A recurrent theme in international economics is the debate on the role of the dollar. As the global reserve currency, the dollar confers on the US an exorbitant privilege to borrow in its own currency, thereby allowing it not only to run large current account deficits but also to finance its fiscal deficit. The exorbitant privilege means that the normal rules of fiscal and monetary policies and capital flows management do not apply to the US in running its twin deficits.

As the US-China tensions intensify, there have been debates on whether the renminbi can emerge as an alternative to the US dollar. China has taken several measures to internationalise its currency. Today, some estimates suggest that 40% of its trade is settled in renminbi.

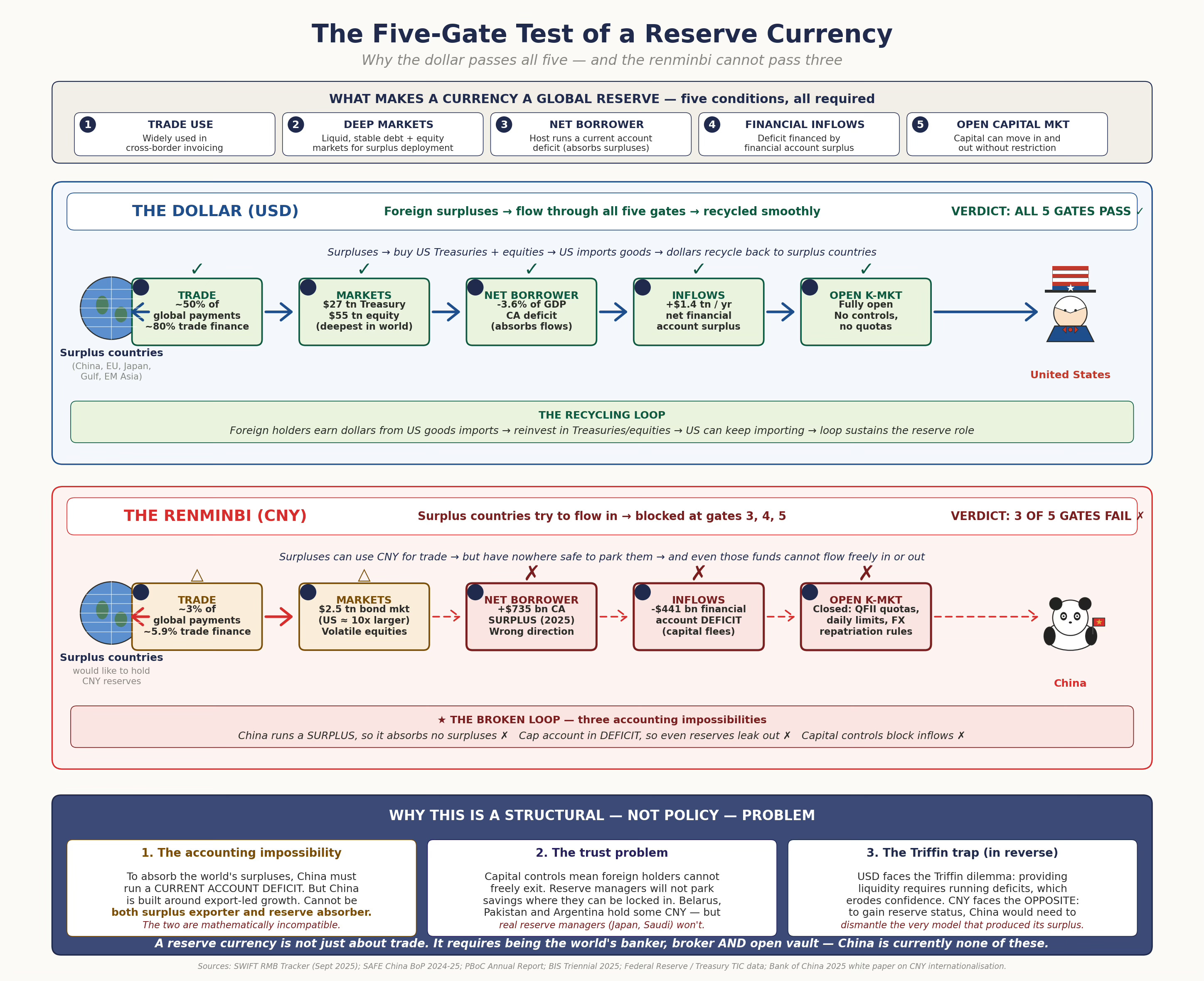

But there's a fundamental problem with China's efforts to prop up the renminbi as a global reserve currency. A currency can be a global reserve not only if it becomes used in cross-border trade transactions, but also, perhaps more importantly, if it has a deep, liquid, and stable market for investing the surpluses generated. In other words, countries should have confidence not only in transacting in this currency but also in retaining and investing their surpluses in it. What use is a foreign currency surplus when there are limited options to deploy it?

Such investments can be in the debt and equity markets in the host country of the reserve currency. This brings into play a third and fourth dimension, which are an accounting reality: the host country must be a net borrower (or run a current account deficit) and must be able to finance it with a financial account surplus. Both in turn require an open capital market (into which capital can be brought in and taken out with ease), the fifth dimension. In the absence of the last three dimensions, the host country will be unable to absorb and deploy the surpluses, and foreigners will not have the confidence to plough their surpluses into this currency.

China is very far from being in a position to offer the renminbi as a credible reserve currency. In fact, the Euro stands a far better chance of being an alternative.

This graphic captures what can be called a five-gate test of a reserve currency.

While the exorbitant privilege may have allowed the US to overcome the Triffin paradox (the only way to be a reserve currency is to run a trade deficit, which will, in turn, erode its status as a haven currency), the burgeoning US public debt and persistently high budget deficits (both of which debase the dollar) threaten this ability.

However, this must be seen against the reality of a world with surpluses that must primarily be parked in some credible currency asset and the absence of any alternative, there are three possibilities: the dollar continuing to be the reserve currency, the euro emerging as an alternative, and the global imbalances getting corrected.

The second option is more feasible than renminbi because Europe already has deep, liquid, and stable financial markets and an open capital account. However, it would also require Europe to run deficits. While Europe has traditionally run surpluses, there are signs that it might be declining. Besides, the European governments, especially Germany, have shown greater willingness in recent times to borrow and undertake fiscal expansion to invest in infrastructure and defence.

The third option is perhaps the most desirable and sustainable insofar as it addresses the distortions in international economic relations. But it would require the US to rebalance towards fiscal consolidation and reduce consumption, China to abandon its beggar-thy-neighbour trade policy and embrace domestic consumption, and Europe to shift towards public investment. The first two are deeply problematic political economy challenges and are unlikely without crises and convulsions.

This leaves us with the conclusion about the dollar’s continued dominance, not because Americans are clever or the Federal Reserve is wise, but because of an unusual coincidence of architecture: a large enough economy, a deep enough financial system, a current account deficit large enough to absorb the world’s surpluses, an open capital account that lets capital exit, and political institutions stable enough to make the open vault credible. No other country currently has all five, and China is structurally prevented from acquiring three of them without abandoning its development model.

Whether you like it or not, for the foreseeable future, the dollar is likely to remain the Hobson’s choice.

No comments:

Post a Comment