China’s weaponisation of its manufacturing dominance, most famously through its control of rare earth magnets production, is generally accompanied by a narrative of resignation that its trading partners must live with this reality till they develop alternative supply chains. It is widely perceived that China has a definitive upper hand, and all other countries, including the US, must play catch-up.

This begs a few questions. Isn’t China susceptible to imported products and services that are essential to its economy? Aren’t there rare earth equivalents that the US and Europe can restrict access to China, thereby bringing a bargaining equivalence between the two sides? What are those rare-earth equivalent dependencies for China today? What is the economic leverage that the West has over China that can be exercised in response to the rare earths restrictions?

This post will examine this question in greater detail.

In a 2025 G-7 summit, the European Commission President Ursula von der Leyen aptly described China’s industrial policies as creating a pattern of “dominance, dependency, and blackmail”.

Having built up dominance and dependency, the blackmail is now intensifying. The hide your strength and bide your timephase is past. In the recent past, China has come up with several measures to leverage its dominance.

China’s widely known weaponisation of its manufacturing dominance has been underpinned by a series of regulations that impose restrictions and penalties. Pre-empting efforts by Western multinationals to diversify away from China, in April this year, to “prevent security risks in industrial and supply chains”, the State Council issued Regulations on Industrial and Supply Chain Security to investigate and punish foreign firms that stop using Chinese suppliers in response to political pressure from their governments. This is a summary.

Under the new rules, regulators can question employees and examine corporate records during investigations. The regulations also allow the authorities to bar companies and individuals from leaving China if they are suspected of moving supply chains elsewhere under foreign pressure… The State Council, China’s cabinet, justified the measures as necessary to protect the country’s economic stability and national security… China’s global network of ports and port-management software gave Chinese officials detailed insight into multinationals’ supply chains, allowing them to detect when companies shift to suppliers elsewhere.

In February, it amended the state secrets law by broadening the scope of the type of information that would be considered a national security risk. It includes a new legal concept called “work secrets”, defined as information that is not an official state secret, but that “will cause certain adverse effects if leaked”. This broad sweep allows for interpretation as convenient for the government, and makes foreign companies and their employees further vulnerable.

The restrictions are not confined to foreign companies. In early June, the State Council announced rules requiring national security screening for Chinese companies seeking to invest overseas.

The rules also give the authorities new powers to scrutinize Chinese companies seeking opportunities abroad, subjecting them to national security reviews that place investments into one of three categories: encouraged, restricted or prohibited. Part of the motivation for this, lawyers say, is to keep money, talent and intellectual property in fields where China has a competitive edge from leaving the country… The measures restrict the movement of certain talent in sectors deemed sensitive, though Beijing has not defined which sectors qualify. They also give officials broader authority to review the movement of capital, including the power to force investors to sell shares or halt investments if national security concerns arise. The rules also lay the legal groundwork for regulators to bar foreign entities from investing or operating in China, including expelling them from the country, in retaliation for actions taken by their governments against Chinese investments.

In this context, it is surprising that even as China increases its bellicosity both in trade and in its foreign policy, especially the breadth and frequency of military actions in the Taiwan Straits, the response from the West has been remarkably muted. Doubtless, the dysfunctional nature of the Trump Presidency has been a major contributor. But the lack of proportionality of response from the US holds, even including the Biden Presidency.

So what are the chokepoints and vulnerabilities that China faces from the West?

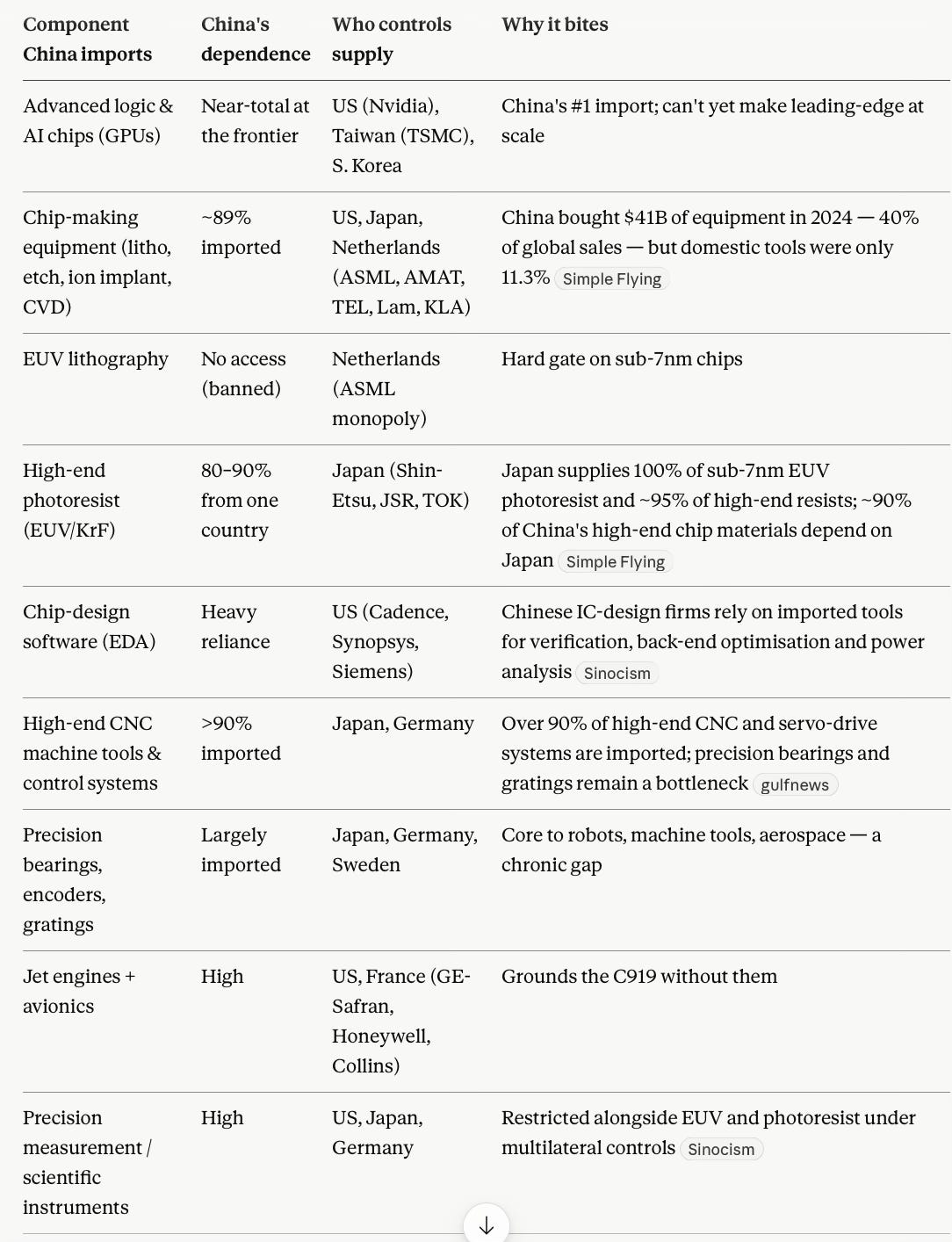

Ironically, China’s biggest vulnerability is in the very industry that it utterly dominates. China dominates the downstreamof electronics (assembly, packaging, volume manufacturing) and the upstream of raw materials (rare earths, gallium, refining), but it is deeply dependent on imports for the midstream - the tools and ultra-pure materials that actually make advanced chips. Underlining this reality, China imported $385 billion of integrated circuits in 2024, more than the $325 billion it spent on crude oil, making chips its biggest single import.

China's vulnerabilities cluster at the highest-precision, most knowledge-intensive nodes, the "tools that make the tools." Photoresist is the cleanest analogue to rare earths: a narrow, chemically exotic input where Japan holds a near-monopoly and a cut-off would, in one analyst's framing, leave Chinese manufacturing with "no rice to cook with". China could meet only about 5% of its own demand for the KrF resists used in 110–180nm chips, and high-end localization was under 5% in 2022. In simple terms, semiconductor equipment is the broadest lever by value, and machine tools are the most pervasive across general manufacturing. More than 60% of the indigenous passenger jet C919’s components, including engines and flight controls, are imported.

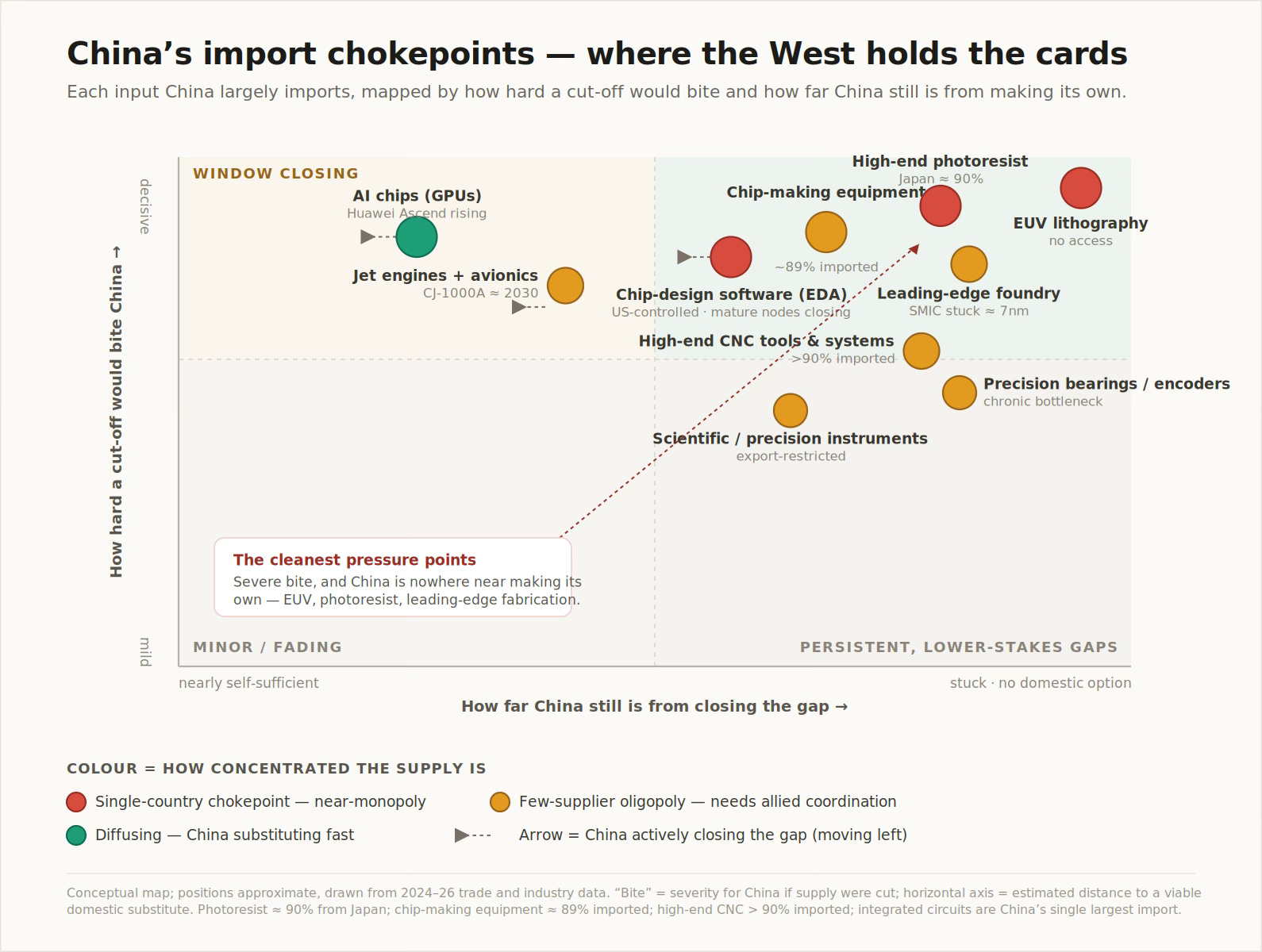

The graphic below plots the levers (or chokepoints) that the West have over China in terms of how hard it bites and how long it would take China to replace them. The colour represents the usability of the lever, without unacceptable self-harm; the dashed arrows show the levers China is actively closing.

The red bubbles (EUV, photoresist, EDA) are near-monopolies a single country can switch off. The amber ones (equipment, foundry, CNC tools, bearings, jet engines, instruments) are oligopolies that only work as leverage if allies coordinate, which is exactly why the US has spent two years building the Netherlands-Japan-Germany-Taiwan coalition rather than acting alone.

The West’s strongest cards (AI chips, EDA software, jet engines) are precisely the ones with a shelf life, because Beijing is pouring state money into domestic substitutes. The genuine bargaining equivalence lives in the top-right quadrant - frontier technology that bites hard and takes a decade-plus to replace (EUV lithography, leading-edge foundry).

It is to be noted that the arrows point left because it points to China travelling in the direction of self-sufficiency. It highlights that while real and binding today, there is a declining shelf-life or option value with these chokepoints.

However, having said this, any escalation risks retaliation. In 2025, the US suspended engine and EDA exports, China tightened rare earths, and within weeks, both sides walked it back into a one-year truce because each could hurt the other badly. It also points to the value of a bargaining strategy where the West gradually introduce restrictions on multiple such products where China depends on imports. The restrictions should be phased in carefully and subtly by plugging the procedural and process links that China exploits to its advantage.

In this backdrop, Ely Ratner and Nick Danby have a very good essay in Foreign Affairs that outlines the broad contours of a plan to identify and squeeze China’s vulnerabilities and do unto it what it is clinically doing by weaponising its strengths. The most obvious one is, as discussed above, to tighten the restrictions on access to the semiconductor chip supply chain.

China continues to leverage chip-smuggling networks, overseas data centers, and model distillation, a technique that exploits access to frontier AI models to replicate their capabilities. New policy measures should target the channels China uses to acquire restricted chips and supporting architecture, including shell companies and unlisted subsidiaries, as well as cloud-based access to U.S. computing power and servicing arrangements that keep older semiconductor manufacturing equipment operational. Equally urgent is synchronizing U.S. export restrictions with those of the Netherlands and Japan, whose companies—ASML and Tokyo Electron—control critical chokepoints in the advanced semiconductor supply chain. Although both governments began strengthening their own policies in 2023, their controls on equipment sales, servicing, and subcomponent exports to Chinese fabrication plants and toolmakers fall short of U.S. restrictions. Washington should press The Hague and Tokyo to close these gaps. If diplomacy fails, it should consider invoking the Foreign Direct Product Rule, which extends the extraterritorial reach of U.S. export controls to restrict products made with U.S. software or technology.

The authors also write that China’s huge export volume and $1.2 trillion trade surplus can be as much a liability as it is a strength, especially at a time when the economy is weakening and struggling for anchors of growth.

It should push back against China’s export surge by bringing advanced economies facing deindustrialization together with developing countries whose own manufacturing aspirations are being displaced. This coalition could then coordinate trade measures to protect their industries, including steel, shipbuilding, batteries, and drones. Alongside tariffs, the United States could pursue high-standard trade agreements that institutionalize requirements for subsidies, state-owned enterprises, and forced technology transfers that China cannot meet. Like-minded partners could also create an anticircumvention regime by strengthening rules of origin, sharing customs data, and imposing penalties on goods routed through third countries to avoid trade restrictions. They could further impose outbound investment screening to prevent companies or individuals in the United States and allied countries from financing Chinese capabilities that the controls seek to limit.

Notwithstanding its large reserves, for a country which imports three-fourths of its crude oil with 90% delivered through vulnerable sea routes, China is extremely vulnerable to energy security.

Below the threshold of a full blockade, the U.S. Treasury Department, through the Office of Foreign Assets Control, can use maritime sanctions to dissuade shipping companies, insurers, brokers, and banks from supporting prohibited shipments. Pressure on insurance, port access, and flag registration would raise costs and create uncertainty for China-bound tankers without requiring direct military action. The Pentagon should nevertheless demonstrate its ability to disrupt or interdict China’s seaborne energy imports by exercising U.S. naval control over key chokepoints along energy trade routes.

Commodity imports are another chokepoint

China imports roughly 80 percent of its iron ore, a foundation of its steel industry, predominantly from Australia. And most of its copper and lithium inputs, which are critical to battery and defense manufacturing, come from Australia, Chile, the Democratic Republic of the Congo, and Peru. As with oil, these dependencies offer additional pressure points that can be leveraged to strengthen deterrence and compound China’s challenges across multiple sectors simultaneously. If Australia were prepared to restrict exports of iron and lithium ore, and the United States and its partners had a plan to tighten access to copper and cobalt, they would send a message to China that its industrial base could be easily disrupted and its defense production capacity degraded if circumstances warranted.

Finally, the US dollar’s dominance is the nuclear option available.

Were Washington to restrict China’s dollar access—moving from sanctions on banks supporting PLA activities to broad limits on dollar transactions in advanced technology and military manufacturing—it could impose severe costs on Beijing, disrupting Chinese financial markets and potentially triggering wider economic instability… Washington must prepare for this scenario by first communicating unambiguously that only severely destabilizing acts would trigger consequences of this magnitude: for example, large-scale cyberattacks on critical U.S. infrastructure, Chinese export restrictions that seriously imperil the U.S. economy, or an armed attack against U.S. allies and partners.

The Cold War and trade tensions between the West and China are here to stay for the foreseeable future and are most likely to be ratcheted up over time. It is therefore important that others can mobilise sufficient bargaining levers with China. All the aforesaid are likely to be very effective in restricting the Chinese economy if deployed in a coordinated manner. This would require the mobilisation of a global alliance, something the US-led West did with great effectiveness during the Cold War with the Soviet Union.

Now, with the hostility and dysfunctionality of the Trump administration, any such cohesive and credible global alliance looks very unlikely. In its absence, whatever restrictions are imposed by the US and EU independently are merely band-aid solutions, and likely to get circumvented in various ways against an antagonist who is disciplined, plays the long game, and does painstaking groundwork to accumulate its strengths and overcome restrictions. Trump 2.0 is, therefore, perhaps the best thing that an embattled Chinese government could have been gifted by its opponents.

No comments:

Post a Comment