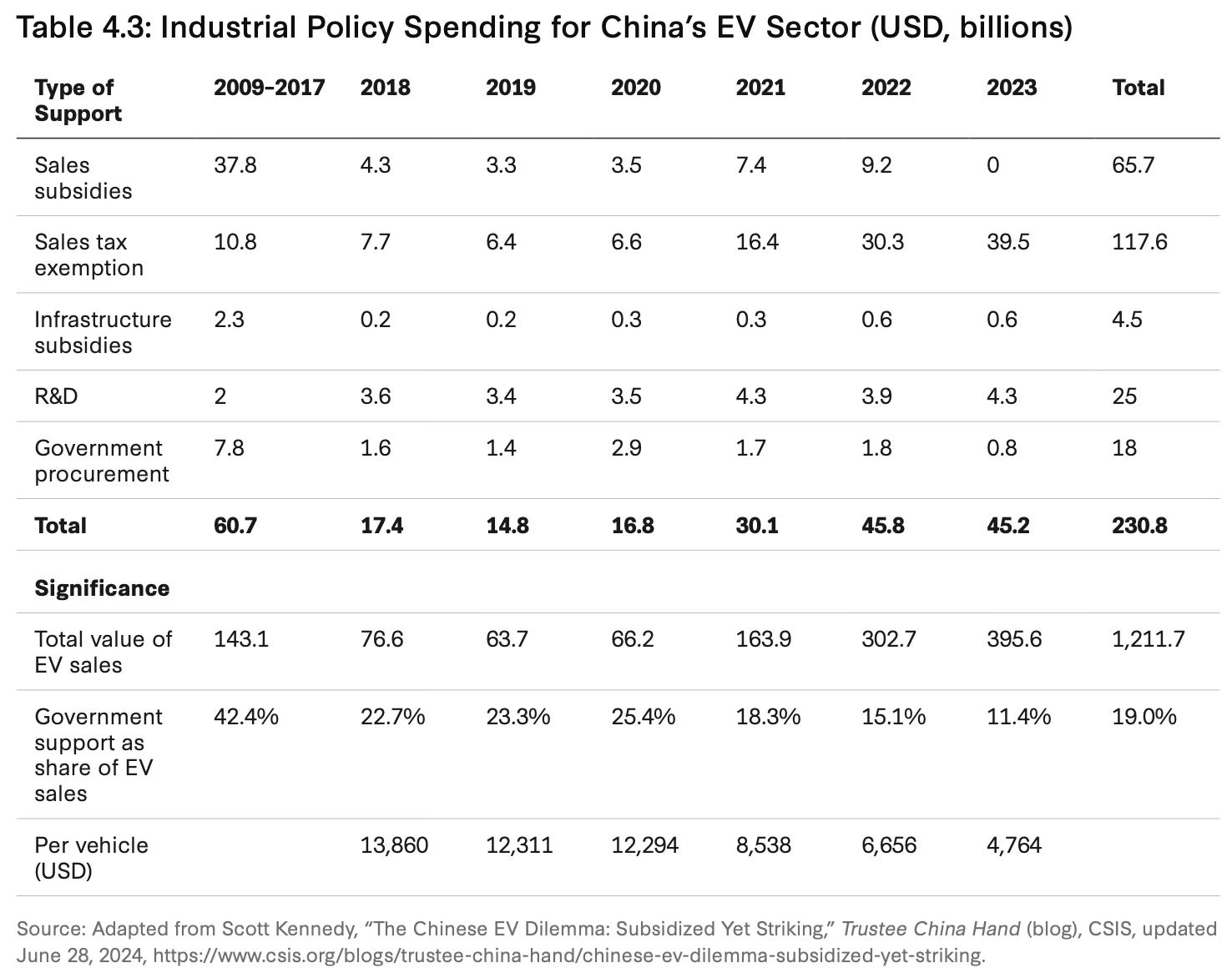

Chinese EV firms are estimated to have received nearly $231 bn in fiscal support in the 2008-23 period.

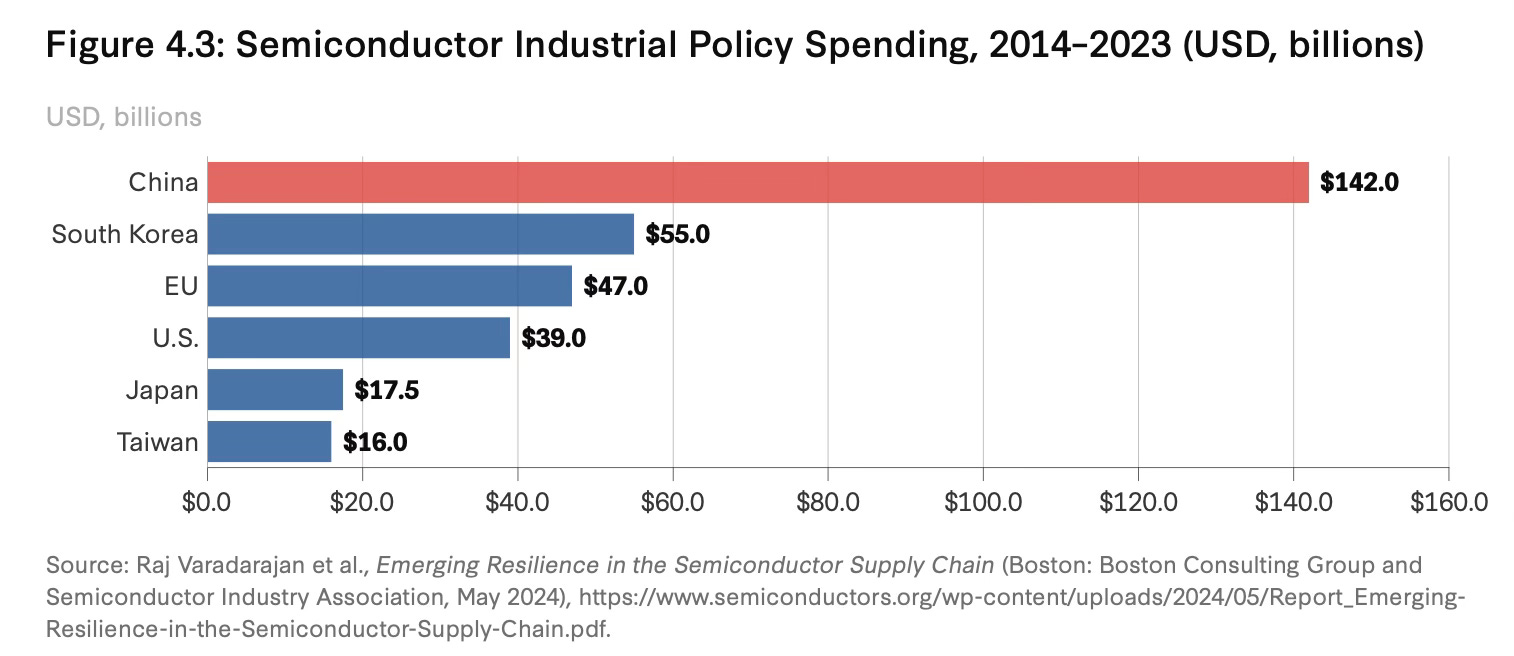

An area where China’s industrial policy has struggled is in the semiconductor industry. Despite outspending competitors by a large margin…

… Chinese firms have struggled to make headway in the value chain.

7. Finally, did China really eliminate poverty?

But while the country has eliminated poverty according to the World Bank’s $3 per day income standard, its definition of poverty is much lower than what the lender considers poverty in an upper-middle-income country such as China. By 2022, more than one in five people in China remained in poverty according to the World Bank’s definition for an upper middle-income country, set at $8.30 of income per day at 2021 prices.

No comments:

Post a Comment