The blockbuster IPO of SpaceX has drawn attention to the role of the index investing market segment, which originated fifty years ago. The scrutiny will only intensify in the days ahead as both Anthropic and OpenAI are listed.

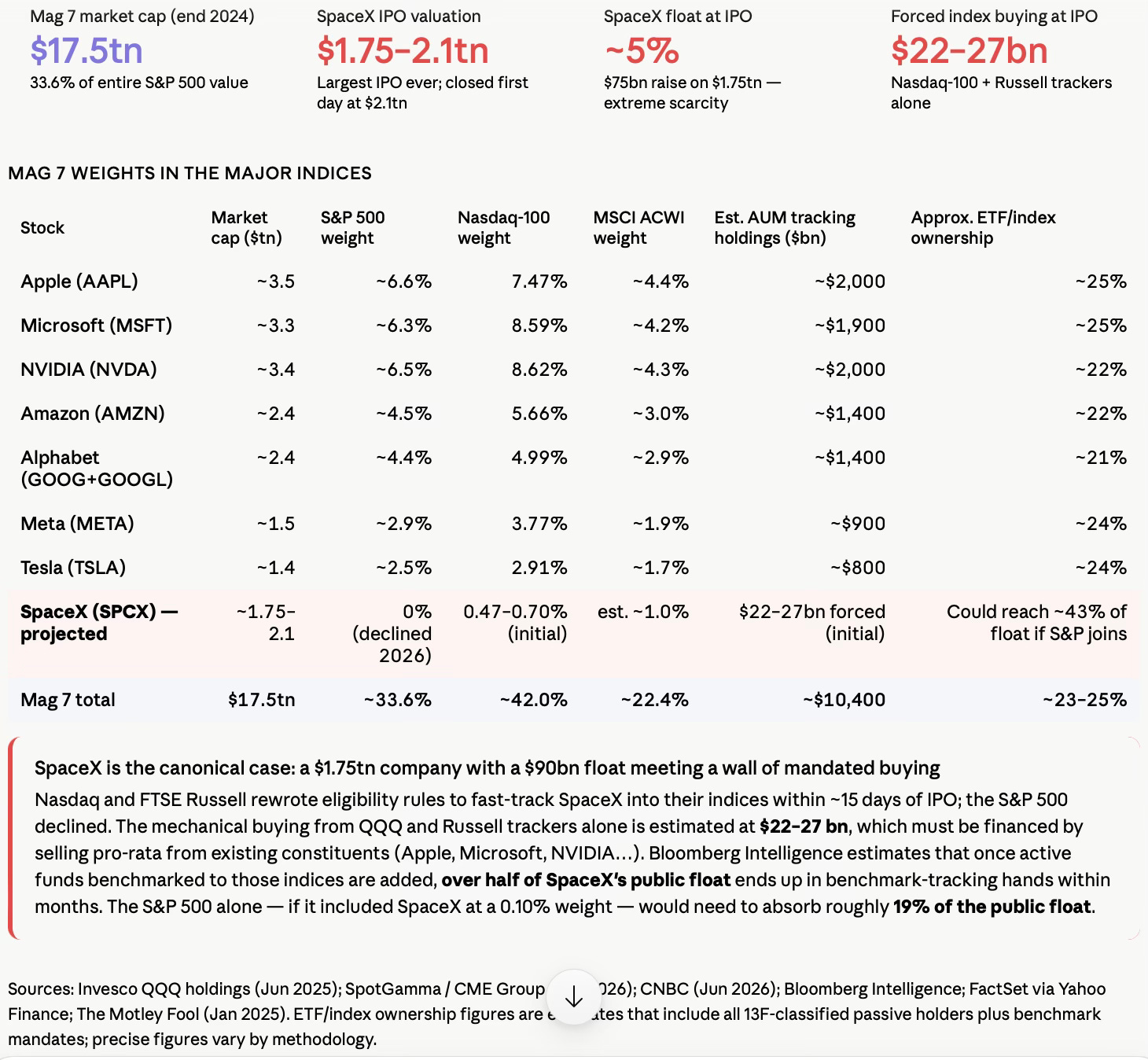

Despite only about 4 per cent of SpaceX’s shares being listed, a high level of demand was built in, also because some index investors will soon be required to add the company to their portfolios. Nasdaq amended its rules (as also CRSP and FTSE Russell) to allow SpaceX to enter the Nasdaq-100 index via fast-track, thereby providing it free liquidity through a captive market. Morningstar follows 6,006 US-registered mutual funds and 5,100 ETFs, covered by 3,203 separate benchmark indices against which $41.1tn of assets are managed.

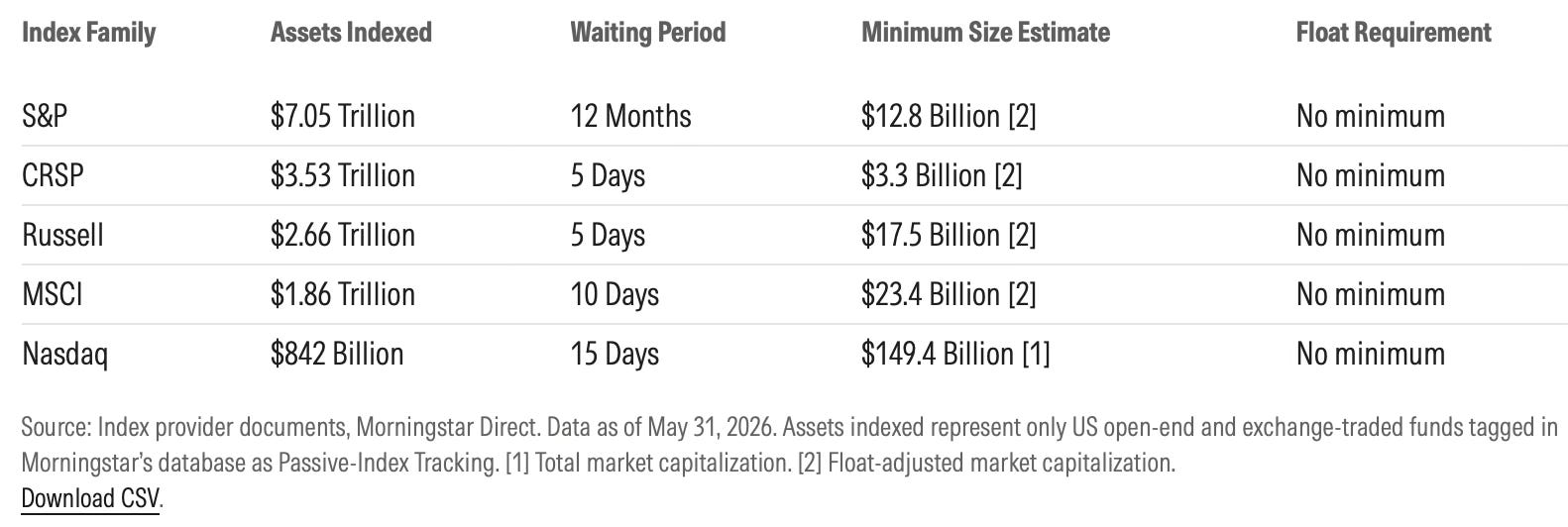

The current entry requirements for indices are very liberal for large companies.

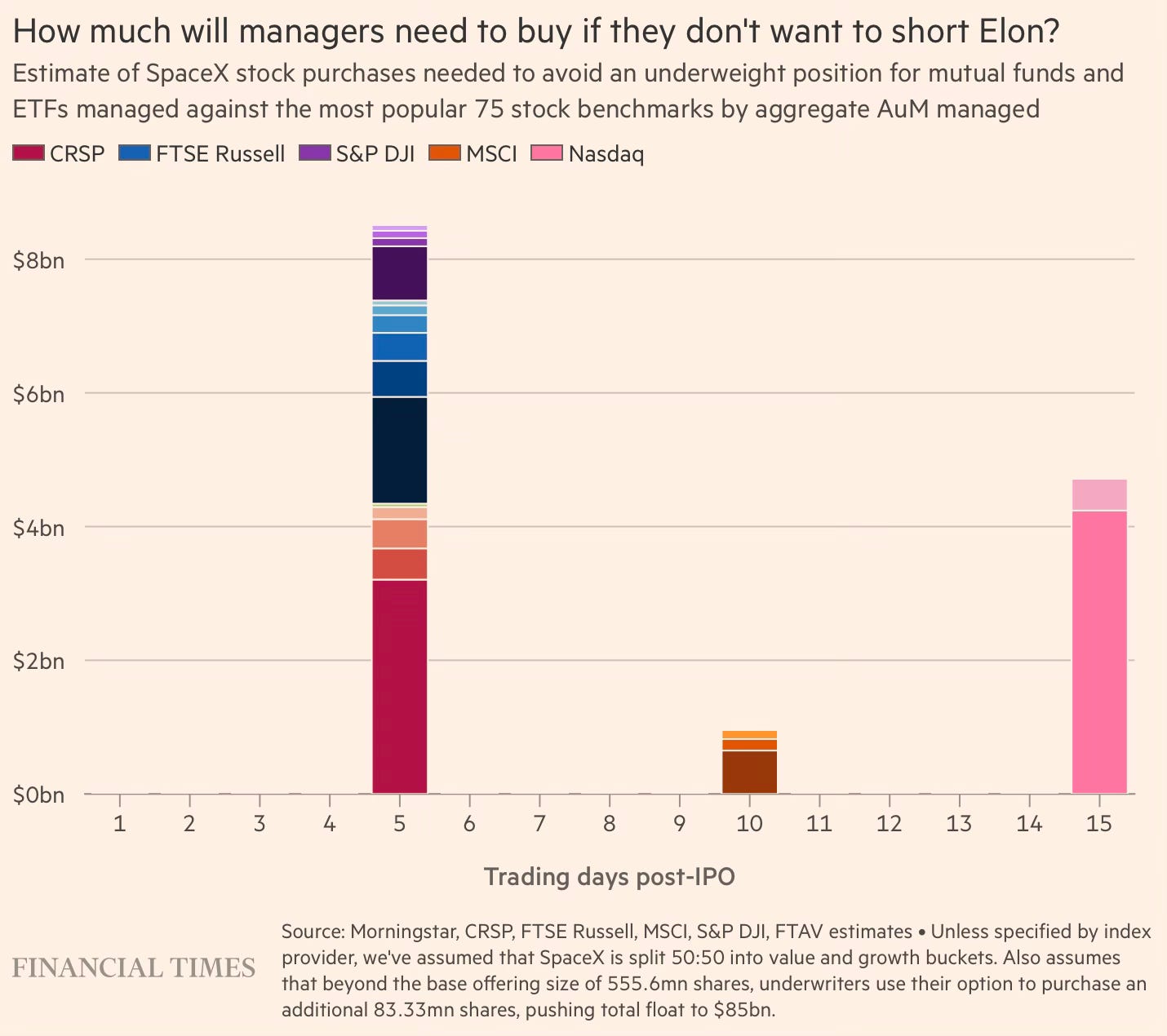

However, what distinguishes SpaceX is its very low float (just 4.25% compared to above 90% for the other big companies) and the fact that it does not yet make any profit. Toby Nangle and Co at FT Alphaville tabulated that active fund managers (who want to ignore Musk) and passive portfolio managers (who have no choice) must purchase $14.2bn of SpaceX stock in the first three weeks of trading to avoid going short.

We think that managers who have absolutely no interest in going either long or short Elon will need to collectively buy $8.5bn of SpaceX stock on the 19th June, a further $1bn on 26th June and a final $4.7bn on July 3. And so we’re talking a cumulative, de facto mandated $14.2bn of mutual fund and ETF orders by July 4 to avoid having to take a view on Elon. That number would’ve been around $11bn higher if the S&P 500 index committee had leaned a different way. But it’s $13.2bn bigger than the $1bn it would’ve been if index committees had sat tight on their existing fast-track methodologies. And this is before we count institutional assets like pension funds, insurers and foundations, as well as every single foreign owner whose benchmarking habits we currently lack information.

So this is a big deal. Clearly, the market has been brazenly manipulated by changing the rules to create the stage for SpaceX (and the other two mega IPOs).

I took the help of Claude to generate a few graphics to understand the scale of index investing, its dynamics and distortions, and possible reforms.

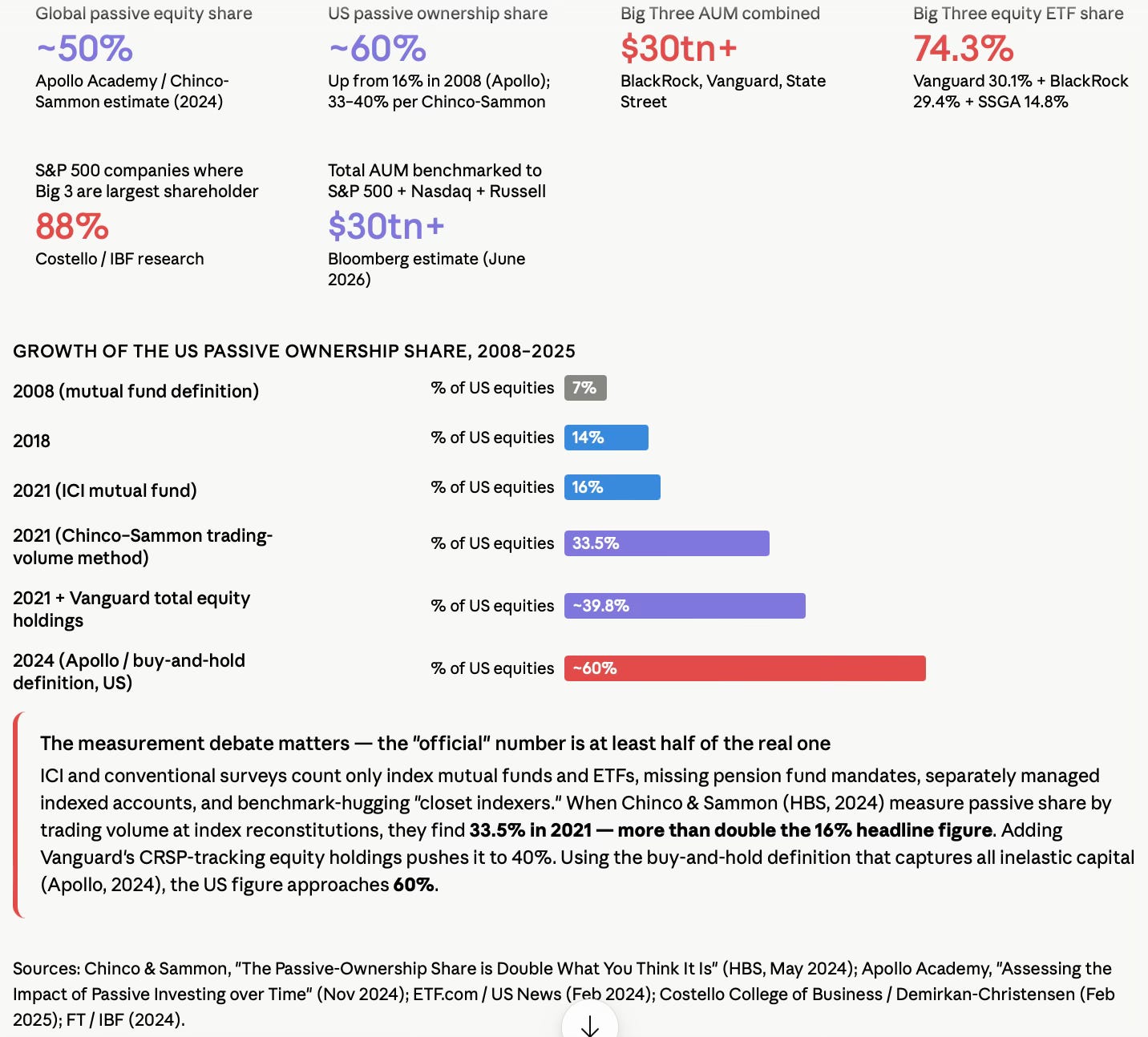

The conventional measures dramatically understate index investing because they count only labelled index mutual funds and ETFs. However, using the indexation definition, passive ownership of global equity mutual funds and ETFs is 50% and 60% for US equities. In fact, a stunning three-fourths of the equity market exposure of the big three US asset managers is through ETFs.

SpaceX’s shares could have an index exposure of 43% in a year when it joins the S&P 500, and that too on a volume which would be a fraction of that for the Mag7 firms. It is estimated that S&P 500 funds would need to absorb 19% of SpaceX's public float upon inclusion, with the Russell 1000 and Nasdaq-100 funds absorbing another 24%. A tiny supply of $22-27 bn would meet a mandatory demand of 43%.

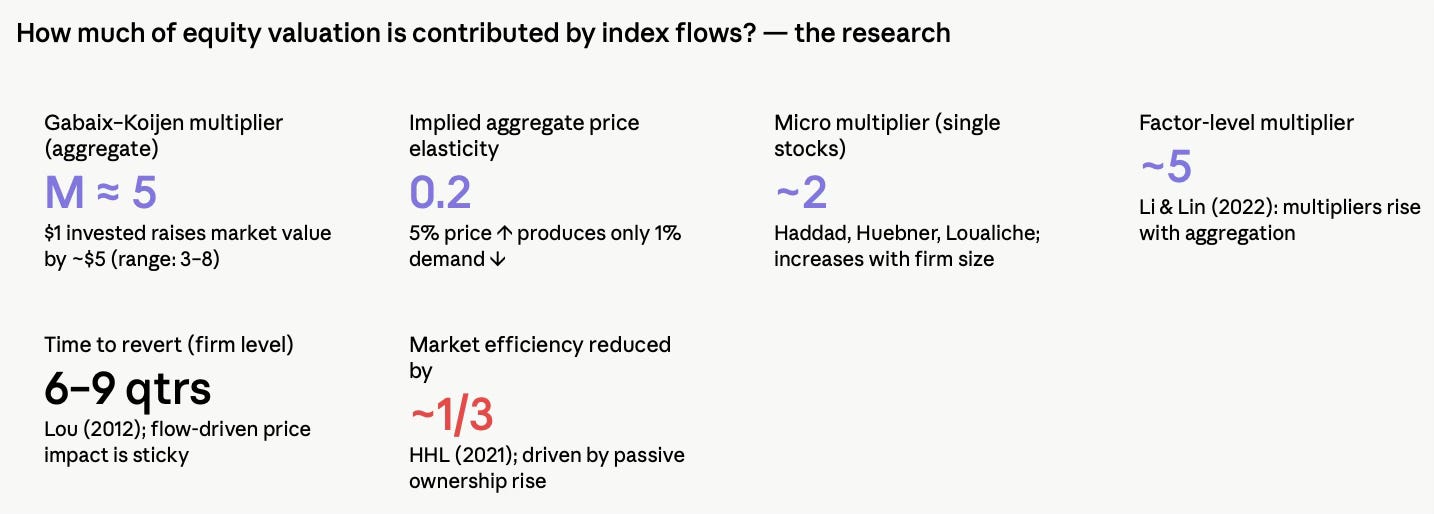

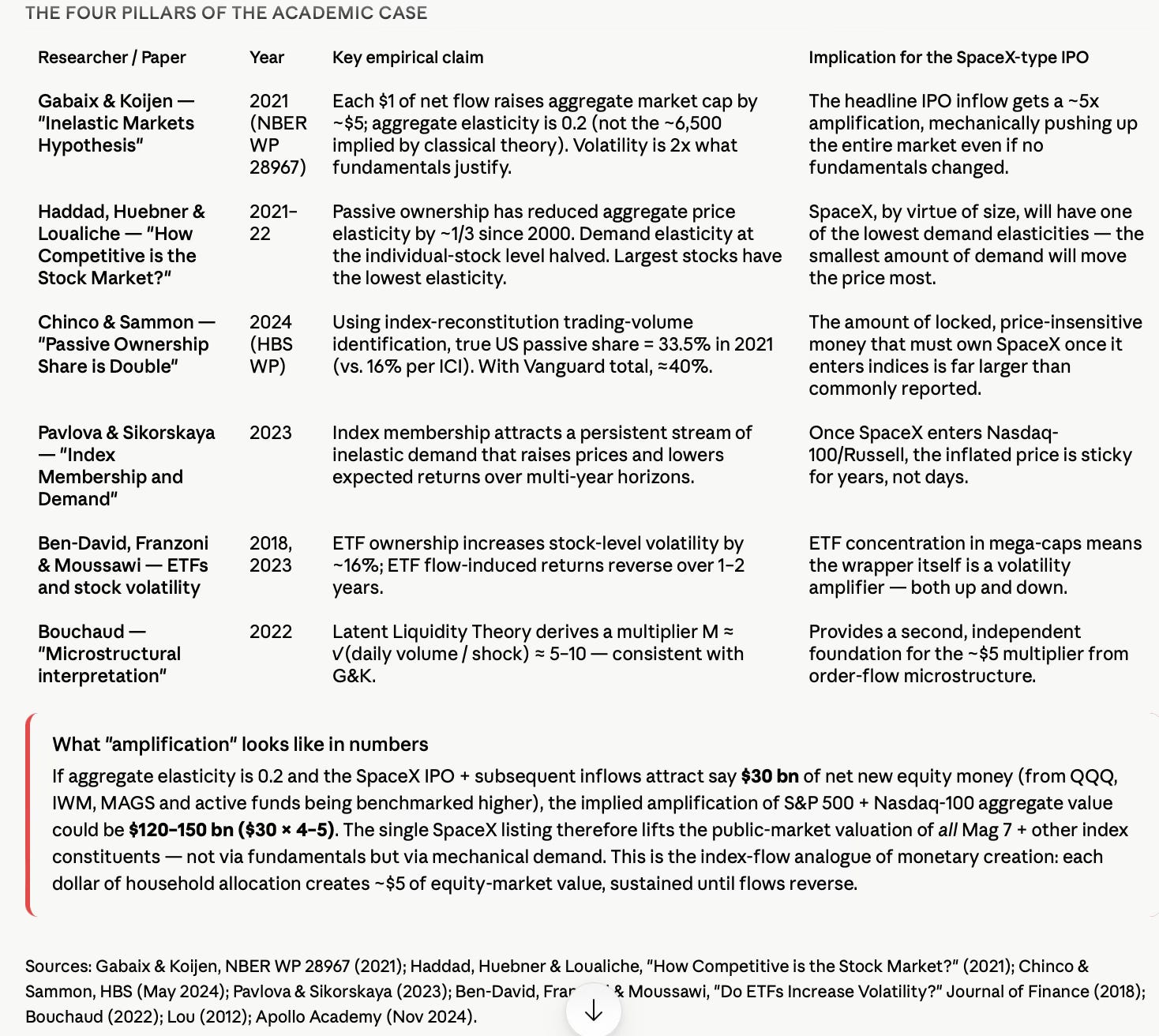

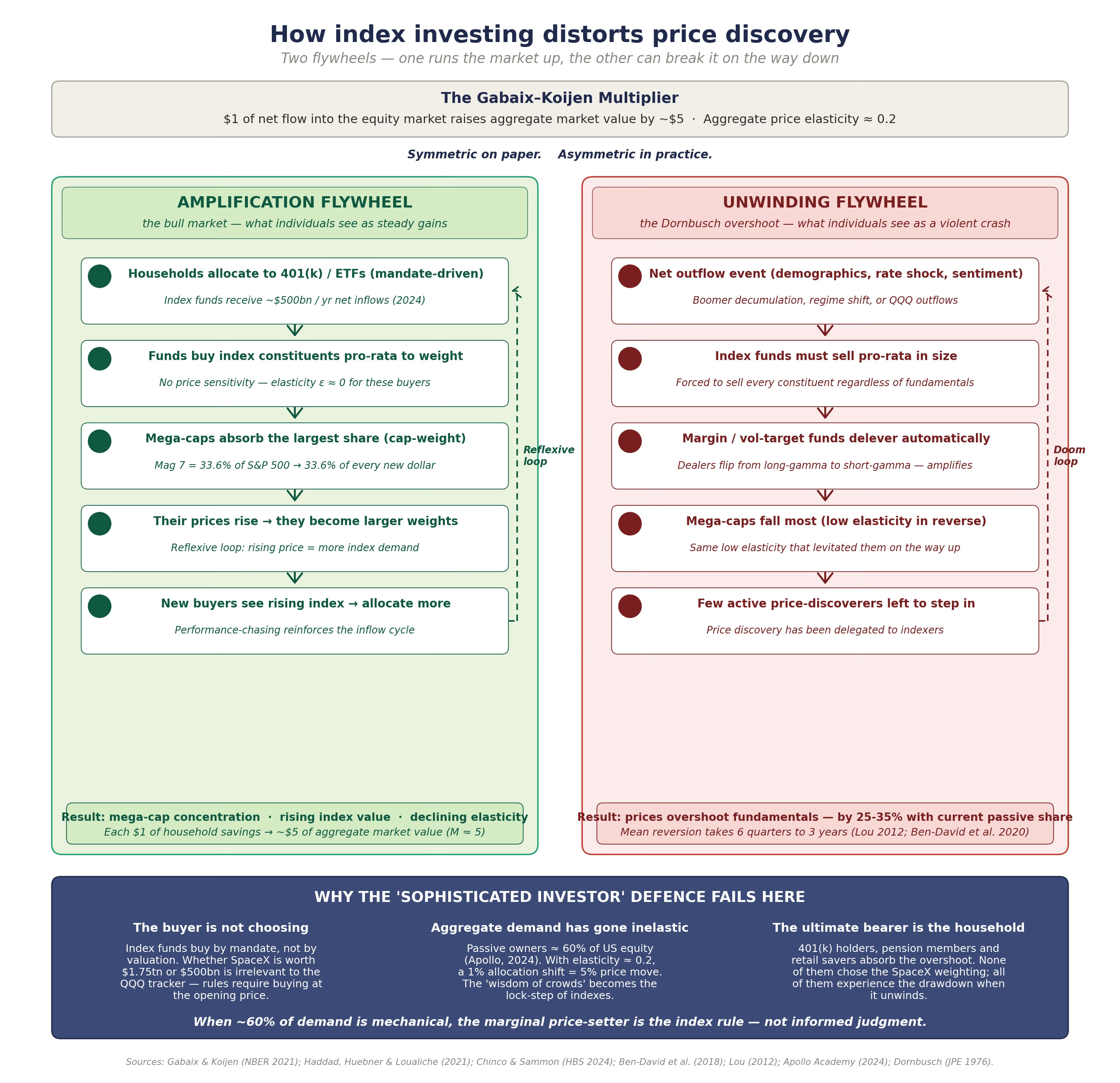

The research on the impact of index inclusion on stock price offers striking findings. Gabaix and Koijen find investing $1 in the stock market increases the market’s aggregate value by about $5. Since marginal holders of equity (index funds, pension funds, insurance companies) operate under mandates that fix their equity allocations within narrow bands, when aggregate demand shifts, few participants can absorb the change, and prices must move substantially to clear the market.

Haddad-Huebner-Loualiche point to a Mathew Effect in indiex investing. They find that a $3.6trn market cap company is only about five times as liquid as a $100bn company, despite being 36 times the size. The largest stocks are disproportionately impacted by each dollar flowing into passive funds, causing the largest stocks to outperform and stock market concentration to rise. Passive investing has reduced market efficiency by over one-third.

Index investing brings the benefits of access to a low fee, diversified, and tax efficient asset pool to the retail investors. In the words of the legendary investor Jack Bogle, index investing is the equivalent of not looking for the needle but instead buying the haystack.

However, it distorts price discovery, creates inelastic demand, amplifies concentration in stocks and asset managers, and erodes governance. All of these distortions are greater for the mega-cap stocks.

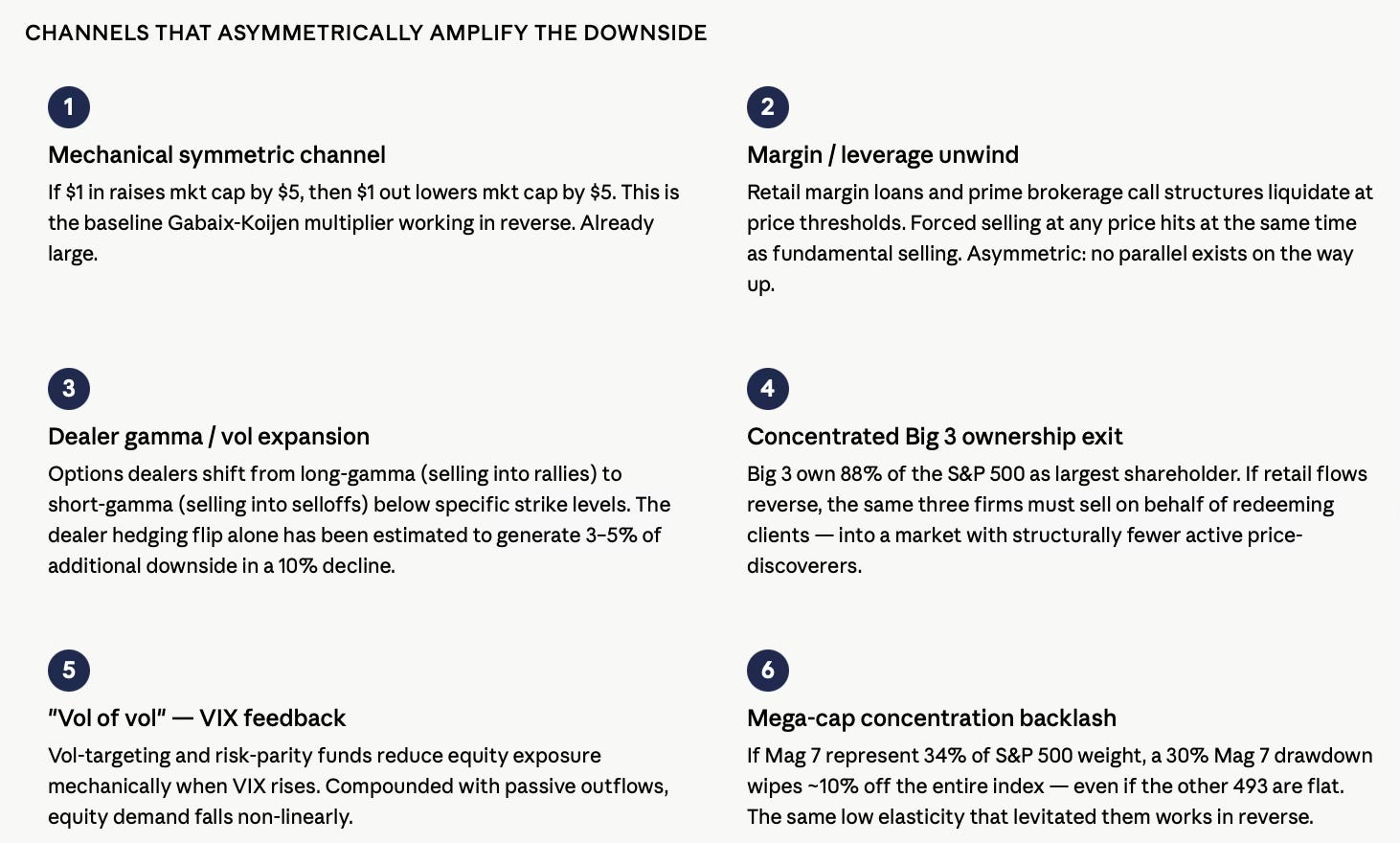

Further, index-investing comes from asymmetric flow elasticity. While passive funds are mechanically symmetric (the 1:5 multiplication), the rest of the system (margin lenders, derivatives dealers, momentum funds, retail behavioural agents) is not. When flows reverse, the multiplier still applies, but additional positive feedback channels switch on, creating an overshoot below fundamental value before mean-reversion can bring prices back. The resultant instability can tip markets into prolonged and deeper downturns. This is an illustrative example

Suppose 2 years post-IPO, growth disappointments and rate-policy reversal trigger a ~20% net outflow from Nasdaq-100 trackers ($280 bn × 20% ≈ $56 bn). Applying the firm-level multiplier (~2 for stock-specific flows, higher for concentrated names): mechanical impact on SpaceX share price could be ~30–45%, on top of any fundamental revaluation. The same flow proportionally affects all Mag 7. Index investing does not just amplify upside — it removes the price-discoverers who normally cushion downside.

Below is a listing of some channels that amplify the downside.

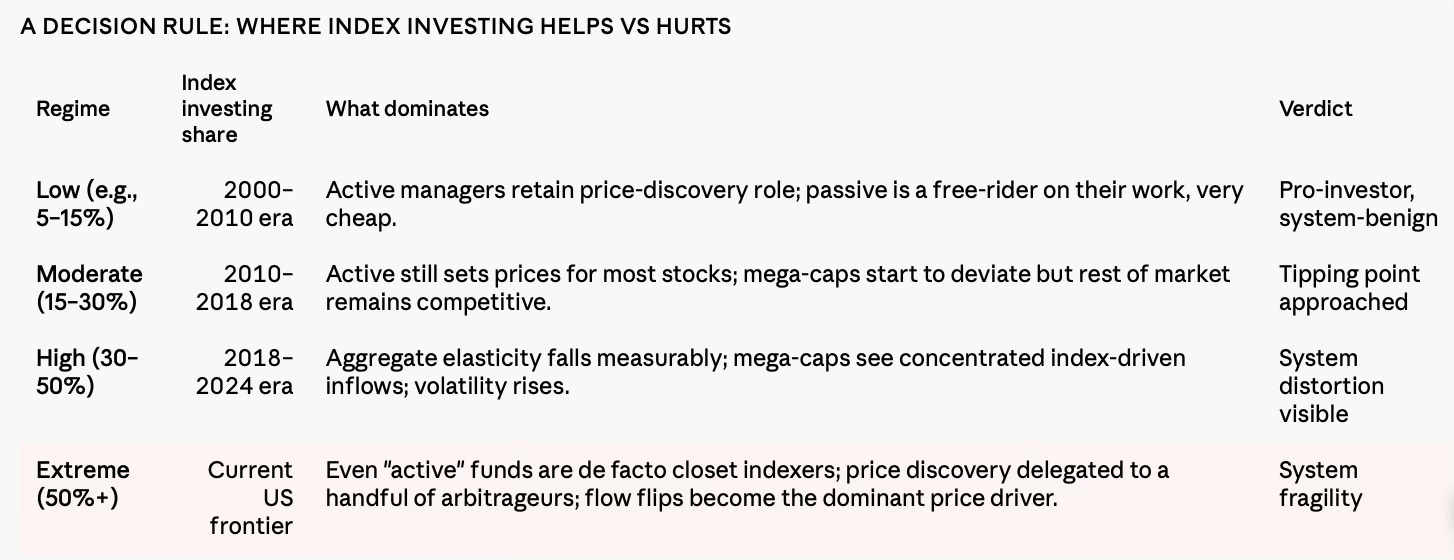

All things taken together, index investing must reconcile the conflicting requirements of democratising investing (through passive funds) and limiting market instability. The answer lies in the empirical fact - the more capital becomes index-tracking, the less price discovery the market performs, and the more the system is exposed to flow-driven valuation and procyclical unwinding. Clearly what is optimal for individual investor is not optimal for market function. In the circumstances, this can be an illustrative framework to reconcile the conflicting requirements.

The problem with index investing is that of internalisation of its negative externalities. Passive investors capture the upside of cap-weighted indexation (low fees, diversification, momentum) without bearing the price-discovery cost, whereas active investors bear the cost of analysis but cannot compete on fees.

This free-riding can be resolved only if passive investors internalise the marginal cost they impose on the system without eliminating the substantial benefits they deliver to retail investors. Like with carbon emissions, this can be done through fees, governance obligations, or structural caps.

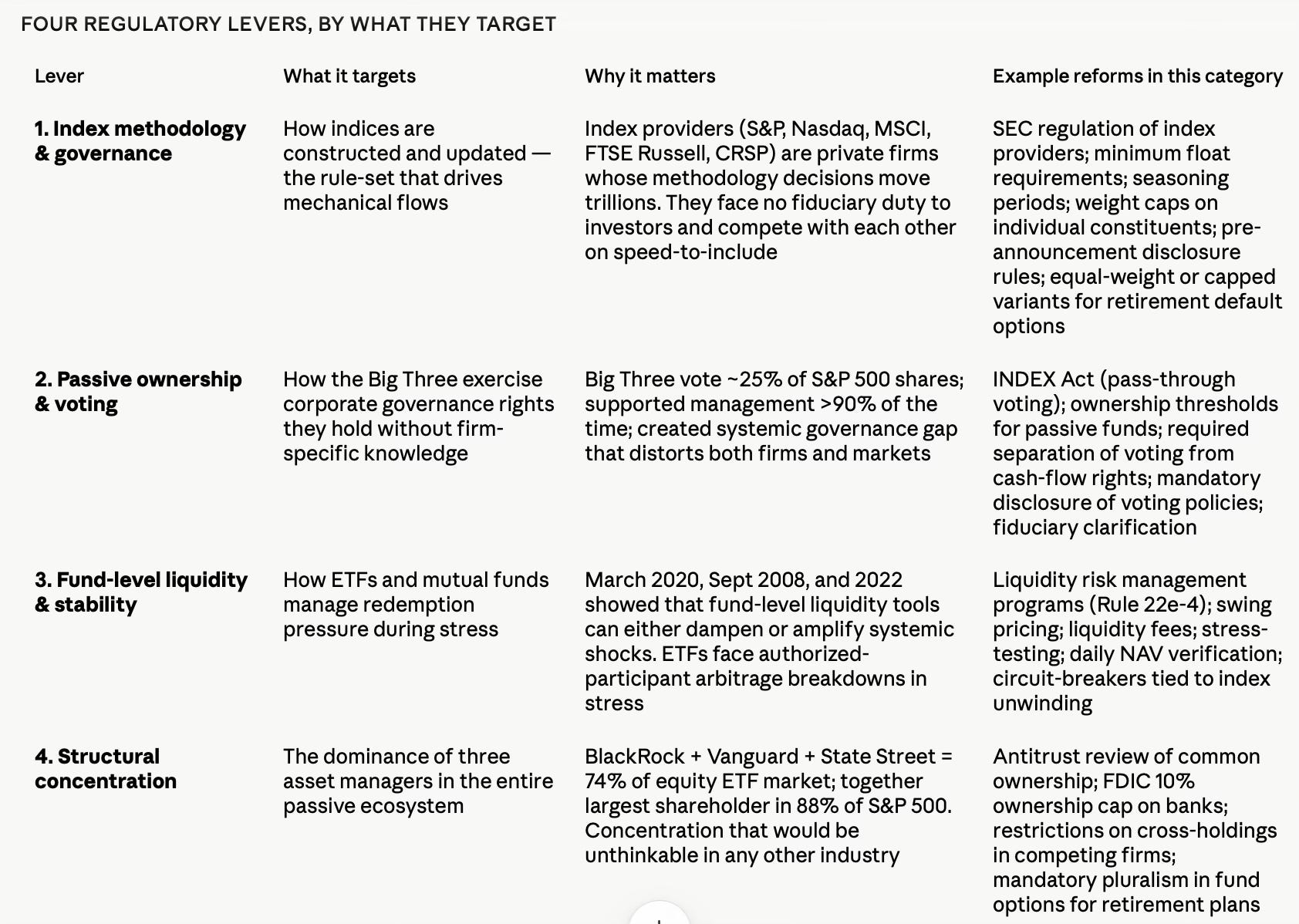

To dive a bit deeper, there are perhaps four levers for reforming index investing - index methodology (rules of index construction), voting and governance obligations, fund-level liquidity thresholds, and limiting structural concentration in the passive investment ecosystem. A combination of all of them is a formidable regulatory toolkit.

Each lever will have its set of reforms. It may be required to prioritise a limited set reforms that have the highest-impact-per-cost. The simplest and highest value reform could be mandatory free float minimums (say 10-15%), a twelve-month public trading history before index inclusion, and a 4-5% cap on any single stock in an index. Second, bring index providers under SEC regulation as “investment advisers” subject to fiduciary duty and disclosure requirements.

Third, for passive funds with more than 1% holding, return governance to the ETF or index fund holders by allowing them to vote their proportionate share directly via the fund, thereby reducing the influence of the Big Three asset managers. Fourth, cap the passive fund ownership of US banks at 10% (the regulatory "controlling interest" threshold) and impose mandatory liquidity stress tests for funds with more than $5 bn AUM in cases of extreme outflows and market dislocation.

Fifth, the Department of Labour should tighten defined-contribution retirement-plan portfolio diversity rules, thereby providing a structural counterweight to cap-weighted default portfolios. Such plans must offer either equal-weight or capped-weight default or cap cap-weighted defaults at e.g. 80% of the plan portfolio. This would reduce forced concentration in 401(k) default portfolios. Finally, there could be regulatory roadmap for orderly winding-down of overweight positions during the life-cycle or retirement transition. A coordinated guidance, including some rule-based gradual decumulation, reduces fire-sale risk.

The proposals above seek to reconcile the diversification and fee benefits of indexation while also internalising its costs. Once index providers face fiduciary duty, once Big Three votes are partially passed through, once retirement defaults include non-cap-weighted options, once liquidity is stress-tested, and there is some transition guidance, the same products can continue to serve retail savers while delivering far less of the distortion that has been documented.

No comments:

Post a Comment