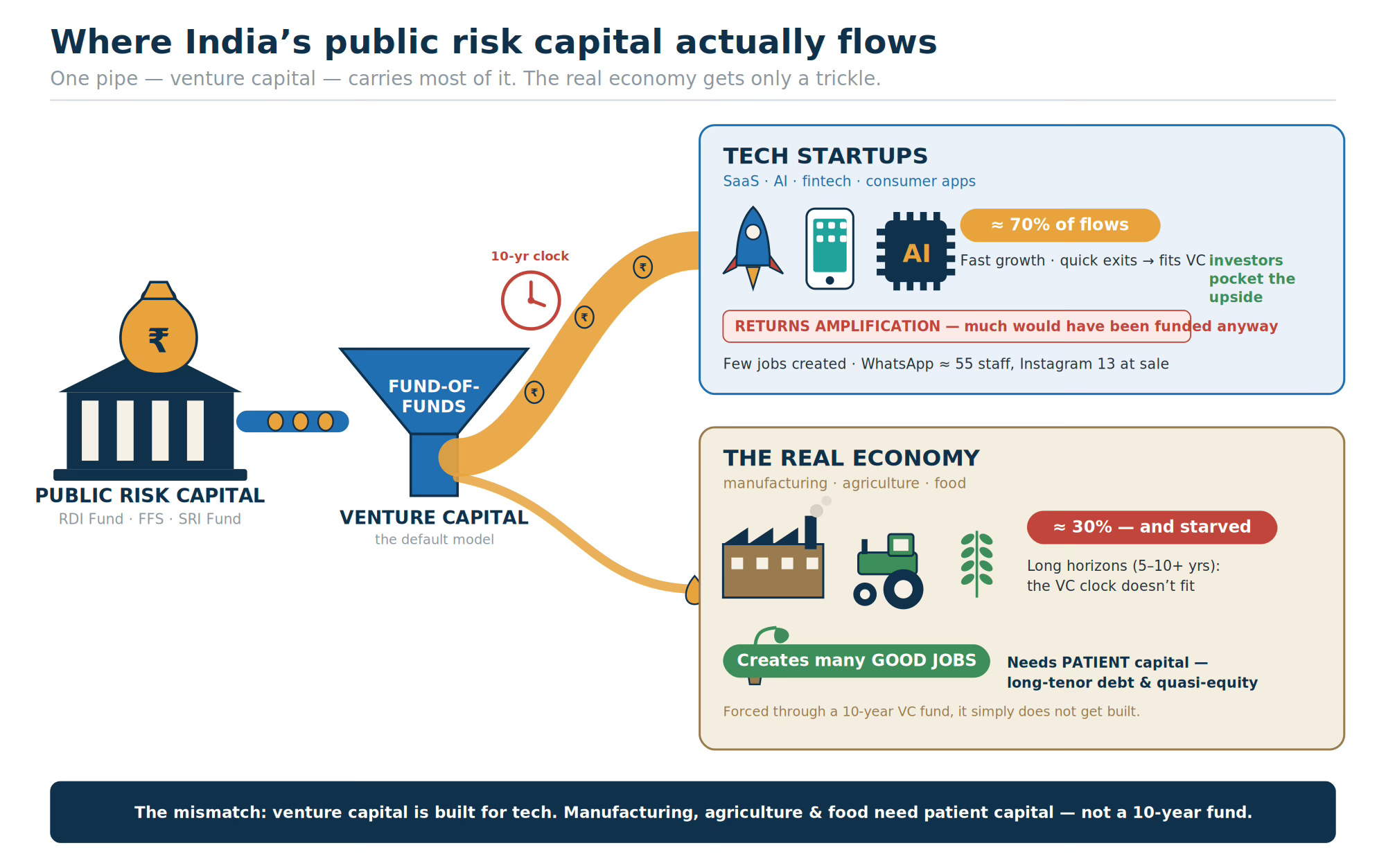

Public risk capital funding of innovation and startups in India is done almost entirely through the VC-driven Fund of Funds (FoF). The RDIF is only the latest effort.

However, as I have blogged earlier, there are two important concerns with public funding of innovation through the FoF approach.

One, would it primarily expand the investable universe of startups (genuine additionality) or primarily subsidise returns on investments that would have happened anyway (returns-amplification for private investors)? Second, would it prioritise scalable digital technology innovations at the cost of manufacturing and industrial innovations?

The evidence on both suggests returns amplification for private investors and the dominance of technology innovators. This should raise concerns about whether scarce public funds are being deployed most effectively. This post points to yet more evidence in this regard.

The Ken has analysed the performance of the Self-Reliant India (SRI) Fund, a Rs 50,000 Cr fund with 20% government contribution (the rest coming from VC and PE) to finance MSMEs, and found both concerns being validated.

The SRI fund model is described here.

SRI Fund is being implemented by NSIC Venture Capital Fund Limited (NVCFL), which is an Alternative Investment Fund (AIF) of Category II registered with SEBI. SRI fund is oriented to provide the funding support through NVCFL to the Daughter Funds for onward provision to MSMEs as growth capital, in the form of equity or quasi- equity, for the following:

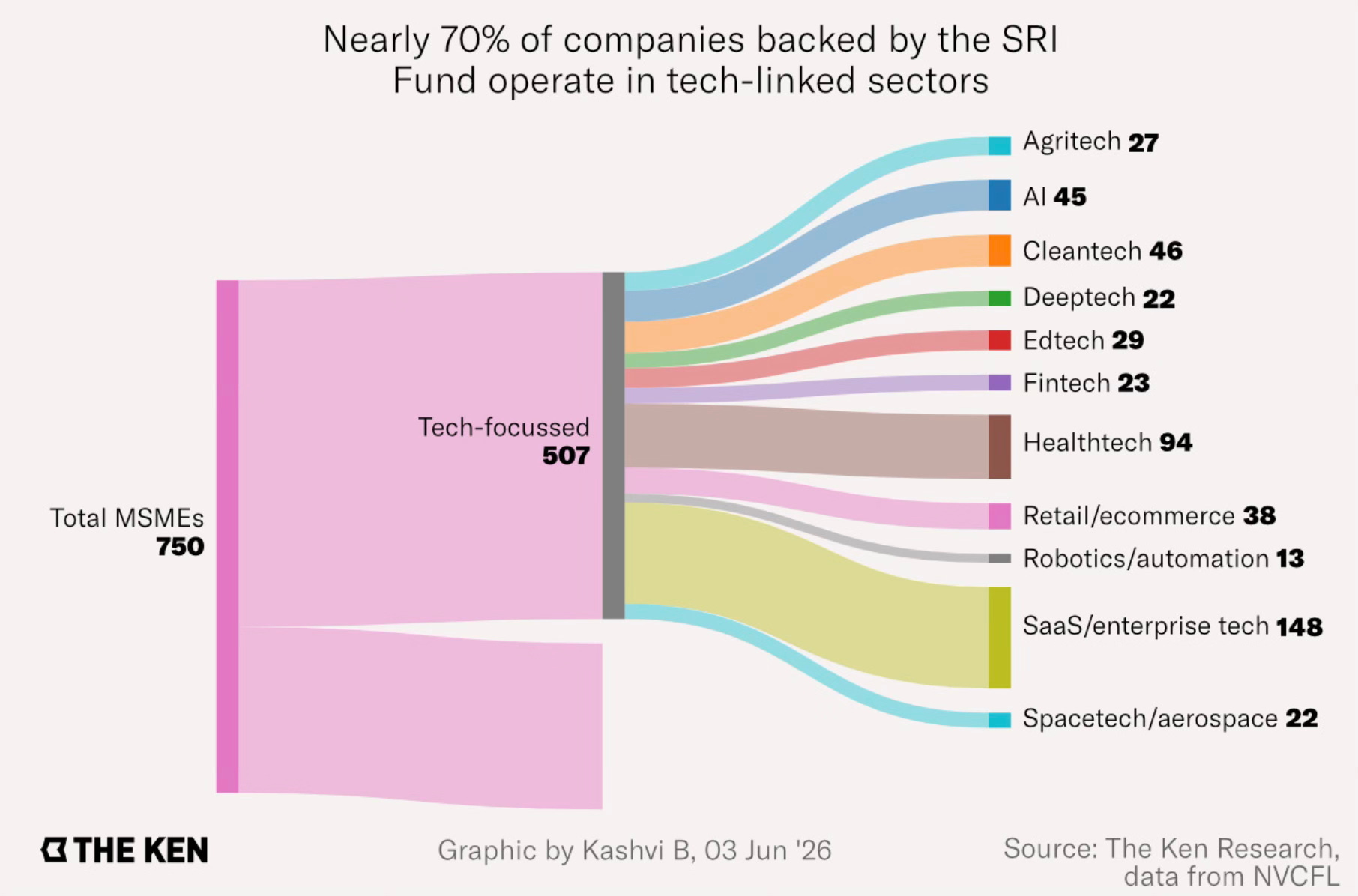

Since the start of the fund in 2020, it has backed around 750 companies and catalysed more than Rs 16,000 crore of investment.

Nearly seven out of every 10 companies it has backed are tech-heavy businesses. Only three are in traditional manufacturing… In fact, several of these companies had already been backed by VC firms before the SRI Fund got anywhere near them. Truemeds, for instance, is backed by Accel, Peak XV, and Westbridge, while Chai Point is backed by Eight Roads Ventures and Saama Capital. Understandably, this dims, if not outright flouts, the proposition of the SRI Fund, which was supposed to scope out companies “ignored” by venture capitalists…

“Fund managers get empanelled under SRI with the intention of backing underserved MSMEs,” said Ishaan Ajay, a development-and-sustainable-finance consultant. “But when faced with the choice between a profitable but slow-growing industrial supplier and a software platform capable of scaling rapidly, they tend to gravitate towards the latter. It’s what they understand the best.” Just consider the numbers. Suppose there’s a precision components manufacturer growing 15% annually with, say, 18% Ebitda margins. That may be a great business, but if you invest Rs 10 crore today, you’ll get only 2–3X your money over seven years. Contrast this with a spacetech company, which, if it succeeds, could be worth hundreds of crores.

“Venture funds are built around the second outcome,” said an analyst at a VC firm. This explains why SRI-funded companies tend to be tech-heavy. For every Bellatrix Aerospace in the portfolio, there’s an invisible machine-parts manufacturer outside it that was passed up… startups are generally more innovation- and tech-heavy, whereas MSMEs tend to be traditional, manufacturing-heavy businesses…

The government, for its part, tries its best to redirect funds towards their intended purpose. If it doesn’t agree with a fund’s investment choices, it expresses its objections, according to a VC with knowledge of the matter. But at the end of the day, it’s one LP among many. And when it can’t sway others, it ends up “recusing” itself from investing in that particular portfolio company, added the VC… “There is no prescription that a certain percentage of the fund must necessarily go towards traditional manufacturing or non-tech MSMEs,” a VC said. Which is the one thing that might have prevented all the confusion.

The point about returns amplification for private investors has also been highlighted in a study of IFC’s blended finance deals in the 2000-20 period, which found comparable financial returns to non-blended projects but “no statistically significant excess private mobilisation beyond what IFC’s standard lending would attract.” In other words, blending did not increase the quantum of private investment — it redistributed risk between IFC and private co-investors.

This finding is echoed in a 2023 study of SIDBI’s Fund of Funds for Startups (FFS) 1.0 by the Impact and Policy Research Institute (IMPRI), India’s Startup Engine: A Policy Review of the Fund of Funds Initiative. It finds that most FFS 1.0 capital went to established VC funds that would have raised capital independently. It also found that “crowding-in effect was primarily reputation/signal, not financial additionality”; the government’s involvement functioned more as a validation of fund managers to private investors than as a necessary injection of capital. While FFS 1.0 delivered a 2x mobilisation ratio, it was mostly in already-functioning VC markets.

As I have blogged several times, the startup and innovation sector is going through the same journey that the infrastructure sector has undergone over the last three decades. Multiple policy experiments to catalyse DFIs - IDFC, IIFCL, NIIF, and now NaBFID - have struggled to crowd in private capital into the riskier infrastructure segments like water supply and sewerage, mass transit, solid waste management, street lighting, energy-saving companies, electricity distribution, etc. Instead, these institutions and instruments may have ended up competing and crowding out private capital in the entirely derisked segments of the infrastructure sector.

In this context, it is also useful to ask the question whether the VC model is the right instrument for the funding of non-technology startups and innovations.

Livemint has two long reads that describe the emergence of consumer food brands catering to the niche category of health-conscious people. Sample this

The past few years have seen a spurt in new food brands specializing in regional staples and cooking ingredients. From rural Bengal winter specialty date palm jaggery (nolen gur) to ancient emmer wheat flour (Khapli atta) from Maharashtra, regional staples are finding customers beyond their states of origin. Some brands like Gurugram-based Anveshan and Two Brothers Organic Farms from Pune have crossed a critical mass, with annual sales close to ₹200 crore in 2025-26… Anveshan sources ingredients from key growing regions—like Pollachi in Tamil Nadu known for its high-quality coconuts and aromatic varieties of groundnut from elsewhere in Tamil Nadu and Karnataka—suited to make cold-pressed oils. The ghee, made from the milk of native breeds like the Gir from Gujarat is made using the traditional bilona process where milk is first set to curd and later churned to separate the butter (this has resulted in a new category called ‘cultured ghee’)…

Venture capital funds are betting on these brands: in September last year, Two Brothers raised a $15 million round taking its total fundraise to $25 million (and its post-money valuation to $85 million or ₹781 crore as per data from market intelligence platform Tracxn)… In April this year, KisaanSay, which markets single-origin grocery items like cardamom from Idukki and black raisins from Nashik, raised ₹34 crore ($3.6 million), taking the total funding at the Gurugram-based startup to $5.6 million since it was set up in mid-2022.

In a way, these brands have also helped promote traditional farming practices with more farmers returning to heirloom grain varieties such as the fragrant, short-grain Kala Namak rice grown in eastern Uttar Pradesh and emmer wheat in Maharashtra and Karnataka. These grains have a low glycemic index (a measure of the spike in blood sugar levels from carbohydrate intake) making them suitable for diabetics and often have higher protein and fiber content compared to conventional hybrid varieties… Three distinct factors—growing consumer willingness to pay for clean food driven by a surge in lifestyle diseases, the rise of quick commerce (allowing brands to quickly test consumer response), and influence of social media platforms are reshaping the premium staples market.

All these businesses are distinct from the rapidly scalable technology startups. Take the story of the Two Brothers Organic Farms.

They use organic farming and traditional methods of primary processing to make ghee, jaggery, Khapli flour, and cold-pressed oils. The jaggery is made using native sugarcane with lady finger extract used as a coagulant. “In Khapli, we have created a revolution. We own a seed bank and pay farmers 2.5-times the price of regular wheat. More than 800 farmers grow this wheat for us in 3,000+ acres,” Satyajit said. “It took us ten years to build this brand. At the back-end, our farms are open to everyone (to visit). Consumers trust us and we have a 70% retention rate. But a proliferation of brands (offering traditional, hand-processed staples) also carries the risk of a dilution in quality standards,” he added with a note of caution.

Much the same can be said about most businesses outside of technology - food, textiles, footwear, manufacturing, recycling, etc. Building these businesses requires painstaking efforts for several years, and there are natural limits to their scalability. They are unsuitable for the VC model of funding, as the second Livemint story about the plant-based nutrition startup Oziva shows.

Venture funding, Aarti Gill (co-founder of Oziva) points out, comes with built-in expectations around exits within five to eight years. Unlike venture-backed software companies, consumer health brands compound slowly through trust, habit and repeat behaviour. “If you have investors willing to stay for 10 or 15 years, that changes the equation completely,” she adds. Gill broadly sees three paths for consumer brands: staying profitable and scaling independently over a long period, going public after reaching meaningful scale, or partnering strategically with a larger company. For Oziva, the third route eventually felt like the most practical one. And, that’s where HUL came in… For Oziva, the partnership offered distribution scale, capital and the ability to build beyond a digitally native audience.

Therefore, at a conceptual level and as a framework, it may be a prudent choice for public policy on the funding of startups to distinguish between technology and non-technology sectors. While VCs are appropriate for technology, with their smaller and rapid growth phase, the same may not be appropriate for non-technology startups, which require longer incubation and growth periods. However, in India, most public risk capital funding happens through the VC-driven FoF strategy, which raises concerns of returns amplification and a preference towards technology startups and innovations.

This is also a concern since technology innovations, far from creating jobs, often also tend to destroy jobs, whereas the non-technology innovations, especially in manufacturing, create good jobs. The graphic below captures the problem.

Note: The percentage breakup is probably even more skewed in favour of technology startups.

It also raises the question of effective strategies - instruments and institutions - for funding such non-technology innovations. How are such innovations funded globally? Are there institutional structures in India (state or central governments) that offer promise and can be adopted with tweaks? What are the lessons from the likes of the Maharashtra Aerospace and Defence Fund? What are actionable recommendations on funding of non-technology startups? If it also requires the government to directly fund them, what institutional structures are most practical and realistic? I’ll explore these in another post.