The AI trade is clearly blowing into a bubble of utterly spectacular proportions.

FT Alphaville points to the interesting reality that both equity valuations and earnings of the underlying companies are in bubble territory. They quote from the monthly market update by Joachim Klement and Francisca Reis of Panmure Liberum.

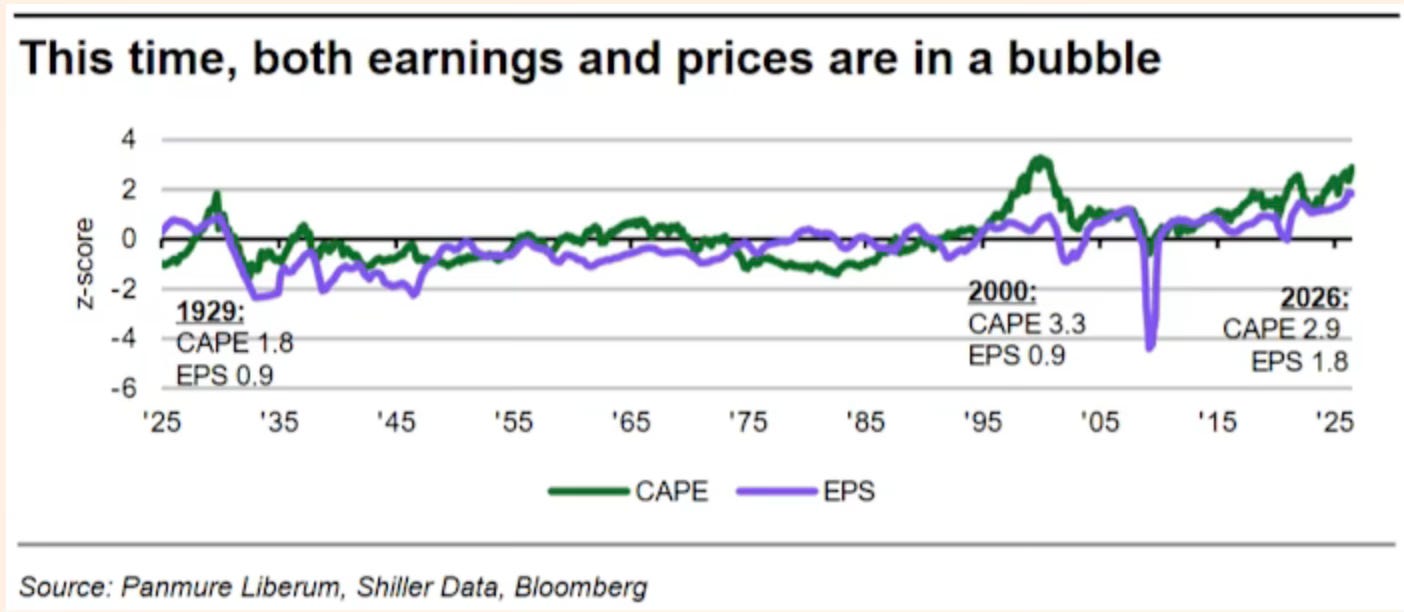

In 1929, the cyclically-adjusted P/E-ratio (CAPE) of the S&P 500 reached 32.6x according to Prof. Robert Shiller’s data. This was 1.8 standard deviations above trend at the time. In 2000, the CAPE reached 44.2x, or 3.3 standard deviations above trend – a clear sign of a bubble. However, as our chart below shows, earnings in both instances were within normal range, less than one standard deviation above trend. Today, the CAPE is at 41.0x, or 2.9 standard deviations above trend. Once again, we are clearly in bubble territory for stock market valuations.

However, unlike in previous bubbles, we are having extremely high CAPE at a time when earnings themselves are 1.8 standard deviations above trend. In other words, we are in a valuation bubble at a time when earnings are in a bubble themselves. If we correct for the earnings bubble, the current CAPE would be 67.6x or 4.6 standard deviations above trend, a bubble that surpasses anything ever seen in US history by an extreme margin. If valuations followed a normal distribution (which they don’t, so don’t take this literally), this would happen in 0.00019% of months or once every 43,432 years.

See just the Shiller CAPE ratio.

That being the case, what makes any assessment of the AI trade problematic is its unique nature.

It is the creation of a general-purpose technology that is most certain to transform several aspects of business models, work practices and trends, and life itself (and maybe even more). There are five stakeholders on the supply side of the AI story - semiconductor chips, cloud and data centre infrastructure, LLMs, financing, and support services. They encompass a vast spectrum of businesses - chip designers and makers, equipment makers, cloud infrastructure services, AI LLM developers, data centre developers, utilities, financial institutions, etc. On the demand side are all the different kinds of AI applications users, spanning every imaginable industry.

While the LLMs and the cloud services are software, the rest are all hardware. At the vanguard are the top public limited companies of our times, all with formidable moats and strong balance sheets. Till the recent surge in private credit, the AI investments were being financed from their large cash surpluses. Further, all of them make massive and growing profits, even creating an earnings bubble. Finally, given the network effects generally associated with digital technologies, the AI landscape is more likely to create winner-takes-all markets.

Also, so far, the AI trade has been running on the massive investments pouring into the development of AI LLMs and their applications. This investment binge is being driven by an intensely competitive race to outdo each other in improving the LLM algorithms and building up scale capabilities. The achievements to date on this have been truly spectacular. The applications development, though gathering pace, is lagging. No killer Apps or hardware have emerged on the landscape.

The true reckoning for the AI trade will depend on whether the AI algorithms developed will find commercially valuable use cases. More specifically, whether these use cases, which will emerge in the years ahead, will justify the massive investments already made and being committed.

Even more specifically, if the market smell tests of the AI promise endure, the bubble will continue to inflate. Such persistence of bubble inflation is, to a great extent, the perpetuation of stories. Elon Musk and SpaceX are the totemic illustrations. The two critical metrics of aggregate profits possible from the AI industry are the addressable market and margins. However, both are nearly maxed out in the valuation pricing on the upstream (supply) side. The best that can therefore be expected is that the downstream (demand) AI applications industry starts to create successful products. This would let the AI trade inflate more, at least for the immediate future.

On the contrary, if the market smell test points to the other way, at least in a few vanguard areas like autonomous driving or software development or healthcare and life sciences, then all bets are off and the wheels will start to come off. Another downward pathway is if the upstream supply-side margins start to get squeezed due to competition or disruption or rising costs. Given the asymmetric nature of such turns (bubble inflated gradually upwards, but the pop could be rapid), we could then see a rapid unravelling of the AI trade, with all its disruptive implications. The disruptions could be economy-wide, far deeper and broader than with the dotcom and other bubbles, given the wide sweep of markets that the AI industry has enveloped.

Interestingly, even as the seven largest data centre operators are planning to spend $848 bn this year, five times what they spent in 2022, the stock prices of the applications-side hyperscalers are struggling. Microsoft is down nearly 20% this year, and Meta is down 11%. The AI trade is now running purely on the chipmakers.

The critical place in the market to keep a close eye on may be the downstream side of AI applications and product development.

No comments:

Post a Comment