While most of the attention has been focused on addressing the flood of Chinese manufacturing imports, another issue that is rapidly emerging as a matter of concern is the rising Chinese FDI globally. The investment problem is rapidly emerging as an important issue, just as the trade issue. It is also an opportunity to ensure that opening up to Chinese FDI does not end up creating another dependency like that which has happened with Chinese imports.

The investment dimension assumes great importance given the rising wall of trade barriers that restrict access to imports from China. In many countries, this includes rising measures to trace and restrict trade re-routing through third countries to avoid barriers. Further, China’s near-complete dominance in industrial metals and many other manufacturing inputs, in addition to manufactured products, means that dependence on Chinese firms is unavoidable for the foreseeable future.

China’s sheer scale of production, especially its ability to supply metals and inputs at prices lower than almost anyone else, has pushed other producers and countries to the margins. This creates a real dilemma: if you try to restrict or control these imports, downstream industries struggle to survive due to higher costs; but if you don’t, dependence only deepens, and domestic capability erodes further. It’s a classic Catch-22, with no easy way out.

Complicating matters is the increasing strategic dimension of China’s manufacturing dominance. The former US Secretary of State Jake Sullivan has recently written that China is pursuing a theory of power that “places production, scale, and control of critical inputs at the centre of its national strategy”.

Chinese leaders are seeking to make the rest of the world dependent on China while making China independent from everyone else. And they have assessed that to achieve this, China does not need to lead in every frontier domain. Instead, it needs to control nodes of leverage—that is, the inputs and systems that advanced economies and militaries depend on to function. Beijing has already captured several of these nodes, including processed rare earths, precursor ingredients for pharmaceuticals, and batteries, and it is striving to capture others, such as robotics.

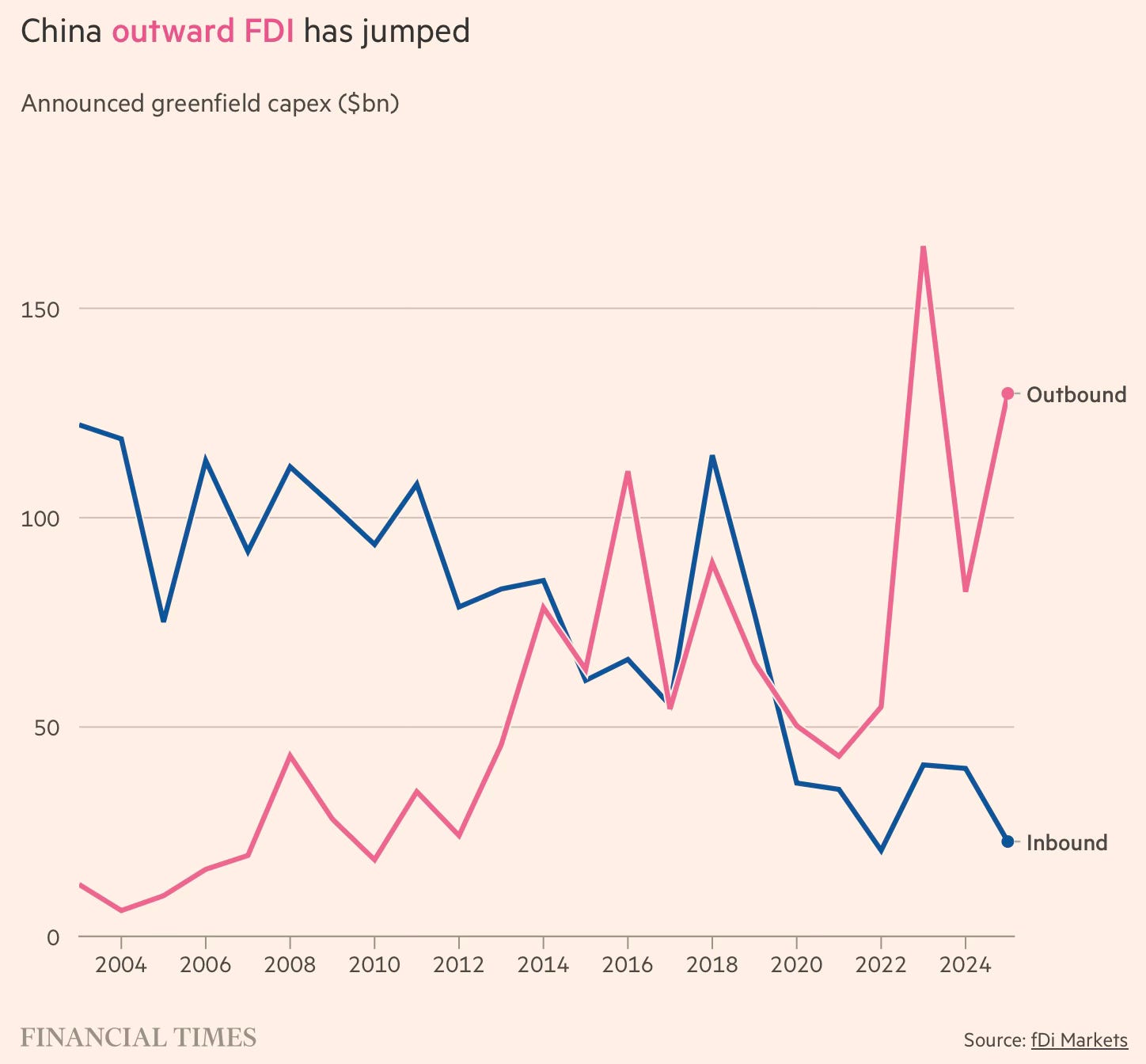

On the investment side, China is now a major outward investor globally. The graphic below shows that even as its inbound FDI has dived, China’s outbound FDI has surged.

Debashis Basu provides some interesting numbers.

With a cumulative overseas investment stock of $3 trillion-3.5 trillion and annual outflows in the range of $160 billion-190 billion, China is a major FDI player across every region. Asia absorbs close to 70 per cent of China’s outward investment stock — roughly $2 trillion-2.2 trillion — largely into Southeast Asia, where Chinese firms have transplanted entire manufacturing ecosystems, particularly in electronics, textiles, electric vehicles, and intermediate goods. Latin America is the second major destination, with a cumulative Chinese investment estimated at $300 billion-500 billion. Europe, while smaller in share, has still absorbed between $100 billion and $200 billion. Africa, though accounting for a smaller share — perhaps $50 billion–100 billion — occupies a strategic position. West Asia, meanwhile, has attracted multi-billion-dollar annual investment in energy, petrochemicals, and, increasingly, renewables.

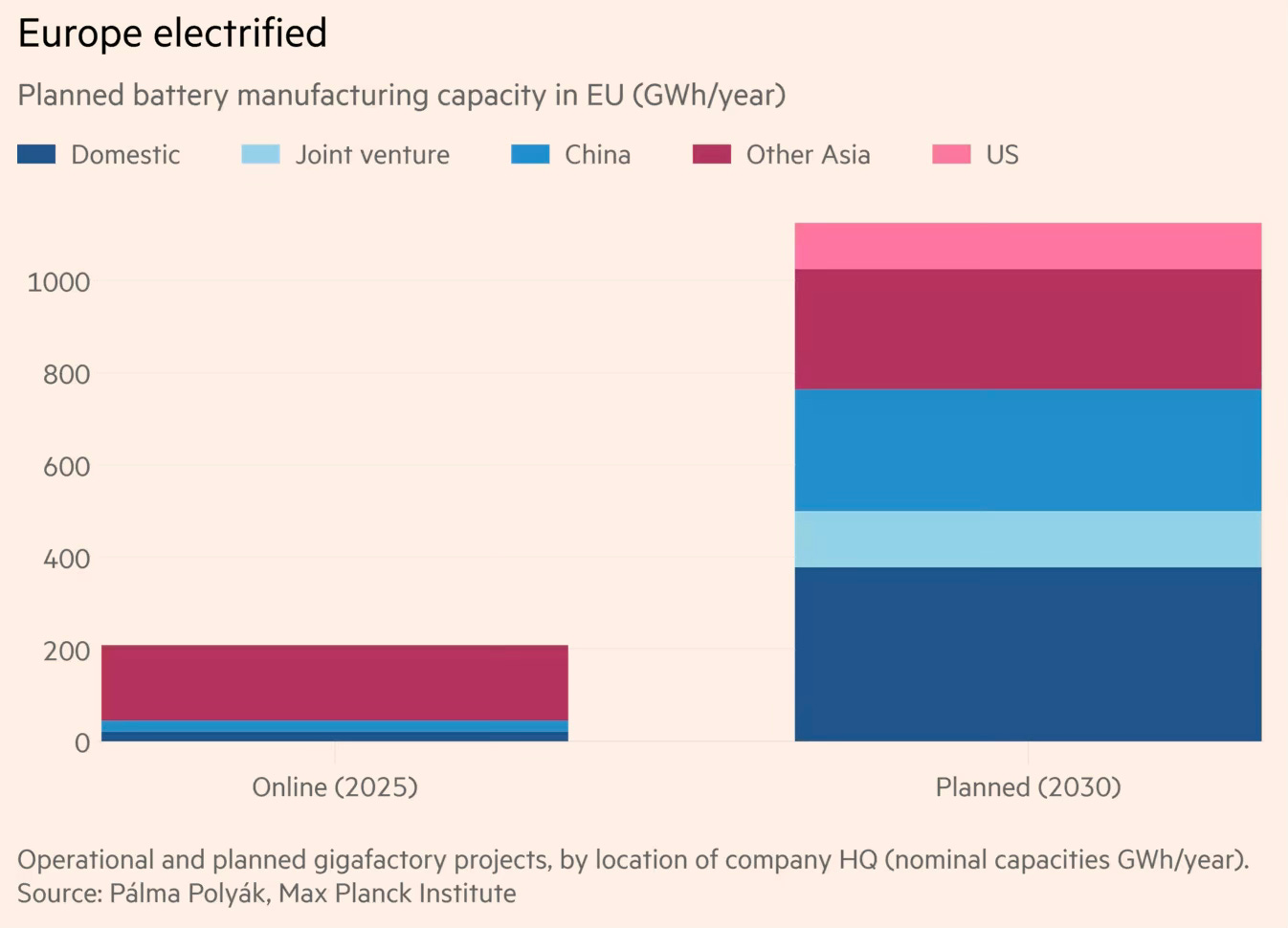

While the US under President Trump has gone the way of imposing strict restrictions, others, including the EU, have been grappling with wooing Chinese FDI, but with conditions. In fact, the EU has emerged as Ground Zero on this issue. Electric Vehicles and battery manufacturing are the most high-profile examples.

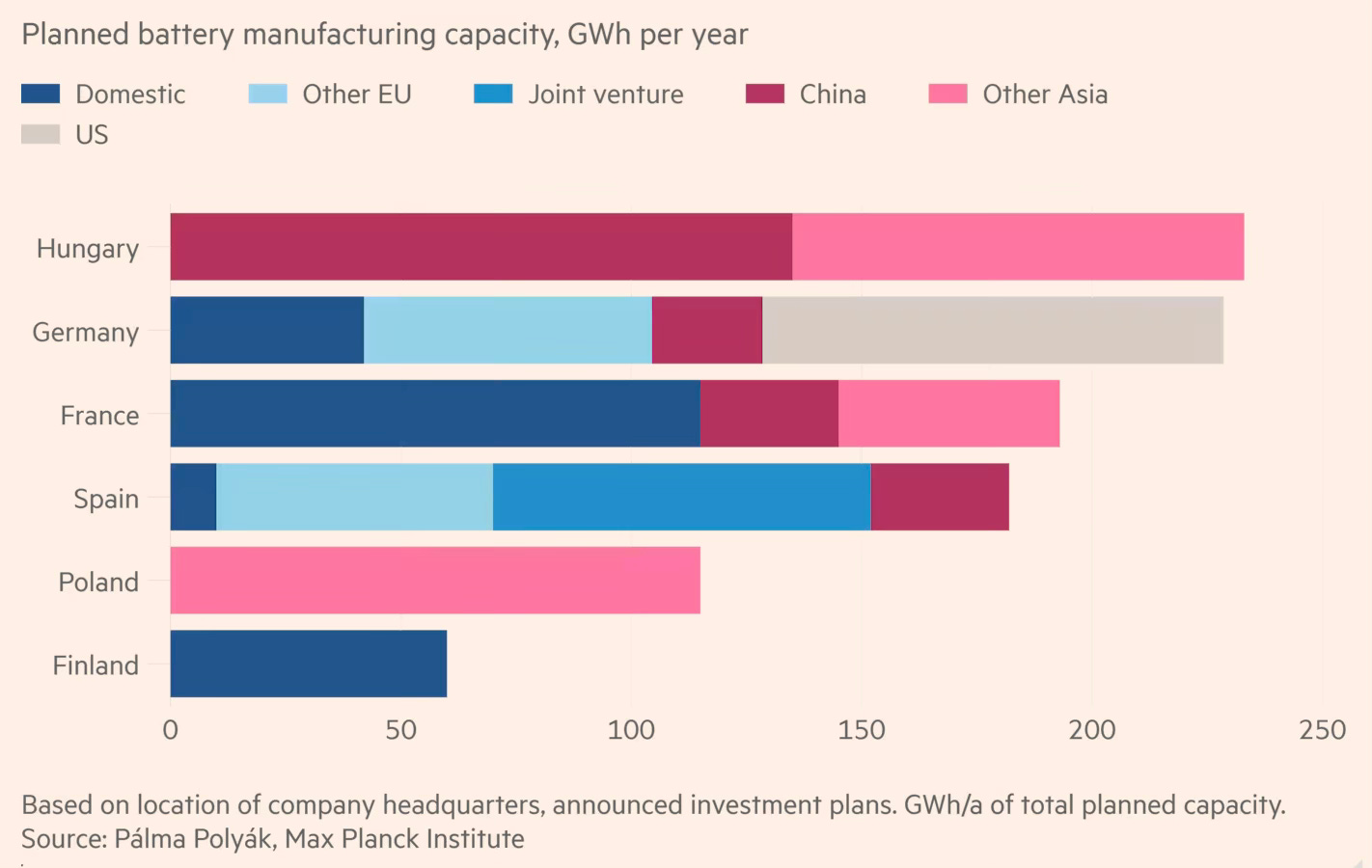

Complicating matters is a collective action problem. While the EU as a whole commits to striving for reducing supply chain dependencies, individual members have an interest in benefiting from Chinese FDI and allowing their countries to be used as the source for exporting to the EU common market area. This has played into China’s hands, as it has pushed low-value-added assembly into these countries. Viktor Orban’s Hungary and Pedro Sanchez’s Spain have been the two Trojan horses for Chinese FDI into the EU.

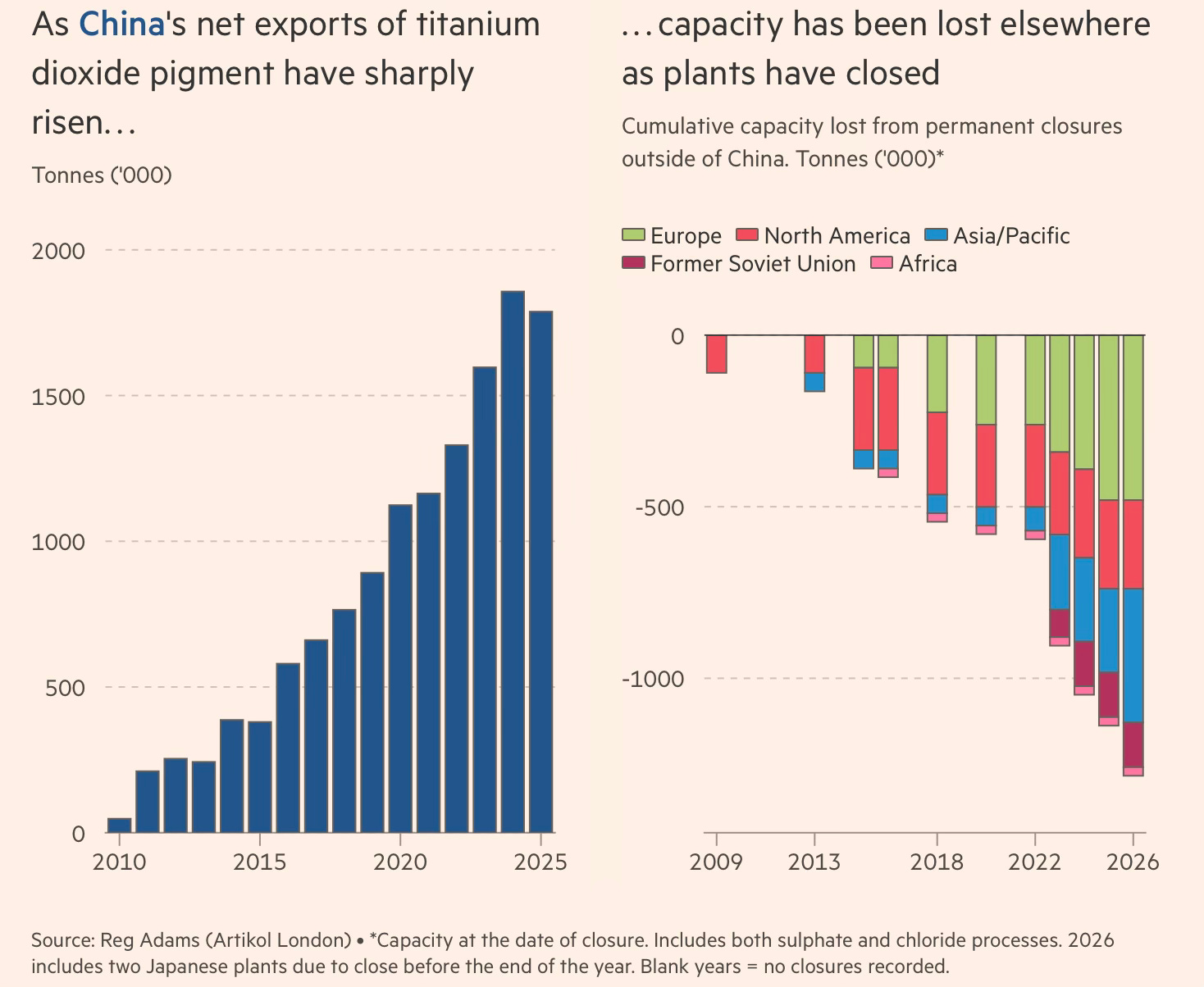

Another example is the UK’s decision to allow China’s Lomon Billions (LB) Group, the world’s largest producer of titanium dioxide (TDO), to buy a bankrupt TDO plant in Teesside owned by Venator Materials UK for $70 million. The Teesside plant went into administration last October with the loss of 270 jobs after more than 50 years making TDO, an industrial whitening agent used in paints and plastics as well as strategic defence and green energy supply chains. TDO is also an input to make titanium metal, a key component in the defence industry.

The deal has faced strong criticism from European and US TDO producers who fear that the LB Group will use the plant as a source to flood the European markets with cheap TDO and drive out its manufacturers. As an illustration, the LB Group produced titanium dioxide at $1,500 a tonne in China, including subsidies, nearly half the estimated $2,800 a tonne cost to produce in the UK.

The scenario posed by critics is real since TDO is a good illustration of how cheap Chinese exports have destroyed manufacturing capacities globally.

LB Group produced titanium dioxide at $1,500 a tonne in China, including subsidies, nearly half the estimated $2,800 a tonne cost to produce in the UK... China became a net exporter of titanium dioxide after 2010, with exports rising from just 48,000 tonnes that year to more than 1.7mn tonnes in 2025, creating a global glut of excess production that coincided with a wave of factory closures outside China. Over those 15 years, factories with a combined capacity of nearly 1.3mn tonnes were shut down in Asia, Europe and the US, according to data compiled by industry analyst Reg Adams, who has tracked titanium dioxide markets since 1993. Chinese capacity hit 5.7mn tonnes at the end 2025.

In fact, the LB Group has made explicit its market strategy.

“By establishing new factories overseas, the company can directly connect with end-markets for production and sales, radiate out to surrounding markets . . . and circumvent high anti-dumping duties.”

The challenge then is to manage Chinese FDI in a manner that it does not end up replacing one dependence with another, Chinese imports with Chinese firms. Instead, the objective should be to use Chinese FDI to build domestic capabilities and reduce reliance on China’s supply chain.

This is going to be easier said than done. Chinese investments are unlikely to come cheaply.

Since President Xi Jinping has already made it clear that China sees supply chain dependence as a strategic security lever (or “weaponised”), Chinese firms will obviously resist and stonewall efforts to use interdependence them to reduce supply chain dependence. In the circumstances, this is going to be a game of cat and mouse where the best that can be expected is a long drawn series of extractions and concessions. China’s FDI hosts should strive for two steps forward and one step backwards.

So what are the strategies being pursued by countries to attract Chinese FDI?

The most comprehensive action plan has been outlined by the EU. The EU’s recently announced Industrial Accelerator Act (IAA) aims at increasing European manufacturing competitiveness and reducing supply-chain dependencies, and includes provisions to exercise control over foreign investment. Member states can veto any FDI exceeding €100mn in strategic sectors if the investor is from a country with more than 40 per cent of global manufacturing capacity.

Further, these FDI projects must fill at least half of their jobs with EU workers and satisfy three of five other conditions. The five conditions are a 49% limit on foreign ownership or voting share, a joint venture structure of the investment with EU partners, licensing of IP and technology to the EU target or asset, incur R&D expenditure of at least 1% of gross annual revenue within the EU, and source at least 30% of inputs from the EU.

An FT article nicely sums up the backdrop for the announcement of IAA.

The law is seen as the EU’s answer to decades of practices in China requiring foreign companies to invest alongside joint-venture partners and transfer their technology to local manufacturers. As Chinese manufacturers have acquired technology and been able to make higher-value products, rivals in Europe complain that they can no longer compete.

China has predictably reacted strongly to the new law and threatened countermeasures. This response is delightfully ironic in coming from a country that did the same for nearly three decades in its journey to establish manufacturing dominance. China’s commerce ministry put out a statement

…runs counter to basic market economy principles such as commercial voluntariness and fair competition… the act violated a range of WTO principles and international agreements governing intellectual property rights and subsidies… It will drag down the EU’s green transition process, damage fair competition in the EU market and bring new shocks to multilateral trade rules… (the EU should delete) “discriminatory requirements against foreign investors, local content requirements, mandatory transfer of intellectual property rights and technology requirements, public procurement restrictive policies, and other content.

There’s a deep irony in these measures coming from Europe, and they also represent the wheel turning the full circle. In their early years of industrialisation, the US and Europe pursued infant industry protection policies to build domestic manufacturing capabilities. Once they became dominant, they embraced the principles of free trade and forced developing countries to lower tariffs and open up their markets. Now, having given up their manufacturing dominance to China, the same countries are back to pursuing protectionist policies to safeguard their industries from Chinese competition.

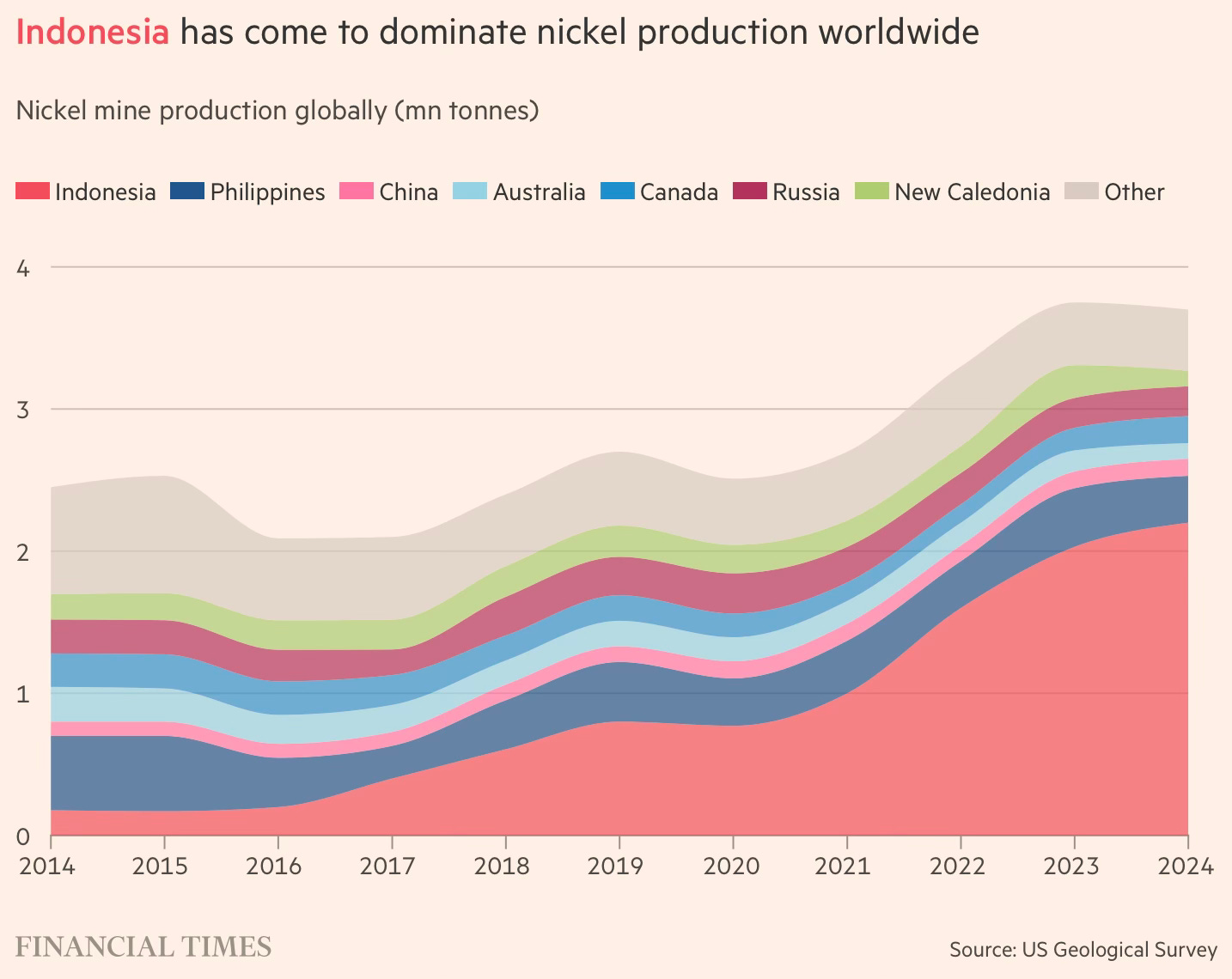

Another example of Chinese investments that should be watched with interest is that made in Indonesia’s nickel processing and refining, and now being made in the same country’s alumina processing and aluminium manufacturing.

In 2014, Indonesia banned the export of raw Nickel, with a total ban from 2020, thereby encouraging Chinese companies, led by the steel giant Tsingshan Holding Group, to set up processing plants across the country. The transformation since has been remarkable for a country that, a decade ago, was not even a major nickel producer.

Although Indonesia held the world’s largest reserves… most of it was low-grade nickel that it had not yet figured out how to process efficiently… Before 2014, most of Indonesia’s nickel ore was sold to nickel and steel manufacturing plants in China… Huge investments came from Chinese steel, nickel and battery manufacturers, including Tsingshan, CATL and Lygend, who partnered with Indonesian mining companies to set up processing facilities. Chinese stakeholders control over 75 per cent of Indonesia’s refining capacity, according to a recent report by C4ADS, a Washington-based security non profit. Not only did the companies bring capital, they also brought the knowledge to process Indonesia’s low-grade nickel reserves quickly and profitably… The Chinese had made advancements in rotary kiln electric furnaces, which turns nickel ore into raw material for steel. They had also mastered the high-pressure acid leach technology, a refining process that converts low grade nickel ore to battery-grade — a procedure that western companies had struggled with for years…

Indonesia has gained control of the market and cemented itself as the epicentre of global nickel production for years to come. Last year, Indonesia accounted for 61 per cent of the global refined nickel supply up from just 6 per cent in 2015… Its market share is expected to grow to 74 per cent by 2028. This means Indonesia now controls more of the world’s supply of nickel than Opec did of oil at the cartel’s peak in the 1970s — then around half of global crude oil output.

And it has achieved this position of market dominance just at the moment when new customers are desperately trying to secure reliable supplies. Not only are carmakers like Tesla, Ford and Volkswagen racing to source the metal for lithium-ion batteries, nickel is also widely used in smartphones and other electronics — as well as being a vital ingredient in stainless steel… Surging production in Indonesia has wiped out competition from companies such as Australian mining group BHP and dramatically reshaped the global supply chain. By flooding the market and driving down prices, the Sino-Indonesian partnership has made it much harder for rivals to produce the metal economically elsewhere in the world.

Similarly, in 2023, Indonesia banned the export of bauxite, the mineral used to make Aluminium, forcing companies to establish domestic refining (bauxite to alumina) and smelting (alumina to aluminium) facilities. Chinese processors, already facing restrictions on capacity expansion in China, moved to Indonesia to invest in the high-margin industry. A combination of Chinese production caps, sanctions on Russian smelters, closures in Africa and Australia due to rising energy costs, and now the damage to facilities in the Gulf has squeezed supply and is driving up prices. This, in turn, could accelerate Indonesia’s smelters build out, especially by the Chinese companies. The country produced 5.9mn tonnes of alumina last year, up from 3.3mn in 2022.

The Indonesian experiment with Nickel and Aluminium export bans and forced domestic processing, primarily with Chinese investments, is a test case for leveraging Chinese companies and their technologies. The extent of localisation and domestic value addition, and technology transfer and spill-overs that have happened in these two industries is not known. Clearly, given the strategic nature of these metals and the attendant leverage, the Indonesians may have missed a trick by not insisting on joint ventures with domestic firms.

Infrastructure is sometimes considered another destination for Chinese FDI. However, as I have blogged here, China is unlikely to undertake FDI in infrastructure. Instead, its primary channel for funding infrastructure is through loans to governments, as has been institutionalised through the Belt and Road Initiative (BRI). This channel is filled with pitfalls and problems that are well documented.

Even equity investments in infrastructure come with strategic risks. An illustration of this is that in ports.

Chinese firms now operate or have a financial stake in at least 129 ports outside China, and have spent at least $80bn on port construction from Antigua to Tanzania, with many of the investments tied to bilateral trade and regional shipping agreements. More than a third of China’s overseas ports are near maritime chokepoints, including the Strait of Malacca, the Strait of Hormuz and the Suez Canal, making them indispensable operators in strategic areas. China’s firm grip on global ports has rattled Western governments. MERICS, a think-tank in Berlin, found that after a terminal operating contract is signed, total trade with China rises by more than a fifth, while countries that allow Chinese firms to run all their terminals at one of their ports see a 19% drop in exports to the rest of the world. Operating ports allowed Chinese firms to prioritise their cargo and vessels and speed up customs and logistics...

China’s reach extends beyond physical infrastructure. LOGINK, a Chinese government-run logistics-management software, is used in at least 24 countries and 86 ports (America banned its use in 2023). LOGINK shares data with CargoSmart, another shipping-management software firm owned by COSCO, another Chinese state-owned firm, and in turn gives it access to the whereabouts of 90% of the world’s container ships. It also has a tie-up with CaiNiao, a logistics provider with hundreds of warehouses around the world... Chinese firms are also building industrial parks and manufacturing facilities close to their existing ports in Africa and Europe.

So what does all this mean for India?

Debashis Basu again provides these numbers on FDI from China.

Chinese FDI in India amounts to a trivial $2.51 billion, or 0.32 per cent of India’s cumulative equity inflows, since 2000. Even if one broadens the definition to include venture-capital investment and indirect flows routed through third countries, the total rises only to $15 billion-20 billion.

The Economic Survey 2023-24 also proposed that India should seek to attract Chinese FDI to benefit from the ‘China plus one’ strategy embraced by foreign multinationals seeking to diversify away from that country.

The challenge, like with all things in public policy, is about how to do it. For a start, it might be useful to study the EU’s IAA. It is important to prepare a multi-track strategy that places different conditions for sectors depending on their importance and the extent of Chinese dominance. I had blogged here outlining some mitigation strategies for India as it grapples with chokepoints in trade.

It must be a conscious strategy of attracting Chinese investors with some broad requirements and then gradually tightening the conditions to first increase domestic value addition and then gradually technology transfer to domestic suppliers. This will be a game of hardball, and India must be prepared to play it with China.

It has had opportunities to pursue this strategy earlier. In 2020, one analysis reported that 16 out of India’s then 29 unicorns had Chinese investors, with them being lead investors in eight. Tencent and Alibaba were the largest investors. As relations soured, these investors were forced out or left.

Basu’s description of how China itself courted foreign investment is appealing in theory, but very hard to execute for several reasons, especially given the current circumstances of countries having to deal with China.

Beginning in the 1990s and accelerating through the 2000s, China actively courted FDI and technology, particularly from Japan, the United States, and Europe, in a period known as “reform and opening up” (gaige kaifang). China did not see foreign capital as a threat; it saw it as an instrument of transformation if the state retained strategic control over direction. Multinationals were often required to form joint ventures, localise production, and, in many cases, transfer technology — the phrase “bring it in” (yin jin lai) capturing this mindset. To take full advantage of this, special economic zones provided infrastructure, policy stability, and export incentives, enabling China to integrate into global manufacturing networks and develop deep supplier ecosystems, skilled labour pools, and process expertise. China used this phase to absorb technology, build domestic champions, and gradually move up the value chain, eventually becoming both an exporter and an investor in the next phase — “go out” (zou chu qu).

I’m not sure that Chinese manufacturing firms will come in with low minority stakes just because of the Indian market size. Historically, it has not happened, even in much larger and more attractive markets like the US and Europe. And Chinese FDI has generally steered clear of India.

This strategy will require high institutional capabilities that track emerging FDI trends and global developments, and dynamically shape and steer India’s FDI policy, especially with respect to China (or countries with land borders). This will have to be quite a different approach from that which has generally been followed by India.

No comments:

Post a Comment