This blog has been a consistent critic of corporate India’s reluctance to invest in R&D. With the emergence of AI applications that are disrupting software development, the big Indian IT companies have been criticised for their low R&D expenditures. There has been a slew of commentary in recent days bemoaning India’s deficient private sector R&D spending and urging corporate India to embrace innovation. See this, this, this, and this.

This blog has argued that the nature of India’s market, with its price-sensitive customers and small premium market segments, may not allow Indian firms the cash flow cushion required to invest in R&D. Others have pointed to cultural and other factors as being responsible. There are problems with each of these lines of reasoning.

I used Claude and analysed the annual accounts and statements for the last five years of the 3-4 top Indian companies and their like-to-like peers in Europe, Northeast Asia, and the US on revenues, profits, margins, and R&D expenditures across eight industries. Specifically, how do the sizes (by turnover) of the median Indian companies and their peers compare? How do they compare on PAT margins and R&D as a share of revenues?

The headline takeaway is that Indian companies tend to be more profitable than mature Western peers (services, autos, pharma, telecom) but smaller in scale and far less R&D-intensive than the global leaders in product/innovation-driven sectors (consumer electronics, software products, EMS modules, speciality chemicals).

While it confirms the low R&D spending of Indian companies, it also points to a more nuanced narrative. While Indian companies are much smaller than their global peers, they are either the leaders or are at the top in profitability.

Let’s examine the headline findings.

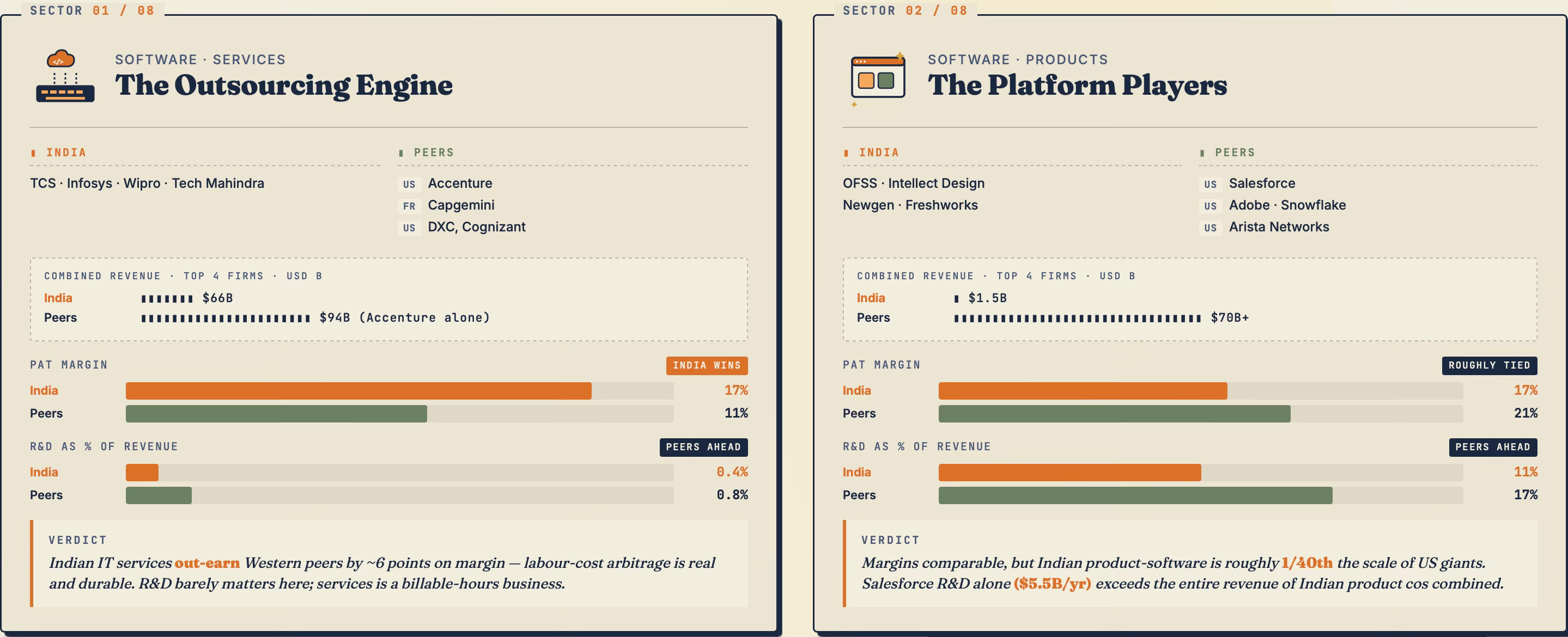

The big IT consulting/services firms are the main targets of the growing chorus of criticism in the mainstream media on the lack of dynamism and low R&D spending. It is worth noting that while Indian software service firms have margins that are significantly higher than their peers (arising not from any innovation or efficiencies but from the labour-cost arbitrage), their R&D spending lags. The R&D as a percentage of revenue runs 0.3-0.5% at Indian firms vs 0.8-1.0% at say, Accenture, a 2-3 multiple gap. Further, while the R&D spending shares of the likes of Accenture have been rising, those of the Indian firms have been stagnant or even declining (Infosys) in recent years.

Also, the R&D expenditures of the big software service firms in the US do not include the significant amounts spent on acquisitions each year. For example, Accenture deploys $2-5bn annually in 30-40 acquisitions per year, many in AI specialities (data engineering, vertical-domain AI, ML platforms), whereas the largest Indian firms do 2-5 acquisitions per year, usually smaller and more conservatively-priced. Accenture treats acquisition as a substitute for internal R&D, while Indian firms treat it as a supplement to organic build-out. The cumulative effect is that Accenture has accumulated dozens of niche AI consulting practices acquired pre-2024, whereas Indian firms have built mostly organically and more slowly.

However, it must also be said that some of the criticism also reflects a tendency to conflate what is an inherently low R&D industry with the R&D-intensive product-focused Big Tech and AI firms. IT services have never been an innovation-focused industry. Further, compared to several other industries (as we shall see), the R&D spending of Indian IT services firms is not that far behind their Western peers.

While Indian software product firms hold up on margins, they too lag on R&D. The 5-6 percentage-point gap between US and Indian product company R&D spending is the closest real number to “the innovation gap” people often talk about. On size, if you take out OFSS, which is a subsidiary of Oracle, there is no Indian company with even $300 million in revenues. The four Indian product companies combined generate ~$1.5 bn in revenue. Salesforce alone does $38 bn. Adobe does $21 bn. They are dwarfs to their global peers. This is the real software industry gap.

In the automobile industry, Indian OEMs outperform their global peers on profitability. The R&D intensity at 3.6% is half of Europe's but comparable to Japan and the US. This conceals the fact that, despite being in the business for decades, the big Indian OEMs continue to depend on foreign designers and engines. They have been comfortable doing business by licensing technology and importing engines. Further, where India really lags is in the frontier technologies like batteries and electric vehicles. All these point to an ambition or aspiration gap.

Indian EMS profitability is again slightly better than that of Chinese and Taiwanese, but the R&D gap is the starkest in the entire analysis. Indian EMS spends 0.5% of revenue on R&D vs Chinese 4.1% vs Taiwanese 2.2%. Indian players are doing pure box-build assembly, whereas the Chinese players are designing modules. This is the value-capture gap. This is an area where the market is at the cusp of a massive expansion, and it is disappointing that Indian EMS’s have not sought to move up the value chain despite the promising opportunities that they face.

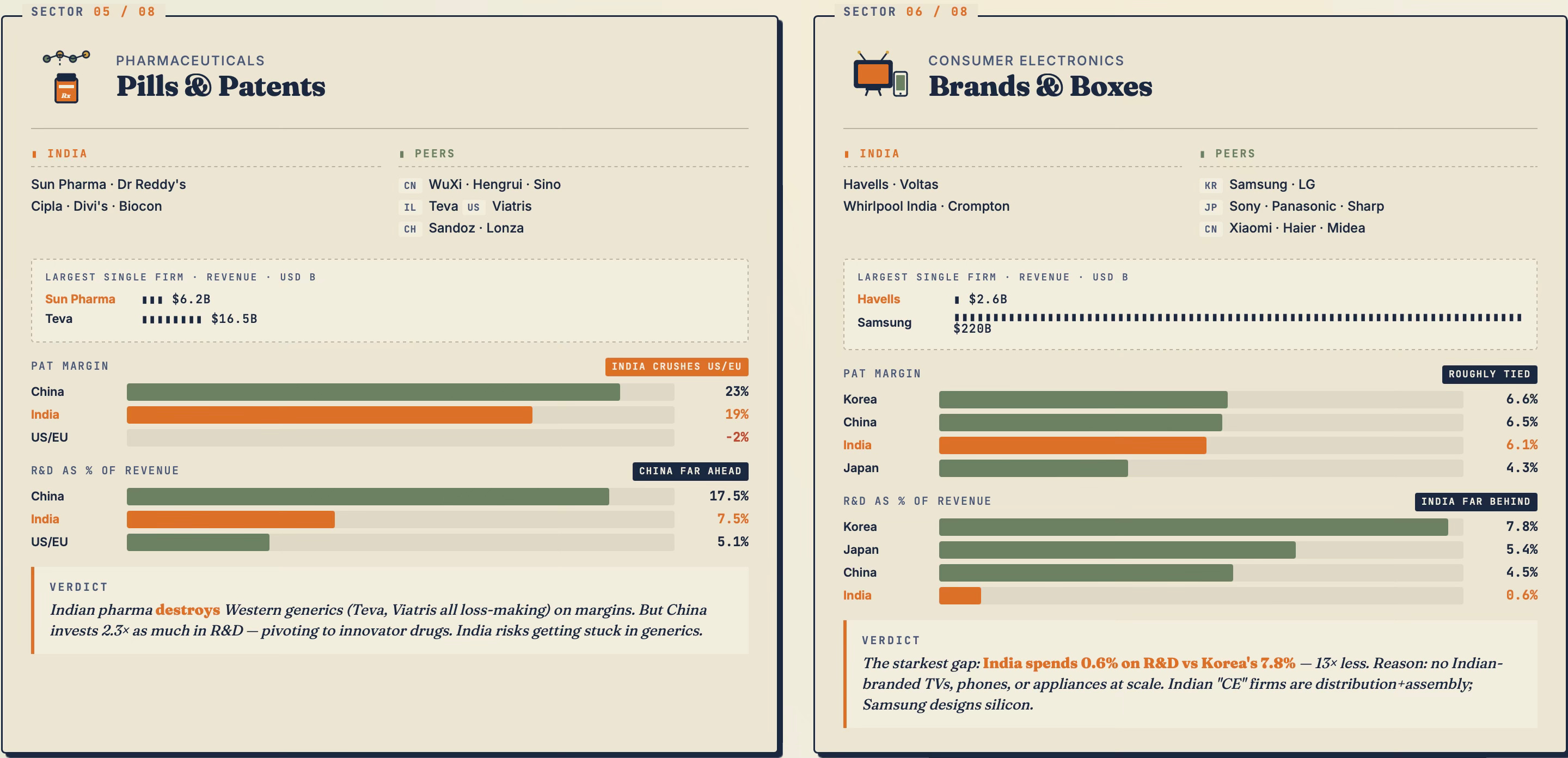

Indian pharma companies fare better than their software counterparts in both margins and R&D spending compared to their Western peers. Here, however, the Chinese are far ahead. Chinese pharma R&D intensity (17.5%) is more than double Indian (7.5%), with Hengrui, Sino Biopharm aggressively pivoting to innovator drugs. India's generics-and-biosimilars model is very profitable today but less R&D-intensive, raising the question of where margins go in 5 years.

The consumer electronics industry must count as one of the biggest disappointments. There is essentially no Indian consumer electronics industry comparable to its global peers. Even the biggest Indian firms are tiny when compared to their global peers. Indian companies (Havells, Voltas, Whirlpool India, Crompton) are appliance brands relying on outsourced electronics, explaining the 0.6% R&D figure compared to Korea's 7.8% or Japan's 5.4%. No Indian brand has any comparable R&D capability. Most of what's made in India is for foreign brands (Apple via Foxconn, Samsung via Dixon).

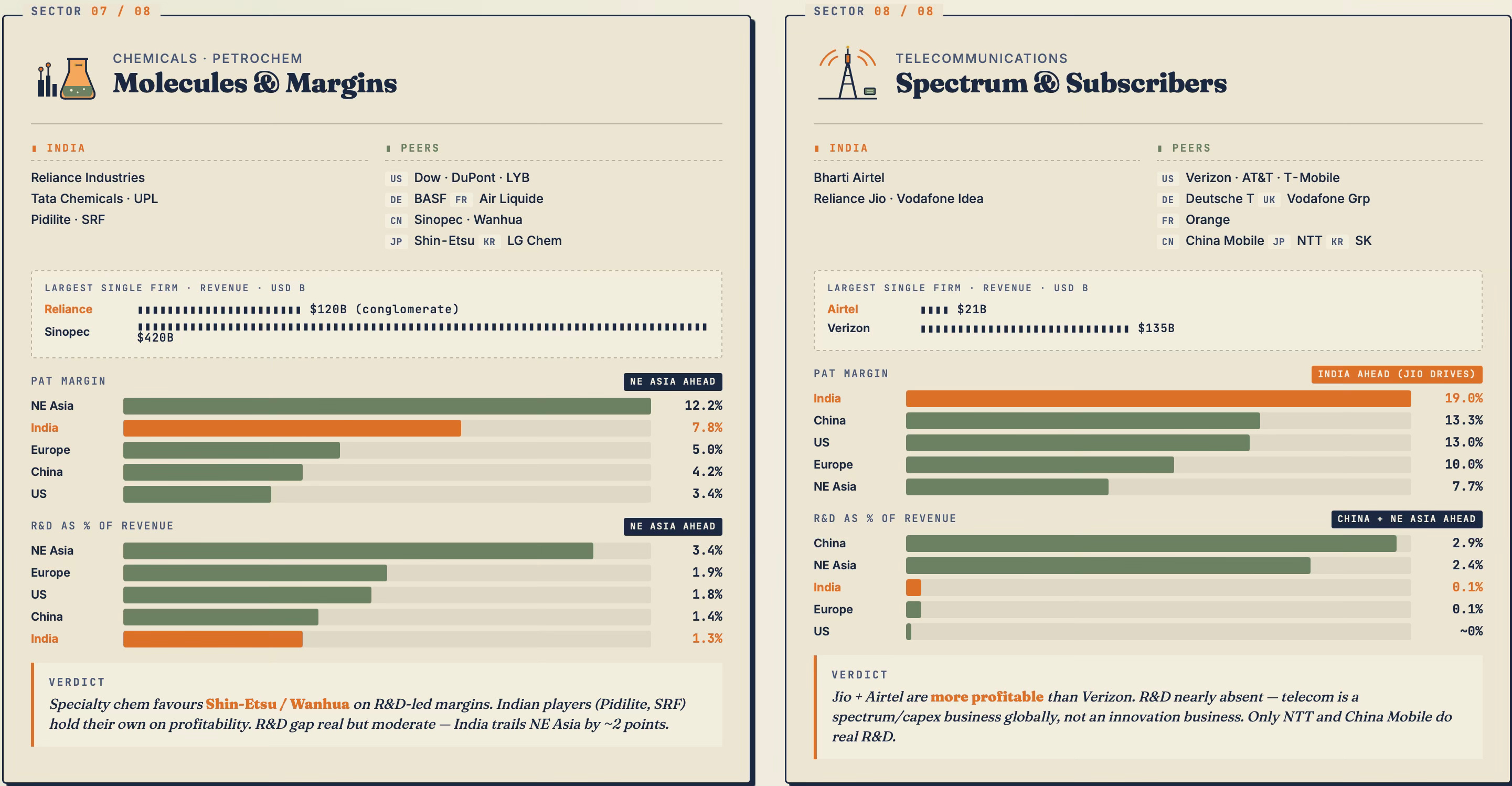

Chemicals is one of India's better stories. While the top Indian firms are large and their margins are second only to Chinese firms, their R&D expenditures again lag.

On the telecom side, Indian service providers are now the most profitable in the world, driven entirely by Jio and Airtel post-Indus-Towers consolidation. Verizon and AT&T look mediocre by comparison. The R&D number for telecoms is essentially zero everywhere except China Mobile and NTT since telecom is considered a capex/spectrum business, not an R&D business.

So what do all these mean?

The failure to produce even a mid-sized IT product firm, even after five decades of being a leader in the software services industry, is more an indictment of India’s entrepreneurship than of the IT services firms themselves. The IT product industry has had several favourable factors confluencing - the IT services industry produced enough talent and experienced professionals to supply both entrepreneurs and team leaders, there is an abundant low-wage workforce, it does not suffer regulatory failures like an inverted duty structure, high input costs or taxes, and there’s a large global market to serve. But even this combination was not enough to make even a one-billion-dollar IT product firm.

More than the IT services industry, it is perhaps the Indian pharma industry that is emblematic of the lack of business dynamism and entrepreneurship. The country has had a serious pharma industry, with several large generics manufacturers, for over six decades. Many of the leading firms of today were established by entrepreneurs who worked in the public sector entities. They had the opportunity to move up the value chain by building massive integrated industrial facilities. Even in contract manufacturing, they have remained stuck at the small-molecule synthesis and have struggled to move up the value chain to complex therapeutics and contract research.

Alongside the software product industry, consumer electronics should perhaps count as corporate India’s biggest failure. India has had a consumer electronics industry for several decades. With a very large market, Indian firms had the opportunity to ride the economic liberalisation, expansion of the middle class, and the global export market.

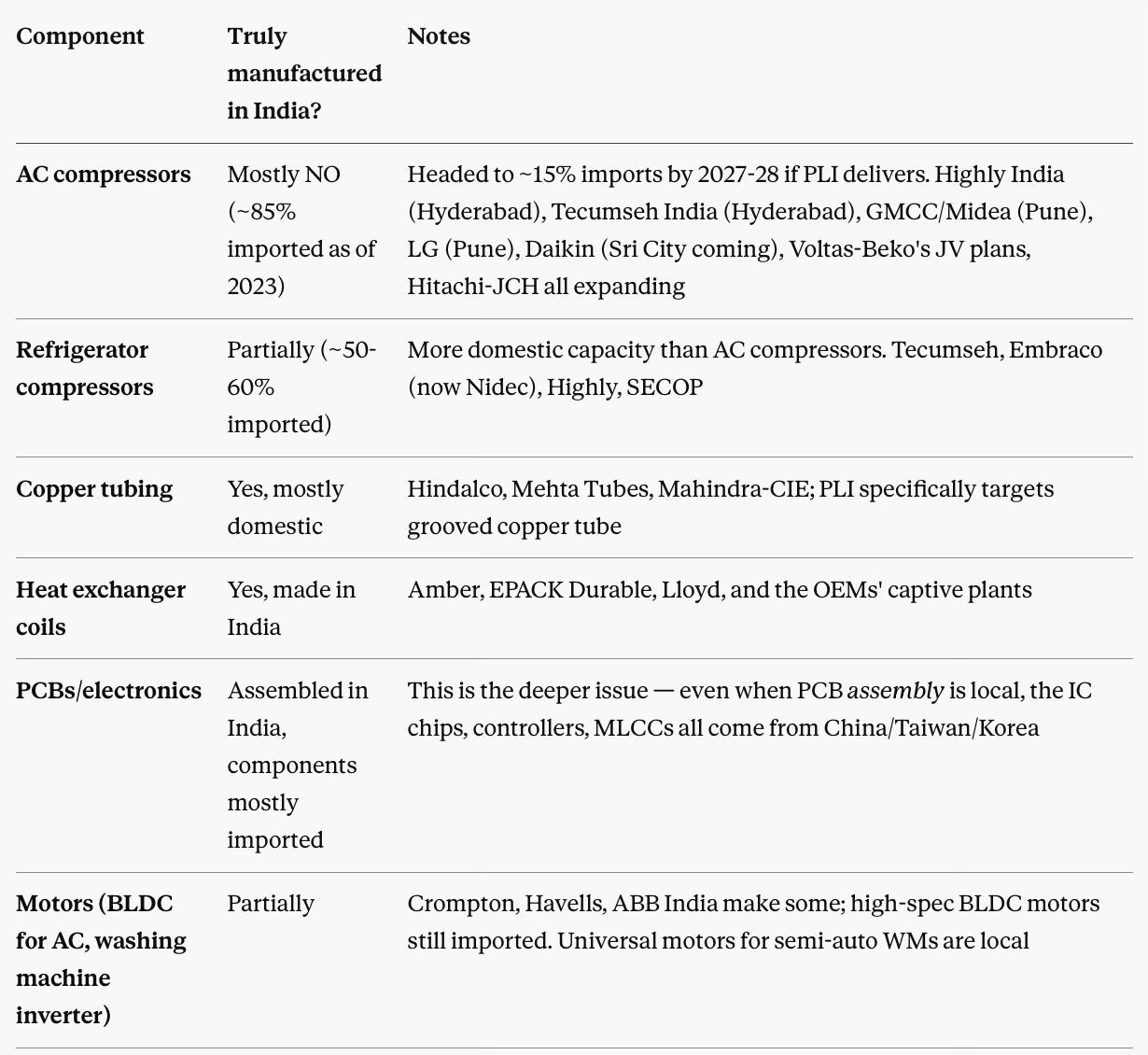

Interestingly, the Korean and Japanese OEMs (LG, Samsung, Daikin, Hitachi) have deeper Indian manufacturing (in terms of value addition in products like refrigerators, air conditioners, and washing machines) than most Indian brands because they invested in component plants in the 2000s-2010s when Indian brands were happy to rebrand imports.

One structural reason for this difference also points to the lack of ambition and reluctance to pursue the export markets. The Korean and Japanese OEMs treat India as a manufacturing base for both the domestic market and exports (LG exports refrigerators to the Middle East from India; Daikin to Southeast Asia). That export-anchored manufacturing economics justifies deeper component investment. Indian brands have historically been domestic-market-only and saw little case for backward integration when components were cheap to import from China.

It is therefore an unfortunate reality that the vast majority of AC and refrigerator compressors, and higher-end motors (for front-load washing machines) are imported.

The above analysis points to a corporate world that is stuck in a comfort zone, reluctant to assume risks by trying to move up the value chain or push aggressively into the next generation of products or technologies. There is a strong preference to stay on the sidelines and wait for technologies and products to emerge elsewhere. I’m not sure whether there is even one industry where Indian firms have been pioneers in showing the way with the next generation of products. Across industries, they always follow the trends in developed markets by copying and imitating.

The large captive market (domestic and foreign) is considered a safe enough moat (thanks to a combination of price-sensitive customers and import protections) that would allow these firms to grow for a long time to come. There is little incentive (apart from inclination) to explore and expand beyond this comfort zone.

In a globalised market, across industries, competitiveness is critically dependent on continuously moving up the value chain. It is a treadmill where, like the Red Queen, firms must run hard to retain their global competitiveness. And Indian firms, across industries, have shown consistent reluctance on this. It points to a problem of what I have described earlier as an entrepreneurship deficit.

With this entrepreneurship deficit comes a low risk appetite. This reflects in the reluctance to deploy capital. Moving up the value chain and expanding to foreign markets, essential requirements to becoming globally competitive, demand assuming significant risks by making large capital investments with long-term bets. These investments would also include cultivating supplier ecosystems, funding and nurturing startups, and long-term partnerships in general. Indian firms, especially the largest ones, have shown great reluctance to assume the risks and make these investments.

The reluctance to invest despite the consistently high margins across industries may be a symptom of the entrepreneurship deficit. As we have observed, firms are satisfied with their domestic markets and have limited or no appetite to expand into export markets. Further, the tepid growth of the domestic market (a reflection of the low aggregate demand growth, in turn a reflection of the narrow base of the consumption class) also discourages significant investments. All this manifests in a preference for short-term gains and avoidance of long-term competitiveness.

This is a nice summary of the motivations driving Indian firms.

India has a large domestic market, and the economy is growing at 6–7%. So, you can bring what has worked elsewhere, deploy it in the market, and make a lot of money. It’s less risky. That’s what corporates have been doing. It’s the cycle of development. But when you want to compete internationally, you need to think about your own ideas.

Another reason to invest more and pursue export markets is to increase size. As the analysis shows, even the largest Indian firms across the eight sectors are small compared to their global peers. Despite being more profitable than their global peers, their much smaller size is an important obstacle to global competitiveness.

The argument that government policies have been a binding constraint is not convincing. For one, the software industry, despite largely serving the global market and not being significantly constrained by public policy, did not produce any product firm or product of note despite several technological trends sweeping the industry in the last three decades. Second, even among the leaders in different industries, there has been little appetite to move up the value chain, expand into global markets or pursue new generation technologies and products. Third, even in localising manufacturing by nurturing local supply chains and partners, storied Indian OEMs have been behind foreign OEMs who have entered the market much later.

Fourth, the argument that import restrictions have prevented Indian firms from becoming competitive flies against the reality that the Northeast Asian economies built their manufacturing successes in highly restricted markets. Instead, as Joe Studwell has written, they gained competitiveness by competing in the export markets.

Now the government has thrown caution to the wind and, through the Rs 1 lakh Cr Research Development and Innovation Fund (RDIF), is funding even large corporates on their R&D endeavours. This may be the most that governments can do to push their industries towards innovating. It remains to be seen whether even this is sufficient.

In conclusion, it appears that Indian firms suffer from an entrepreneurship deficit, risk aversion, and a lack of intrinsic desire to think big (by moving up the value chain, pursuing next-generation technologies, and expanding into export markets). They seem satisfied with serving their captive local markets, continuing their existing product lines and business models, and following global leaders in technology and product trends. This is a reality, borne out strikingly by evidence. Whether it is culture or something else can be a matter of debate.

PS: On the issue of entrepreneurship, Claude had this comment on the prospects for India’s software services industry.

Accenture sells outcomes and prices its services on the value of the transformation. Indian firms sell capacity and price on the cost of the underlying labor. Generative AI threatens the capacity-pricing model directly because it compresses the labor hours needed. It enhances the outcome-pricing model because AI-enabled transformations are higher-stakes and command premium fees.

This is why the next 2-3 years will be the real test: not whether Indian firms have AI capabilities (they clearly do), but whether they can shift their pricing and packaging model fast enough before Generative AI deflation hits their core managed-services contracts. Accenture has already crossed that bridge; TCS, Infosys and Wipro are mid-bridge with the macro tailwind weakening.

This is a test of entrepreneurship and reinvention of business models for the Indian IT services firms.

No comments:

Post a Comment