Forward guidance has assumed a central role in monetary policy making in recent years as central banks try all possible means to stimulate economic growth. The forward guidance literature makes the distinction between Delphic guidance about public statements about “a forecast of macroeconomic performance and likely or intended monetary policy actions based on the policymaker’s potentially superior information about future macroeconomic fundamentals and its own policy goals,” and Odyssean guidance that involves clarifying ex-ante on the policymaker’s professed commitment.

In this context, Ippei Fujiwara andYuichiro Waki argue that unlike Odyssean guidance, the Delphic guidance on private information available with central banks can be destabilising. Using a New Keynesian model, they find,

The underlying mechanism is simple and operates through the forward-looking, price-setting behaviour of sellers, i.e. the New Keynesian Phillips curve. Imagine that the sellers also receive some (private) information that is useful in predicting future cost-push shocks. Such information influences their inflation expectations and, therefore, the prices they set today. Their price-setting decisions become more susceptible to future cost-push shocks, and, everything else being equal, inflation becomes more volatile. Conveying news about shocks to the central bank’s loss function and shocks to the natural rate of interest has the same effect. In contrast to Odyssean forward guidance that helps stabilise inflation and the output gap, Delphic forward guidance can destabilise them in New Keynesian models.

A little asymmetric ignorance would help.

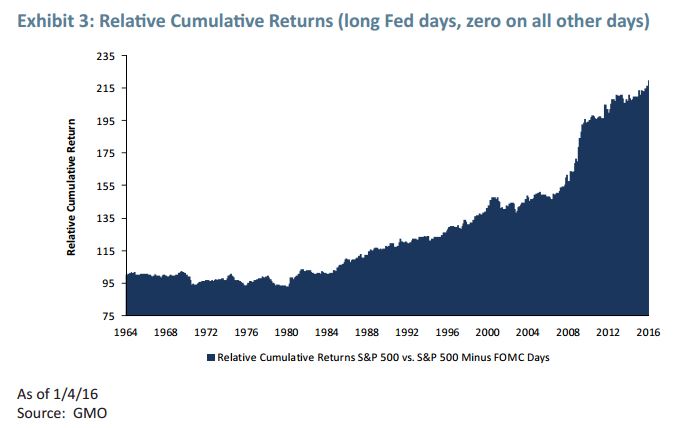

In this context, this GMO study by James Montier and Philip Pilkington assume relevance. They document very significant positive effect on equity prices over the past 30 years on FOMC meeting days after the meetings announcements. Their analysis found that since around 1985 the markets started to react significantly to FOMC days. Using a strategy of going long (buying) on the meeting days and zero on all other days of the year, over the years, they find

The authors write,

This means that we removed around 18 days a year in the 1960s, 14 days a year in the 1970s, and 8 days a year from 1981 onwards. During the period 1964 to 1983 there was absolutely no effect from removing these days. But, from 1985 onwards, removing fewer days began to have a major and increasing impact on the market. In fact, FOMC days account for 25% of the total real returns we have witnessed since 1984... the chance of this occurring randomly was only 0.0086% (that is, 86 out of 1 million).

Breaking down the effects over periods, they find that the average returns on FOMC days in the 2008-12 period were 29 times higher than the average on non-FOMC days!

In fact, the result was not, in a statistically significant manner, any different even when the Fed was tightening.

As the authors say, "it appears that the stock market reaction wasn’t driven by easing so much as it was by the fact that the FOMC was meeting at all!" Their monetary adjusted CAPE (cyclically adjusted price-to-earnings ratio), obtained by replacing the FOMC day returns with non-FOMC day average, leaves the markets significantly lower than today.

No comments:

Post a Comment