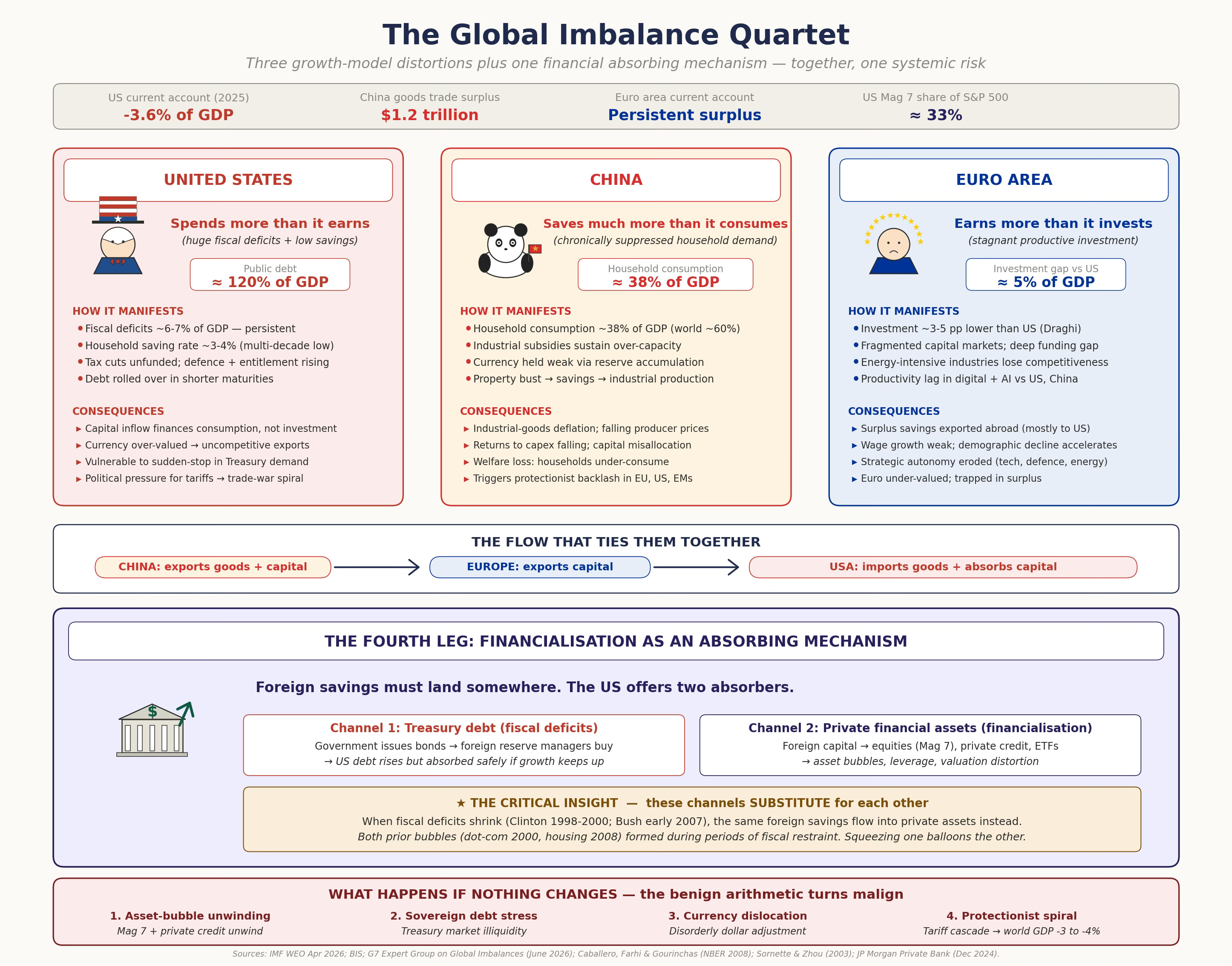

President Donald Trump’s single-minded pursuit of rebalancing the US economy using tariffs is unlikely to yield much without addressing fundamental distortions that have crept into the US economy and financial markets. Trade surpluses are a mere symptom of deeper malaises. I had blogged about the global twin structural imbalances, arguing that an American economy skewed towards consumption and a Chinese one skewed away from consumption are two sides of the same coin.

Helene Rey (see also this report to G7) has a very nice summary of global imbalances, where she locates it within the dynamics of saving and investment, and questions the focus on tariffs.

A country that saves more than it invests lends abroad and runs a current account surplus; one that invests more than it saves borrows and runs a current account deficit. It is the collective saving and investment decisions of a country’s households, companies and government that drive imbalances. There is now some agreement — crystallising in the G7 discussions — that the sources of imbalances are linked to unbalanced growth models and mostly made at home: chronically weak consumption in China, feeble productive investment in Europe and outsized fiscal deficits in the US. Tariffs are not an effective mechanism to change any of those and issuing an international currency is no justification to run current account deficits.

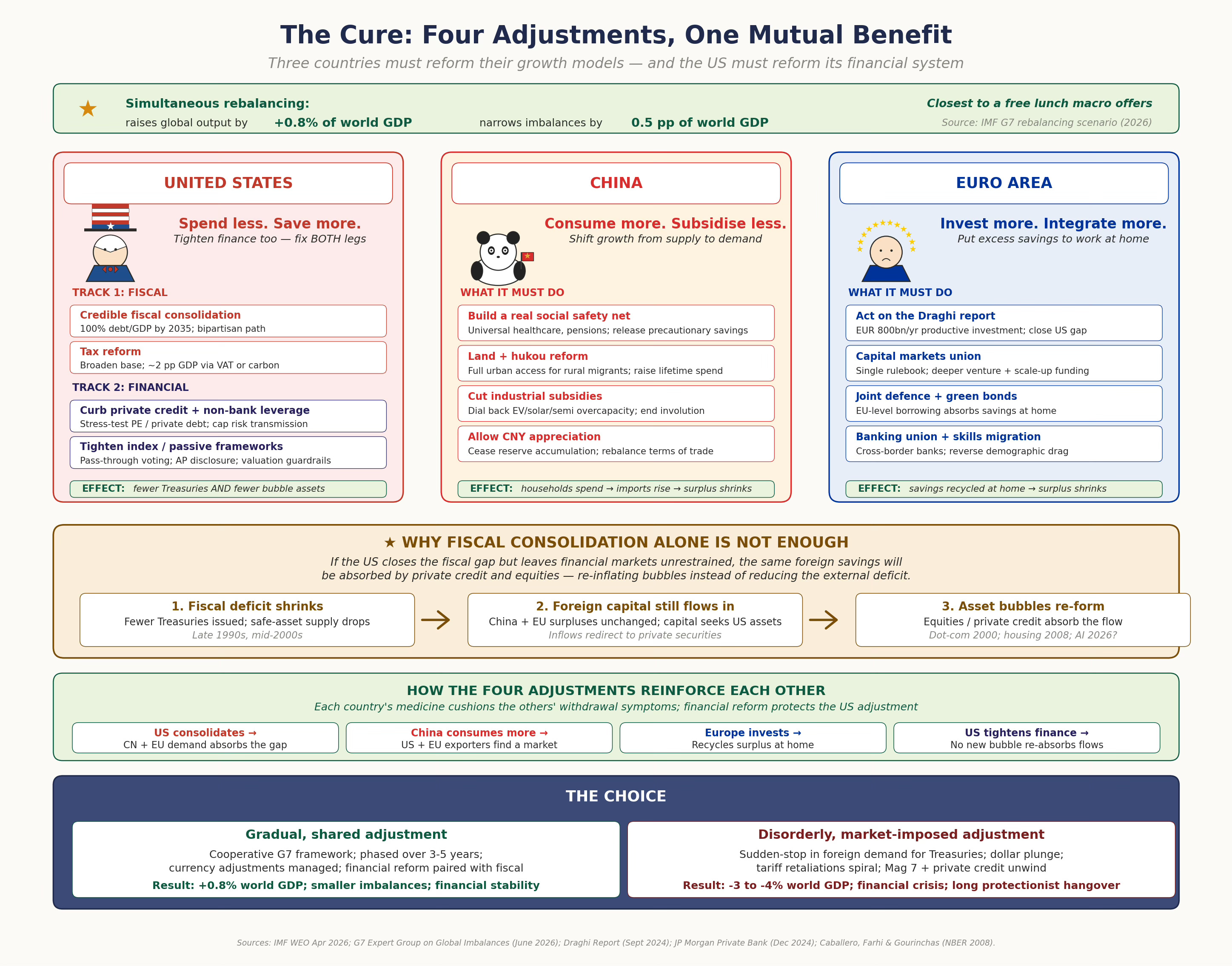

She also proposes the solutions in terms of complementary actions.

China rebalancing towards consumption, Europe lifting productive investment and America repairing its public finances are not three grudging favours. They are parts of a single, mutually reinforcing policy. One country’s exports are another’s imports; one country’s capital outflow is another’s inflow. When all three move at once, each adjustment cushions the others: the deficit country that consolidates finds external demand waiting as surplus countries spend more at home, and the surplus country that stimulates demand finds a market at home rather than a protectionist wall… The IMF’s scenario of simultaneous rebalancing raises global output by around 0.8 per cent and narrows medium-term imbalances by half a percentage point of world GDP.

I think this analysis misses a critical fourth leg of the imbalance, financialisation. It cannot be seen as merely a symptom of US borrowing. As evidence, there are two natural experiments. The last two episodes of US fiscal deficit reduction (in the late nineties and mid-2000s) were accompanied by financial market bubbles (the dot-com bubble and housing and mortgage market bubble).

Underlining this, Ricardo Caballero, Emmanuel Farhi, and Pierre Olivier Gourinchas have shown that if the financial markets do not work well, the economy might accommodate investments that deliver a rate of return that is below the growth rate of the economy. In this situation, both stock market bubbles and government debt can play the useful role of displacing inefficient investments.

Foreign savings flowing into the US must find a US asset to absorb them - either Treasury debt (the fiscal deficit channel) or private financial assets (the financialisation channel). These two are substitutes, not complements. Squeezing fiscal deficits without restraining private credit pushes the same global savings glut into asset bubbles. So US fiscal consolidation alone is not sufficient, and must be paired with financial-sector reform that prevents the likes of private credit from filling the void.

I asked Claude to generate a graphic that describes the global imbalances quartet.

So, how to address these imbalances?

The rebalancing would require global diplomacy and coordination to mobilise support from all key stakeholders. This looks onerous in a deeply polarised world, of rising tensions between the West and China and the unpredictable and whimsical nature of the Trump Presidency.

In fact, among the four adjustments required, interventions pertaining to the much-derided Euro area appear to be the most promising and likely to materialise. In fact, on investments, the train has already started.

It is possible that a deep crisis on the economic front, a very likely near to medium-term possibility in either case, may force both China and the US to rebalance towards consumption and consolidation, respectively. However, there are daunting political economy challenges to be overcome in both countries, especially the US.

It is the fourth leg that might prove the most challenging. The financial markets are where the power of entrenched interests is so strong that it might require a counter-revolution to upend the order and regulate financial markets more tightly. This will also require global coordination and collective action, and not mere reforms at the US front.

No comments:

Post a Comment