The Gulf War threatens to damage economic prospects on multiple fronts, especially on the external account, especially for oil importers. For countries like India, which are acutely dependent on imports of oil and gas, and that too from the Gulf, the increased oil prices translate into rising imported inflation, widening current account deficit, weakening rupee, and pressure to raise interest rate. A combination of all these puts pressure on the external account and leads to sudden stops (of capital inflows) and capital flights (capital outflows).

In response, economic orthodoxy advocates allowing the currency to depreciate and serve as the automatic stabiliser by squeezing imports and boosting exports. However, as Sachidananda Shukla writes, this is no free lunch. Allowing the rupee to fall runs the risk of steep declines due to overshooting, hurting investor confidence and weakening purchasing power. Episodes of sharp declines can dent credibility, whose recovery is easier said than done. As Mundell-Fleming’s Impossible Trinity shows, a country cannot pursue an independent monetary policy and hope for modest depreciation in the market for capital flows.

In this context, how does India’s external account stack up?

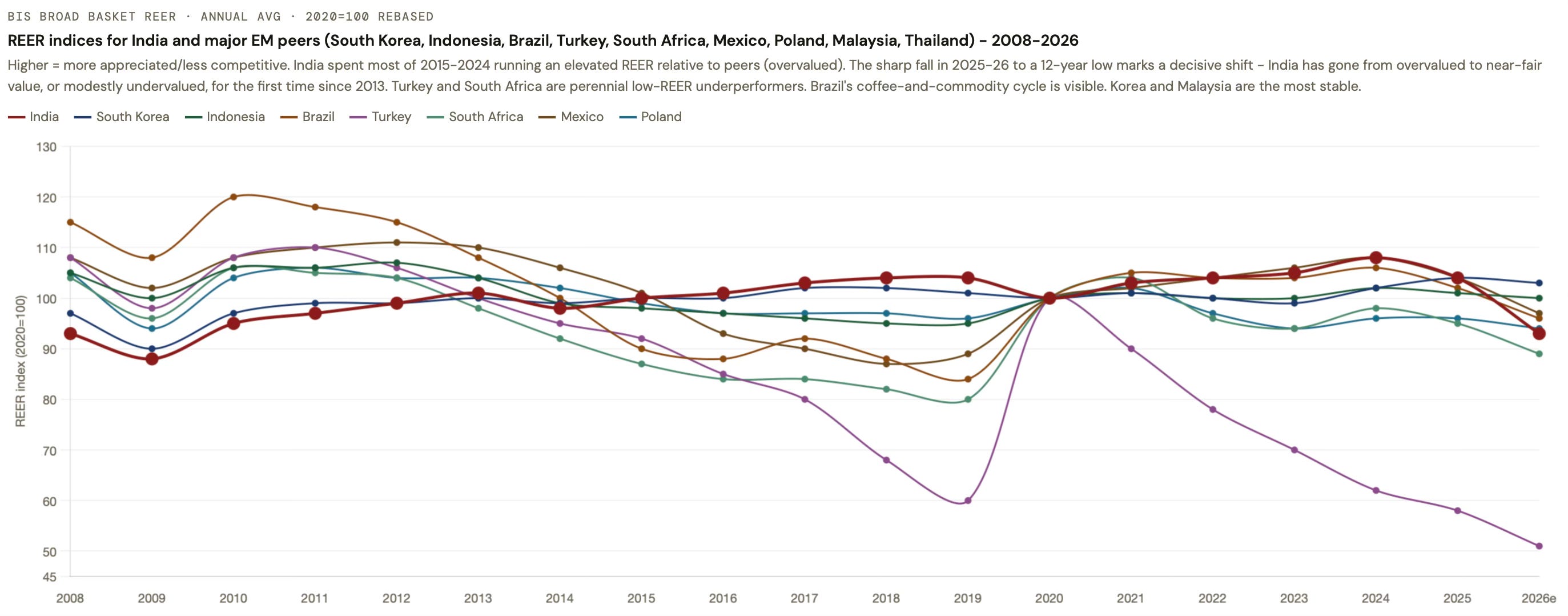

India entered the Gulf War with pressures building up on its external account due to net FPI outflows, zero net FDI flows, adverse global trade situation, and so on. Further, by maintaining the rupee overvalued for several years, there was no cushion available for calibrated depreciation. The only silver lining is the rising services exports.

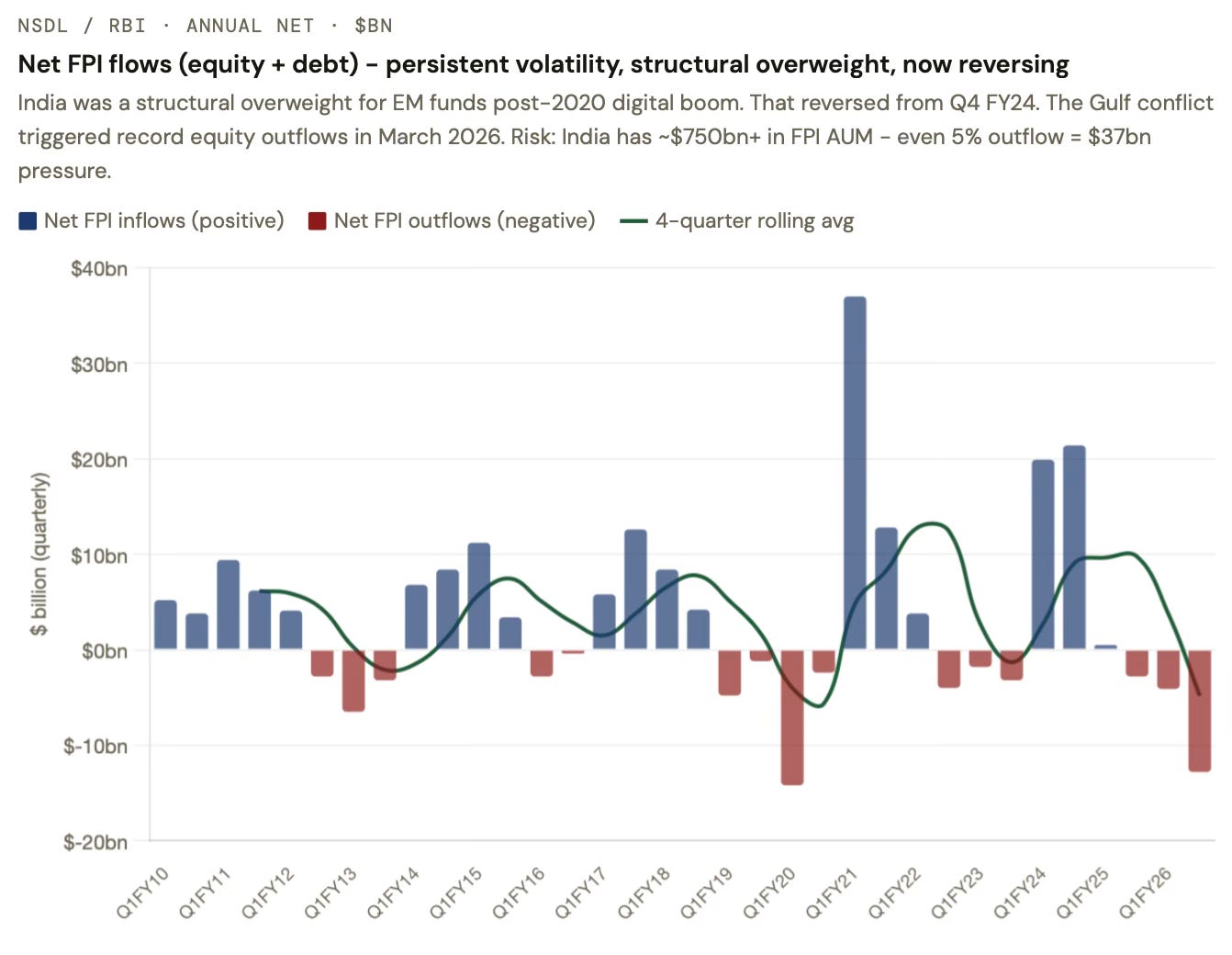

For a long time, India was the darling of emerging market (EM) funds, who had been overweight on Indian equity markets. However, once the tide turned since October 2024, it has been a steep decline with FPIs pulling out $45 bn. FPIs are now underweight on India, ownership is at a 15-year low, it has underperformed EM equities by 50 percentage points, and it is estimated that there would be another $12-15 bn of possible selldown. But worryingly, even after the poor performance, India trade at 50% premium to EM averages. Having missed the AI story and with other markets recovering from their low baseline (just as India is declining from its high baseline), there’s no immediate reason to reverse the course on India.

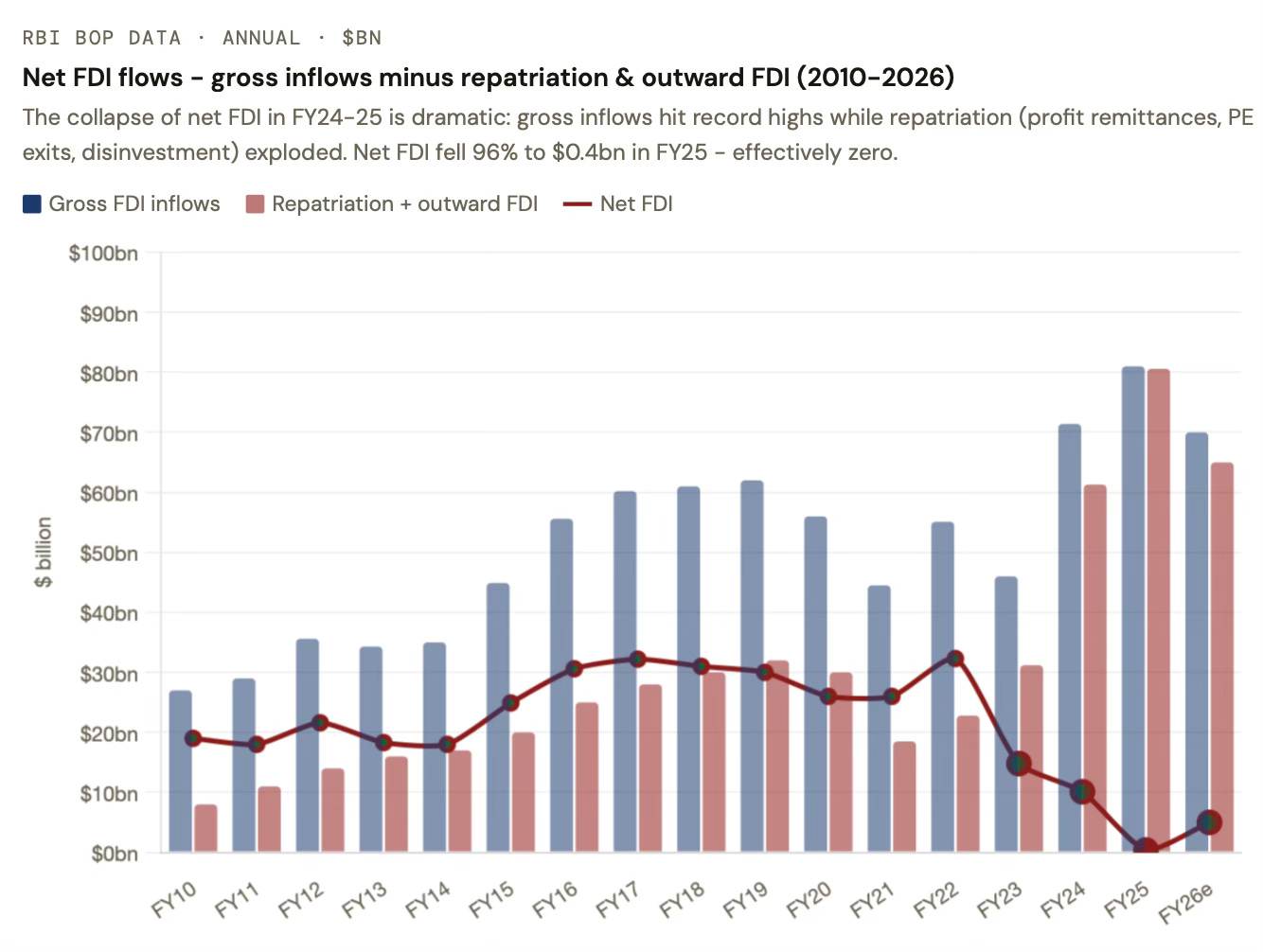

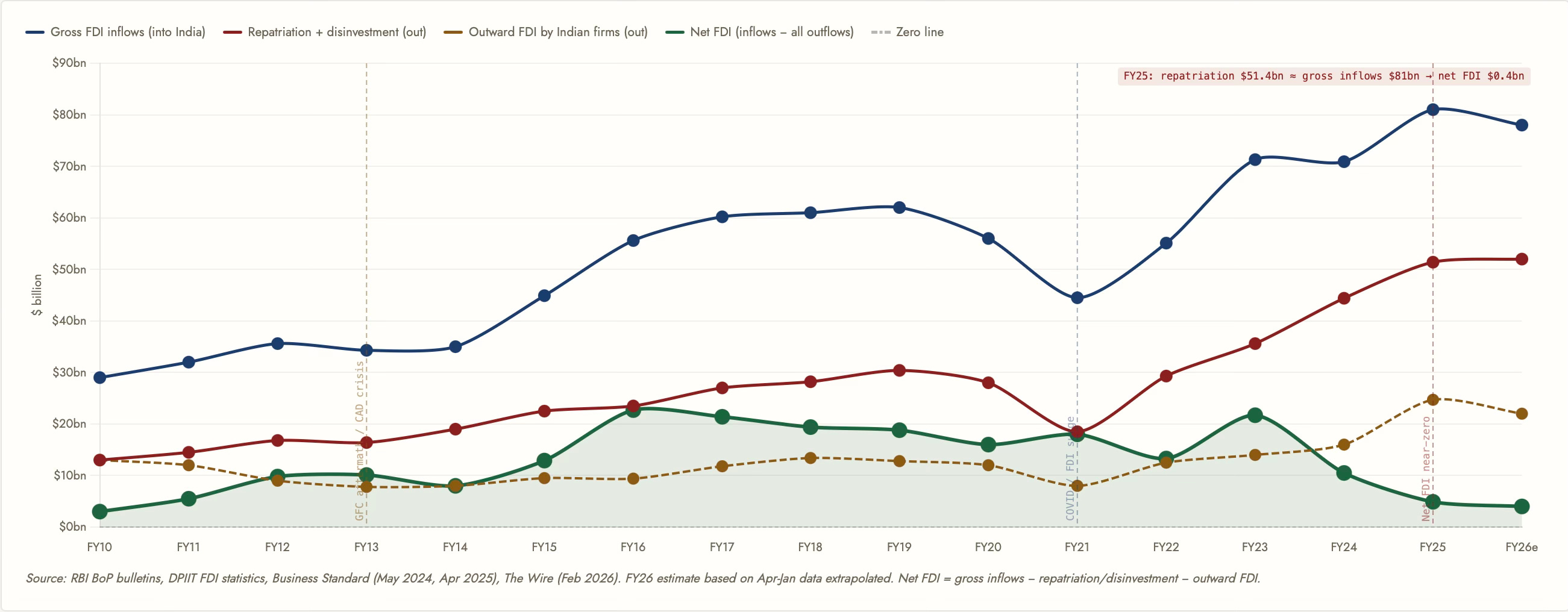

The net FDI inflows has been steeply declining since FY22, after being stable in the $25-30 bn range since FY15. The sharp increase in outward FDI flows starting from FY23 is an important reason.

Gross inflows more than doubled over 15 years (from $29bn to $81bn), but repatriation quadrupled (from $13bn to $51bn) and outward FDI surged, leaving net FDI near zero by FY25. In FY26, net FDI recovered partially but repatriation is running at record monthly highs (it touched $4.9 bn in Jan 2026).

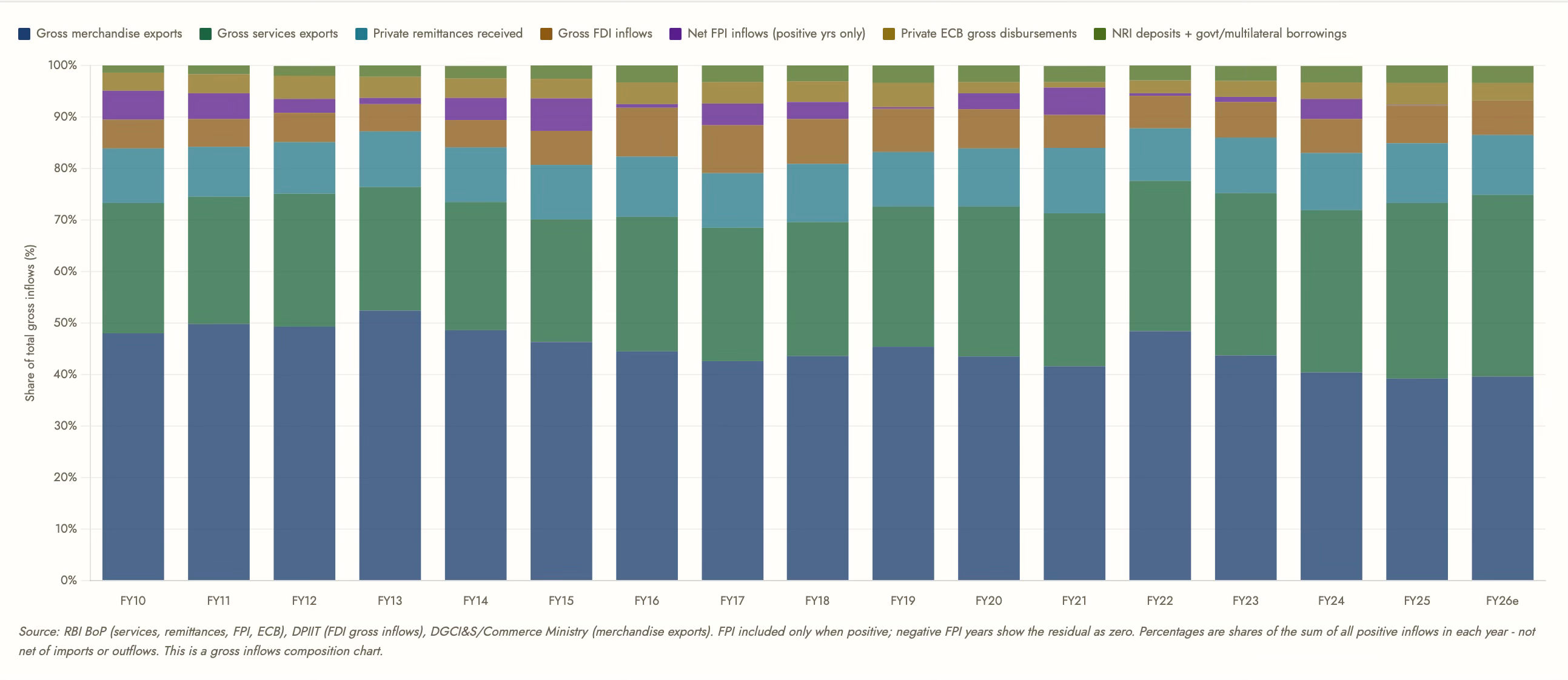

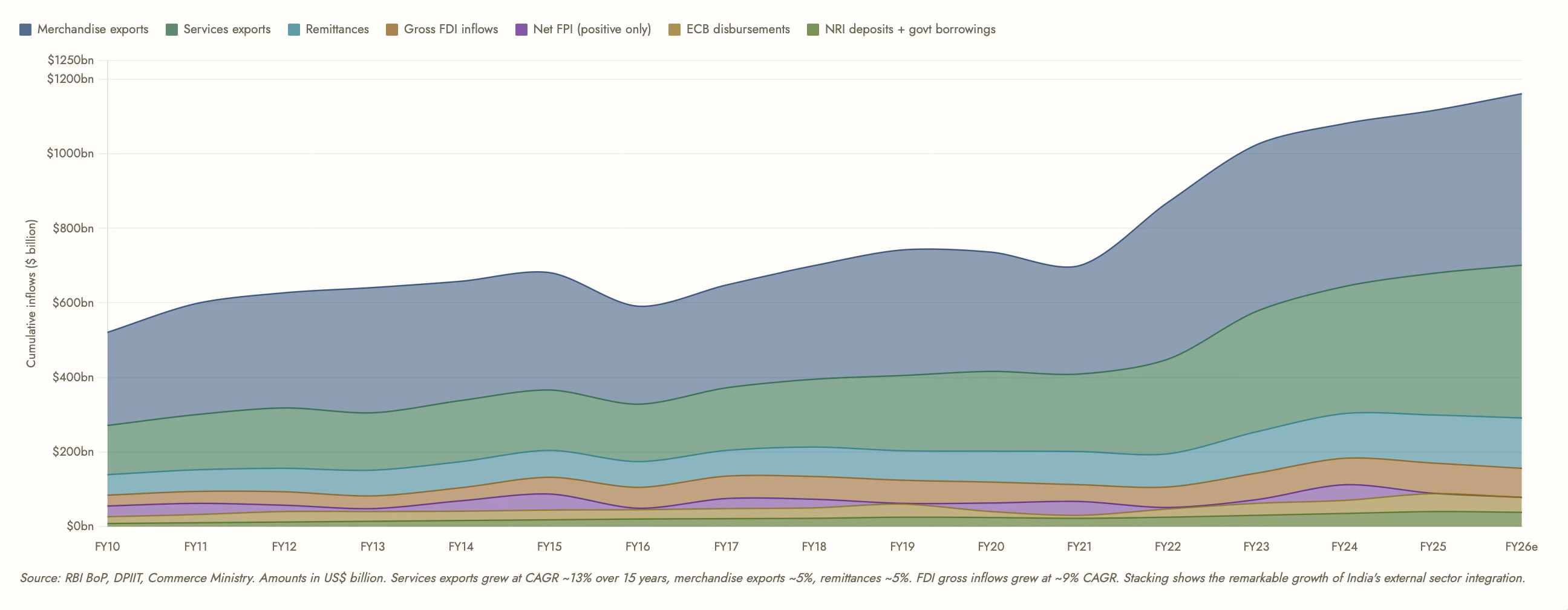

An analysis of India’s total gross foreign inflows shows that merchandise exports have shrunk from 48% in FY10 to 39.2% in FY25, whereas services exports (rose from 25.3% to 34.1% in the same period) and remittances (10.6% to 11.6%) together now account for the dominant share, while net FDI and net FPI have shrunk as shares.

In absolute value terms, the total gross foreign inflows have doubled from ~$600bn in FY10 to nearly $1.2 trillion by FY25. It has to be borne in mind that goods exports, services exports, and remittances form the major share, with FDI and FPI being secondary contributors.

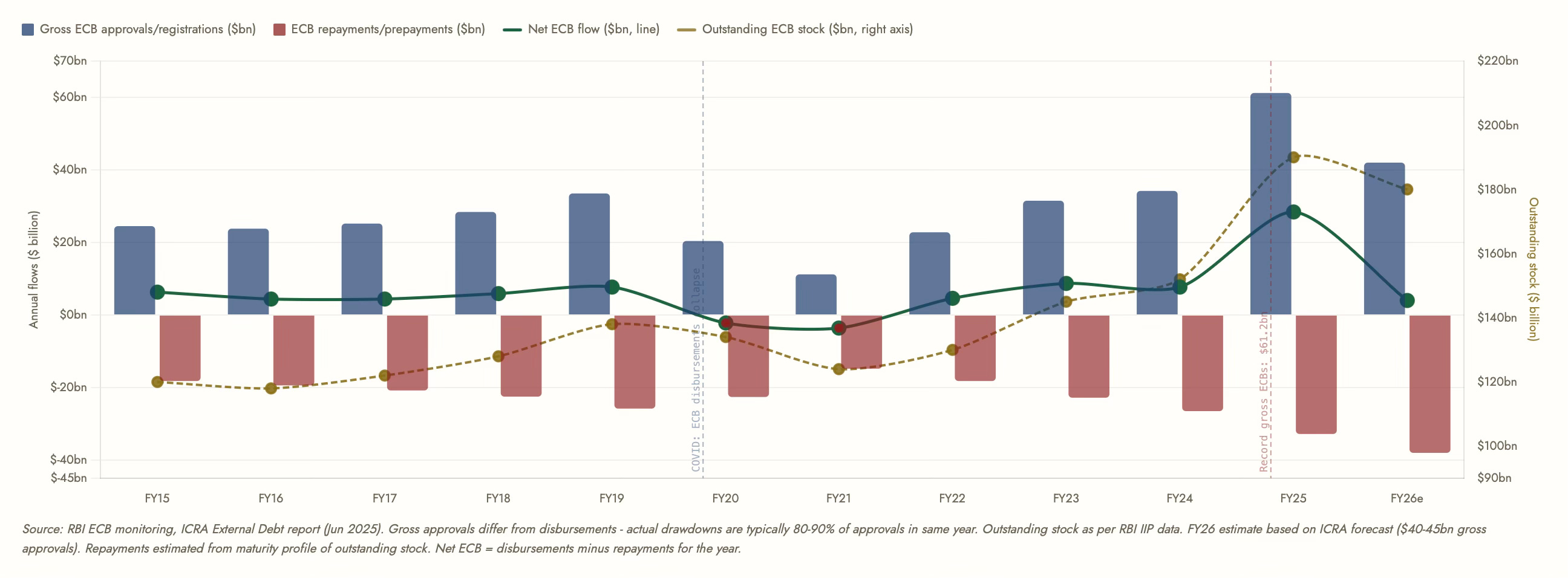

India’s corporate sector actively uses overseas borrowing as a cheaper alternative to domestic credit (especially when domestic interest rates are high). Gross ECB approvals surged in FY25 to hit a record $61.2bn as domestic liquidity tightened. Repayments have also risen, constraining net ECB as a financing source. As of September 2024, the outstanding stock stood at $190.4bn, rising from $124 bn in FY21. The 50% increase in ECB stock also means higher repayment outlflows going forward. The Gulf war has raised ECB cost (higher risk premium, weaker rupee raises hedging cost) while reducing domestic alternatives.

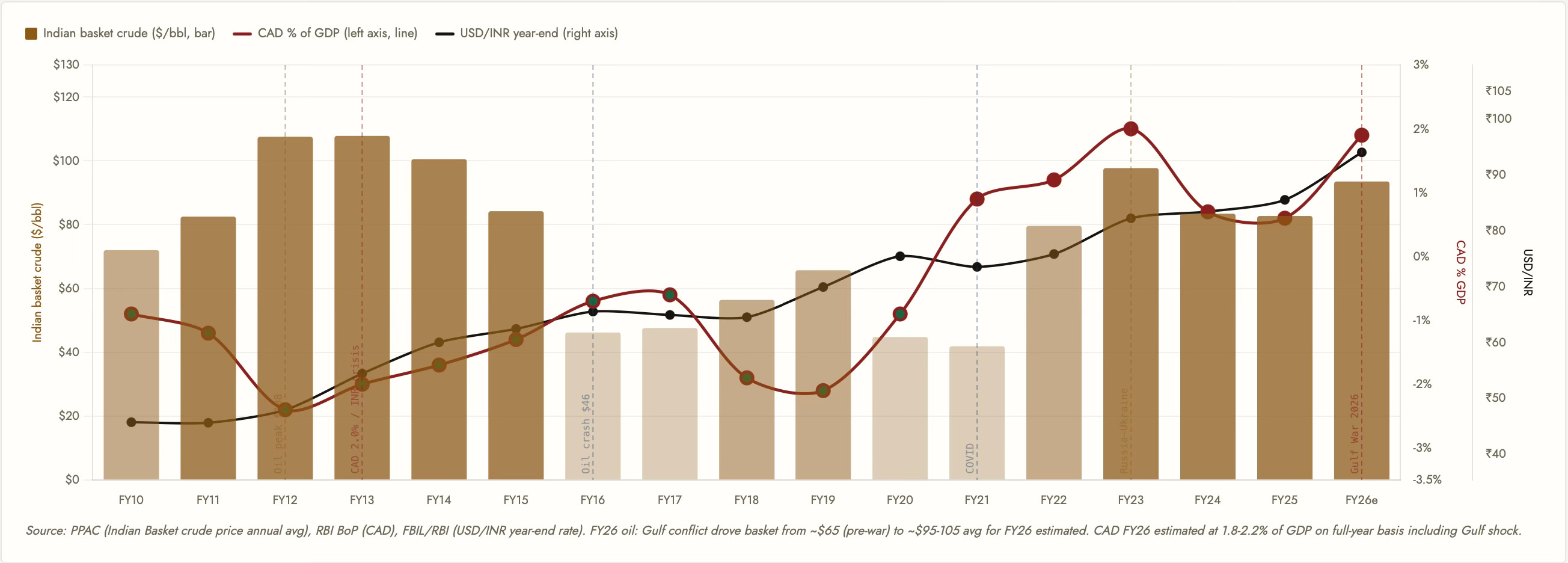

Econ 101 teaches us that higher oil prices lead to increased current account deficit (CAD), and weakens the currency. The graph shows that this dynamics played out in each of the four crises - FY12-13 (leading up to the taper tantrum), FY 20 (pandemic), FY22 (Russia-Ukraine war), and now the Gulf War. It shows that as the basket prices rose, CAD as a % of GDP rose. It is also to be noted that the Indian economy benefited from six to seven years of low oil prices, which also allowed the government to realised higher tax revenues by limiting the pass-through in global prices to the domestic market.

And the rupee depreciated episodically by about 65% over the last 15 years.

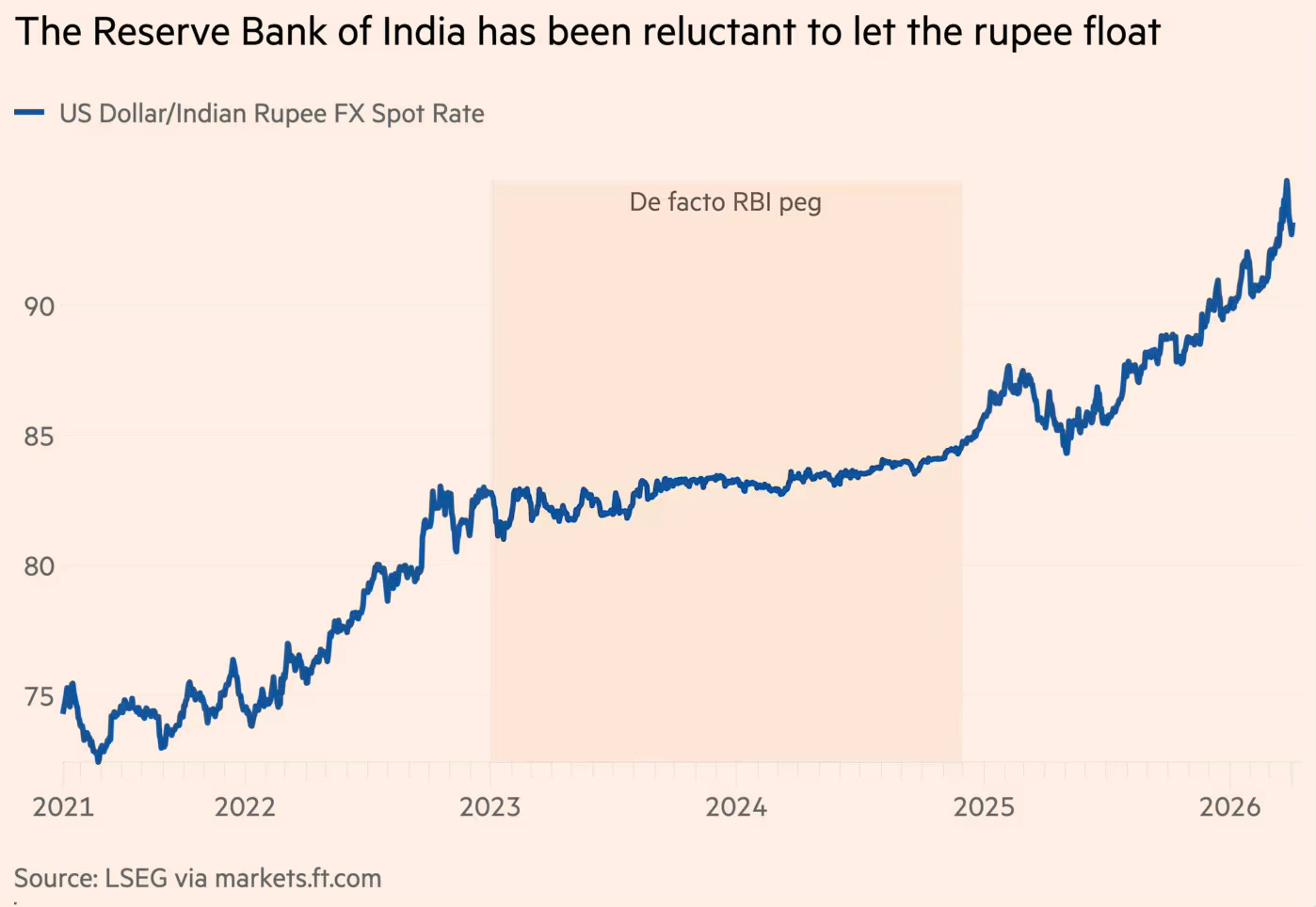

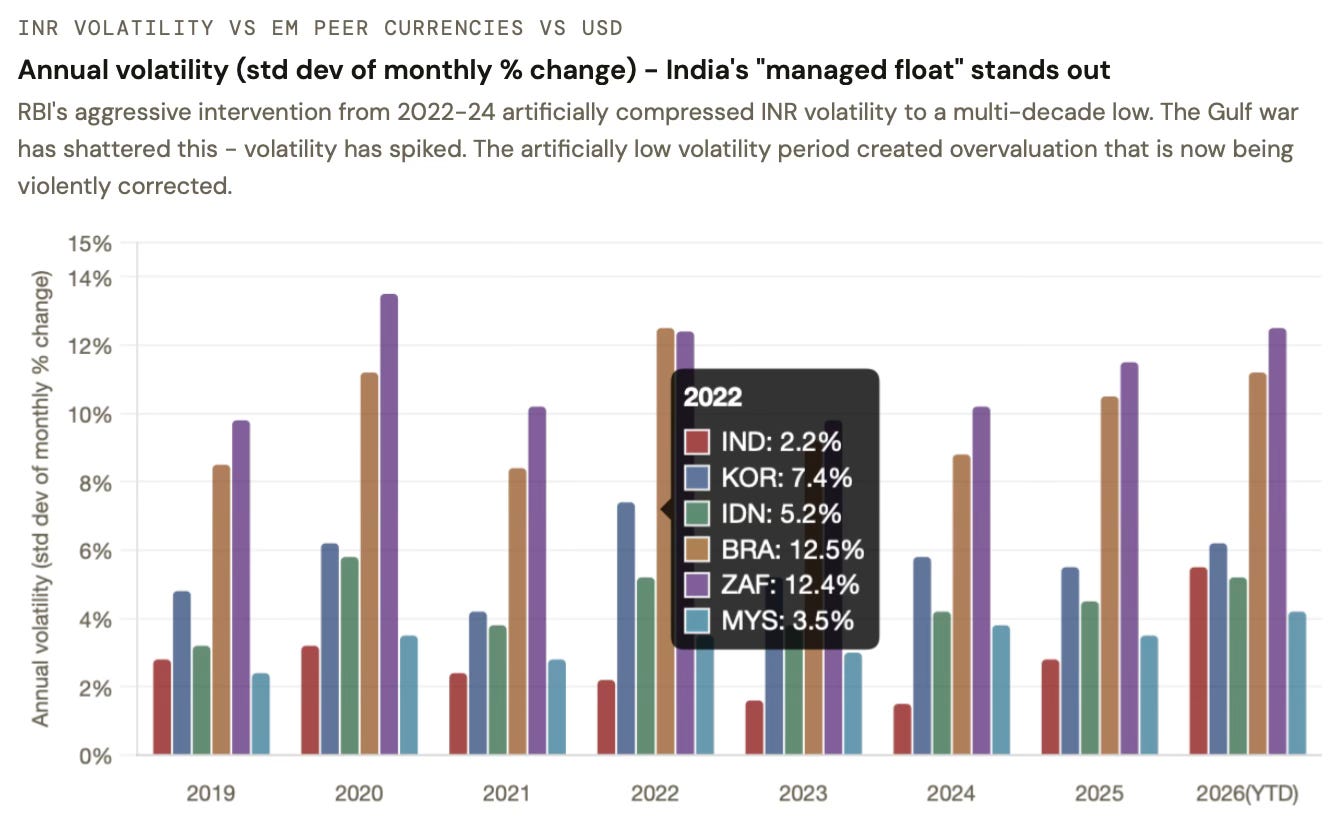

For sometime in 2023 and 2024, the RBI was intervening heavily to suppress volatility and prevent the currency from depreciating.

INR has been a remarkably stable currency over the last two decades. From 2015 to 2025, but for a brief pandemic blip, it was the strongest currency among peers. Now since the beginning of 2025, it has become one of the weakest currencies, only ahead of Turkey and South Africa.

After being the most stable EM currency in the last seven years, the rupee’s volatility has increased sharply in 2026.

So what does this portend for the external account?

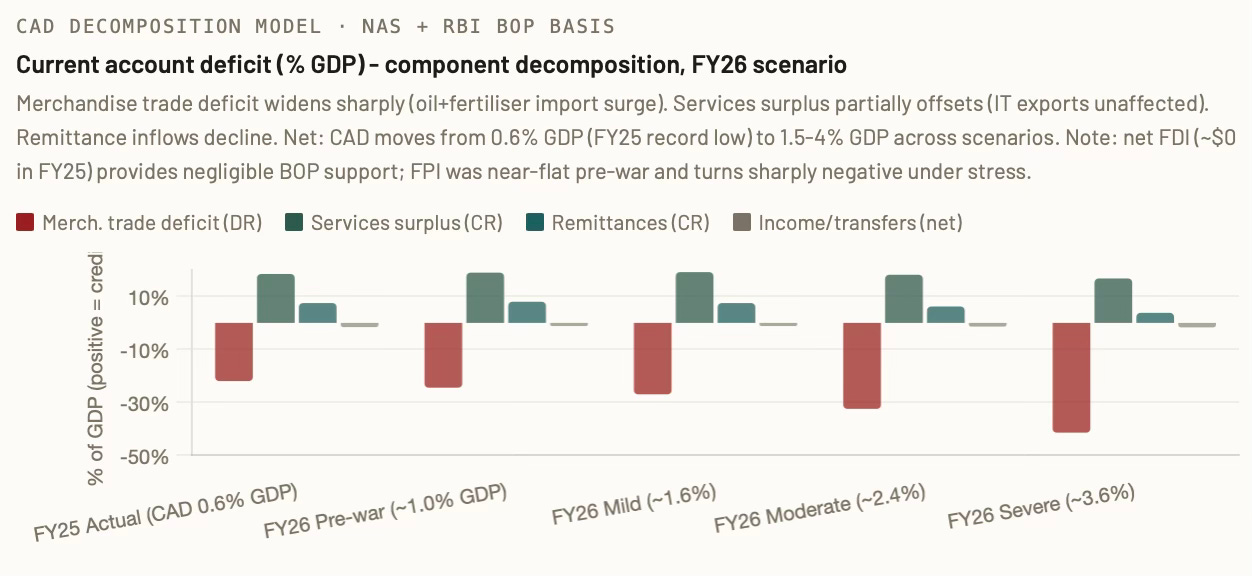

Assuming three scenarios of the Gulf War and squeeze on oil from the Strait of Hormuz - mild (4-6 weeks, $80-90/bbl, now no longer relevant), moderate (3-6 months, $95-110/bbl, which looks likely now), and severe (>6 months, $120-200/bbl), the net CAD is estimated to move from 0.6% of GDP pre-war to 2.2–2.6% in the moderate scenario and 3.2–4.0% in the severe scenario.

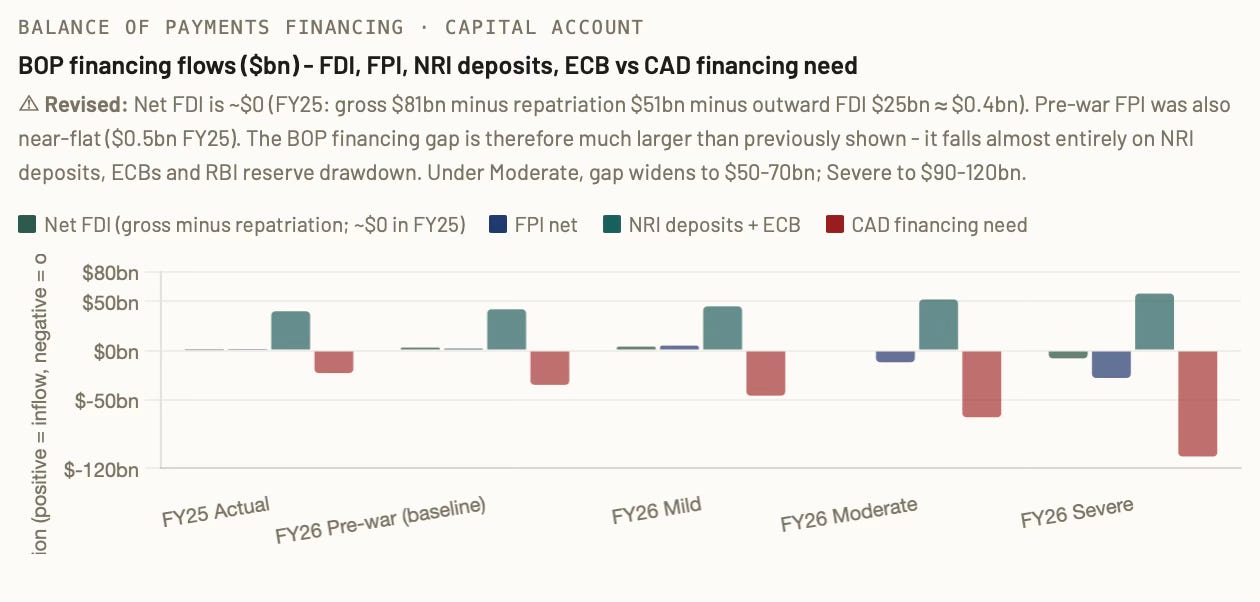

In stress scenarios, repatriation of FDI actually accelerates (PE exits, MNC profit remittances, Indian firms investing abroad), so net FDI can turn negative. The CAD financing need reveals a financing gap of $50-120 bn in the moderate to severe scenarios, requiring significant reserve drawdown and/or higher FCNR(B) NRI bonds. ECB borrowings are likely to remain constrained due to greater risks and higher cost of capital.

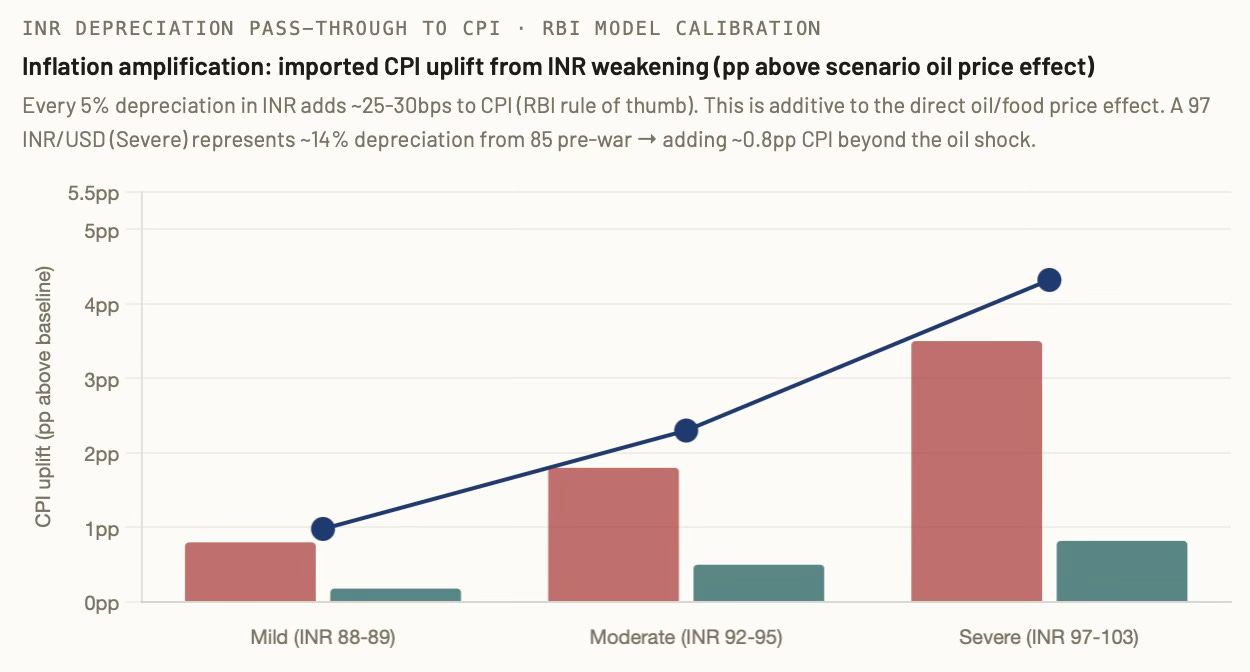

The impact on the domestic economy through inflationary pressures is significant. A 5% INR weakening adds ~25–30bps to CPI above and beyond the direct oil/food price effect, creating an amplifying loop in the severe scenario.

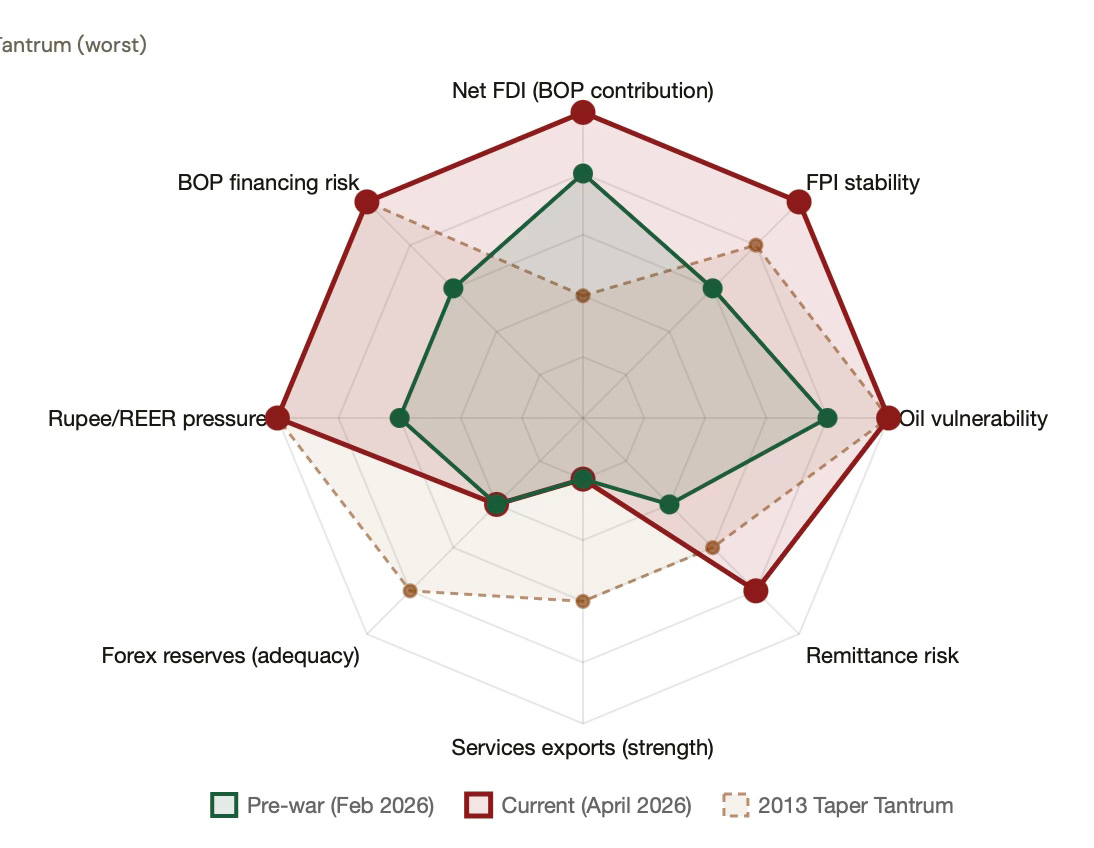

Bringing all this together, the radar chart shows that on 6 of 8 dimensions, India’s current external vulnerability is worse than pre-war February 2026, and comparable on the worst dimensions (oil, rupee, BOP financing) to the 2013 Taper Tantrum. The redeeming factors are the rising services surplus and the foreign exchange reserve level. The RBI faces the classic impossible trinity: defend the rupee (deplete reserves, distort adjustment) or let it depreciate (amplify inflation, undermine confidence). The optimal path — gradual managed depreciation with NRI incentives and tight communication — is the 2013 playbook, and it is available again.

In conclusion, the Gulf War poses the biggest risks for the external account since the taper tantrum episode. Therefore, the outcome of the negotiations between the US and Iran has significant implications for the Indian economy.

No comments:

Post a Comment