"These fixed costs of administering a loan can explain why interest rates for small loans are so high, why they vary so much across borrowers, and why the poor pay higher interest rates. Since borrowers with little wealth must get small loans, the fixed administrative cost has to be covered by the interest payment, which pushes the interest rate up. But high interest rates exacerbate the problem of getting borrowers to repay. Total lending therefore shrinks further, pushing up interest rates even more, and so forth, until the loan is small enough and the interest rate high enough to cover the fixed cost for even a small borrower. In other words, the presence of fixed costs introduces a kind of multiplier into the process of determining the amount lent and the rate charged... And if the borrowers are poor enough or the fixed administrative cost is high enough, the interest rate could become infinite: these borrowers will be unable to borrow at all."

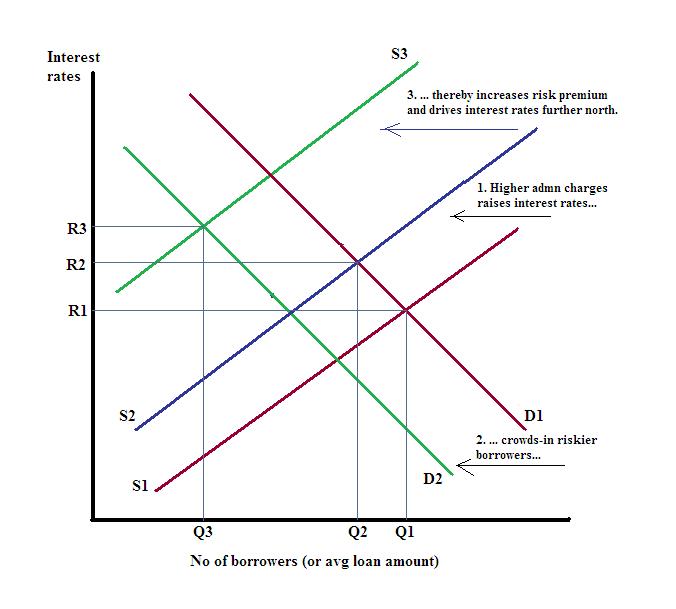

The sequence of events goes something like as follows

1. The lender has to incur a fixed cost on maintaining a large recovery machinery and general administration of the loan. In view of the large numbers of these borrowers and the specific nature of such loans (no collateral loans to those without any prior credit history), the fixed enforcement costs (due to more enforcers, need to collect information on a larger number of people etc) are likely to be large. The larger fixed costs coupled with smaller loan amounts means higher interest rates.

2. Higher the interest rates, the less credit-worthy borrowers will "crowd-out" the more credit-worthy ones, and an adverse selection effect will be generated. The higher interest rates would attract borrowers who are intrinsically more likely to default. This too adds to the administration cost at the margins.

3. Higher interest rates will naturally lower the size of loans. This also means that the absolute interest repayments will form a larger percentage of the loan principal. In other words, smaller loans means that the fixed costs as a percentage of the loan amount will be higher, thereby driving the interest rates even higher up.

Here is a graphical illustration of how the high administration charges of micro-loans drives up the rates, crowds out the best borrowers, lowers average loan amounts, and thereby forces rates even further up.

The moral hazard is amplified by the presence of multiple and competing lenders. The cost of a likely default is often lowered by the possibility of another lender waiting in the wings to step up when the need arises again. In this context, it would be interesting to examine the moral hazard effect on private micro-lenders arising from the presence of government micro-finance (if they default there, they can always fall back on the government)?

The cost of default has to be higher than the interest payment so as to minimize the possibility of default. As Banerjee and Duflo point out, the incentive of a continuous relationship with the bank/micro-lender often provides the deterrent against default.

The fundamental issue being raised here is this. Micro-finance has emerged as one of the major sources of channeling credit to poor people. It is arguable that even as micro-finance has grown in importance, it may have had unintended effect of taking away the focus from penetration of conventional banking into rural areas and among the poor.

However, as the aforementioned reasoning/modelling suggests, micro-finance services only a specific category of customers among the poor. While regular consumption needs and business working capital requirements (with their focus on adequacy and timeliness) are optimally serviced by micro-loans, small-business capital investments (which need larger and longer tenor loans) would require conventional banking.

Conventional banking will always be the preferred choice for customers borrowing higher amounts with longer tenors. Further, there will be a large share of the poor who cannot afford the higher rates charged by the micro-financiers. Under the circumstances, the total consumer welfare among the poor can be maximized only if micro-loans complement, and not substitute, conventional banking sources.

7 comments:

A question that arises is whether the authors 'Abhijit V. Banerjee and Esther Duflo' seek to name rising administrative costs as the only, or even the most important reason for MFIs to lend at higher interest rates.

Traditional banking and lending wisom have always held that risk is directly related to interest rates and a riskier investment causes banks to charge a higher interest rate.

After reading the article i have not been able to understand the chain of reasoning that leads to the conclusion mentioned in my first para.

I reproduce some more material from the same study below.

"but, in a survey of a 120 slums we conducted in Hyderabad, only 6 percent had a bank loan. On the other hand, 68 percent had loans (obtained from informal sources, such as moneylenders), and the average outstanding loan balance conditional on having a loan was over $1,000. The average interest rate they were paying on these loans was 3.85 percent per month or about 57 percent per year. "

The numbers seem to suggest that the informal sector is still very dominant in meeting the credit needs of the poor. In light of this, attempts by governments of the day to throttle them, is likely to hit the poor more than the "usurious" lenders.

Perhaps one can try small organizations run by volunteers working part time (either for free or for a small sums), in small areas they know. And a few such can come under the umbrella of a cenral office which confines itself giving training and supplying money. I have seen a small organization working in a village where only one person is paid for working part time. The total amount is small, about 3 lakhs and served 70-80 people so far, and it has been running for four years without any defaults and the interest rate is one percent a month calculated on the amount left after each month.

May be for the poor who is in need of immediate cash,for example a health emergency, it does not matter as to what is the interest rate.... but what matters is the availability of cash for immediate use.

Is it only the poor and slum dwellers who face high interest charges? I think every credit card user runs the risk of incurring a very high interest rate.... and yet everyone loves to hold one. It is for the simple reason that having a credit card gives a feel of security in case of emergency.

In the case of credit cards, there is not much administrative charges, it is just the high rate of default that ends up as high interest charges. In a nutshell, for someone's default or faulty identification of customers, every card holder is asked to pay a higher interest.

It is a fact that very few % of credit card users withdraw cash through credit cards as the interest rates are ex-orbitant for cash drawl.so, when it comes to credit card users not much hue and cry on high interest rate is there since by virtue of awareness in usage of credit cards that makes a bonafide user is more careful about when and for what to use a card and if we can bring that awareness among the poor and who access MFI's on when to fall back on MFI's then may be the default rate will come down and administrative costs might reduce.

sir, administrative costs are surely one of the largest contributors to the high interest rates. i am inclined to think it is the largest contributor. in any case, the small size of micro loans means that interest rates will have an inherent upward bias.

interest rates are a sum of the cost of capital, administration costs, risk premium, and a reasonable rate of return. in case of micro-loans, since the loan amounts are small, the per-capita administration costs are much higher than that for the regular borrowers. often, the reduced risk premiums (due to say, group collateral) are more than off-set by the higher per-capita admin costs.

the nature of micro-loan borrowers means that a self-feeding loop of higher rates crowding-out better borrowers, thereby forcing rates up higher and also lowering loan sizes even more, gets generated.

i completely agree with you that moneylenders are the most important source of credit for the poor, even in urban areas. therefore any attempts to throttle them, without having in place alternative sources of channeling credit, is likely to rebound badly and adversely affect the poor. and their dominant presence, as the hyderabad figures suggest, means that any attempt to drive them out is doomed to fail.

thanks Mr Gaddeswarup for your point. i fully agree with the decentralized (should we say franchise) model u suggest. in fact, by keeping the size and area of operation small, the administration costs can be brought down significantly, thereby enabling the MFIs to lend even smaller sums at lower rates.

the model of small village-level franchises (adequately supervised) working under the broad umbrella of a central organization providing capacity building and re-financing support is excellent. but the critical thing here would be the transaction costs incurred in co-ordinating between these rural "franchises".

Rajesh, my argument was that MFIs are inherently prone to charging higher interest rates (or atleast the larger MFIs).

in view of this, it may not be advisable to have a strategy that focuses on promoting MFIs while neglecting on the penetration of conventional banking. both are not substitutes. in fact, i will argue that the former would form the major share of the credit market, with MFIs servicing a smaller portion.

Post a Comment