This post will provide a framework for thinking about the erosion of financial market discipline.

The FT has an article on an inflating earnings bubble in the financial markets.

Analysts are now forecasting a 25 per cent increase in S&P 500 company earnings for the coming year, according to Bloomberg data… Ben Inker, co-head of asset allocation at GMO, said forecasts for the next two years were “rising at an exceedingly high rate, nothing we have seen outside of a crisis recovery”. Consensus estimates for coming-year profits have risen by almost 20 per cent in six months, the biggest such jump since 2021…

Capital Economics analysts warned this week that “AI-related equity markets may be approaching a point where earnings expectations and capital expenditure assumptions become difficult to sustain” and a correction in these could “trigger a broad equity market pullback”. Michel Lerner, head of UBS’s investment analytics platform HOLT, said “shares in the AI food chain are priced to maintain supernormal profits” and warned of an “earnings bubble” forming in the market. While exceptional profits appear likely to keep being delivered in the immediate future, he said, “the likelihood of sustaining these levels of profitability and growth is incredibly low”.

This earnings bubble supplements an already inflated valuations bubble.

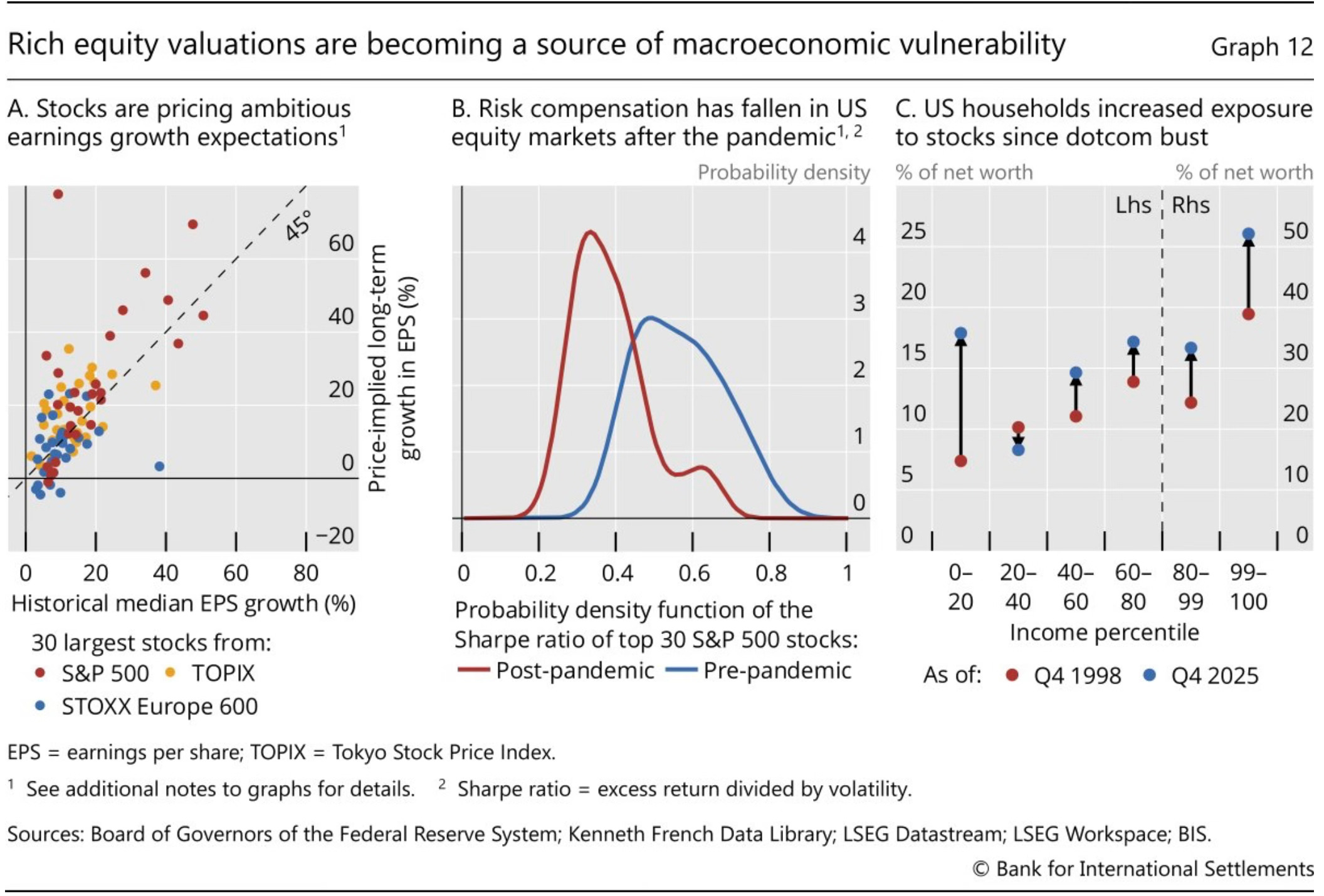

The BIS Annual Report has an excellent graphic that shows that stocks are pricing an earnings bubble, underpricing risk, and household exposure has increased sharply.

The implied long-term earnings growth for the largest corporations sits well above recent historical benchmarks, with US stocks often trading at large premia to peers in other major markets. These implied rates often exceed even the elevated growth that some of the technology firms have delivered in their relatively short lifetimes. As these firms mature and command a larger share of the market, sustaining such high growth could become increasingly challenging… Risk premia on the largest US stocks have compressed markedly since the COVID-19 pandemic, with the distribution shifting clearly to the left. This points to growing investor complacency and reduced compensation for risk-bearing… A major equity market correction could have larger macroeconomic consequences today than in the past. Household equity exposures have grown over the past few decades, both relative to total wealth and income. A large correction in valuations could have more pronounced wealth effects and sharper consumption pullback than in the past. And with US stocks accounting for an outsized share of global equity markets – about 64% of the MSCI Global index – the wealth impact from a US-led repricing could propagate globally.

And, the report says, all this is fuelled by a complex web of private circular transactions involving hyperscalers, chip makers and AI labs.

Chip makers and hyperscalers take equity stakes in AI labs or neocloud providers, who in turn commit to multi-year purchases of chips or computing power. Data centre construction is increasingly outsourced to third parties that lease facilities back to hyperscalers on long-dated contracts with embedded exit clauses. The terms of such deals are typically poorly disclosed, with risks of the same asset being pledged multiple times. Together, such arrangements account for a sizeable share of sector-wide financing and forward revenue. A sharp repricing of equity risk could prompt a reassessment of corporate credit risk and lead to tighter credit conditions more broadly…

Any tightening in credit conditions could expose existing vulnerabilities in the less transparent private credit space, whose reach has expanded among middle market and small firms… A larger shock, whether from a renewed inflation surge or a sharp AI-led repricing, could trigger a more widespread credit crunch… The growing role of private credit also raises concentration risks. Direct lending funds, dominant players in the private credit ecosystem, have quadrupled their lending to the AI and information technology (IT) sectors in the past five years, to about 15% of their portfolios. These loans tend to be larger than those in other sectors, while their terms such as tenor and pricing remain broadly similar, raising questions about lending standards and risk pricing.

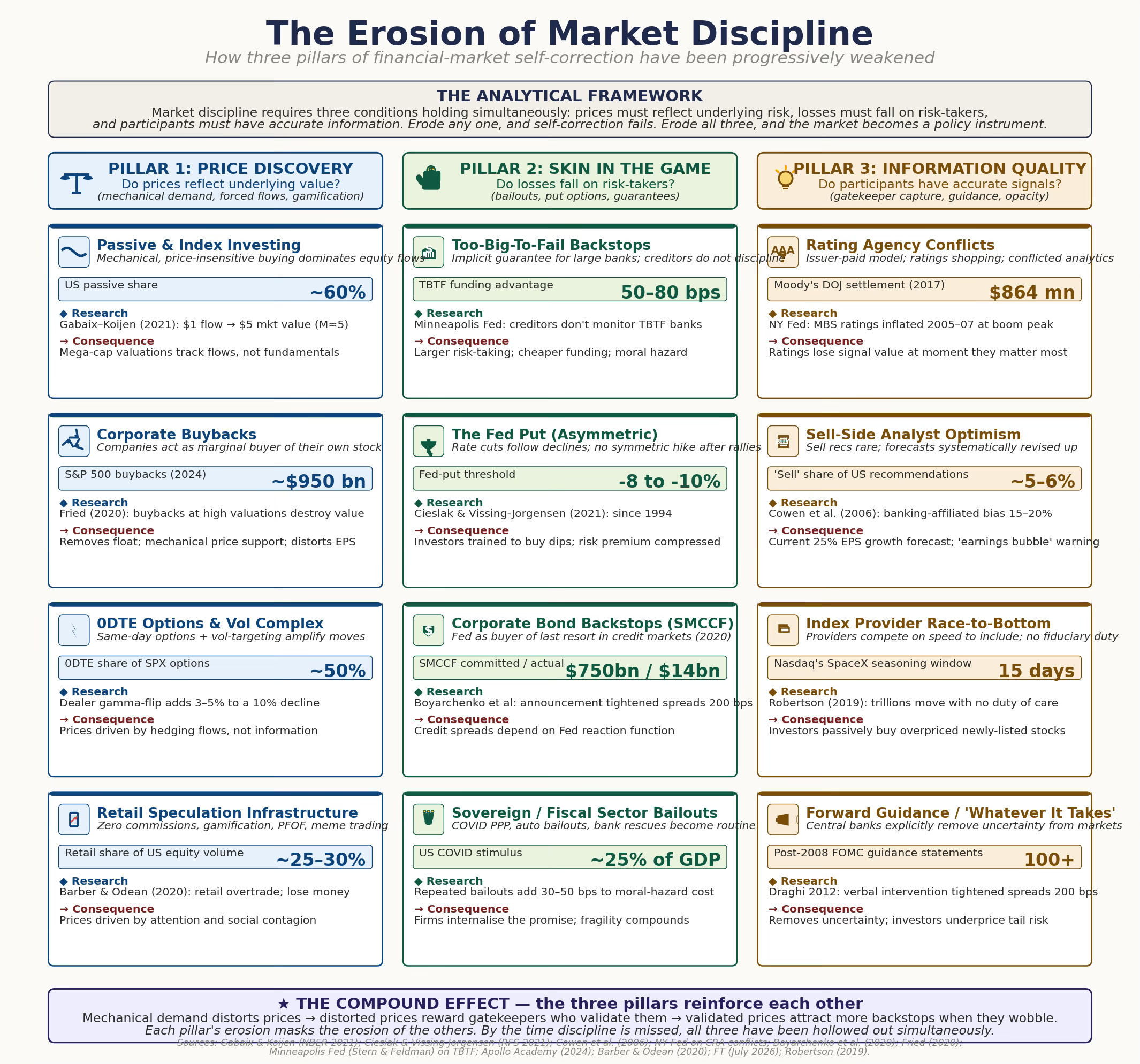

In this backdrop, it is useful to ask the question whether financial markets have lost their disciplining powers. What is it about modern financial markets that makes them underprice risk?

For sure, greater access to information has bridged information asymmetries, increased transparency, and reduced uncertainties and risks. And this has, in turn, lowered price discovery frictions and increased market efficiency. However, this has gone alongside trends in the opposite direction. Already, the complexity of financial instruments obscures risks and distorts price discovery. But other market practices have emerged in the last two decades that distort incentives and erode the market discipline. Some of them are consequences of the aggressive expansion of central bank monetary policy toolkits in the aftermath of the Global Financial Crisis.

There is a moral hazard created by the market participants’ internalising the belief that too-big-to-fail institutions or industries will always be bailed out. The institutions themselves come to view this as an insurance against their risk-taking. Well-intentioned actions of central bankers like forward guidance and commitments to backstop against shocks (Greenspan Put and Draghi’s “whatever it takes”) create similar moral hazard across markets. The gradual erosion of gatekeeping standards (ratings inflation, audit failings, index inclusion - e.g., for SpaceX) distorts incentives and leads to underpricing of risks. Excessively bullish market guidance, like with AI stocks now, fuels a cycle of irrational exuberance that amplifies bubbles. Finally, the inherent dynamics of financial markets bake in the fear of missing out among the institutional investors.

The fundamental basis for any efficient market is that information flows facilitate price discovery, and the costs of the actions of market participants are internalised. Based on this, an analytical framework on financial market discipline can be built on three pillars - information quality (participants must get accurate signals); price discovery (prices reflecting the underlying value); and skin in the game (losses must fall on risk takers). All three must hold simultaneously for market discipline.

The three erosions are not independent. Mechanical demand distorts prices; distorted prices reward gatekeepers who validate them; validated prices attract more backstops when they wobble. Each pillar’s erosion masks the erosion of the others. By the time discipline is missed, all three have been hollowed out simultaneously. This is why the current market environment can display record-high valuations (Price Discovery pillar broken), narrow risk premia (Skin in the Game pillar broken), and record-optimistic analyst forecasts (Information Quality pillar broken) - all at the same time, without triggering any traditional warning system. The system that would normally catch such a configuration has been progressively disassembled.

Interestingly, each erosion channel began as a reasonable response to a specific problem. Deposit insurance solved bank runs. Forward guidance solved communication ambiguity. Passive investing solved active-fund underperformance. Rating agencies solved information asymmetry. None of them is wrong in isolation. The problem is what happens when all the individual protections are stacked simultaneously, and all of them are pursued to their extremities. The system loses its balance.

The market’s self-correcting machinery is gradually replaced by a suite of external supports, and the participants who set prices become smaller and smaller relative to the participants who follow rules. At some point, arguably reached, the market is no longer a disciplinary mechanism at all. It is a policy instrument with an ambiguous owner. That is why the current earnings-bubble concern is qualitatively different from previous bubbles in that there is no obvious mechanism left through which the market disciplines its own excess.

So what can be done to restore the disciplining powers of the market?

Quite simply, it should be about restoring accurate price signals, consequences and costs of risk taking, and the trustworthiness of information, and all by going back to first principles.

The restoration of price discovery requires both thickening the market (a high concentration of buyers and sellers) and increasing liquidity (allowing assets to be transacted without significantly impacting the price). The internalisation of the costs of risk-taking demands rolling back moral hazard-inducing backstops and bailouts, or at the least ensuring these interventions are priced appropriately. Finally, restoring the quality and credibility of information requires separating information provision from the transactions side of financial intermediaries, and letting the market guide with information. An agenda is outlined below.

This must be complemented with cross-cutting reforms such as restrictions and greater oversight on revolving-door personnel movements, enhancing the white-collar prosecutorial capabilities of regulators, enhancing the supervision of non-bank financial institutions (NBFI), macroprudential capital surcharges for risk concentration, etc.

The problem, though, is that these are all very difficult reforms even at the best of times, but particularly difficult now. The silver lining is that a big crash can create the conditions for such reforms.

No comments:

Post a Comment