I blogged here on the emerging AI economy. This is an update on the trends in AI spending.

As the hyperscalers - Alphabet, Amazon, Meta, and Microsoft - ramp up their data centre investments to $720 bn in 2026, their age of bountiful cash flows is over. Three of them are expected to have at least a quarter of negative cash flows, and Alphabet will only just scrape above.

At around 40% of their revenues this year, the cloud giants’ capital expenditures will surpass those of the oil industry during the shale boom in the 2010s and the telecoms industry during the dotcom bubble in the 1990s… Nowadays investors judge the success of these firms on the basis of concentrated revenue contracts stretching far into the future, rather than dispersed sales received today. Mostly these contracts involve selling computing capacity to model-makers like OpenAI and Anthropic, which are themselves incinerating vast piles of cash. Total future revenue agreements have risen to $2trn, from $730bn last year, at Amazon, Google, Microsoft and Oracle (Meta is a buyer, rather than a seller, of computing capacity)…

Since the start of last year the big five have raised $260bn from bond markets, a quarter of all such borrowing by listed American non-financial firms… Nearly a third of the haul from selling bonds this year is in currencies other than the dollar… Much larger obligations lurk off-balance-sheet. The biggest are $820bn of future payments to lease data centres yet to be built, up from $270bn a year ago. Commitments to spend money on other things, like packing their data centres with chips, have risen as fast. Amazon, Google, Meta and Oracle now disclose $680bn of such obligations. Other bills are tied to special-purpose vehicles: separate entities with their own balance-sheets. Last year one assembled to build Meta’s new data-centre in Louisiana issued the biggest single corporate bond in history.

This is an interesting summary of the dynamic driving this investment boom

The five firms (hyperscalers plus Oracle) have assumed the role of central planners, attempting to make the complex chain of returns on investment work across the AI economy: data centres are useless if businesses don’t find models worth paying for, which only happens if model-makers can raise enough capital to make them. In the process, the hyperscalers have sacrificed their own returns… Big tech has also liberally lent its creditworthiness across capital markets. Many firms that contract with the giants can take those contracts to the bank (literally) and raise more debt.

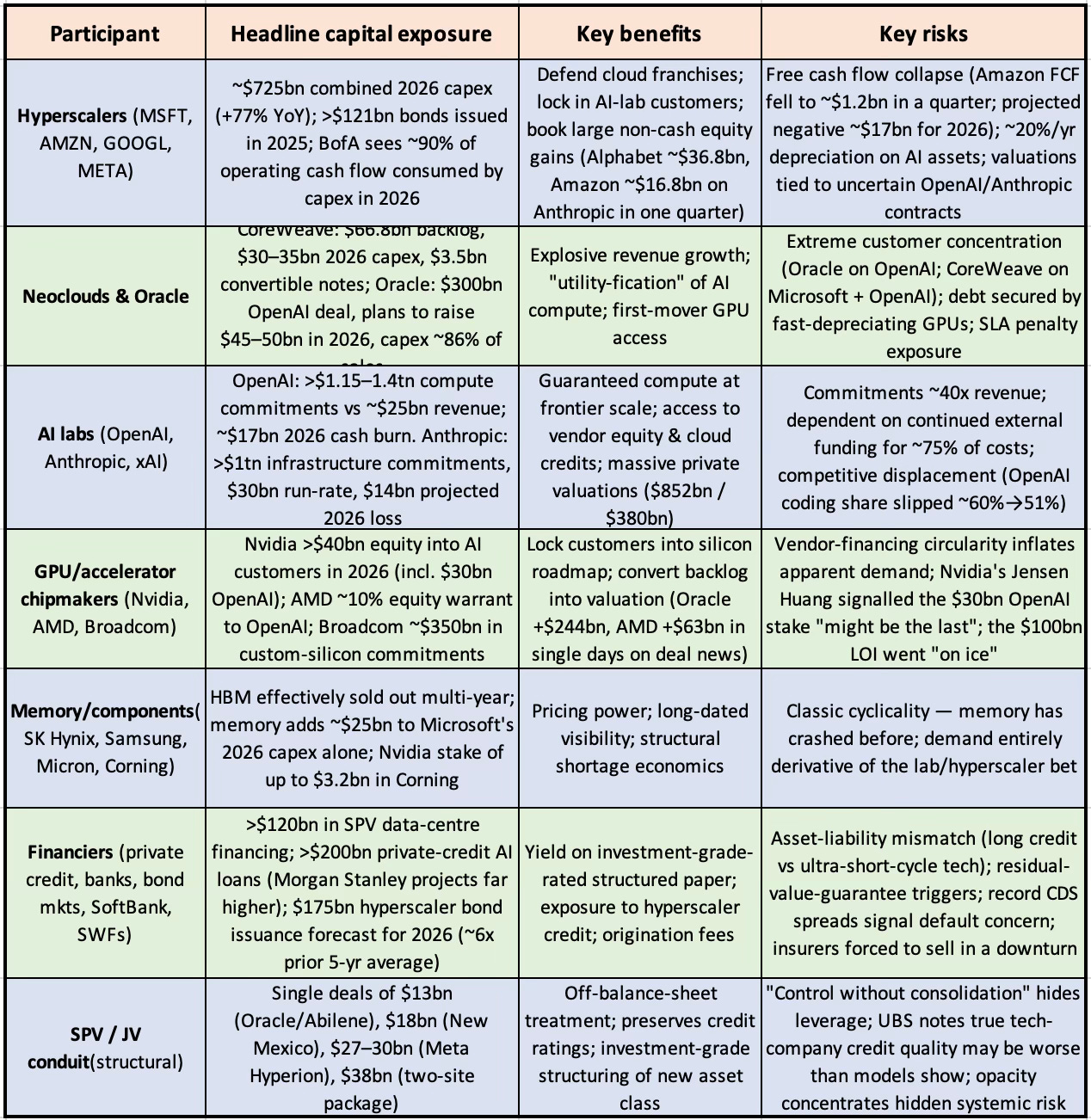

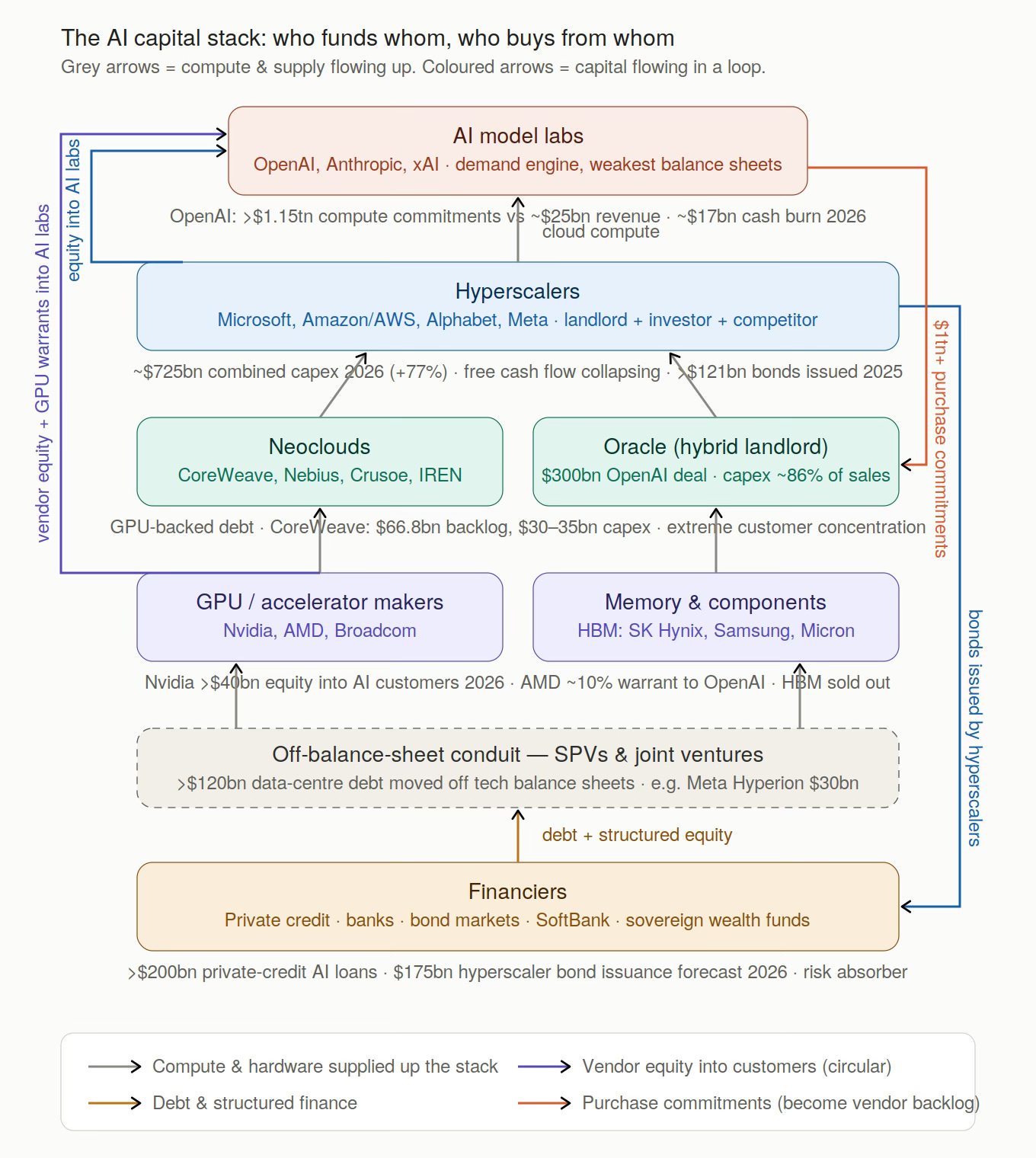

There are perhaps three overlapping risks - circular financing, vendor financing, and off-balance-sheet leverage - which are not a set of isolated deals but a single integrated capital structure spanning seven participant types.

Claude generated this comprehensive diagram that captures the linkages across these seven layers.

A chipmaker (and hyperscaler) writes an equity cheque to an AI lab (purple, up the left side), the lab converts it into a purchase commitment back to that same chipmaker and the cloud landlords (orange, down the right side), the commitment becomes backlog that supports the vendors' valuations and their bond issuance (blue), and financiers fund the whole build through SPVs and private credit (amber). Money does not exit the system; it rotates.

Three properties convert a set of bilateral deals into a self-reinforcing system. First, circularity inflates apparent demand - taking equity from vendors and using it to support further borrowing has made the boom dependent on convoluted financial engineering (echoing the 1990s, when telecom-equipment makers like Lucent and Nortel advanced money to customers to buy equipment, only to face write-offs when bankruptcies hit). Second, a single weak node is load-bearing - if OpenAI cannot meet commitments, Oracle’s revenue, CoreWeave’s backlog, Nvidia’s and AMD’s sales, and the SPV lenders’ collateral all reprice together. Third, the risk has been pushed to where it is least visible (into private credit and SPVs) while equity markets have already capitalised the optimistic case. If demand does not materialise, no amount of financing ingenuity can address it, and given the amounts involved it is certain to have very large financial-market and economy-wide impacts, cascading through the balance sheets of corporates, financiers and households.

The risks are concentrated and largely contingent — they crystallise only if AI demand disappoints, but if it does, they crystallise simultaneously across all seven categories because they share the same underlying bet. Everything rests on AI demand growing fast enough to justify >$1tn in lab commitments and ~$725bn in annual hyperscaler capex. If the revenue curve stays ahead of the cost curve, the circularity is just efficient capital allocation. If it doesn't, the same circularity becomes the risk transmission mechanism.

All this circularity is also generating its set of accounting distortions. Robin Wigglesworth points to the curious spike in the “other income” line of the hyperscaler's quarterly account statements, attributable to the changes in valuations of their investments in AI companies.

Alphabet, for example, booked $37.7bn of “other income” in just the first three months of the year, accounting for over half the company’s net income over the period. Amazon reported “other income” of nearly $16bn in the first quarter, up from $2.7bn in the same period last year. That was nearly half its overall net income for the three months. Microsoft reported “only” $942mn of other income in the first three months of the year, but this line item has now made $7.2bn over the past nine months… what constitutes “other income” in this case: the ebb and (mostly) flow in the valuations of their sizeable private investments in companies like OpenAI and Anthropic…

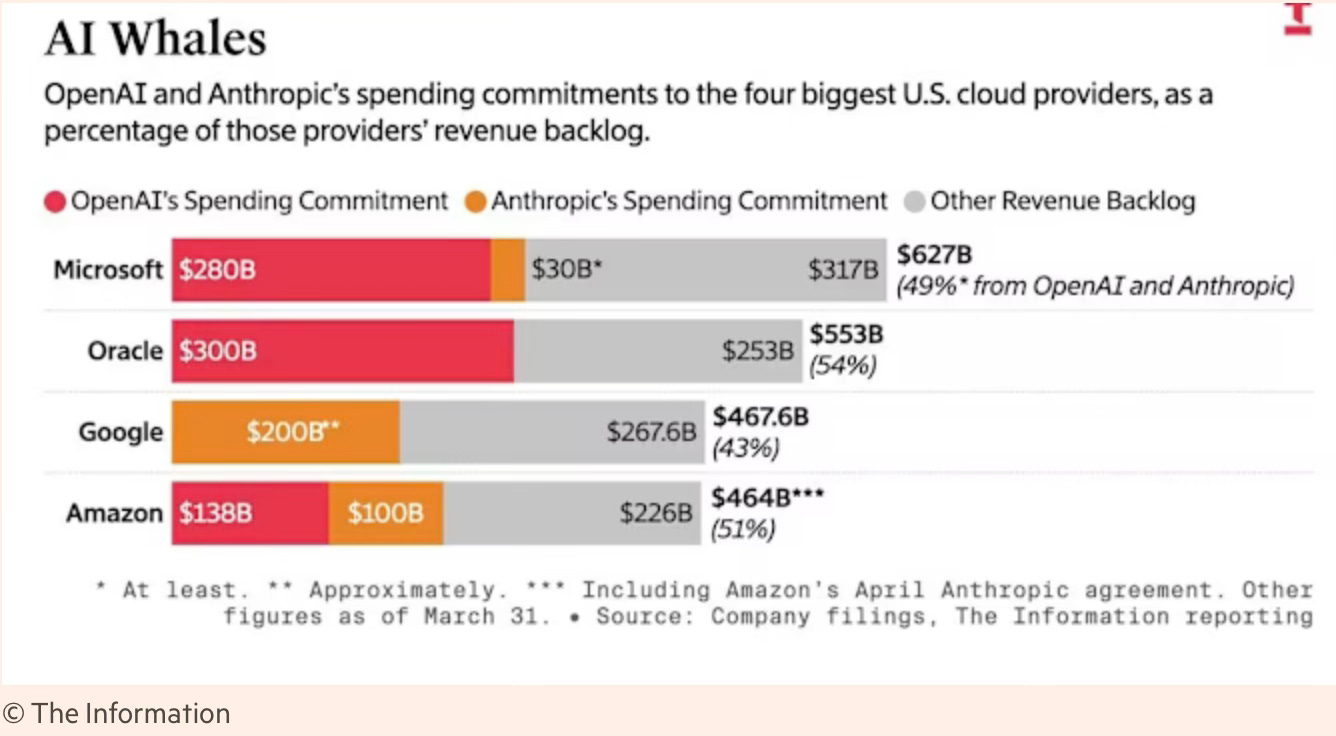

Not only have private investments and increasingly engorged funding rounds become a meaningful driver of the hyperscalers’ aggregate earnings, but the money the hyperscalers have pumped into the likes of Anthropic and OpenAI has allowed the AI companies to sign huge computing deals with Alphabet’s Google Cloud, Microsoft’s Azure and Amazon Web Services… OpenAI and Anthropic now make up about half of the entire cloud computing order books at Oracle, Alphabet, Amazon and Microsoft.

A vendor invests equity in its own customer; the customer uses that equity to pre-commit purchases from the vendor; the vendor books the purchase commitment as backlog; the backlog supports the vendor’s own valuation and borrowing.

Even though AI expenditures are building the plumbing for the next-generation economy, something is unsettling about the scale and pace of spending. More worrying is the concentration and circularity of the transactions. Is AI spending going to be the mother of all circular trade bubbles?

No comments:

Post a Comment