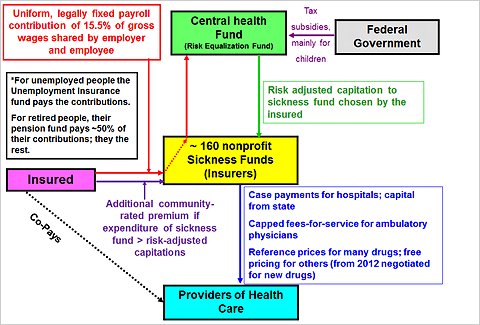

Employees and pensioners pay 8.2% of their gross wages/pensions, while employers/pension funds must contribute 7.3%, for a total contribution of 15.5% of gross wages/pensions upto a maximum wage of (or pension) of 44,550 euros. Unemployed people pay premiums in proportion to their unemployment compensation, and for the long-term unemployed the government pays the sickness fund a fixed per-capita payment. The coverage is for the entire family. Insurance is tax-financed for children. Employees/pensioners earning above 49,500 euros (in 2011) are free to opt out of the statutory system and purchase private, commercial coverage, but if they do, they cannot ever return to the statutory system unless they are paupers.

In order to equalize actuarial risk among the competing sickness funds, all premium payments go into a national risk-equalization fund, from where a capitation (that is risk-adjusted for the employee/pensioner and dependents) is paid out to chosen sickness fund of the employee/pensioner. Recent federal legislation has forced private insurers to levy on younger people higher premiums than their actuarial risk can justify to build up an old-age reserve, thus preventing premiums from climbing too rapidly with age.

In countries like India, where health insurance market is in its nascent stages and state and central governments have been experimenting with various models, the German model is instructive. The most important attraction of the German model is its offering of community-rated universal coverage for a basic prescribed package of benefits. This arrangement minimizes actuarial risks and keeps down both premiums for the insured and administration costs for the insurers.

Currently in India a number of states and the Union Government are rolling out independent insurance schemes, each for different categories of citizens within the same geographic area. Such fragmented schemes, by concentrating risks, run contrary to the principles of optimal risk management and increases the costs for all sides. Since most of those covered in such schemes are subsidized, the governments end up paying the higher premiums. Insurers hedge for both the higher risk and the actuarial uncertainties associated with such specific and concentrated risk pools by demanding higher premiums.

An ideal system would be for the Government of India to bring together all state governments on board in a national health insurance scheme which is universal for a basic package of benefits. The scheme should be community rated and opened to all insurers, public and private. An Aadhaar-complaint database can be maintained to administer this scheme and subsidize premiums for certain categories of citizens. All citizens should be mandatorily covered under the scheme, and those requiring additional coverage be permitted to buy supplementary insurance (additional benefits) from the market.

See this excellent comparison of health insurance systems from fourteen countries.

Update 1 (9/3/2012)

Conservatives in the US have for long advocated consumer-driven health plans (CDHPs) which combine high-deductible health plans (HDHPs) with Health Savings Accounts (HSA). The HDHP's have low premiums, out-of-pocket payment caps, no co-payments, but high deductibles. The consumer desposits a fixed amount each year into the HSA, which is tax-deductible and gets carried forward, and which can be used for regular out-patient medical expenses and for payment of deductibles.

It is argued that since consumers make the payments (of deductibles and other regular medical expenditures) directly and are therefore responsible for their health care purchase decisions, they are more likely to optimize on their treatment options. In regular health insurance models, the consumer is completely divorced from the payment decisions, thereby generating several incentive distortions.

Critics see this as part of efforts to introduce more private participation into health insurance and make consumers responsible for their health care plans. They also see this, along with the Republican supported plans to replace Medicare with vouchers that can be used to purchase health insurance plans from private insurers. The rising health care costs, asymmetric information problems in health care, and the lack of expertise in consumers to shop for the best possible insurance alternative, and so on make such consumer-choice plans inefficient and burdensome for consumers. See Paul Krugman's critique here.

See this Youtube video on CDHPs. See this excellent paper comparing helth insurance systems from across the world. See this account of the Swiss health insurance model.

2 comments:

Back to disecting the Indian topics please

a. USDINR

b. IIP getting crushed

c. Powershortage looming

d. RBI behind the curve

e. supply side getting killed !!

etc etc

Hi Gulzar Sir,

Yes, the health Insurance scheme at a central level is a real benefit for every citizen of India whoever working in public sectors or private sectors or any kind of employment. Its all mixed up when we study the Health Insurance schemes that are available in the market and for a common man who really want to insure his old parents or family with out any conditions apply flaws - I hope the Central government can only make it. This is really a good idea for the political parties to keep this in their next election mandate :-).

nevertheless, the challenging part is bringing all the states on the table. Thanks sir, you're great

Post a Comment