1. Less discussed achievements of Abenomics, on corporate governance and capital market reforms that are major contributors to the country's economic resilience and equity market rebound.

“Reforms, new policy ideas, and civil society participation arrived in a heady rush (with Abe),” says Jamie Allen, who recently stepped down as secretary general of the Asian Corporate Governance Association (ACGA), a non-profit membership organisation driving effective corporate governance practices throughout Asia. He lists the Japan Stewardship Code of February 2014 (it has undergone two revisions since, in 2017 and in 2020); the Ito Review, in August 2014, which put return on equity (RoE) and corporate competitiveness on the map; the Corporate Governance Code of June 2015; a new third system of board governance, the Audit and Supervisory Committee Company, in 2015; the growth of sustainability reporting, strongly encouraged by the Financial Services Agency and the Ministry of Economy, Trade and Industry (METI); the emergence of new director-training institutes; an official set of Guidelines for Investor and Company Engagement in June 2018; new METI guidelines on group governance in June 2019. “Part of (Abe’s) government’s genius was to link CG reform not to risk reduction — as in most markets where governance is a corrective to excessive corporate risk taking — but to the long-term growth of companies and the revitalization of the underperforming Japanese economy,” avers Jamie...

Japan Inc was cash-heavy and that the financial indicators for Japanese companies trailed their European and United States counterparts. Years of poor capital allocation led to low RoE and low price to book (P/B)... The challenge was to link governance and financial performance, which the Tokyo Stock Exchange did through its focus on capital allocation... In March 2023, the exchange asked companies with a P/B ratio below 1 to disclose specific policies and initiatives to lift their value above it. While there may have been other financial indicators for companies to focus on, like return on capital equity or return on capital employed, the exchange narrowed in on P/B, which is now the prominent indicator. Since then, companies have begun focusing on capital efficiency. They have begun buybacks, mergers, spinoffs, unwinding crossholdings, and disposal of treasury stocks. All these are standard tools for any well-managed company but were shunned by Japanese enterprises.

As can be seen, these are not the kind of big bang ones that commentators harp on. Instead, they are the plumbing of corporate governance and equity market regulation. These less noticed reforms are the kinds of reforms that countries need.

2. India's trade story in numbers over the last two decades

The total merchandise exports figures went up from $63.84 billion in 2003-04 to $314.40 billion in 2013-14 (a rise of $250.62 billion), and now stand at $437.06 billion (a rise of $122.65 billion). So, while the merchandise exports grew almost four-fold during 2004-14, they grew by a little over a third during 2014-24. The services exports, however, grew from $46 billion in 2003-04 to $167 billion in 2013-14 (a rise of $123 billion) and to $340 billion in 2023-24 (a rise of $173 billion from 2013-14). Thus the rise in exports of services is more than the rise in the exports of merchandise in the past ten years... the share of petroleum products (Chapter 27) in our exports basket has stagnated around 20 per cent in the past ten years. The share of gem and jewellery (Chapter 71) exports (7.7 per cent) have halved during the past 20 years. The share of pharmaceuticals (Chapter 30) has doubled in 20 years but still is only around 5 per cent. The shares of chemicals (Chapters 28 and 29) at 5.2 per cent and farm, marine etc. products (Chapters 1 to 24) at 11.01 per cent have stagnated in 20 years. The share of cotton including yarn, fabrics etc. (Chapter 50) at 5.4 per cent has gone up from 3.9 per cent two decades back. The share of highly labour intensive readymade garments (Chapters 62 and 63) has gone down from 8 per cent to 3 per cent in 20 years. The success story is that of engineering products exports (Chapters 72 to 89) whose share in our total exports went up from 18.78 per cent in 2003-04 to 21.33 per cent in 2013-14, and now stands at 29.01 per cent. The share of other products has halved at 13.06 per cent in the past 20 years. From these figures, it is clear that engineering and petroleum products account for almost half of our exports.

3. Tamal Bandopadhyay has a very good column taking stock of the Insolvency and Bankruptcy Code.

A November 2023 report of rater Crisil Ltd pointed out that the recovery rates (as a percentage of admitted claims) have fallen from 43 per cent to 32 per cent between March 2019 and September 2023 even as the average resolution time has more than doubled, from 324 to 653 days. Realisation by financial creditors, as a percentage of liquidation value, has also dropped from 194 per cent to 168.5 per cent during this period... Since the IBC’s inception, 6,815 cases have been admitted to the NCLT, and 2,827 of these cases, that’s 41 per cent, are still undergoing the resolution process. The average resolution time has been rising and is now at a three-year high. Till December 2023, of the 6,815 cases, 891 had been resolved (against financial creditors’ claims of Rs 9.09 trillion, the realisation is Rs 3.1 trillion); 2,376 ended in liquidation (1,789 received no resolution plans and 587 got at best a couple of plans); and 721 in voluntary liquidation.

There are two problems that are not easily addressed. One, corporate India's innate instincts of using vexatious litigation to delay and subvert the process. Two, more importantly, the judiciary's willingness to foist themselves on these cases and leave them unheard for months (as the Videocon-Vedanta case pending in Supreme Court for more than two years shows).

4. Have long run neutral interest rates in the US gone higher?

The neutral rate, sometimes called “r*" or “r-star," can’t be directly observed, only inferred... Every quarter, Fed officials project the longer-run interest rate, which is, in effect, their estimate of neutral. Their median estimate declined from 4.25% in 2012 to 2.5% in 2019. After subtracting inflation of 2%, that yielded a real neutral rate of 0.5%... if inflation resumes its decline, questions about neutral would drive how much the Fed ultimately cuts rates. The Fed wants to “normalize policy, but ‘normalize’ to where?" said David Mericle, chief U.S. economist at Goldman Sachs. “They are not going to stay in the 5s, but normalization is not going to take them all the way to 2.5%. Where in the 3s or 4s they feel comfortable stopping is still up in the air." There are several factors cited for why neutral may be rising: soaring government deficits and strong investment driven by the green-energy transition and an artificial-intelligence-fueled frenzy for electricity-intensive data centers. Higher productivity from AI could also lift long-run growth and the neutral rate. Dallas Fed President Lorie Logan warned in a recent speech that interest rates may not be as restrictive as believed because of a higher neutral rate. “Failing to recognize a sustained move up in the neutral rate could lead to over-accommodative monetary policy," she said... Interest-rate futures suggest the fed-funds rate will stabilize around 4% in coming years.

5. Interesting that the growth of GST collections have lagged behind the growth rates of nominal GDP and Income Tax.

The tax cut failed to achieve its goals, as private investments have not taken off and the government has been forced to pump in massive amounts through capital expenditure to support the economy. At the same time, the immediate result of the tax cut is visible in collections, which is expected to be 3.2% of GDP in 2024-25, significantly less than the average mop-up a decade before the decision. As such, the government’s coffers are being filled more by personal tax collections than by corporate tax, raising questions about whether it is indeed pro-corporate.

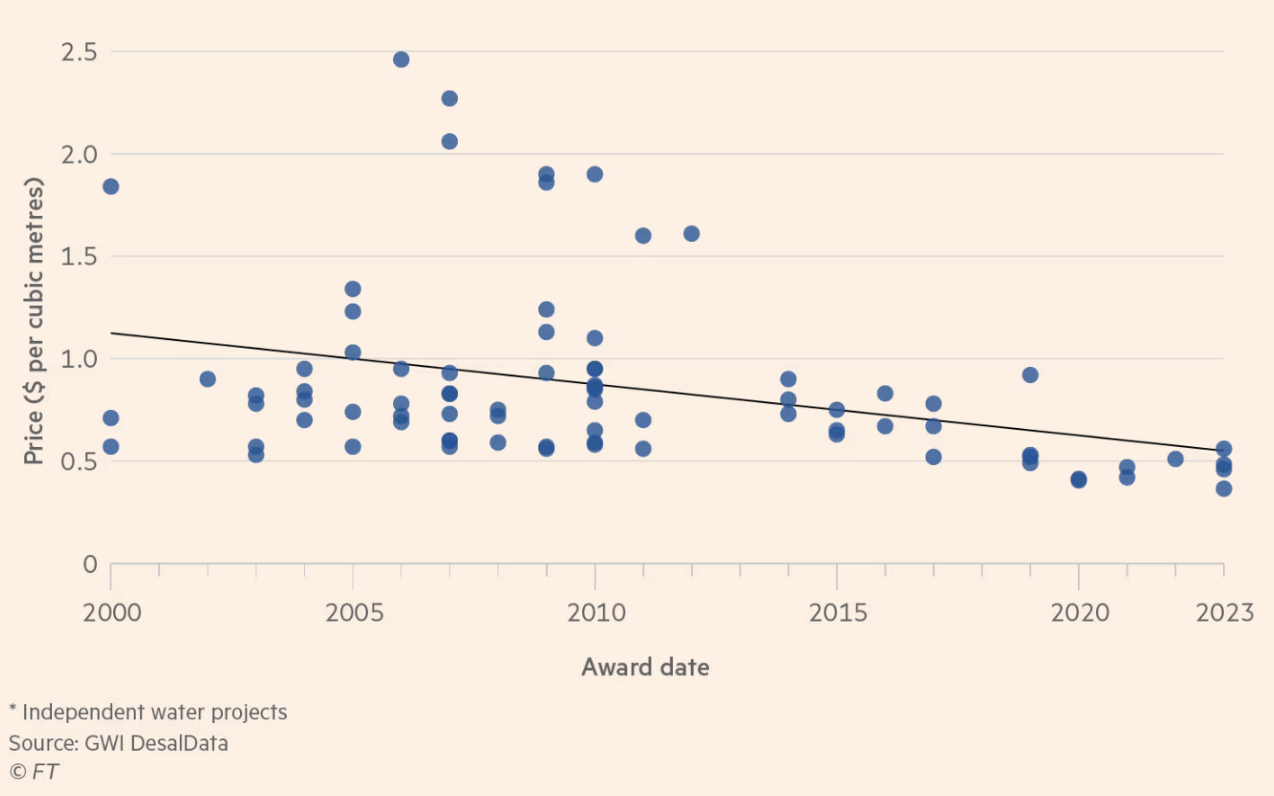

Older, thermal plants, which used heat to turn salt water into steam, delivered potable water at more than $3 per cubic metre. Since then, reverse osmosis technology — in which water is pushed through a membrane to remove salt, minerals and impurities — has taken over. Plants cost less to build — perhaps $400mn to purify 500,000 cubic metres per day, says Christopher Gasson of GWI. Including installation, a return on capital and operating costs, that translates to $0.30 per cubic metre of water. Newer plants also need less energy — 2.6KWh per cubic metre — and are increasingly powered by cheap solar plants. The cheapest plant in the world gets energy at $0.025/KWh, or $0.07 per cubic metre. Put that together and it explains how the Hassyan project in Dubai has promised desalinated water at just $0.37 per cubic metre. For reference, drinking water in London is priced at £1 per cubic metre. At this sort of level, desalination becomes more affordable for dry, coastal areas, not just in the Middle East but also in Egypt, Algeria and Morocco, which are all building new plants... the market for new plants is expected to grow by perhaps 8 per cent a year from now to 2030... early movers in the desalination sphere, including Saudi Arabia’s ACWA power, Spain’s Acciona and France’s Veolia, have a clear advantage in a competitive race.

A couple of months ago, my insurance company decided to raise the price of the yearly insurance premiums on our Brooklyn home by 51 per cent over three years, after more than doubling the estimated cost to rebuild should it burn to the ground or be washed away in a hurricane. While neither outcome seems likely for a limestone townhouse that sits on a hill more than a mile and a half away from the nearest flood zone, our insurer came up with an estimate that was more than double what the house would go for on the open market, making coverage both excessive and unaffordable... No one was willing to sell us a premium for the market value of our home and simultaneously prepared to write us a cheque for that value in case of total loss. We had two choices. Take out a policy with a handful of luxury insurers that would only sell us far greater coverage than we wanted for much more than we could afford. Or go with a budget policy offering roughly a third of what it would cost to buy a similar home in the case of a total loss — with the money only paid out if we chose to rebuild on site... we have any number of friends with similar homes who are paying wildly different prices for insurance. When I asked our broker how it was possible, or even legal, for a neighbour with the same insurer and the exact same house three doors away to pay a bit more than half our new quote, she told us that their premiums would very likely be raised next...How could there be so few options, so little transparency and such tolerance of inflation and inefficiency in a market as big as New York? Why was my home, which has never been seriously damaged by weather, being risk-assessed like something in a hurricane flood zone that is more than a mile and a half away? Why is the insurance industry so bad at pricing risk in a more precise way around the city, and indeed, much of the rest of the country?

Talk about free markets and their magic! This is a great example of how markets on their own fail to work, thereby necessitating regulation and government intervention to make them work effectively.

8. China economy imbalance facts of the week.

China’s investment to gross domestic product ratio, at more than 40 per cent last year, is one of the highest in the world, according to the IMF, while private consumption to GDP was about 39 per cent in 2023 compared to about 68 per cent in the US. With the property slowdown, more of this investment is pouring into manufacturing rather than household consumption, stimulating oversupply, western critics say. “China is responsible for one-third of global production but one-tenth of global demand, so there’s a clear mismatch,” US secretary of state Antony Blinken said in Beijing last week... China’s high national savings rates, which, at more than 47 per cent of GDP in 2022, are double the world average.

“The solution has always been a massive increase in investment,” Pettis says. But, he adds, with signs of over-investment now “everywhere”, from the property sector to overbuilt infrastructure, and debt to GDP at about 300 per cent, “you can see that investment can no longer be the solution”... Greater consumption would also necessarily mean reducing the role of manufacturing or investment in the economy. This could be done by unwinding China’s intricate system of subsidies to producers, which includes government infrastructure investment, access to cheap labour, land and other credit, says Pettis. But if that was done in a big bang fashion, the share of household consumption to GDP would increase while overall GDP would contract as manufacturers suffered. This was obviously not a politically preferable option for Xi. “They are locked into this system,” Pettis says.

9. Michael Pettis has a nice summary of the economic imbalance problem.

China’s structurally-high domestic saving rate is the result of a decades-long development strategy in which income is effectively transferred from households to subsidise the supply side of the economy — the production of goods and services. As a result of these transfers, growth in household income has long lagged behind productivity growth, leaving Chinese households unable to consume much of what they produce. Some of these subsidies are explicit but most are in the form of implicit and hidden transfers. These include directed credit, an undervalued currency, labour restrictions, weak social safety nets, and overinvestment in transportation infrastructure. These various policies automatically force up Chinese savings. By effectively exporting excess savings through the subsidy of the production of goods and services, China is able to externalise the resulting demand deficiency...China’s structurally-high domestic saving rate is the result of a decades-long development strategy in which income is effectively transferred from households to subsidise the supply side of the economy — the production of goods and services. As a result of these transfers, growth in household income has long lagged behind productivity growth, leaving Chinese households unable to consume much of what they produce. Some of these subsidies are explicit but most are in the form of implicit and hidden transfers. These include directed credit, an undervalued currency, labour restrictions, weak social safety nets, and overinvestment in transportation infrastructure. These various policies automatically force up Chinese savings. By effectively exporting excess savings through the subsidy of the production of goods and services, China is able to externalise the resulting demand deficiency.

10. The economic imbalance is also creating foreign policy tensions, and increasingly with other developing countries over cheap Chinese imports flooding their markets and destroying local industries.

Brazil’s industry ministry has launched a number of investigations into the alleged dumping of industrial products by China as Latin America’s largest economy reels from a wave of cheap imported goods. At the request of industry bodies, the ministry has in the past six months opened at least half a dozen probes on products ranging from metal sheets and pre-painted steel to chemicals and tyres... In addition to Brazil, China’s steel exports to Vietnam, Thailand, Malaysia and Indonesia have risen sharply in recent months... In Thailand, the government has accused Chinese companies of evading anti-dumping duties, while industry groups have warned of big losses from cheaper steel in the market. Vietnam’s government has launched investigations into dumping of wind towers and some steel products from China after complaints from the local industries. In August last year Mexico imposed tariffs of 5-25 per cent on imports of hundreds of goods from countries with which it does not have a free trade agreement, with China being one of the countries most affected.

11. A less discussed but one of the most remarkable achievements of energy policy, foreign policy (and the European Project), and infrastructure mobilisation was the success of Germany and Europe in replacing Russian natural gas imports in the aftermath of the Ukraine invasion. Germany took the lead in establishing LNG import terminals, Floating Storage Regasification Units (FSRU).

Wilhelmshaven was the first floating storage regasification unit (FSRU) to come online during the crisis but many more are in the works. Since Russia started cutting pipeline supplies to Europe in 2021, at least 17 liquefied natural gas (LNG) terminals have been planned or are under construction. LNG received by these FSRUs have helped replace all but 10 per cent of the gas supplies that previously came to the EU from Russia via pipelines, helping to reduce gas prices from record highs of over €300 per megawatt hour in August 2022 to near pre-crisis levels of around €30 per megawatt hour today. The energy crisis that Europeans feared two winters ago has not come to pass, thanks to a combination of unprecedented energy policy interventions, cuts in demand and good luck... The bloc is reliant on imports, either through pipelines or LNG shipments, for nearly 90 per cent of its supplies. Before the war, flows through four main pipelines from Russia accounted for around 40 per cent of the EU’s total supplies.

The higher prices being paid in Europe led LNG traders to prioritise deliveries to customers there over those in Asia, says Tom Marzec-Manser, head of gas analytics at ICIS. “Market signals were fundamental in allocating resources where it was needed.”

According to S&P Global, the penetration of all categories of hybrids has gone up from 9 per cent globally to 11 per cent in 2023 and is neck-and-neck with electric cars, though the latter are marginally ahead at 12 per cent, compared to 10 per cent in 2022. In the United States, hybrid sales in 2023 were 1.4 million and overtook electric cars, which sold 1.2 million. Globally, sales of plug-in hybrids grew faster, going up by 43 per cent in 2023, compared to a 28 per cent increase for electric cars.

Plug-in hybrids have two engines and the electric part has a much larger battery than in the regular hybrids. As the name suggests, plug-in hybrids require to be plugged into an electric socket to charge their battery. A regular hybrid gets its battery (smaller than in plug-ins) charged by the gasoline engine – the two complement each other -- and regenerative braking. Plug-in hybrids in China grew by 85 per cent in 2023, while electric vehicles grew by 70 per cent. In India, the popular hybrids, such as Toyota Hyryder and Maruti Suzuki’s Grand Vitara, do not require to be plugged in. The global trend towards hybrids is now visible in India, where they are being seen as an essential bridge to EV land... Electric cars attract a goods and services tax (GST) rate of 5 per cent. Hybrid cars attract 28 per cent GST, but the cess takes the total tax incidence to 43 per cent, unless it is a small car. ICE cars attract the same GST, but the cess takes the total to up to 50 per cent, varying according to the size of the body and engine.

This is an interesting cautionary tale from Norway about the promised emission benefits from EVs.

A study by Goehring & Rozencwajg, a natural resource investor, says despite the noise on Norway’s successful model for electrification of cars, the country forks out $4 billion on electric vehicle subsidies annually, as much as it does for building highways and maintaining public infrastructure, which has a big financial impact. Goehring & Rozencwajg also points out that despite all the action on the electric front in Norway — 20 per cent of all vehicles on the country’s roads and 80 per cent of new vehicles are electric — gasoline demand has gone down by only 4 per cent. That is because Norwegians are reluctant to give up their ICE cars even after they have bought an electric. Two-thirds of car owners in Norway have at least one ICE vehicle, and they continue to use it.

This effect is likely to be more pronounced in India.

13. Shyam Saran has a good oped on the ongoing situation in Gaza, which is clearly a genocide and a humanitarian disaster happening with the full knowledge of the UN and the international community and with so limited restraints on Israel. As Saran writes, the political survival of Netanyahu depends on the continuation and escalation of the situation in the region.

No comments:

Post a Comment