I have a co-written oped with Dr D Subbarao in Indian Express which calls on reinventing the IAS - transform itself so as to be able to lead the social transformation, lead the movement to discard the chalta hai attitude and embrace a badal sakta hai attitude.

Saturday, December 30, 2017

Thursday, December 28, 2017

Thoughts on NCLT and GST

The two biggest economic reform events in India in 2017 have been the roll-out of the Goods and Services Tax (GST) and the operationalisation of the Insolvency and Bankruptcy Code (IBC) through the National Company Law Tribunal (NCLT). A few observations on both.

On GST, the government faced two challenges. One, achieve consensus among States through protracted negotiations involving give-and-take so as to get the Parliamentary approval. Two, operationalise GST among millions of enterprises through a very intrusive IT solution, the vast majority of whom had never used such systems.

Both these meant that the best GST policy design and implementation plan was off the table. The challenge was to negotiate and ensure the most satisfactory second-best solution.

In a raucous democracy with high-stakes negotiations conducted in full public glare, that too in real-time and at frenetic pace to meet an imminent deadline, and given the confrontational collective attitudes and behaviours of all parties concerned, the government cannot be faulted for prioritising the achievement of consensus to get legislative nod over the purity of the GST design. After all, nothing about the design is set in stone.

The implementation plan, while largely a bureaucratic exercise, is critically dependent on the design. When the design features were subject to negotiations till the last minute, the challenge of incorporating the changes, and testing and validating them in very aggressive timelines becomes formidable. In any case, as countless examples of such massive project roll-outs show (recollect the chaotic roll-out of the Affordable Health Care Act insurance exchanges in the US), the challenge is not so much to get the best solution out, but to respond swiftly to emergent challenges and rectify them at the earliest. The initial few months of adoption chaos is par for the course.

A very active GST Council has been consistently refining the GST design elements since its roll-out. Given that these changes have to be incorporated into the IT system, almost in real-time, the implementation challenge looks even more daunting.

I am not well-placed to comment on the basic software design features (not related to emergent GST design changes), including ease of use for the largely IT illiterate users, of the GST solution or on the implementation processes. On the former, given that one of India's leading software companies has been in charge of its development for a long-enough time, I would be inclined to hold them responsible for such technical failings. On the latter, we need to examine the robustness of decision-making and process protocols, within the implementation Secretariat, as well as engagement with State Commercial Taxes departments. Was the commitments made for incorporation of GST Council decisions into the IT solution based on judgements that accounted for technical considerations? The bureaucracy cannot absolve itself off the blame on failings in these areas.

It would be very useful to study, compare, and learn from the decision-making protocols and processes associated with Aadhaar and GST, the two big IT solution roll-outs in the country's history.

More changes on the GST design features are on the anvil. In any case, a year-long iterative process and an implementation stabilisation period of 12 months is not at all unreasonable for such roll-outs. The verdict on the whether GST roll-out was done well or not will have to wait till then.

My initial reaction after the disastrous first case resolved under the IBC was one of dismay. But the government reacted swiftly to make changes to limit promoters gaming the resolution process and gaining control through the backdoor, including prohibiting promoters with non-performing loans for more than a year from bidding with resolution plans. One can argue that those changes could have been easily anticipated while framing the original regulation and that the response in terms of completely shutting out promoters, and not just "wilful defaulters", from even placing proposals before creditors is too restrictive.

On the former, I am sympathetic. But on the latter, I am not sure whether India's corporate eco-system is mature enough to responsibly engage with such flexibility and not abuse it. Any regulation is a trade-off involving flexibility that can be embraced or abused. A consistent feature of India's business landscape, across sectors, has been the egregious gaming of regulations, not so much at the margins but by large and responsible sections of corporate sector. In the circumstances, the standard bureaucratic response has been to err on the side of caution with restrictive regulations. The universal voucher reconciliation requirement or the Anti-Profiteering Agency in case of GST are examples. I feel that while reasonable people can agree or disagree on the specific set of restrictions in each case, it is important to appreciate the bureaucratic line of thinking in such cases.

As Livemint reports, the IBC appears to have already triggered some changes in the behaviours of errant promoters. That is welcome news. And I feel this deterrence taking root and shaping debtor attitudes, could become the biggest achievement of this reform. But on the substantive part of resolution, I foresee challenges ahead with the capacity of the system to execute the resolution process with fidelity and that of the market to absorb these transactions. I foresee challenges and struggles.

Tuesday, December 26, 2017

China facts of the day

The Economist has these figures on the Chinese appetite for lifts,

In 2000 some 40,000 new lifts were installed in the country. By 2016 the number was 600,000—almost three quarters of the 825,000 sold worldwide. China not only wanted more skyscrapers; it wanted taller ones. More than 100 buildings round the world are over 300 metres; almost all of them were built this century, and nearly half of them in China. The country is home to two-thirds of the 128 buildings over 200 metres completed in 2016. Other countries may content themselves with a few show-off pinnacles. China buys them by the dozen.

This is a fascinating (and disturbing) account of how Chinese digital companies are using personal data to score a person's social credit and offer the full spectrum of services covering the daily lives of Chinese. Sample this,

Alipay knows that at 1 pm on the afternoon of August 26, I rented an Ofo brand bike outside Shanghai’s former French Concession and rode north, parking it across from Jing’an Temple. It knows that at 1:24 pm I bought a snack in the mall next to the temple. It knows that afterward I got in a Didi car bound for a neighborhood to the northwest. It knows that at 3:11 pm I disembarked and entered a supermarket, and it knows (because Alibaba owns the supermarket, which accepts only Alipay at checkout) that at 3:36 pm I bought bananas, cheese, and crackers. It knows that I then got in a taxi, and that I arrived at my destination at 4:01 pm. It knows the identification number of the taxi that drove me there. It knows that at 4:19 pm I paid $8 for an Amazon delivery. For three sweet hours—one of which I spent in the swimming pool—it does not know my whereabouts. Then it knows that I rented another Ofo bike outside a hotel in central Shanghai, cycled 10 minutes, and at 7:11 pm parked it outside a popular restaurant. Because Ant Financial is a strategic investor in Ofo, Alipay might know the route I took.

Monday, December 25, 2017

The costs and benefits of transport aggregators

The beneficial effects of transport aggregators like Uber stand out, especially given the experience of consumers with business as usual taxi operators. They are much more convenient (lower wait times, ease of hailing, doorstep access etc) and far cheaper, which in turn induces more people to use such services.

Peter Cohen et al used granular surge pricing data to estimate that the overall consumer surplus generated by UberX service in the US in 2015 was $ 6.8 bn, and that each dollar of consumer spending generates about $1.6 in consumer surplus. Chungsang Tom Lam and Meng Liu used Uber and Lyft data for New York City to show that platform users gain 72 cents per dollar spent on these platforms, with 64% of the welfare gains coming from dynamic pricing.

But these studies are confined to the consumer side. How about the externalities - the impact on the urban transport eco-system? In particular, the costs of congestion are well documented, and how much does the addition of aggregators worsen it?

Peter Cohen et al used granular surge pricing data to estimate that the overall consumer surplus generated by UberX service in the US in 2015 was $ 6.8 bn, and that each dollar of consumer spending generates about $1.6 in consumer surplus. Chungsang Tom Lam and Meng Liu used Uber and Lyft data for New York City to show that platform users gain 72 cents per dollar spent on these platforms, with 64% of the welfare gains coming from dynamic pricing.

But these studies are confined to the consumer side. How about the externalities - the impact on the urban transport eco-system? In particular, the costs of congestion are well documented, and how much does the addition of aggregators worsen it?

CityLab points to a just released report by Bruce Schaller who found that during 2013-17 the number of taxi/aggregator vehicles in the Manhattan Central Business District (CBD) rose 59% on weekdays, and the number of such vehicles in the same area in late afternoon doubled to over 10,000 vehicles, and though taxi trips declined, total passenger trips rose 15%. He shows that aggregators contributed to a 36% increase in the amount of miles traveled by for-hire vehicles in the CBD, with lengthier trips and more "deadheading" (cars traveling without passengers). The result of all this was an 18-19% reduction in average traffic speeds.

Another study of Regina Clewlow and Gouri Shankar Mishra of University of California, Davis used data from comprehensive surveys in seven US cities in the 2014-16 period and came to similar conclusions. They found that ride-hailing services led to an average 6% reduction in use of bus services, and that 49% to 61% of ride -hailing trips would not have been made at all, or by walking, or biking or transit.

There is an even more damaging dynamic at play. Ridership of the New York mass transit system has been declining in recent years, on the back of poor service quality and safety concerns. Schaller's research suggests that aggregators are amplifying the decline, especially by drawing the more affluent passengers off trains into cars. As City Lab points out, this can trigger a death spiral - "fewer transit riders means less revenue and demand for improved transit" and a poor quality mass transit system used by the less well-off. This dynamic applies to cities in any developing or developed country.

In simple terms, the assessment of such innovations are about whether the private benefits from them are commensurate with their social costs. The former are amenable to being quantified and often rigorously too. In contrast, the latter are very difficult to capture and have long-drawn general equilibrium effects. The resultant propensity to under-estimate the latter causes an exaggeration of the benefits of such innovations.

In simple terms, the assessment of such innovations are about whether the private benefits from them are commensurate with their social costs. The former are amenable to being quantified and often rigorously too. In contrast, the latter are very difficult to capture and have long-drawn general equilibrium effects. The resultant propensity to under-estimate the latter causes an exaggeration of the benefits of such innovations.

More fundamentally, the biggest urban transportation challenge is to achieve the modal shift away from private vehicles to mass transit systems - increase the share of public transport and decrease the share of private vehicles. Therefore, any innovation or disruption that improves the efficiency and thereby increases the use of private vehicles, as transport aggregators like Uber appears to be doing, fails the first-order test of social benefit.

Sunday, December 24, 2017

Progress on tax base erosion

One of the big distortions in corporate finance, with increasing relevance in recent years, has been the tax deduction allowed on interest expenses. This has allowed companies in developed economies to lower their tax liabilities (and thereby boost profits) by leveraging the low interest rate regime and load up debt, even to the extent of using them to finance share buy-backs.

Fundamentally, the favourable treatment give to debt has not only led to erosion of the corporate tax base but has also encouraged corporate indebtedness. Most worryingly, it has encouraged resource misallocation towards speculative financial market activities that have in turn furthered the trend towards excessive financialization.

In this context, the G-20 and OECD's Base Erosion and Profit Shifting (BEPS) project to modernise international tax rules had in 2015 recommended that interest expense deductions be capped at a net interest/EBITDA ratio in the range of 10-30%, at the discretion of national governments. However, it allows for actual deductions in cases where the entire group’s ratio is higher than the fixed ratio, thereby acknowledging the supremacy of the principle of tax deduction on interest expenses.

Accordingly, the UK Government led the way by promulgating a Fixed Ratio Rule as part of its tax rules.

The Fixed Ratio Rule will limit the amount of net interest expense that a worldwide group can deduct against its taxable profits to 30% of its taxable earnings before interest, taxes, depreciation, and amortisation (EBITDA). A modified debt cap within the new rules will ensure the net interest deduction does not exceed the total net interest expense of the worldwide group. The Group Ratio Rule allows a ‘group ratio’ to be substituted for the 30% figure. The group ratio is based on the net interest expense to EBITDA ratio for the worldwide group based on its consolidated accounts.

One of the less discussed, maybe even partially redeeming, feature of the Trump administration's tax reform plan is the introduction of limit on the tax deduction on interest expense. The rules state that the deduction shall not exceed the sum of the tax payer's business interest income and 30% of the adjusted EBITDA. The provision becomes tighter by 2021 by making it 30% of EBIT. However, it allows for "carry forward of disallowed interest" which allows corporates to deduct the remaining interest expense in the following years, upto the fifth year after the expense is incurred.

Whatever the qualifications, these are undoubtedly positive developments to correct a serious distortion to corporate financing.

It is expected to hurt private equity firms which have specialised on leveraged buyouts to generate returns. It is estimated that in the US, nearly 70% of companies with debt more than five times EBITDA would be negatively affected.

Friday, December 22, 2017

Jonathan Haidt on the liberal outpouring

City Journal has a fascinating abstract of Jonathan Haidt's recent lecture at the Manhattan Institute. He talks about the wonder called a "fine-tuned liberal democracy",

When we look back at the ways our ancestors lived, there’s no getting around it: we are tribal primates. We are exquisitely designed and adapted by evolution for life in small societies with intense, animistic religion and violent intergroup conflict over territory. We love tribal living so much that we invented sports, fraternities, street gangs, fan clubs, and tattoos. Tribalism is in our hearts and minds... Here is the fine-tuned liberal democracy hypothesis: as tribal primates, human beings are unsuited for life in large, diverse secular democracies, unless you get certain settings finely adjusted to make possible the development of stable political life. This seems to be what the Founding Fathers believed. Jefferson, Madison, and the rest of those eighteenth-century deists clearly did think that designing a constitution was like designing a giant clock, a clock that might run forever if they chose the right springs and gears... They built in safeguards against runaway factionalism, such as the division of powers among the three branches, and an elaborate series of checks and balances. But they also knew that they had to train future generations of clock mechanics. They were creating a new kind of republic, which would demand far more maturity from its citizens than was needed in nations ruled by a king or other Leviathan.

He points to the rise of centrifugal forces and weakening of centripetal forces that hold together the social fabric. In particular, he points to the absence of a unifying enemy, divisive social media, growing immigration and attendant diversity, radicalisation of the Republican Party (fuelled by the likes of Fox TV), and the new identify politics of the Left.

On the last, he quotes Jonathan Rauch to define identity politics - a “political mobilization organized around group characteristics such as race, gender, and sexuality, as opposed to party, ideology, or pecuniary interest.” He gives the example of Martin Luther King's speech as an example of good kind of identity politics "because it framed our greatest moral failing as an opportunity for centripetal redemption". He contrasts this with a new version of identity politics taught in universities since the last five years - intersectionality.

The term and concept were presented in a 1989 essay by Kimberlé Crenshaw, a law professor at UCLA, who made the very reasonable point that a black woman’s experience in America is not captured by the summation of the black experience and the female experience. She analyzed a legal case in which black women were victims of discrimination at General Motors, even when the company could show that it hired plenty of blacks (in factory jobs dominated by men), and it hired plenty of women (in clerical jobs dominated by whites). So even though GM was found not guilty of discriminating against blacks or women, it ended up hiring hardly any black women. This is an excellent argument. What academic could oppose the claim that when analyzing a complex system, we must look at interaction effects, not just main effects?

He describes its consequences,

But what happens when young people study intersectionality? In some majors, it’s woven into many courses. Students memorize diagrams showing matrices of privilege and oppression. It’s not just white privilege causing black oppression, and male privilege causing female oppression; its heterosexual vs. LGBTQ, able-bodied vs. disabled; young vs. old, attractive vs. unattractive, even fertile vs. infertile. Anything that a group has that is good or valued is seen as a kind of privilege, which causes a kind of oppression in those who don’t have it. A funny thing happens when you take young human beings, whose minds evolved for tribal warfare and us/them thinking, and you fill those minds full of binary dimensions. You tell them that one side of each binary is good and the other is bad. You turn on their ancient tribal circuits, preparing them for battle. Many students find it thrilling; it floods them with a sense of meaning and purpose.

And here’s the strategically brilliant move made by intersectionality: all of the binary dimensions of oppression are said to be interlocking and overlapping. America is said to be one giant matrix of oppression, and its victims cannot fight their battles separately. They must all come together to fight their common enemy, the group that sits at the top of the pyramid of oppression: the straight, white, cis-gendered, able-bodied Christian or Jewish or possibly atheist male. This is why a perceived slight against one victim group calls forth protest from all victim groups. This is why so many campus groups now align against Israel. Intersectionality is like NATO for social-justice activists.This means that on any campus where intersectionality thrives, conflict will be eternal, because no campus can eliminate all offense, all microaggressions, and all misunderstandings. This is why the use of shout-downs, intimidation, and even violence in response to words and ideas is most common at our most progressive universities, in the most progressive regions of the country. It’s schools such as Yale, Brown, and Middlebury in New England, and U.C. Berkeley, Evergreen, and Reed on the West Coast. Are those the places where oppression is worst, or are they the places where this new way of thinking is most widespread?

Let me remind you of the educational vision of the Founders, by way of E.D. Hirsch: “The American experiment . . . is a thoroughly artificial device designed to counterbalance the natural impulses of group suspicions and hatreds . . . This vast, artificial, trans-tribal construct is what our Founders aimed to achieve.” Intersectionality aims for the exact opposite: an inflaming of tribal suspicions and hatreds, in order to stimulate anger and activism in students, in order to recruit them as fighters for the political mission of the professor. The identity politics taught on campus today is entirely different from that of Martin Luther King. It rejects America and American values. It does not speak of forgiveness or reconciliation. It is a massive centrifugal force, which is now seeping down into high schools, especially progressive private schools.

It is this dynamics of intersectionality that has made the liberal opinion leaders advocate simplistic positions in favour of free-trade, globalisation, deregulation, immigration, excessive individualism and individual rights, and so on. The backlash is for everyone to see.

Tuesday, December 19, 2017

The challenge with job creation in India

India's labour market problem is not one of literal unemployment, but of productive employment. Alternatively, we have a problem of disguised employment - employee claims education and skills beyond the requirements of their job. In more practical terms, it is one of sorely deficient well-paying formal sector jobs.

Let us be clear. In a large economy like India, where the vast majority of workforce is rural and informal, some form or other of bare subsistence employment is always likely to be available. The real problem is availability of (formal sector) jobs appropriate for a skilled workforce, much less the ones that meet their aspirations.

So, for example, R Gopalan and MC Singhi are barking up the wrong tree. They quote Labour Bureau data from 200910 to 2015-16 to claim that "India's jobless growth is a myth". But they do nothing to refute the central problem. In fact, unwittingly, they end up substantiating it,

The Labour Bureau survey (2015-16) has categorized workers according to their monthly income levels. Most of the workers, 84% of all, whether self-employed, regular wage earners, contract workers or casual workers, were getting an income of less than Rs10,000 per month (Figure 1). Regular wage earners or salaried-class workers were better off, with 57% having a monthly income of Rs10,000 or less. Finally, 96.3% of casual workers, including those who were employed for public works, and 85% of self-employed persons had a monthly income of Rs10,000 or less. Enough work was also not available for nearly 40% of the workers; they were being employed for only a part of the year. In terms of decent, productive and well-paid jobs, considerable gaps continued to persist.

Given that nearly 90% of the workforce is employed in the informal sector, predominantly with less than regular wage incomes and more likely as casual workers, it is fair to say that the overwhelming majority of new entrants get an income less than Rs 10000. In fact, the vast majority would have monthly incomes far less than Rs 10000. Now, how much can Rs 10000 get you if you are a migrant, even if single though with a commitment to save something to send back home, in a big city? Not to speak of the deductions that come along with formality. Manish Sabharwal has been a constant chronicler of all these. So clearly we have a problem of inadequate supply of productive, and therefore well-paying, jobs.

Gopalan and Singhi end up with suggestions that are unlikely to be relevant or actionable, much less effective,

It is necessary, then, to evolve strategies to create supplementary opportunities for the self-employed, improve the female labour force participation rate, increase the ratio of female to male job seekers, and reduce interstate differences.

No quibbles with the need to improve female labour force participation rate, but this is a second order challenge to more fundamental structural failings. But the suggestion to create supplementary opportunities for self-employed may be exactly the wrong path to follow as a job creation strategy (though maybe appropriate as a poverty alleviation strategy).

As I have blogged earlier, India's problem is not too little entrepreneurship, but too much and mostly of the wrong kind. India's labour market is characterised by unproductive, informal, self-employment based subsistence entrepreneurship. Instead there should be a much greater share of workers employed in productive, formal sector jobs.

In fact, India needs more of the dynamic entrepreneurs, of the type that creates productive jobs. As Ejaz Ghani and Co have shown, the only two reliable predictors of such entrepreneurship are infrastructure and human resource quality. In simple terms, they show that dynamic entrepreneurship require educated entrepreneurs who start formal enterprises. In contrast, the vast majority of the MUDRA entrepreneurs are more likely inadequately (or poorly) educated, creating more of informal subsistence entrepreneurship.

The quality of human resource development goes beyond entrepreneurs and has relevance for the workers themselves. For example, while the new worker may claim education and skills appropriate for productive jobs, those skills may be of a quality inadequate to meet the requirements for productive employers. All this takes us to the issue of poor quality of education, at all levels, and the resultant supply of "unemployable" graduates and post-graduates, who make both poor workers and poor entrepreneurs.

On the demand-side of the labour market, there is the problem associated with the the larger existing formal sector enterprises, where job creation is constrained by the continuing weakness in capex spending.

In conclusion, we really do have a jobs problem. More specifically very limited supply of formal and productive jobs. Most worryingly, the mainstream debates confuse poverty alleviation strategies with job creation strategies.

Update 1 (14.01.2018)

Mahesh Vyas refutes Messers Gopalan and Singhi here.

Update 1 (14.01.2018)

Mahesh Vyas refutes Messers Gopalan and Singhi here.

Monday, December 11, 2017

Eco-system as a constraint on outcomes-based policies

I have blogged earlier here about the under-appreciated difficulties with targeting outcomes. Apart from the three challenges raised in that post, there is another equally important challenge. This concerns ecosystem constraints.

It is commonly assumed that the existing ecosystem can be disciplined to achieve the desired outcomes through efficiency improvements, by getting human and physical capital to work more and better. What if this is not at all true?

This post gives three examples of how outputs or outcomes-focused technology or process interventions disrupted entrenched equilibriums and raised difficult administrative challenges.

Consider school education. We have no clear idea of how much of learning outcomes realisation is a function of early childhood education, classroom instruction, remedial support in classroom, peer-engagement, off-school hours engagement at home, and the grade-appropriate competency levels themselves. What are their relative weights? How do those vary across socio-cultural contexts? What if the competency standards are too ambitious? Or what if home engagement is critical?

Consider primary health care. This study found that doctors spend limited time and asked very few questions (as against what the medical protocol dictates) when treating patients. And it is pervasive across developing world, though nowhere as bad as in India. While unambiguously accepting the larger point about apathy and incompetence, it is also important to highlight the plumbing reality - the Out Patient load, when doctor is available, in PHCs can be far higher than what any systems can deal. Once this becomes the norm, a newly recruited doctor, over a few years, deeply internalise the challenge and forms a response that instead of treating the patient only tries to get done with the long-que of patients before lunch! Just imagine a GP in UK dealing with 30 patients turning up over a two-hour window with just one nurse for assistance.

Nowhere is this more relevant than with state capacity. It is unrealistic to expect public systems as they exist now to deliver sectoral outcomes in scale and anywhere close to the defined benchmarks. Right now, these systems are entrapped in a low-level equilibrium of low human and physical resource allocations, unfavourable socio-economic conditions, and tolerance for and expectations of sub-par outcomes. Even the most incentive compatible financing strategy cannot be expected to have anything other than marginal effect on the system.

Fundamentally, this should have been simple. Development is hard. The resolution of complex problems demand multi-dimensional policies that directly and proactively address deep structural failings, and persistent effort in their implementation. So to expect outcomes-targeting to magically deliver the result is plain naive.

But that we still fall prey to the lure of such apparently neat and simple solutions can be blamed on our psychological urges. We want to do something quickly about these complex problems. We find the logic of outcomes-based policies irresistible. So we seek refuge in them.

But they will not work!

Monday, December 4, 2017

The alternative assets universe and India

The latest quarterly update of infrastructure funds from Preqin shows that the total dry powder held by unlisted infrastructure funds has reached a record high of $154bn as at September 2017. Most of this is routed to N America and Europe, with just $20 bn earmarked for all of Asia, including China and Japan.

As regards India, the total dry powder currently available aimed at investing in India is just $3 bn. The vast majority of this comes from overseas funds, rather than domestic fund raising. In fact, India forms just 7% of the $65 bn unlisted infrastructure assets in the Asia-Pacific region.

As to the entire alternative investment funds industry - private equity, venture capital, real estate, infrastructure, private debt etc - the total assets under management (AUM) as of December 2016 was $598 bn. India's share was $42 bn, of which $13.5 bn was the dry powder.

The major share of the AUM in India went into PE/VC funds. The PE sector has been boosted by the pick-up in exits, $10 bn in each of 2015 and 2016, and $7 bn to date this year.

While $7 bn of the $23.6 bn in the PE/VC sector is dry-powder available for deployment, a very small proportion of this is currently earmarked for buyouts. This allocation is contrast to elsewhere, including in Asia, where buyouts form the dominant share.

Two observations

1. The government has planned infrastructure investments in the range of $700-1000 bn over the coming five years. It is estimated that a significant share of the investments will come from foreign investors. But, as these numbers show, we would be happy if even 10% of these investments come from abroad. Therefore, expectations of the National Infrastructure Investment Fund (NIIF) being able to leverage its $3bn corpus ten-fold etc are simply unrealistic.

One approach to attracting more infrastructure funds is by selling commissioned assets where revenue streams are predictable. Entities like NTPC and NHAI should consider divesting certain existing assets both attract infrastructure funds as well as mobilise resources to finance newer projects.

One approach to attracting more infrastructure funds is by selling commissioned assets where revenue streams are predictable. Entities like NTPC and NHAI should consider divesting certain existing assets both attract infrastructure funds as well as mobilise resources to finance newer projects.

2. The new Bankruptcy Code and the resultant wave of distressed assets sales promises to flood the Indian market with massive buyout opportunities. The domestic market may not be deep enough to absorb anything beyond the first few sales. Foreign buyout funds would be essential for the fair price discovery required to make these sales sustainable, both commercially (for banks) and politically.

While the currently earmarked amounts India-focused buyout funds is negligible, this distressed asset sales present a great opportunity to attract a big volume of such funds and deepen India's alternative assets market. This may require more strategic approaches to some of these sales, including bundling assets into groups so as to make it large enough to be commercially attractive.

As to the distressed assets sales themselves, two articles in Mint point to the challenges that are likely to be faced going ahead. One concerns the 26 GW of thermal power assets without any power purchase agreements, which makes them risky even after write-downs and restructuring. In these cases, as I have argued earlier, it may have to fall on NTPC to become a buyer of last resort.

The other one relates to steel sector, where the problems are worse still and massive haircuts may be necessary. And, unlike with power assets, it may be very bad idea of have an inefficient SAIL buy them up. In this case, strategic sales by bundling assets assume relevance.

As to the distressed assets sales themselves, two articles in Mint point to the challenges that are likely to be faced going ahead. One concerns the 26 GW of thermal power assets without any power purchase agreements, which makes them risky even after write-downs and restructuring. In these cases, as I have argued earlier, it may have to fall on NTPC to become a buyer of last resort.

The other one relates to steel sector, where the problems are worse still and massive haircuts may be necessary. And, unlike with power assets, it may be very bad idea of have an inefficient SAIL buy them up. In this case, strategic sales by bundling assets assume relevance.

Tuesday, November 28, 2017

The year of bubbles in a snapshot

As one more year of monetary accommodation draws to a close, John Mauldin has these bubble facts

- A painting (which may be fake) sold for $450 million.

- Bitcoin (which may be worthless) soared nearly 700% from $952 to ~$8000.

- The Bank of Japan and the European Central Bank bought $2 trillion of assets.

- Global debt rose above $225 trillion to more than 324% of global GDP.

- US corporations sold a record $1.75 trillion in bonds.

- European high-yield bonds traded at a yield under 2%.

- Argentina, a serial defaulter, sold 100-year bonds in an oversubscribed offer.

- Illinois, hopelessly insolvent, sold 3.75% bonds to bondholders fighting for allocations.

- Global stock market capitalization skyrocketed by $15 trillion to over $85 trillion and a record 113% of global GDP.

- The market cap of the FANGs increased by more than $1 trillion.

- S&P 500 volatility dropped to 50-year lows and Treasury volatility to 30-year lows.

- Money-losing Tesla Inc. sold 5% bonds with no covenants as it burned $4+ billion in cash and produced very few cars.

If all this is not enough to take the punch-bowl away, then we can be rest assured that real-world monetary policy will always be asymmetric - loosen when faced with economic weakness to ease conditions and stoke demand, and refrain from tightening when overheating for fear of bringing the house down. Prefix it with Greenspan or not, one cannot but not walk away with the feeling that central bank actions in recent years have released a moral hazard named Central Bank Put!

Friday, November 24, 2017

Managing organisations - the importance of trust and delegation

I have a simple hypothesis about managing organisations. There are several complex dynamics at play, but there is one non-negotiable attribute - trust and delegation. A good leader is one who has the instinct to trust the right people, the confidence to delegate, and the restraint to step in only when required.

Consider the example of a District Collector in an Indian district. He is responsible for the administration of all development and regulatory activities in the jurisdiction. Take the example of sanctioning and stage-wise approval of the release of payments for engineering works - school/hospital buildings, roads, irrigation structures and so on. In all these cases, the Collector has to exercise some judgement to make decisions.

How does he know that all the 125 school buildings or 12 roads or 245 irrigation structures to be sanctioned this calendar year are the most appropriate ones? How can he be sure that the first instalment for the school building is being released only after the foundation stone has been completed? How can he be assured that the building or the road has been completed with good quality before sanctioning the release of the final payment?

For sure, there is administrative guidance by way of formal delegation of powers, which though can be changed by following the due process, that define the sanctioning and payment release powers of officials at each level. But most often than not, even these are a very narrow and conservative delegation, more appropriate for a time when government was limited - there were limited number of such schools to be sanctioned and limited scope and sectors of administration. The modern administration and its scope demands further delegation.

How do different Collectors respond? Some go by the official playbook. This leaves them with the dilemma of approving something which they have not physically seen, but based on what is on record. And given that what is on record can be aggregates, incomplete, irrelevant, misleading, or even plain incorrect, as is most often the case, the Collector has to exercise judgement calls. And the numbers of such files are huge in most districts.

Faced with this dilemma, some, known as query masters, raise questions and insist on clarifications, which in turn cascades into more questions and so on. Some others, inspection masters, demand personal inspections, which can never be completed for even one round of approvals given the sheer volume of work. And even when they inspect, they are unlikely to be satisfied, since the contractors are likely smarter and the Collector likely does not have the professional competence to make conclusive assessments of malafide and fraud. The approval gets delayed and the work drags on. Cost escalates and contractors abscond, forcing re-tenders which come with multiples of the original cost.

Then there are the corrupt, who approve everything as it comes, since the transaction has already materialised as planned before the file reaches their table. And they rationalise, and rightly so, with the argument that they are only sanctioning some thing as per the formal delegation of authority and they cannot be held accountable if the facts are contrary.

There are also a few who decide to revisit the delegation of powers and either directly or indirectly delegate their own approval powers. The extent of delegation varies from context to context, and is made on the person's best judgement of what is the most appropriate level - a trade-off of perfection and efficiency. They manage to get the right people in some of the more important places, trust them, and delegate authority. They struggle hard initially to put in place appropriate safeguards to mitigate the associated risks. They create monitoring mechanisms that rely on credible and easily collectible direct or proxy indicators and open alternative channels of feedback that helps them keep abreast of the field situation. They also put in place independent quality assurance mechanisms.

The very significant amount of time saved by way of delegation helps them focus on maintaining the fidelity and rigour of these feedback and monitoring channels. It gives them more personal time. By ensuring that 100 of the 125 buildings are completed on time, even at the risk of poor quality in 25 schools, the fiscal gains too are very large.

The benefits go way beyond such personal or financial gains. Such delegation, and the attendant signal of trust, empowers the next line of command. Those being trusted are now likely to feel morally inclined to not let down their leader. They assume greater responsibility. Within a reasonable period of time, a spirit of collective ownership can infuse the entire organisation.

For sure, the last category of Collectors run the risk of the occasional blow-ups - the road that develops pot-holes a month after its inauguration, the sunk flooring of the new building, the irrigation canal gate that develops leaks in the first week, and so on. And such risks materialise in a few cases. It does not help that the vested interests gang up to show-up and amplify the smallest omissions. The challenge is not to eliminate such risks. No matter what anyone does, the corrupt and mischievous will always find their way to retain some rent-seeking channels. The challenge is to minimise such eventualities by deterring them through very good feedback systems, practical but credible monitoring systems, and by making deviance very costly.

This framework of analysis is equally applicable to every organisation - big and small, general and specialised, public and private - and all levels of decision-making.

We all like to be in control of things. We prefer full information and logical neatness when taking decisions. We hate ambiguity and prefer certainty while making decisions. This is the human in all of us.

I will argue that this ability to trust and delegate has little to do with being logical or smart. It is almost completely a behavioural attribute, though one which can be inculcated through conscious but painstaking practice. Giving up anything, much less power, is not something we are likely to be comfortable with. All of us start this way. But the realisation of this very insight and training ourselves to internalise it can be the epiphany for those few who manage to break away. It also helps to be confident of your own abilities. Confidence helps trust people and the trust, in turn, enables delegation.

Slice and dice, analyse and dissect any organisation which ever way you want, there are decisions to be made. Such decisions involve judgement calls that demand a trade-off between exactitude, with all its attendant delays and other perils, and efficiency, with all its potential for blow-ups.

Deregulation in governments is the most classic example of these dynamics at play. It ranges from the Collector's proclivity to demand more information and inspections before approving payment releases to the Goods and Services Tax (GST) Council's insistence for voucher reconciliation before tax credits are reimbursed to the reluctance of the University Grants Commission (UGC) or the Medical Council of India (MCI) to adopt more light-touch regulations. In some ways, it is also lazy administration or management, since it avoids the need to be wiser and to work hard to manage complex environments.

Daniel Kahneman talks about decision making involving System I or System II. The former is instinctive and the latter is reflective.

Over a life-time as we gather experience, we need to train the System I to drive the vast majority of decision-making. For sure, we can train our instincts using heuristics like what some District Collectors do. We can make the System I internalise the insights of System II, but leave the decision making with System I. A good tennis player's ground strokes are System I at work.

There are always some of the complex decisions, those with stakes which are higher, where System II may have to dominate. The same good tennis player uses System II to strategise a Plan B when faced with being two sets behind or when the opponent is blazing all guns and hitting the lines consistently.

We need to make judgement calls over what demands the attention of System I and what System II.

The Collector, or any other decision-maker, should train him(her)self that all bar critical administrative decisions respond to System I impulses. This requires trusting and delegation. This is, most often, the difference between getting stuff done and not. But it is, at a deep enough level, our choice to use the System I or System II as our default decision-making strategy.

Wednesday, November 22, 2017

More thoughts on Indian agriculture

I had written sometime back about the corrosive effects of loan waivers arguing that such "assault on incentives" are far more pernicious than giving electoral freebies.

India has witnessed and explosion of farm loan waivers in the last year or so as part of electoral politics in states which held assembly elections. And with the next election season on, the trend continues unabated.

But this issue cannot be seen in isolation. It has to be seen as part of the entire agriculture eco-system in India.

Actually agriculture is a pretty complex system and conventional market solutions have been shown to not work. Gluts and shortages are inevitable - bad weather is a risk; good prices lead to excess cultivation next year and resultant drops, and vice-versa; global supply shocks and resultant price fluctuations are always round the corner; poor storage and other forward linkages make farm sales the only option etc. Pain and suffering follows.

Developed countries, over decades, have sought to address this problem through less distorting approaches - mainly crop insurance and/or direct payments. It helped that they have good irrigation systems, farms are bigger, forward linkages are better, credit access simple, and markets are functional.

We have none of the positive conditions, and crop insurance and direct payments are both very expensive and run into problems of effective administration.

But we have this smorgasbord of inefficient and distorting things - subsidised crop loans and their recurrent waivers; procurement and MSP (which feeds into the PDS); fertiliser subsidy; free farm power; agriculture IT exemption; minor irrigation programs like PMKSY etc. Worse still, each one has generated its set of powerful entrenched interests, which reflexively gang up as a vocal electoral constituency whenever they are threatened. Making matters complex, it cannot also be denied that each one of these, in their very sub-optimal ways, contributes to mitigating, even if partially, the fundamental problem, and the resultant pain and suffering.

So we have a very bad self-reinforcing and perpetuating equilibrium. A chakravyuha, from which exits appear very daunting.

I have not come across anything satisfactory as a path out of this. Except the gradual process of development - build irrigation systems, transition people out of agriculture, consolidate farms, let linkages and markets develop etc - and the gradual introduction of things like crop insurance. In this dismal environment, doubling farm incomes may well be the government's most over-optimistic promise yet.

There may be just a few avenues to manoeuvre. Given that the crop insurance scheme is one of the government's bigger initiatives, and one of the most progressive (as well as efficient), I think it should actually spend more energies and resources on it. As experience from across the world shows, premium support will always entail big subsidies and this may be worth paying. Can the government also think of phasing out some of these other subsidies and phasing in more of crop-insurance support? For example, it could encourage states which are willing to do farm power metering and a low agricultural tariff (to start with), to be provided a much higher premium support subsidy.

But alternatively, there is some merit in reframing both the MSP and crop-insurance. Instead of government procurement (except, and only to the extent required, for wheat and paddy), the MSP should be announced and farmers should be given the differential between the MSP and the market price, as is being tried out now in Madhya Pradesh for onions.

Similarly, there is a compelling case to dispensing with crop insurance, with all its transaction costs and reimbursement delays, and making direct payments when the crop fails. After all, if the identification of farmers affected has to be done even with insurance and a major share of the premium will have to be subsidised to make the insurance payouts meaningful enough, then the supposed advantages of an insurance model compared to direct payments looks questionable.

Update 1 (01.01.2018)

This article has the description of the Madhya Pradesh's Bhavantar Bhugtan Yojana.

But alternatively, there is some merit in reframing both the MSP and crop-insurance. Instead of government procurement (except, and only to the extent required, for wheat and paddy), the MSP should be announced and farmers should be given the differential between the MSP and the market price, as is being tried out now in Madhya Pradesh for onions.

Similarly, there is a compelling case to dispensing with crop insurance, with all its transaction costs and reimbursement delays, and making direct payments when the crop fails. After all, if the identification of farmers affected has to be done even with insurance and a major share of the premium will have to be subsidised to make the insurance payouts meaningful enough, then the supposed advantages of an insurance model compared to direct payments looks questionable.

Update 1 (01.01.2018)

This article has the description of the Madhya Pradesh's Bhavantar Bhugtan Yojana.

Sunday, November 19, 2017

A primer on the rise of populism and a way forward

There are several narratives surrounding the rise of populism and events like the election of Trump and Brexit. I have written about it here, here, and here. This is an attempt at articulating the narrative based on news stories from the week.

1. What is happening? The remarkable post-war economic, social, and political stability across developed societies, especially in the US, was built on an underlying consensus on certain values. This consensus revolved around the commitment to the values of free-market capitalism, liberal social order, and democracy. Political positions converged to reflect this consensus.

But as the fascinating graphic below shows, this consensus has been breaking down and the median liberal and conservative positions in the US has diverged significantly over the past decade.

2. Why is it happening? But this consensus was accompanied by a less benign bipartisan elite convergence (more of it latter) which effectively ended up capturing the economic and political establishment.

The rapid and fairly inclusive economic progress achieved in the period helped underpin this consensus and paper over fissures that were developing due to forces like trade liberalisation, globalisation, de-unionisation, and skill-biased technological changes. But once growth started slowing, for a variety of factors, these fissures started to show up.

But mainstream political parties, captives as they had become of elite interests, failed to see the breakdown in social consensus. The liberal elites too became caught up in their rhetoric.

Nothing has been more emblematic of this isolation of elites from the electorate than the staggering levels of economic inequality, which has been widening at a rapid pace since the millennium. As the graphic below shows, in the US, the share of national income going to the top 1% has nearly doubled from 11% in 1980 to 20% in 2014.

While trade, technology, de-unionisation, immigration, business concentration etc played a role, Jonathan Rothwell argues,

Almost all of the growth in top American earners has come from just three economic sectors: professional services, finance and insurance, and health care, groups that tend to benefit from regulatory barriers that shelter them from competition. The groups that have contributed the most people to the 1 percent since 1980 are: physicians; executives, managers, sales supervisors, and analysts working in the financial sectors; and professional and legal service industry executives, managers, lawyers, consultants and sales representatives. Without changes in these largely domestic services industries — finance, health care, the law — the United States would look like Canada or Germany in terms of its top income shares.

He also points to how the elite capture of institutions that sets the rules of the game have contributed to an elite premium and rapid widening of inequality,

The United States also stands out in terms of how much money its elite professionals earn relative to the median worker. Workers at the 90th percentile of the income distribution for professionals make 3.5 times the earnings of the typical (median) worker in all occupations in the United States. Only Mexico and Israel, which have very high inequality, compensate professionals so disproportionately. In Switzerland, the Netherlands, Finland and Denmark, the ratio is about 2 to 1. This ratio, the elite professions premium, is very highly correlated with income inequality across countries.

Others are noticing these trends. A new book, “The Captured Economy” by Brink Lindsey and Steven Teles, argues that regressive regulations — laws that benefit the rich — are a primary cause of the extraordinary income gains among elite professionals and financial managers in the United States and of a reduction in growth. This year, the Brookings Institution’s Richard Reeves wrote a book about how people in the upper middle class have shaped both legal and cultural norms to their advantage. From different perspectives, Joseph Stiglitz, Robert Reich and Luigi Zingales have also written extensively about how the political power of elites has undermined markets.

Problems cited by these analysts include subsidies for the financial sector’s risk-taking; overprotection of software and pharmaceutical patents; the escalation of land-use controls that drive up rents in desirable metropolitan areas; favoritism toward market incumbents via state occupational licensing regulations (for example, associations representing lawyers, doctors and dentists that block efforts allowing paraprofessionals to provide routine services at a lower price without their supervision).

Economic geography too has played a role. Richard Florida has documented the increasing trend of concentration of poverty, both across cities and within them. Defining concentrated poverty as neighbourhoods where 40% or more residents are below the US poverty line, he writes,

The number of people living in concentrated poverty has grown staggeringly since 2000, nearly doubling from 7.2 million in 2000 to 13.8 million people by 2013—the highest figure ever recorded. This is a troubling reversal of previous trends, particularly of the previous decade of 1990 to 2000, where Jargowsky’s own research found that concentrated poverty declined. Concentrated poverty also overlaps with race in deeply distressing ways. One in four black Americans and one in six Hispanic Americans live in high-poverty neighborhoods, compared to just one in thirteen of their white counterparts.

Similar concentrations can also explain Brexit. Sarah O' Connor has this fantastic essay on the declining fortunes of the once popular English seaside tourist resort town of Blackpool. The article shows how Blackpool has become "a net importer of ill health, unemployment, and precarious labour and a net exporter of good health and skilled labour". It talks about the "Shit Life Syndrome" that has contributed to a self-fulfilling downward spiral of despair and misery.

And this manifests in social problems that affect the current generation...

And this manifests in social problems that affect the current generation...

... and the future generation too.

... and the future generation too.

See this commentary on the article by Ananth. The opioid epidemic that is sweeping large parts of the US mirrors Blackpool's problems across the Atlantic. And it affects all the similar groups of people.

See this commentary on the article by Ananth. The opioid epidemic that is sweeping large parts of the US mirrors Blackpool's problems across the Atlantic. And it affects all the similar groups of people.

3. So what can be done? The always incisive Dani Rodrik describes the political situation as a pooling equilibrium, recounts its consequences, and points to a solution to wean the electorate away from populist demagogues,

3. So what can be done? The always incisive Dani Rodrik describes the political situation as a pooling equilibrium, recounts its consequences, and points to a solution to wean the electorate away from populist demagogues,

Conventional and reformist politicians look alike and hence elicit the same response from much of the electorate. They lose votes to the populists and demagogues whose promises to shake up the system are more credible... A pooling equilibrium can be disrupted if reformist politicians can “signal” to voters his or her “true type"... It means engaging in costly behavior that is sufficiently extreme that a conventional politician would never want to emulate it, yet not so extreme that it would turn the reformer into a populist and defeat the purpose. For someone like Hillary Clinton, assuming her conversion was real, it could have meant announcing she would no longer take a dime from Wall Street or would not sign another trade agreement if elected.

In other words, centrist politicians who want to steal the demagogues’ thunder have to tread a very narrow path. If fashioning such a path sounds difficult, it is indicative of the magnitude of the challenge these politicians face. Meeting it will likely require new faces and younger politicians, not tainted with the globalist, market fundamentalist views of their predecessors. It will also require forthright acknowledgement that pursuing the national interest is what politicians are elected to do. And this implies a willingness to attack many of the establishment’s sacred cows – particularly the free rein given to financial institutions, the bias toward austerity policies, the jaundiced view of government’s role in the economy, the unhindered movement of capital around the world, and the fetishization of international trade.

In other words, the most promising solution may be to let the house burn down completely!

Wednesday, November 15, 2017

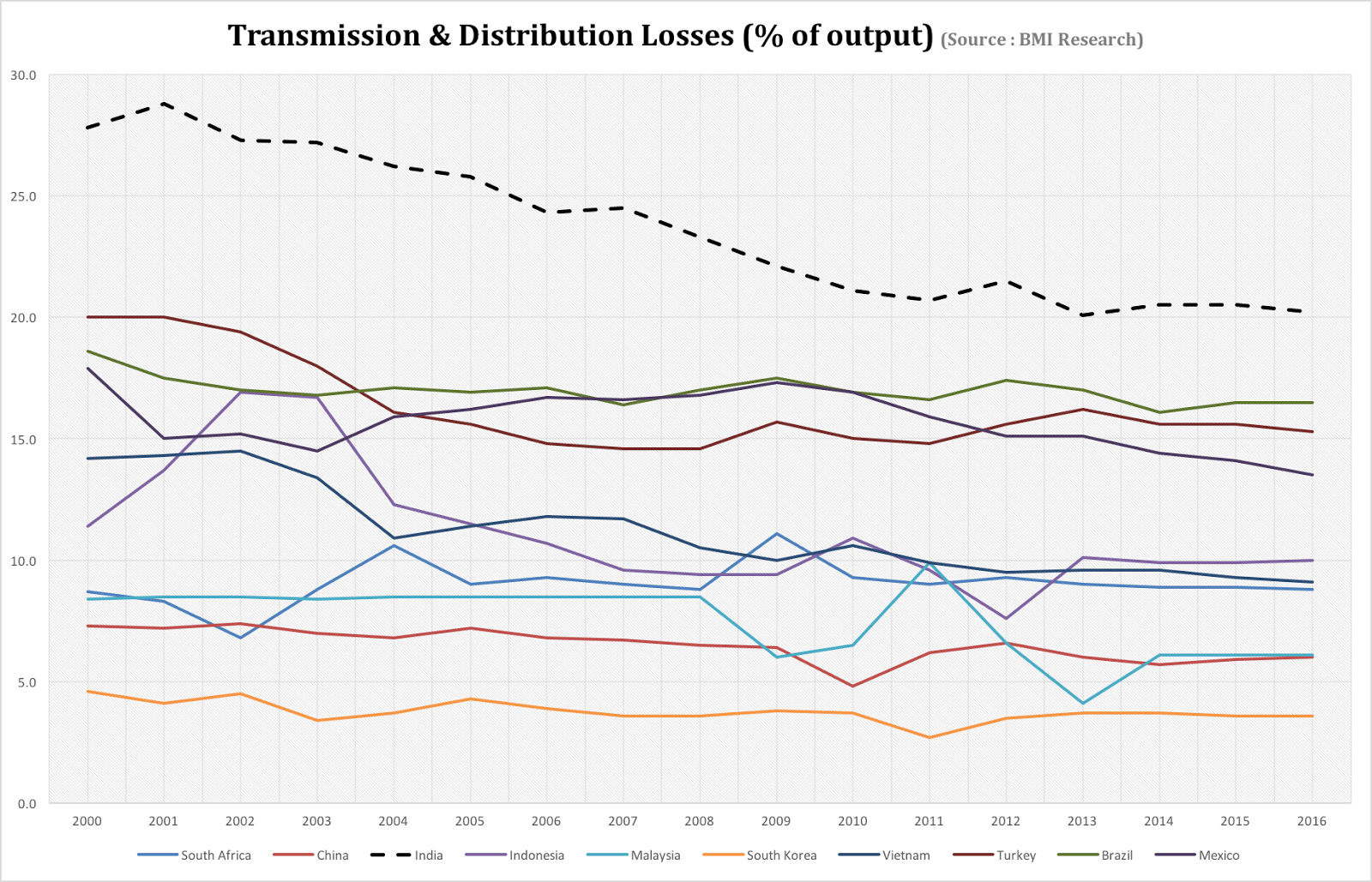

Graphical summary of India's power sector

A graphical summary of India power sector

1. Among major developing economies, despite its much higher economic growth rates, India has had the weakest growth in net capacity addition in recent years.

2. Interestingly growth in net power consumption has remained more or less steady since 2000, even during the high-growth periods of 2003-08. In contrast, economies like Vietnam and China have had much higher net power consumption rates in their high growth years.

3. This is even more surprising since India's very low percapita consumption ought to have a given a low base thrust. Note that, like with Indonesia, India's percapita consumption has barely inched forward over the past decade-and-half.

4. The relatively lower demand is also reflected in the remarkably stable growth in Plant Load Factor (PLF), even in the thermal sector, despite the significant increases in capacity addition in recent years. One would have thought that with the recent increases in capacity addition, the PLF should have risen.

5. The Achilles Heel though remains the very high transmission and distribution (T&D) losses, whose decline, worryingly enough, has plateaued off this decade. Come to think of this, the two phases of accelerated power restructuring programs appear to have had limited effect on loss reduction.

This blogger has consistently held the view that India's power surplus is deceptive. It conceals the suppressed demand arising from a combination of factors - fiscally enfeebled discoms preferring load reliefs to buying power whose cost of service is not recovered in the tariffs, deficient transmission infrastructure preventing evacuation of all available power, and displaced (to diesel generators etc) and suppressed economic activity due to poor quality of supply eroding business competitiveness.

Sunday, November 12, 2017

Weekend reading links

1. An MGI article draws attention to the digital disruption of the banking industry from platform companies which dominate the distribution end of multiple businesses,

Consider Rakuten Ichiba, Japan’s single largest online retail marketplace. It provides loyalty points and e-money usable at hundreds of thousands of stores, virtual and real. It issues credit cards to tens of millions of members. It offers financial products and services that range from mortgages to securities brokerage. And the company runs one of Japan’s largest online travel portals—plus an instant-messaging app, Viber, which has some 800 million users worldwide. Likewise, Alibaba is not just an enormous e-commerce company; it is also a large asset manager, lender, payments company, B2B service, and ride-hailing provider. Tencent is making similar advances, from a chat-service base. And Amazon continues to confound rivals with moves into the cloud, logistics, media, consumer electronics, and even old-fashioned brick-and-mortar retailing—and lending and factoring for small and medium-size enterprises...

We found that “manufacturing”—the core businesses of financing and lending that pivot off the bank’s balance sheet—generated 53.0 percent of industry revenues, but only 35.0 percent of profits, with an ROE of 4.4 percent. “Distribution,” on the other hand—the origination and sales side of banking—produced 47 percent of revenues and 65 percent of profits, with an ROE of 20 percent. As platform companies extend their tentacles into banking, it is the rich returns of the distribution business they are targeting. And in many cases, they are better positioned for distribution than banks are.

A greater potential threat for Indian banks may not be from the private sector banks, which too has not come out too favourably from the NPA problems, but from the fintech companies. Like the great Chinese companies, are the Indian fintech companies going to seize the moment?

2. It is the annual smog and odd-even vehicle season time in Delhi. Two excellent articles from Harish Damodaran and Mridula Ramesh unpacks the complex nature of the challenge arising from farmers in W Uttar Pradesh, Haryana and Punjab burning their post-harvest waste.

The central challenge is that farmers have a limited 15-20 days to prepare their fields for the Rabi wheat season, making burning of the harvest waste as the easiest and cheapest option. One solution, which Damodaran explores is to use machines which are able to mulch and evenly spread both the loose straw residue (top-part of the crop cut by combined harvesters) and the standing stubble. Facilitating the provision of these machines through custom hiring centres, even with subsidies, may be a very good idea.

Ramesh suggests encouraging the collection and composting of the harvest materials. The compost, can in turn, be used by farmers as fertilisers or to produce biogas. She advocates a "straw-harvest" subsidy, as a Direct Benefits Transfer (DBT), to farmers based on verification of whether harvested fields have been burnt or not.

3. A Livemint story on Bharatmala project has a graphic which captures arguably the biggest economic growth challenge - continuing weakness in private sector capex cycle, especially in the infrastructure sector.

And it is not the traditional problems like land acquisition or financing constraints that is holding back stalled projects, but fuel/input supply and government clearances

4. The one area where work-flow automation, facilitated by technologies like blockchain, can be very disruptive is in the logistics management of global trade. Sample this,

To quantify the documentation involved in ‘business as usual’, Danish shipping giant Maersk tracked a shipment of flowers from the Kenyan port of Mombasa to Rotterdam. The process generated dozens of documents and nearly 200 communications involving farmers, freight forwarders, land-based transporters, customs brokers, governments, ports and carriers. Maersk’s blockchain-based approach, developed with IBM, puts all documents into a single, template-based workflow, kicked off when the farmer submits the packing list. As each step is completed, documents are captured and shared so participants can see what has been submitted, when, and by whom. No one party can modify, delete or even append any record without the consensus from others on the network.

5. Edmund Phelps follows Olivier Blanchard in holding on the natural unemployment rate hypothesis and their "structural" explanations,

The structuralist perspective on macroeconomic behavior led to the concept that came to be called the “natural” rate of unemployment, borrowing from the notion, which arose in Europe during the interwar years, of a “natural” interest rate. Yet the term “natural” was misleading. The basic idea of the structuralist approach is that while market forces are always fluctuating, the unemployment rate actually has a homing tendency. If it is, say, below its “natural” level, it will rise toward this level – and the rate of inflation will pick up... The “natural rate” itself may be pushed up or pulled down by structural shifts. Moreover, shifts in human attitudes and norms may also have an impact... What explains the paradox of low unemployment despite low inflation (or vice versa)? So far, economists – structuralists as well as diehard Keynesians – have been stumped. The answer must be that the “natural rate” is not a constant of nature, like the speed of light. Certainly, it could be moved by structural forces, whether technological or demographic. It is possible, for example, that demographic trends are slowing wage growth and reducing the natural rate.

The low interest rates and low inflation have been on a secular decline for more than three decades. There are real forces, not structural ones, behind these - globalisation (global production and supply chains), trade liberalisation (and global markets for goods and services), weakening of trade unions (and the erosion of employee bargaining power), skill-biased technological changes (concentrated wage increases to the top of income ladder) and so on. Ignoring them on the face of overwhelming evidence and refusing to yield ground on theoretical constructs like "homing tendency" of unemployment rate is one more example of what makes economists lose credibility.

6. The period of regulatory arbitrage may be coming to an end for the internet superstars. A British employment tribunal, ruling on a petition by a group of 19 drivers, has rejected Uber's plea that its drivers are self-employed as independent contractors and therefore there was no need for it to pay employment benefits. The ruling means that Uber drivers will have to be given benefits like a minimum wage and paid time-off.

The European Court of Justice is also expected to rule soon about whether Uber should be regulated as a taxi service, subjected to rigorous safety and employment rules, or as a digital platform connected independent contractors and passengers.

7. The events in Middle East, centered around the actions of Prince Mohammed Bid Salman of Saudi Arabia, and the diplomatic response to them from the US, both motivated by the desire to contain Iran, are surely fuelling the flames of a new set of crisis in the region. The forced resignation of Lebanese Prime Minister Saad Harari is clearly an attempt to weaken the power exercised in Lebanon by Iran through the Hezbollah. But this may be a bad miscalculation for a regime which is already mired with botched adventures fighting the Houthi rebels in Yemen and escalated diplomatic face-off with Qatar. And all this in the midst of a massive internal drive to round-up dissidents, ostensibly in the name of an anti-corruption campaign. Add in the Israeli dimension and you have a deadly cocktail.

8. Times captures the one area where Trump's legacy can be more far-reaching than that of any other President - judicial appointments. Sample this,

Mr. Trump is poised to bring the conservative legal movement, which took shape in the 1980s in reaction to decades of liberal rulings on issues like the rights of criminal suspects and of women who want abortions, to a new peak of influence over American law and society.

Talking of judiciary, not a pretty picture across in India on an extraordinary day in the Supreme Court on Friday. Fortunately enough, the Indian Supreme Court has managed to survive with credibility intact despite its leadership in the recent past, though it is not clear whether the same can be repeated now. If we are splitting hairs about an obvious case of conflict of interest and acceptance of recusal, then matters are clearly at a crisis point.

9. Fascinating graphic on the evolution of container ships from a new MGI report on the future of container ship.

10. Finally, some figures from Alibaba's record breaking Single's Day haul,

10. Finally, some figures from Alibaba's record breaking Single's Day haul,

Alibaba shuttered the tills on its biggest Singles Day shopping festival to date — a $25.4bn haul that saw Chinese shoppers snap up more than $1bn worth of mobile phones, shoes and lipsticks every hour. More than 777m parcels were shipped out in what has become the biggest day by far in the global retail calendar... Nine out of 10 purchases were made via mobile phones... Alibaba has turned Singles Day — numerically written as 11.11 — into an event many times bigger than any US shopping day sales... 140,000 brands, including 60,000 international names, offered 15m items for sale.

Subscribe to:

Posts (Atom)