1. Europe's counterpart to the American stock market's Magnificient Seven is the eleven companies dubbed Granolas.

The crunchy acronym was coined by Goldman Sachs for pharma companies GSK and Roche, Dutch chip company ASML, Switzerland’s Nestlé and Novartis, Danish drugmaker Novo Nordisk, France’s L’Oréal and LVMH, the UK’s AstraZeneca, German software company SAP and French healthcare firm Sanofi. In the past 12 months the group has accounted for 50 per cent of gains on the Stoxx Europe 600 index, which hit a new high on Thursday, and for about half of all mergers over the past five years... The Granolas as a group have climbed 18 per cent over the past 12 months beating the Stoxx 600’s 7.5 per cent rise over the same period. Over the past three years, the Granolas have performed in line with the US’s Magnificent Seven... and with much lower volatility... The Granolas are more diverse than the exclusive tech focus of the Magnificent Seven. The top performer in the past 12 months is Novo Nordisk, which has been boosted by investor enthusiasm over its weight loss and diabetes drugs, and is up 69 per cent. The Granolas’ share of the Stoxx Europe 600 index has climbed to 25 per cent, approaching the Magnificent Seven’s 28 per cent weighting in the S&P 500. However, the European grouping, which has a combined market capitalisation of about $3tn, is dwarfed by its US peers, which have a combined value of around $13tn. The Granolas are cheaper than the Magnificent Seven on an earnings multiple, trading at 20 times next year’s forecast earnings, compared with the Magnificent Seven’s 30 times. Both sets of companies are widely seen as having strong balance sheets and healthy margins, and — despite European companies’ reputation for focusing on dividends — invest similar shares of cash flow into research and development and capital expenditure.

Japanese stocks this week finally surpassed the peak (only in nominal terms, mind) after a 17.5 per cent rise this year. The great question now is whether this will actually be taken by the endlessly patient Japanese public as marking the end of the post-bubble era. And, if it is, whether Japanese households decide it is time to channel some of their $7.7tn hoard of cash and deposits into domestic stocks that, even here, look cheap compared with those in the US. The Bank of Japan calculates that only 13 per cent of Japan’s liquid household assets are in equities, against more than 40 per cent in the US and 21 per cent in Europe.

4. Fascinating account of the spectacular rise of Lotus Bakeries and its Biscoff brand of caramelised biscuit and spread that has become a favourite of Gen Z. After decades of sleepy growth, the 92-year-old Belgian company's shares have boomed over the last decade.

Group sales have risen three-fold since 2013, while those of Biscoff-branded goods have almost quadrupled as recipes ranging from Biscoff cheesecake to Biscoff espresso martinis proliferate on social media, particularly on TikTok, where they garner millions of views... The newfound popularity has propelled Biscoff into the top five biscuit maker globally by sales, according to the company, as the pandemic-accelerated snacking boom continues despite inflation pinching consumers’ budgets. The group, whose brands also include Nakd snack bars and Trek flapjacks, reported a 21 per cent rise in annual sales last year helping it surpass €1bn in revenue for the first time. Within this, sales of Biscoff-flavoured products hit a €500mn milestone, having also risen a fifth. Shares of Lotus Bakeries, which have more than tripled in four years rallied 20 per cent in a day earlier this month to a record high...A brand version of Belgium’s speculoos — a spiced shortcrust biscuit — Lotus Bakeries has been based in Lembeke, a town close to the Dutch border, since 1932. Its recent burst of success can be traced back to 2009, when chief executive Jan Boone, then managing director, partnered with Christophe De Vusser, his schoolmate and former colleague at Bain & Co and now the incoming chief executive of the consulting group, to develop a business plan focused on internationalising the Biscoff brand. They were convinced that it could go further than traditional Belgian market because of its unique taste, long shelf life and low-cost production process. “Back then as a company, we said, ‘If we can create one global brand, I think we’ve done a good job,’” Boone, the grandson of the founder, told the Financial Times. “We obsessively managed Biscoff . . . and you see that focus really works out for the company.”In 2019 Lotus Bakeries opened its first US factory for Biscoff in Mebane, North Carolina, freeing up capacity in its Lembeke facility to pursue more markets in Europe including Germany and France. Starting with founder Jan Boone Sr, Lotus has long marketed its biscuits as a good accompaniment for coffee with Biscoff being a portmanteau of the words biscuit and coffee. “If somebody thinks about a coffee, we want them to think about Biscoff,” said Isabelle Maes, chief marketing officer at Lotus Bakeries. Its popularity has soared in recent years, boosted by increased demand during the pandemic for snacks and at-home baking as well as the explosion of user-made videos suggesting recipes. Boone said content on TikTok has helped convert the nearly century-old company into a “young and interesting” brand which it has capitalised on through partnerships with global brands including McDonald's, KitKat, and Krispy Kreme.

5. Fascinating article about the ageing fleet of wind turbines in Europe and the end-of-life dilemma it presents on whether to invest in upgrades or walk away from them.

About a fifth of the continent’s roughly 90,000 onshore turbines are at least 15 years old — and the normal lifespan of a wind farm with minimal maintenance is 20 years. In Spain, a pioneer of wind power in the 1990s along with Germany and Denmark, wind parks aged 15 or older are half of the total — the highest proportion in the EU, according to trade body WindEurope... What is best for the bloc’s electricity system — and indeed the planet — is not always the right choice for corporate owners. At the same time, there is pushback from local residents who do not want the vast structures in their backyard... Letting them expire would waste a valuable resource because the earliest wind farms are in prime sites with the strongest gales... Madrid, and the EU, are pushing for what experts call repowering: taking down the oldest turbines and using the same sites to erect cutting-edge new windmills, which are taller, more efficient and pump out more electricity. But the shift can be a costly, complicated process...A typical 20-year-old machine, whose blade tips reach as high as 90 metres, generates 800kW. A new model produces 7,000kW with blades that rise to 240m or more, surpassing the height of the One Canada Square skyscraper in London’s Canary Wharf. A single rotation produces more energy than an average Spanish household consumes in a day. Because new turbines capture more wind, WindEurope estimates that repowering on average triples a facility’s annual electricity output (in gigawatt hours) with a 25 per cent reduction in the number of machines. Deloitte estimates that repowering could deliver two-thirds of the increase in wind capacity Spain needs to meet its 2030 targets... A repowering overhaul means sacrificing, for a time, the steady cash flow that operators earn from selling electricity... The simple alternative is to extend a turbine’s lifetime with a few replacement parts, whether that is new blades, gearboxes or generators. A carefully maintained existing machine can keep spinning for 35 or 40 years, but will not get the EU closer to its target of renewable power accounting for 42.5 per cent of overall energy consumption by 2030.

This dilemma comes on the back of the gradual disappearance of wind power subsidies, a bad year in 2023 for the wind industry, surging wind power costs in Europe since the pandemic, NIMBY hostility conflated with rural-urban divides, bird deaths, and litigation.

6. The higher interest rates have sparked an interesting reversal of fortunes for US pension plans.

The average top 200 US corporate pension fund now has 105 per cent of the assets needed to fund its benefits, the highest ratio in 15 years, according to BlackRock, which has urged its corporate pension clients to consider reopening their plans.

This has triggered some thinking about opening up closed defined benefit pension plans, with IBM recently opening its long-closed DB plan to new participants.

Nearly half of large US employers still sponsor a DB plan, though only 21 per cent are open to new hires, according to consultancy Mercer. It recently surveyed chief financial officers and found that 65 per cent of other big companies with residual pension plans have considered reopening them and 88 per cent would do so if they could reduce their concerns about risk. Should interest rates go back down sharply, today’s surpluses would turn into liabilities. That’s a big driver of a parallel trend in the other direction that has seen a record number of US companies paying to offload their closed pension plans to insurers while rates are high.

There's a new option being considered,

Market-based cash-balance plans pool resources and offer the option of payments for life like a traditional pension, but the final payout is based on the plan’s investment returns, limiting the employers’ exposure. On the plus side for employees, each participant gets a personal account and can opt for a lump sum at retirement instead of a regular payment. To my mind, this is the best solution to date, as it shares the market risk while also giving employees an account balance they can check and control. Ideally, employers would follow IBM’s example by offering a supplemental 401k plan to allow employees to put in pre-tax dollars and benefit from long-term equity market growth.

7. Interesting reality-check about Indian startups.

India is proud that it has produced about 110 startup unicorns. Bravo. However, only 13 have faced the test of the public markets, accounting for just $1.5 billion out of a total of $4,200 billion; of the 13, only six are reported to generate positive operating cash flows, which is the most basic test of business acumen and success. All of these six positive-cash flow unicorns were founded around 2005, and have built an enterprise track record of almost two decades, and the average age of these six founders was 57 when they began.

8. Fine New Yorker profile of author Vaclav Smil.

The average American used two hundred and eighty-five gigajoules in 2012, he said, and two hundred and eighty-four gigajoules in 2022, despite significant efficiency gains in every category. And our record would look worse if, during the past few decades, American companies hadn’t shifted so much manufacturing to fossil-fuel-powered factories in Asia. This dilemma is easy to see on American roads. The best-selling vehicles in the United States last year were Ford F-Series pickup trucks (which for many drivers have taken the place of station wagons). As has often been observed, many models get roughly the same number of miles per gallon as the Ford Model T, which was first manufactured in 1908. But the reason is not that modern engines are inefficient. On the contrary, they’re so remarkably efficient that they now power vehicles that weigh multiples of what the Model T did, despite being loaded with power-hungry features and requiring comparatively little maintenance. In all our vehicles, no matter how they’re powered, improvements in energy efficiency often result in increases in curb weight. A Tesla Cybertruck weighs more than three tons; an all-electric GMC Hummer EV’s battery pack alone weighs almost a ton and a half, or roughly eight hundred pounds more than an entire Mitsubishi Mirage. Manufacturing those vehicles is energy- and raw-material-intensive, and it has devastating environmental impacts beyond adding to the atmosphere’s carbon load.

9. Vivek Kaul questions the premiumisation story about the Indian economy - a trend towards an increasing share of premium products in the consumption basket of consumers. Two data points are useful - the share of two-wheelers in the total vehicle population, and the volume of air travel compared to rail travel. This is about two wheelers

Further, as per the Road Transport Yearbook 2019-20, cars, jeeps and taxis formed 13.8% of vehicle population in 1991. In 2020, they formed 13.4% of the vehicle population. During the same period, the proportion of two-wheelers increased from 66.4% to 74.7%. So, three out of four vehicles are two-wheelers. This may have marginally changed in the last few years as two-wheeler sales have slowed down and cars may now form more than 15% of India’s vehicle population, but trying to pass this off as premiumization of the entire Indian economy is a little too much... Further, from April 2023 to January 2024, firms sold 14.97 million two-wheelers in the domestic market. If this pace continues they will end up selling close to 18 million units in 2023-24, significantly better than the 15.86 million units sold in 2022-23, but still well short of 21.18 million units sold in 2018-19. Also, entry level two-wheelers, like entry-level cars, aren’t selling well.

And this is about air and rail travel

From April to November 2023, the total number of passengers taking domestic flights stood at 101 million. If things continue at this pace, the number of domestic passengers in 2023-24 should cross 150 million, higher than the 2019-20 peak of 141.6 million... From April to September 2023, the latest data available, around 1.47 billion individuals travelled the Indian Railways. At this pace 2.94 billion passengers will travel the Railways by the end of the current financial year. Now, compare this to the more than 150 million passengers expected to travel by air. That is around 5% of non-suburban railway travel. How can any premiumization story not take the 95% into account? Also, 2.94 billion people will be lower than the 3.65 billion people who travelled in 2018-19 and 3.94 billion in 2012-13, but higher than 2.6 billion in 2022-23. In addition, as the Indus Valley Report of 2023 pointed out, 1% of Indians account for 45% of flights.

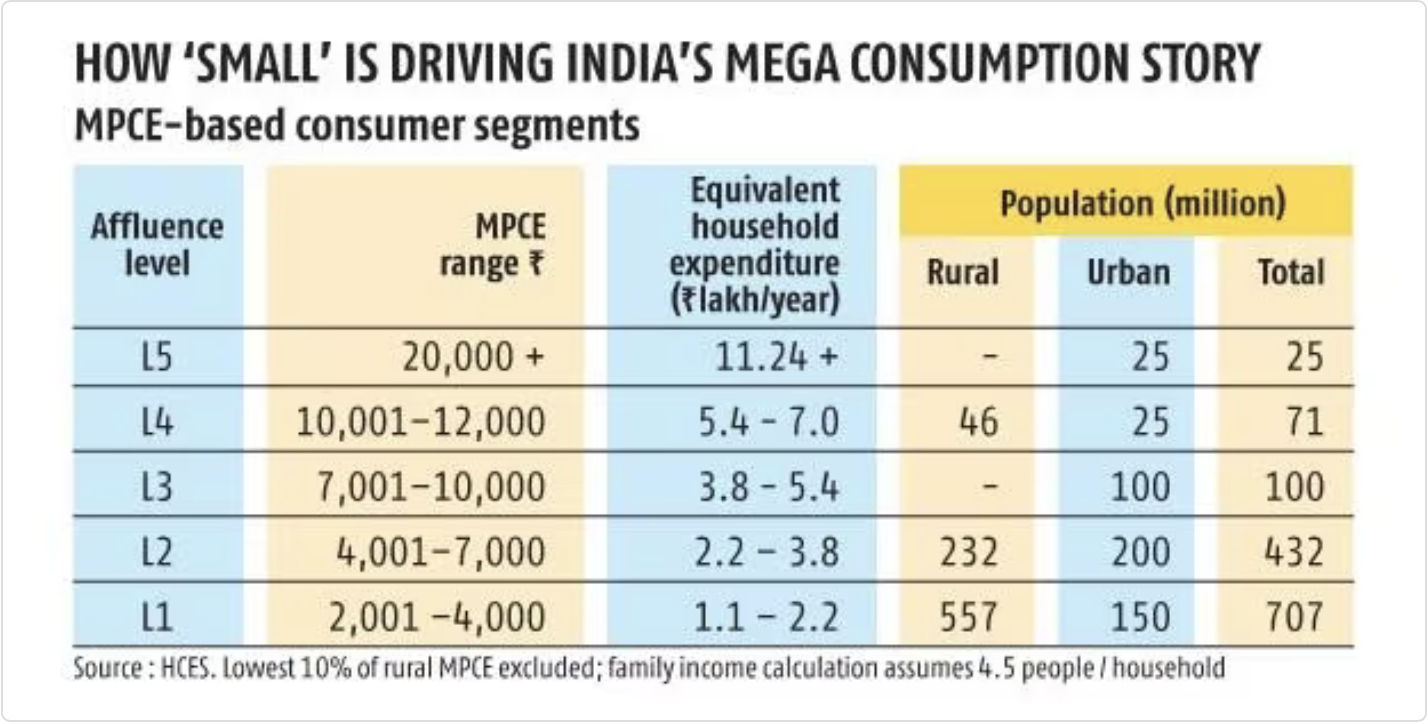

In another article, Rama Bijapurkar provides more data that questions the premiumisation of the economy.

In the table, enthusiasts for defining the “middle class” are free to locate the middle class anywhere they think appropriate. What does not change is the modest expenditure levels vis-a-vis most other markets. While we await data on household characteristics by monthly per capita consumption expenditure (MPCE) class, using Kantar data the 4 million urban and 0.4 million rural households having car, air conditioners and laptops/PC probably fall into L5, and the 114 million households, equally divided between urban and rural areas, with a refrigerator, two-wheeler, and colour TV mostly belong to L2.

Also interesting is that in the richer band of L4, there are almost double the number of rural consumers than urban. L3, the bridge class of 100 million urban people, is likely what a lot of marketers empirically observe and create the “mild premium” segment for (and incorrectly bet large on it). Now to put some perspective into the Lamborghini discourse: A little over 100 Lamborghinis have been sold in a year in India. The equivalent number for Maruti Swift is over 200,000 and for all cars is 4.1 million. Lamborghini has sold 10,112 cars worldwide — so India’s 100 is certainly a big deal for them. But how big a deal is it for us to peg our consumption theories around? Secondly, even the 4.1 million new cars sold in this country are mostly bought by the richest 10 per cent of households with some spillover into the next 10 per cent.

Just 25 million people, in perhaps 6-8 million households, have annual consumption expenditure of above Rs 11.25 lakh!

All this also underlines the point recently made by Uber CEO Dara Khosrowshahi while on an India visit that Indian consumers are extremely demanding but are unwilling to pay for anything. He also indicated that Uber in India was currently serving the upper middle class.

10. Interesting statistic about the variations in the trends with fiscal devolutions over time

The share of the southern region (Andhra Pradesh, Telangana, Karnataka, Tamil Nadu and Kerala) in the divisible tax pool has declined from 21.1 per cent during 2000-05 (the award period of the 11th Finance Commission) to 15.8 per cent during 2021-26 (under the 15th Finance Commission). However, over the same period, northern states like Uttar Pradesh (including Uttarakhand) and Bihar (including Jharkhand) have also seen a fall in their share, though in lesser magnitude. Odisha, too, has seen a decline in its share. Among those who have gained are high income states like Gujarat and Maharashtra, low income states like Madhya Pradesh (including Chhattisgarh), Rajasthan and the Northeastern states, with the exception of Assam. This is not really a North-South divide as it is made out to be.

This on the declining divisible pool

Even as the states’ share in the divisible tax pool (tax collected by the Centre and shared with the states) has gone up from 29.5 per cent under the 11th FC to 41 per cent under the 15th FC, the divisible tax pool itself has shrunk. With the Union government relying more on cesses and surcharges to raise resources the divisible tax pool has shrunk from 88.6 per cent of Centre’s gross tax revenues in 2011-12 to 78.9 per cent in 2021-22 as per the RBI. As a result, states’ share has averaged just about 34 per cent of gross tax revenues.

11. Ruchir Sharma on the Indian equity markets

Since early 2023, the median stock is up more than 40 per cent... foreign money is flowing in, but not as fast as domestic money. As a result, foreign portfolio investors now own less than 40 per cent of the stocks that are available for public trading, down from 60 per cent a decade ago... The amount of money Indians hold in targeted investment plans has tripled this decade to nearly $110bn. Over the past two decades, the number of publicly listed companies in India multiplied by a factor of nearly five to 2,800, even as it was falling by a quarter to 4,700 in the US, where oligopolies began to exert a stronger grip on most industries, not just tech. Remarkably, 180 companies in India have tripled in value this decade and now have a market capitalisation of $1bn or more. That is more than in any other country, including the US. Most bull markets see excesses build up over time; in India, they are visible in subsets of the growing retail investor class. In 2023, Indians purchased more than 85bn options, or nearly eight times the volume in the US, and on average held those contracts for less than half an hour. Amid the frenzy, regulators ordered trading platforms to open with a warning that 90 per cent of retail investors are losing money on these trades.

12. The Math premium in the UK

The £500,000 lifetime earnings premium that a maths graduate can expect relative to other graduates: this equates to more than 15 additional years of median earnings. Even those who do maths to A-level enjoy a 10 per cent earnings premium relative to someone else in the same job.

13, It'll be very interesting to see what happens in Javier Milei's experiments in Argentina!

A political outsider inaugurated in December on a promise to take a chainsaw to the state, Milei surprised Argentina by eking out the country’s first budget surplus in 12 years in January. That was achieved by slashing payments to provinces, freezing budgets and not uprating pensions and benefits fully for inflation, which was running at 254 per cent a year last month. Economists have warned that such drastic spending cuts may not be sustainable. But Milei, a former economist and TV pundit, believes that having brought down inflation from a peak of 25.5 per cent a month in December to 20.6 per cent in January and an expected 15 per cent in February, he can turn around the crisis-stricken economy this year without congress...

According to a report by consultancy Invecq, nearly half of the fiscal adjustment the government made to reach a surplus in January came from not fully uprating pension and social spending for inflation, though some social security payments, such as food stamps and child benefit, have been increased. Analysts warn that the key to Milei’s success will be how long poorer Argentines, who have already endured runaway price increases, tolerate such measures. Argentina’s confederation of unions has already held a nationwide general strike against his government and several smaller protests have taken place.

It remains to be seen whether the admiration for his actions among free-marketers will remain once the consequences start to show. I guess, they'll then argue that the opponents sabotaged and diluted the actions of the President.

14. The problem with timing the stock market exits

Duncan Lamont, head of strategic research at Schroders, calculates that US stocks have been at a record high in 30 per cent of the 1,176 months going back to 1926. If anything, the market performs slightly better in the 12 months after a record is struck, churning out 10.3 per cent above inflation compared with 8.6 per cent the rest of the time. The adage that it is time in the market that matters, rather than timing the market, also holds. Resisting the temptation to jump out of stocks around the time of record highs delivers meaningful benefits. If you switch in to cash at those points, then over 10 years you lose 23 per cent of your wealth, he calculates.

15. Finally, one of the things with the US economy is its resilience. Times has an article that points to the possibility that easing of restrictions on immigration may have played an important role in boosting the economy.

A resumption in visa processing in 2021 and 2022 jump-startedemployment, allowing foreign-born workers to fill some holes in the labor force that persisted across industries and locations after the pandemic shutdowns... Net migration in the year that ended July 1, 2023, reached the highest level since 2017. The foreign-born now make up 18.6 percent of the labor force, and the nonpartisan Congressional Budget Office projects that over the next 10 years, immigration will keep the number of working Americans from sinking. Balancing job seekers and opportunities is also critical to moderating wage inflation and keeping prices in check. International instability, economic crises, war and natural disasters have brought a new surge of arrivals who could help close the still-elevated gap between labor demand and job candidates.

No comments:

Post a Comment